The content on this page has been converted from PDF to HTML format using an artificial intelligence (AI) tool as part of our ongoing efforts to improve accessibility and usability of our publications. Note:

- No human verification has been conducted of the converted content.

- While we strive for accuracy errors or omissions may exist.

- This content is provided for informational purposes only and should not be relied upon as a definitive or authoritative source.

- For the official and verified version of the publication, refer to the original PDF document.

If you identify any inaccuracies or have concerns about the content, please contact us at [email protected].

Explainer: Proportionality in UK and Ireland GAAP (June 2026)

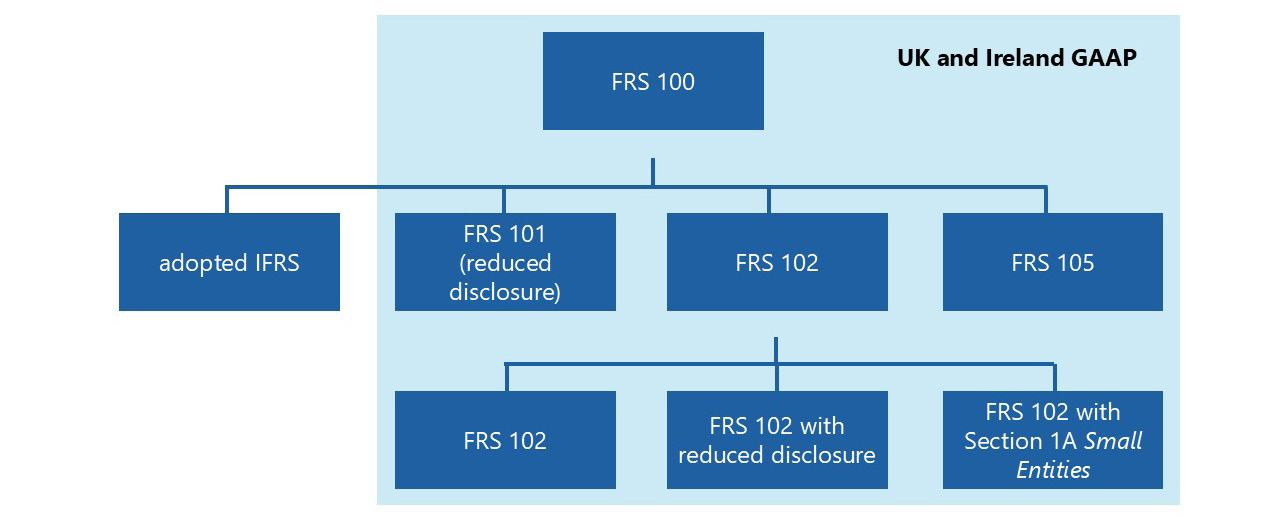

Which financial reporting frameworks are available?

To comply with company law in the UK and Ireland, company financial statements must either be prepared in accordance with IFRS Accounting Standards adopted for use in the relevant jurisdiction ('adopted IFRS'), or Financial Reporting Standards (FRSs) issued by the Financial Reporting Council (FRC) ('UK and Ireland GAAP'). Publicly-listed companies are required to apply adopted IFRS in the preparation of their group accounts but may choose between adopted IFRS and FRSs for the preparation of their individual accounts. Most other entities have a choice between the two frameworks. Refer to this link for further information on the financial reporting framework: UK Accounting Standards (overview).

Which financial reporting standards are available?

FRS 100 Application of Financial Reporting Requirements sets out the high-level requirements for the preparation of general-purpose financial statements.

The financial reporting regimes vary in how comprehensive and complex they are, in a manner correlating to the size and complexity of the entities most likely to apply them. An entity may always choose to 'opt up':

The FRC's overriding objective in developing financial reporting standards is to enable users of accounts to receive high-quality understandable financial reporting proportionate to the size and complexity of the entity and users' information needs. In achieving this objective, the FRC aims to provide succinct financial reporting standards that, amongst other things, have consistency with global accounting standards, promote efficiency within groups, and are cost-effective to apply.

The following sections discuss how the FRC achieves proportionality in each standard.

FRS 101 Reduced Disclosure Framework

FRS 101 sets out an optional reduced disclosure framework for 'qualifying entities' (within groups) that otherwise apply the requirements of adopted IFRS (subject to some amendments for compliance with company law). The standard is intended to enable cost-effective financial reporting within groups to reduce reporting burdens, particularly for groups that apply IFRS Accounting Standards in their consolidated financial statements. The FRC's decisions about disclosure reductions are based on the presumption that qualifying entities usually have few users of their financial statements, and particularly few users external to the group. Any external users are likely to be providers of credit that are interested in information about the liquidity and solvency of the qualifying entity.

FRS 102 The Financial Reporting Standard applicable in the UK and Republic of Ireland

FRS 102 is the 'main standard' in UK and Ireland GAAP. It was based originally on the IFRS for SMEs Accounting Standard, but is available to a much wider range of reporting entities (both in size and nature). Accordingly, FRS 102 is also informed by developments in 'full' IFRS Accounting Standards as the FRC seeks proportionate solutions for this broad constituency. The FRC has carefully developed FRS 102 to balance consistency with global standards, and proportionality. Recent examples include the way in which the principles of IFRS 15 Revenue from Contracts with Customers and IFRS 16 Leases were accommodated in the amendments arising from its second periodic review, effective 1 January 2026.

Qualifying entities: Like FRS 101, FRS 102 offers disclosure reductions for 'qualifying entities' within groups.

Small entities: Provisions for small entities are set out in Section 1A of FRS 102. Recognition and measurement are generally consistent with 'full' FRS 102, but presentation and disclosure requirements are simplified. In recent years, the UK and Irish governments have increased the size thresholds, making Section 1A available to more entities. Small entity financial statements are often not subject to audit.

FRS 105 The Financial Reporting Standard applicable to the Micro-entities Regime

FRS 105 is available to the very smallest reporting entities. Unlike the other standards, a preparer is not expected to ensure a 'true and fair' view – rather, compliance with the minimum requirements of company law is presumed to suffice. FRS 105 financial statements are not usually subject to audit. Although based on FRS 102, FRS 105 contains various recognition and measurement simplifications. Presentation and disclosure are also much simplified, but this is by law rather than a decision of the FRC. In recent years, the UK and Irish governments have increased the size thresholds, making FRS 105 available to more entities, although the FRC has in the past found that only about half of micro-sized entities choose to apply the micro-entities regime.

Get in touch

London office:

13th Floor,

1 Harbour Exchange Square,

London, E14 9GE

Birmingham office:

5th Floor, 3 Arena Central,

Bridge Street,

Birmingham, B1 2AX

+44 (0)20 7492 2300

www.frc.org.uk Follow us on LinkedIn