Annual Reports and Accounts are the foundation of decision making in the UK capital markets, supporting investment, growth and wider economic confidence. This has been true of the traditional paper report and is now true of the structured digital report where the rapid and widespread adoption of artificial intelligence has increased the importance of companies providing accessible, high-quality machine‑readable data.

Since 2021, certain companies admitted to trading on UK regulated markets, such as the London Stock Exchange (LSE), have been required to produce their annual financial report in a structured digital format (called iXBRL) under FCA rules enabling that information to be machine-readable. They must file this to the Financial Conduct Authority's (FCA) National Storage Mechanism (NSM) within four months of the year end.

Our Role

The Financial Reporting Council (FRC) plays a central role in supporting high‑quality structured digital reporting in the UK through its responsibility for developing and maintaining the UK taxonomies and reviewing the quality of digital filings. The taxonomies translate accounting standards into a consistent digital framework, enabling companies to produce machine‑readable reports that are comparable and decision‑useful. Alongside this, the FRC supports the effective implementation of structured reporting through guidance and tools, as well as ongoing engagement with preparers, software providers, and other stakeholders. This combined approach helps promote consistency, address emerging issues, and drive continuous improvement in the quality and usability of structured data across the market.

The FRC also supports the FCA in maintaining the UK Single Electronic Format (UKSEF) approach to filing (allowing one set of accounts to be filled to both the FCA and Companies House), developing tools and guidance and delivering a programme of quality reviews. This paper summarises the most common issues identified through those reviews and highlights where relatively small changes could improve the quality and usability of structured data.

Our review

Our review is based on a detailed review of 30 UK listed companies’ 2024/25 digital annual reports, market-wide analysis of digital reporting using analysis tools developed by the FRC as part of the CODEx project, and ongoing engagement with report preparers, software providers and other stakeholders. We have also directly notified companies of significant issues identified through our review to support enhancements in the quality of their reporting.

Summary of findings

Structured digital reporting (SDR) for listed companies is now well established across the UK market. Our review found that most files are well structured and comply with requirements; however, we continue to identify areas where basic checks would address quality issues, alongside more judgmental areas. Key issues included:

Findings

- Inconsistent Level of Tagging - Disclosures that cover multiple accounting topics are often not fully tagged. Companies frequently apply only a single, high‑level tag where more detailed or multiple tags are required, reducing consistency and comparability across filings.

- Accounting Meaning - Tags are sometimes selected based on label wording rather than the underlying accounting meaning. This can result in disclosures being associated with incorrect concepts, or identical figures being tagged inconsistently within the same report.

- Use of Custom Extensions - Company‑specific extensions continue to be created in situations where appropriate standard tags already exist, particularly for alternative performance measures, equity movements, and cash flow items. This fragments comparable information across the market.

- Anchoring of Extensions - While extensions are generally anchored, anchors are often overly broad or not conceptually precise. Anchoring to generic or weak concepts limits the usefulness of extensions for analysis and interpretation.

- Earnings Per Share (EPS) Scaling Errors - EPS continues to be one of the most common sources of error, typically caused by incorrect scaling (i.e. £45 rather than 45 pence).

- Website Availability and Accessibility - Some companies still fail to make their structured digital report easily available on their website, delay publication, or do not provide a viewer-friendly version. This limits access for investors and reduces the value of structured reporting for data and AI use.

- Errors and Warnings Not Addressed - Validation errors and warnings identified during preparation or filing are not always fully investigated or resolved. Ignoring warnings can indicate underlying data quality issues and reduces confidence in the structured data.

- Filing Process and Timeliness Issues - A proportion of companies continue to file late or fail to ensure that their structured report is successfully published on the National Storage Mechanism. This interrupts access to data and creates compliance risk.

- UK‑Specific Tagging Requirements Applied Inconsistently - Mandatory UK‑specific tags used to support combined FCA and Companies House filing are sometimes omitted or applied to the wrong information (for example, group tags applied to parent‑only disclosures), reducing accuracy and potentially creating future filing risks.

| Name | Structured digital reporting factsheet |

|---|---|

| Publication date | 20 May 2026 |

| Type | Information sheet |

| Format | PDF, 490.8 KB. View HTML version |

Common areas for improvement

In this section:

A key purpose of the structured digital reporting programme is to support the use of data to compare companies and inform investment decisions. Our review identified several areas where improvements would support greater consistency.

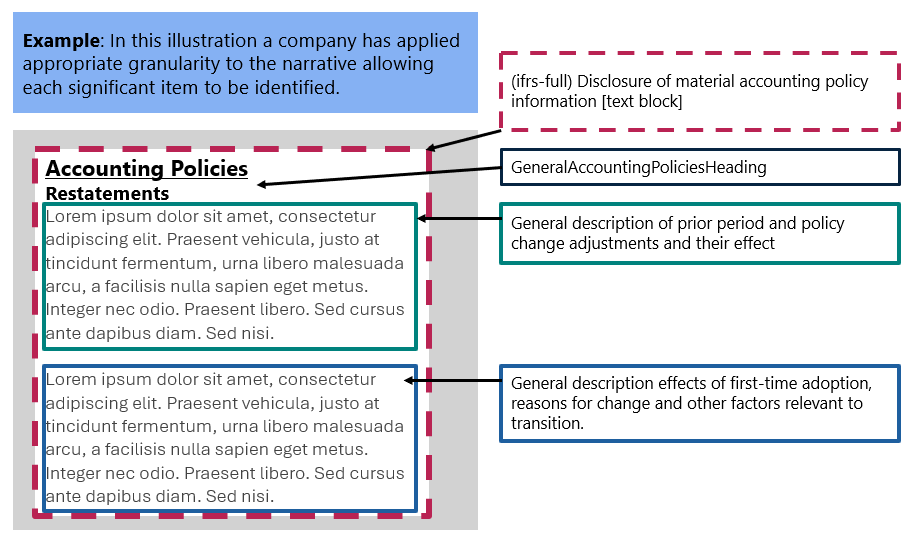

1. Inconsistent level of tagging

What is the issue: The FCA requires companies to tag detailed disclosures (accounting policies, descriptions and details) with all tags relevant to the topics they cover. This creates challenges for filers, as notes may cover more than one topic or elements related to a single topic may be spread across several notes. Where this occurs, filers should apply multiple relevant tags to a single note to reflect the nature of the disclosure; this is often called nested tagging.

This issue most commonly manifests in the following ways:

- Adjusted or operating profit – Adjustments or operating profit notes often include reconciliations and narrative that cover key movements. These are both relevant to the understanding of the adjustment/calculation and also the thematic area (e.g. Foreign Exchange). Our review noted that these additional thematic tags were often not applied and companies only applied a custom extension to the note

- Single block tagging – Tags are available across several categories, including those covering material accounting policies, thematic policies (e.g. disclosure of material accounting policy information, description of other policies relevant to understanding the financial statements, and accounting policies for foreign currency translation), and individual disclosures (e.g. revenue disclosures and disclosures of operating segments). In many cases, disclosures require more than one tag. For example, revenue-related disclosures may require both a description of the accounting policy for revenue recognition and disclosure of revenue from contracts with customers. Similarly, foreign exchange disclosures may require tags for both foreign exchange and hyperinflation, while financial instrument disclosures may require tags for derivative financial instruments as well as fair value disclosures. However, we observed instances where only a top-level or a single tag had been applied.

Why it matters: When users consume data, they will be looking for specific tags and disclosures. If these are not expansively and consistently tagged then they may not consume all the relevant information.

What can you do: The FCA provide a list of mandatory tags that filers can use to support their review. Whilst this list is extensive, we recommend that filers ensure that policies and disclosures relating to significant and material are fully tagged to support investors’ use.

Example of granular tagging

2. Accounting meaning

What is the issue: Tagging should accurately reflect the nature, substance, and purpose of the underlying accounting information. A recurring issue arises where selected tags do not faithfully represent the accounting meaning of a disclosure. Instead, tags may be chosen based on superficial similarities or applied inconsistently within the same report, reducing both accuracy and comparability.

This issue most commonly manifests in the following ways:

Label‑driven tag selection

Tags are selected based on similarities in label wording rather than alignment with the correct accounting concept. For example:

- The tag “Cash and cash equivalents if different from statement of financial position” is applied even though the disclosed balance fully agrees with the statement of financial position.

- A Remuneration Committee Report is tagged using “Disclosure of employee benefits”, despite the narrative content extending beyond employee benefit disclosures and not representing an accounting note.

Inconsistent or inappropriate classification of assets

Assets with different accounting characteristics are grouped under incorrect tags. For instance, Goodwill and other intangible assets are incorrectly tagged using “Intangible assets other than goodwill”, resulting in a mismatch between the tag definition and the reported balances.

Inconsistent tagging of identical figures

The same numeric disclosure is associated with different tags when it appears in multiple locations within the report, creating internal inconsistency and undermining data usability.

Why it matters: Even when the reported amounts themselves are correct, the use of incorrect or inconsistent tags can cause users to extract the wrong accounting concept. This undermines confidence in structured data, reduces comparability, and can lead to inaccurate analysis or interpretation.

What you can do: Choose tags by accounting definition and context, not just label wording. Apply each tag consistently to all instances of the same concept and review repeated figures to confirm alignment throughout the report.

3. Extensions

What is the issue: The FCA rules are flexible, allowing companies to reflect the nature of their reporting by creating company-specific tags called extensions. However, we have observed examples where filers have created extensions despite the availability of an appropriate standard tag.

This is most observed in:

Alternative performance measures and adjusting items

Extensions are frequently created for measures or adjustments where suitable standard elements already exist. For example, a bespoke Management fees extension is used instead of the standard Portfolio and other management fee income tag, notwithstanding close alignment in accounting meaning.

Equity movements

Within statements of changes in equity, similar movements are often tagged using bespoke elements rather than standardised ones, reducing comparability. For instance:

- An extension is created for Transfers in respect of share options, even though the standard tag Exercise options increase in equity could have been appropriately applied.

- Extensions are used for Transactions with non‑controlling interests where a standard anchored IFRS tag combined with an appropriate dimension would have provided a clearer and more consistent representation. By extending instead, the structure of the equity analysis column is weakened.

Asset classification and cash flow–related disclosures

Custom tags are applied even where existing standard tags would be suitable. For example:

- Property, plant and equipment is extended to Property, plant and equipment other than capital work in progress, despite Construction in progress already being separately tagged, meaning the standard Property, plant and equipment element could have been used without loss of information.

- More broadly, bespoke tags are applied to cash flow and related line items even where appropriate standard IFRS tags are available.

Why it matters: The unnecessary use of extensions reduces comparability across companies by fragmenting similar disclosures into multiple bespoke concepts. This increases complexity for data users and makes automated analysis more difficult, limiting the overall usefulness of structured data.

What you can do: Companies should focus on the use of standard tags where an appropriate element exists and challenge those undertaking the tagging around the need for extensions, particularly in frequently reported areas such as cash flows and equity movements. Extensions should be used only where a disclosure cannot be represented using existing taxonomy concepts, with a documented rationale.

4. Anchoring

What is the issue: To support usability, SDR relies on anchoring, whereby extension elements are linked to relevant IFRS taxonomy elements to aid interpretation and analysis. Our review indicates that, where extensions are used, companies generally comply with the technical requirement to anchor them to standard IFRS tags. However, the anchors selected do not always represent the closest, most specific, or most informative accounting concept. As a result, the analytical value of the tagged data is reduced for users. This issue most commonly arises in the following ways:

- Anchoring to overly broad concepts - Extensions are frequently anchored to high-level or generic IFRS elements rather than to a more specific or narrower concept that better reflects the underlying disclosure. In some cases, the most relevant or material component within a breakdown is not anchored at all, despite a suitable narrower standard element being available.

- Conceptually weak anchoring despite technical compliance. Although anchors often meet minimum regulatory and technical requirements, they are not always conceptually appropriate or sufficiently precise. In some cases, disclosures relating to non‑current assets are anchored to current asset concepts, creating a clear mismatch between the accounting nature of the item and the anchor used. More broadly, anchors may be selected that are overly generic or only loosely related to the underlying disclosure.

Why it matters: When extensions are anchored only to broad or non‑specific concepts, users struggle to interpret their meaning. This reduces the usefulness of structured data, limits analytical insight, and diminishes confidence in the ability of anchoring to convey the underlying accounting substance.

What you can do: When using extensions, companies can ensure they are anchored to the closest and most informative standard concept available, rather than defaulting to high‑level tags. Anchoring decisions should be guided by accounting meaning rather than technical convenience, with particular care taken in complex areas such as cash flows and equity movements.

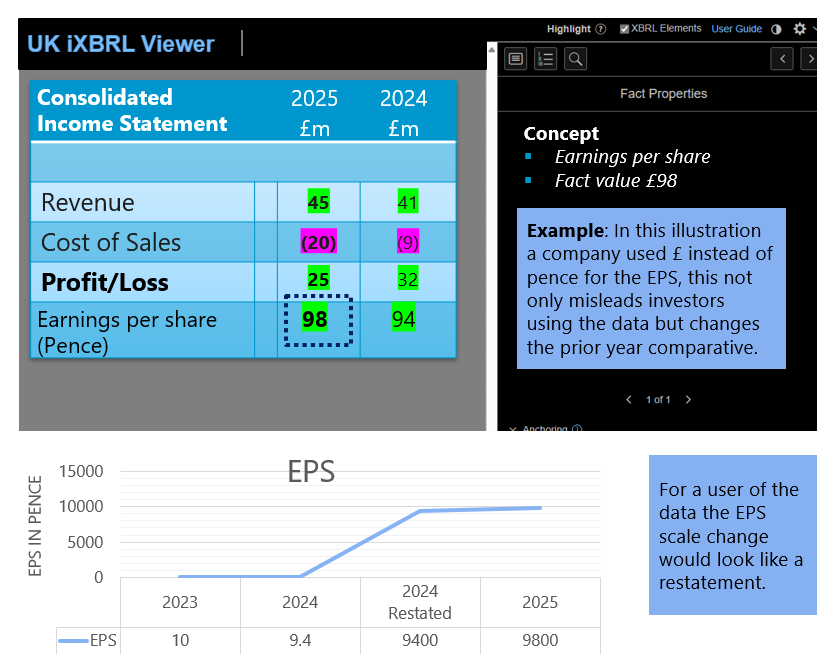

5. Earnings Per Share

What is the issue: Errors affecting earnings per share (EPS) continue to occur more frequently than expected, given the prominence and widespread use of this measure by investors. These errors are usually caused by an incorrect scale being applied.

These issues typically arise where EPS is treated in the same way as other numeric disclosures within a table, for example, being scaled to thousands or millions despite EPS usually being presented in pence or cents.

Why it matters: Incorrect scaling can materially distort EPS values in structured data, even where the rendered report appears correct.

While the value shown to readers may appear correct in the report, the resulting structured data can become implausible when extracted and analysed.

What you can do: The FRC wrote to a number of companies highlighting issues with these metrics. To avoid such issues, filers should address common causes including:

- Uniform scaling applied across tables - The same scale is applied to all figures in a table without appropriate adjustment for per‑share measures.

- Limited visibility during preparation and review - EPS scaling errors are often not immediately apparent and can be easily overlooked during tagging and review processes. Therefore undertake a detailed review of the data that the tagging produces to identify obvious errors.

Example of EPS scaling error

6. Website Availability

What is the issue: Our implementation work on structured digital reporting noted that placing a copy of the iXBRL report on a filer’s website (preferably with a viewer) is good practice. Our review noted that some companies are failing to do this.

Why it matters: Structured digital reporting can improve access to decision‑useful data for professional and retail investors. Where data is difficult to access or use, the value of reporting is reduced. FRC research in 2023 indicated that institutional investors were accessing iXBRL reports via filers’ websites. AI tools also increasingly rely on the XHTML version of reports. Providing a copy of the structured digital report in the investor section of a filer’s website supports access and re‑use.

What you can do: Most tagging tools support packaging iXBRL files with a viewer. Open-source tools can also be used to produce a viewer file, which should be compatible with most filer websites. If filers want their report to be fully accessible to large language models, they may also want to place the XHTML file (the human-readable report) directly within their website (rather than only within a ZIP file).

7. Errors and Warnings

What is the issue: XBRL (which underpins structured digital reports) supports data quality through validations. Validations are designed to identify technical issues with the file, items within the file that might be unusually structured, don’t add up or may indicate missing mandatory tags. Validations typically occur both within tagging software and at the receiver’s portal and reviewing any errors or warnings should form part of a filer’s review process. Our review identified files where warnings indicated substantive issues that did not appear to have been remediated.

Why is it important: The validation process is designed to support data quality. Errors which are not fixed may lead to the file being rejected by the NSM, and ignored warnings impact the ability of data users to use the data.

What you can do: We recognise that some software used by filers for tagging may not produce clear explanations for errors and warnings (although many do). However, we recommend ensuring that sufficient time exists in the process to follow up any issues with your vendor or tagging agent.

8. Filing process and timeliness

What is the issue: We noted that around 10% of companies filed their structured reports late this year, and that a number of companies did not have a file on record at the National Storage Mechanism (NSM).

While we and the FCA followed up with individual companies where files were missing, companies should ensure that filing processes operate effectively.

Why is it important: These are process failures rather than tagging capability issues, and they interrupt the availability of structured data to users and regulators and create non-compliance risk for filers.

What can you do: Our discussion with some of the impacted filers identified that the report had often been produced but failed FCA validation during the filing process. We recommend that companies build into their process a post submission check of the FCA’s National Storage Mechanism website to see if your filing has been published by the FCA to ensure that the annual report is available and is displaying as expected.

How long it takes companies to file digital reports at the FCA

| Months | Filings |

|---|---|

| <2 | 29 |

| 2-3 | 204 |

| 3-4 | 253 |

| 4-5 | 57 |

| 5-6 | 20 |

| 6+ | 35 |

9. UK-specific tagging requirements applied inconsistently

What is the issue: In 2022, the FRC introduced an approach that allows filers to use a single file to meet both FCA and Companies House filing requirements. This approach can reduce burden and support timely filing at Companies House. It requires certain mandatory information to be tagged within the report; some relate to the whole group and some only to the parent entity. Our review noted cases where filers applied these tags to the wrong information (for example, applying a group tag to parent‑only information) or omitting some elements.

Why it matters: Inconsistent or inaccurate application of required tags can affect users of the data and, while not currently part of Companies House validation, may lead to files being rejected in future.

What you can do: The FRC provides specific guidance on the mandatory tags for UKSEF. Companies can use this to support their review.

Conclusion

Structured reporting is now an ongoing quality discipline rather than just implementation. Filing risks are low, but inconsistent tagging threatens data quality and trust—especially with increased AI use. High-quality structured data delivers clear value to users. Investors, analysts, regulators and AI tools depend on accurate, consistent tagging to compare performance and extract insights efficiently. Where tagging is incomplete or misaligned, it reduces comparability and increases the risk of misinterpretation; where it is done well, it enhances transparency and confidence in the market.

Looking ahead, two priorities stand out. First, a stronger focus on quality and judgement—ensuring tags reflect the underlying accounting meaning, supported by robust review and clear ownership. Second, improving accessibility and usability—through timely filing and making structured reports easily available in formats that support user and AI consumption.

Together, these steps will help ensure structured reporting delivers reliable, decision‑useful data and continues to support effective capital markets.