Warning

The content on this page has been converted from PDF to HTML format using an artificial intelligence (AI) tool as part of our ongoing efforts to improve accessibility and usability of our publications. Note:

- No human verification has been conducted of the converted content.

- While we strive for accuracy errors or omissions may exist.

- This content is provided for informational purposes only and should not be relied upon as a definitive or authoritative source.

- For the official and verified version of the publication, refer to the original PDF document.

If you identify any inaccuracies or have concerns about the content, please contact us at [email protected].

Risk and Viability summary slidepack

Principal Risk Reporting – Key messages

- The annual report is an important source of information for investors. Principal risk disclosures provide a basis for engagement with a company.

- The challenge for companies is getting the appropriate balance of company-specific, succinct and useful information whilst not giving away any competitive advantage.

- Investors vary in terms of how they like to see risks disclosed, although they are unanimous in their desire for company-specific information.

- Investors seek to understand both the principal risks identified by the company and how the company is managing those risks. They gain confidence in management when risks are clearly linked to the business model, show any changes in risk year on year and give some indication of the potential impact of risks occurring.

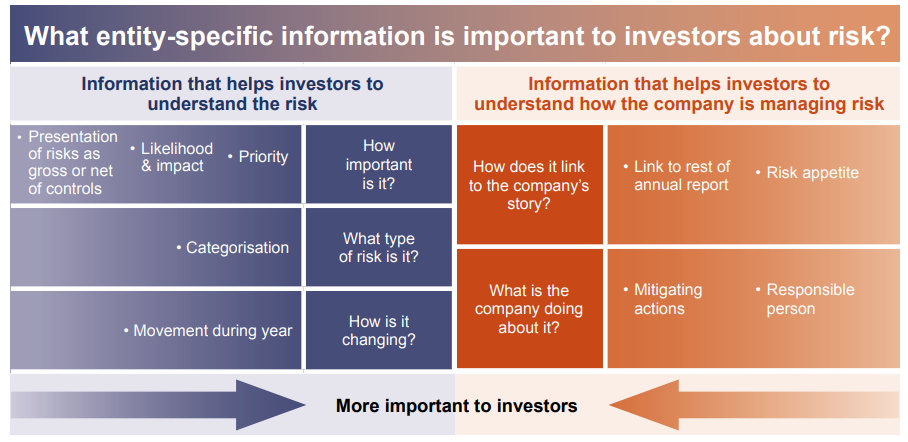

The graphic below shows how risks should be linked to other parts of the annual report.

Attributes of good principal risk disclosure

Investors gave us their views on the presentation of principal risk disclosures. From this, the Lab has compiled a list of disclosure attributes that are important to investors.

The full report includes examples of each of these attributes.

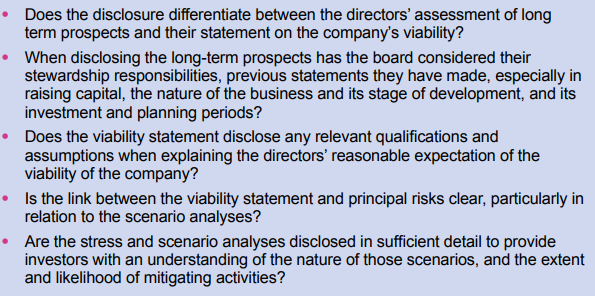

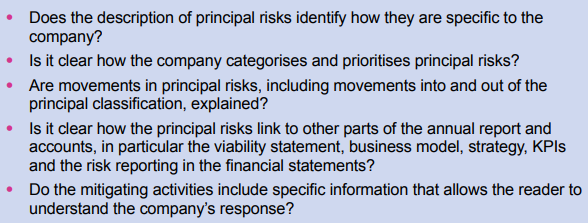

Quick questions for companies on their principal risk disclosures

Viability statement reporting – Key messages

- The introduction of the viability statement has improved board level consideration of long term sustainability and resilience to risk. Investors report that this has resulted in good discussions with companies around risk management.

- However, this is often not reflected in the disclosed viability statement.

- Investors would like companies to provide information on the sustainability of the business model and the company's resilience to risk. This goes beyond an extended going concern report which only focuses on liquidity.

- Companies could provide better discussion around the periods they have considered in their assessment of prospects, and how these have led to the chosen viability period.

- Performing stress and scenario analyses has improved decision-making and helped companies determine their risk appetite. Investors also find details of the stress or scenario analyses that have been performed very useful.

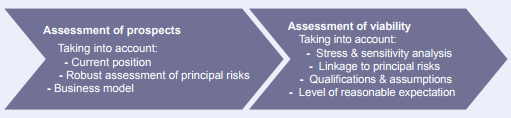

Two-stage process in developing a viability statement: assessing prospects and stating viability

- The directors should firstly consider and report on the prospects of the company taking into account its current position and principal risks. Secondly, they should state whether they have a reasonable expectation that the company will be able to continue in operation and meet its liabilities as they fall due over the period of their assessment, drawing attention to any qualifications or assumptions as necessary.

- Many investors would like more information about the risks and prospects of a company over a longer time period consistent with the company's investment and planning periods (the first stage) even if the statement (the second stage) is limited to a shorter period.

Quick questions for management on their viability statement disclosures