Understanding the UK Taxonomy Suite

In our previous section we discussed why it was important to understand the underlying requirements that drive digital reporting. The requirements for the mandate will determine which taxonomies are applicable for your reporting. In the UK the FRC support digital reporting that provides taxonomies which support the UK Companies House, HMRC and the Charity Commission filing programs.

For listed Companies the allowed taxonomies are covered in FCA guidelines.

This section:

- Explains how digital reporting works by showing how taxonomy tags are used to give meaning and structure to financial and narrative information.

- Describes how tags, hierarchies and dimensions are applied in practice so reported information can be consistently prepared, understood and analysed.

A good analogy for digital reporting is using a dictionary. The taxonomy provides the term with a definition derived from standards or legislation, and the preparer provides a value to map to it. This is easy to apply to quantitive/financial reporting (i.e. Revenue can be clearly represented as a number with a unit/currency and a date period) but is more complex for qualitative/narrative reporting where there might be a lot of variety in how preparers choose to report or where material narrative information appears spread out in different sections of the report.

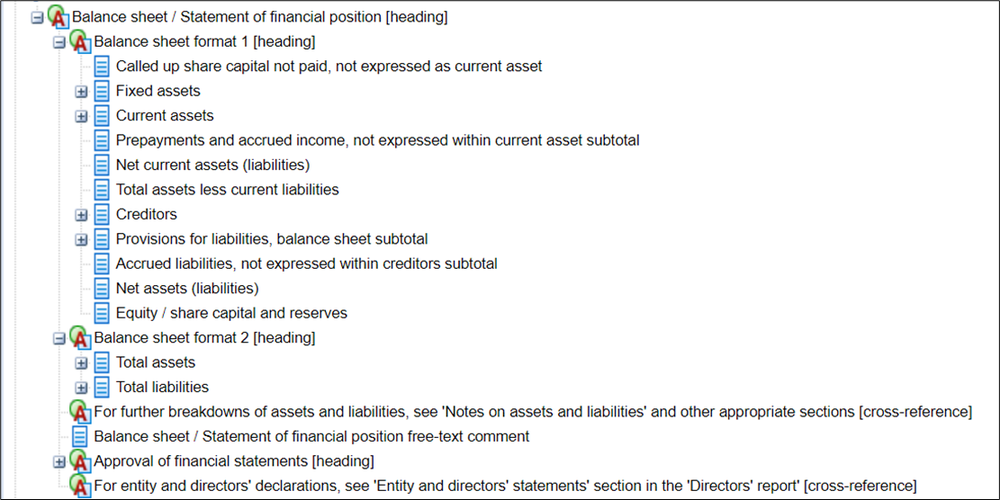

Preparers of digital reports must understand the accounting or other regulatory meaning of the information they are trying to tag using the concepts defined in the taxonomy. They then need to use specialist software to add the tag to the disclosure. Tagging may be manual (i.e. click and drag in the report to highlight the relevant text or number, and then to drag a tag from the taxonomy to it) or automated, depending on the software used. Preparers must use the tags that are available in the UK Taxonomy Suite to tag UK-specific information required by UK regulators. Tags are presented in a hierarchy with more detailed tags appearing below major ones. For example, the tags available for the Balance Sheet are in the 222 - Balance sheet/Statement of financial position folder. The image below shows that all of the balance sheet tags come under the Balance sheet / Statement of financial position [heading] tag (i.e. they are all children of the parent heading tag).

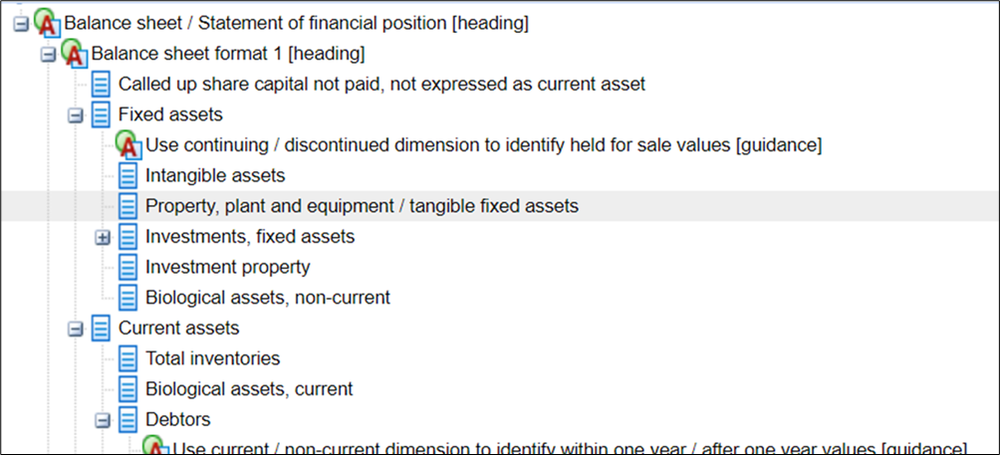

Some of these concepts can be expanded (note the +/- sign next to some of the tags, for example Fixed assets). This demonstrates the logical separation of related concepts, allows for granular reporting, and shows the relationship of concepts in the hierarchy. For example, Fixed assets and Current Assets are children of Balance sheet format 1 and Property, Plant and Equipment is a child of Fixed assets.

Taxonomies use “dimensions” to give more granularity to line item disclosures without requiring new line item tags to be added to the taxonomy for every eventuality. They are similar to dropdown menus with options to add essential detail. Most people will come across this while using an online shop. For example, when purchasing shoes, you might see options like size and colour that you need to select to fully describe what you intend to order; there is a difference between “a shoe” and “a red shoe in size 8”.

For a financial modelling perspective, dimensions should be thought of as identifying the different columns in a table of information, while ordinary line item tags represent the rows. For example, Revenue could be the line item/row and there could be columns that show a breakdown by country. Although every number on the row would be tagged with Revenue, each individual number would have its own country dimension tag applied (e.g. Revenue/UK, Revenue/USA, Revenue/France, Revenue/China).

Although this is a simple, pragmatic example, taxonomies principally use dimensions to capture the nuance of complex disclosures. In addition to dimensions, there are range of types of tags that help to capture the meaning and granularity of disclosures for the purpose of preparing, consuming and using the data. A full description of these is beyond the scope of this resource centre; readers are referred to the guidance available on the FRC taxonomies website for more information.