The content on this page has been converted from PDF to HTML format using an artificial intelligence (AI) tool as part of our ongoing efforts to improve accessibility and usability of our publications. Note:

- No human verification has been conducted of the converted content.

- While we strive for accuracy errors or omissions may exist.

- This content is provided for informational purposes only and should not be relied upon as a definitive or authoritative source.

- For the official and verified version of the publication, refer to the original PDF document.

If you identify any inaccuracies or have concerns about the content, please contact us at [email protected].

TAC Public Meeting June 2026 Paper 3b: Proposed amendments to SASB Standards - Phase 1 Part 2 - Stakeholder feedback summary

Executive summary

| Date | 16 June 2026 |

| Paper reference | 2026-TAC-016 |

| Project | Proposed amendments to SASB Standards – Phase 1 Part 2 |

| Topic | Stakeholder feedback summary |

| Objective of the paper | This paper summarises outreach activities and stakeholder feedback in relation to the ISSB's March 2026 Exposure Draft: Proposed Amendments to the SASB Standards and IFRS S2 Industry-based Guidance (SASB/ED/2026/1). |

Decisions for the TAC

There are no decisions for the TAC, but please share any comments on the general themes and specific points raised by stakeholder in relation to the SASB Standards for:

- Agricultural Products (FB-AG);

- Meat, Poultry & Dairy (FB-MP); and

- Electric Utilities & Power Generators (IF-EU).

Appendices

- Appendix 1: Electric Utilities & Power Generators stakeholder feedback

- Appendix 2: Meat, Poultry & Dairy stakeholder feedback

This paper has been prepared by the Secretariat for the UK Sustainability Disclosure Technical Advisory Committee (TAC) to discuss in a public meeting. This paper does not represent the views of the TAC or any individual TAC member.

Context

1The ISSB published the SASB Standards Exposure Draft (ED): Proposed Amendments to the SASB Standards and IFRS S2 Industry-based Guidance (SASB/ED/2026/1) in March 2026.

2The SASB/ED/2026/1 continues Phase 1 of the ISSB's project on Enhancing the SASB Standards and sets out proposed amendments to three SASB Standards: Agricultural Products (FB-AG), Meat, Poultry & Dairy (FB-MP), and Electric Utilities & Power Generators (IF-EU).

3The TAC Secretariat conducted stakeholder outreach activities to obtain feedback from relevant stakeholders about the proposed changes to the three standards, but also to gain a better understanding of how the SASB Standards are currently being used and whether this is likely to change with the implementation of UK Sustainability Reporting Standards (UK SRS).

Summary of outreach activities

4Outreach activities conducted consisted of:

- Bilateral interviews with 6 preparers.

- A stakeholder roundtable on 11 May 2026 which included 11 preparers (10 current SASB reporters and one prospective adopter) and one investor.

Bilateral interviews

5Bilateral interviews with preparers focused on the detailed aspects of the proposed amendment, including disclosure topics, metrics and technical protocols. They also captured views on preparers' broader approach to sustainability reporting, including the identification of risks and opportunities and the role of SASB Standards in that process.

6One additional bilateral interview with an investor, covering all three SASB Standards for this consultation, is scheduled for end of June and has not been included in this summary.

Stakeholder roundtable

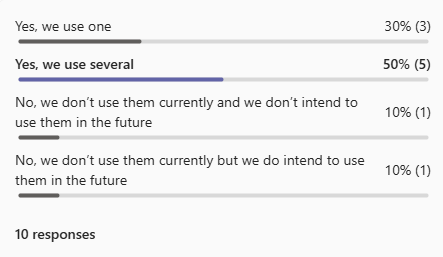

7The stakeholder roundtable held on 11 May 2026 was on the ‘Role of SASB Standards in UK sustainability reporting'. Two polls were used to understand if and how the participants use the SASB Standards. The two polls, including the responses, are detailed below.

- Question 1: Do you currently use the SASB Standards?

- Question 2: Do you currently use SASB Standards alongside other sustainability-related standards and frameworks and, if you do, which standards and frameworks do you use?

8The roundtable discussions focused on general views on the role of the SASB Standards and their usefulness. We asked the following questions:

- How are the SASB Standards currently being used?

- How are they expected to be used to comply with UK SRS?

- What could improve their usefulness for the UK market?

9The roundtable discussions also considered the broader themes already discussed by the TAC, including the role of the SASB Standards in the IFRS literature and how the SASB Standards are currently structured. The TAC has already agreed to include these themes in its consultation response, but this roundtable provided an opportunity to test the TAC's views with other market participants.

Stakeholder feedback

General themes

10A number of stakeholders commented on the value of the SASB Standards and on industry specific guidance. Preparers gave examples of how the SASB Standards supports the identification of sustainability-related risks and opportunities and related disclosures. However, preparers also noted that the SASB Standards in some cases do not necessarily connect to sustainability-related risks and opportunities that could have current and anticipated financial effects on the entity's prospects.

11A few stakeholders stressed the importance of clarity around the role of the SASB Standards in the context of the UK SRS. A stakeholder noted that there was still confusion about the status of the SASB Standards in the IFRS literature and welcomed the amendment in UK SRS as clarifying their position as guidance.

12Some preparers noted that a key reason for using the SASB Standards was to provide standardised data for ESG ratings. One preparer noted that the ratings were linked to the entity's transparency, i.e. the number of metrics it disclosed, and it was therefore better to disclose a greater number of metrics. However, preparers also agreed that they were comfortable not disclosing all of the metrics and that their disclosures aimed to focus on material information for investors.

13Preparers noted that certain SASB metrics were still US-centric despite the ISSB's previous work to enhance their international applicability. Preparers also noted that there was duplication between the SASB Standards and the ISSB Standards. However, a preparer also commented that the SASB Standards were relatively streamlined compared with the GRI Standards and that the SASB Standards disclosure topics and related metrics were generally material.

14One preparer commented that there were differences in interpretation between entities using the SASB Standards, resulting in differences in disclosures. Another preparer in the bilateral interviews commented that the issue around differences in interpretation between entities using the SASB Standards was exacerbated by a trend in the proposed amendments moving from quantitative to qualitative metrics, flagging that definitions and guidance would be required to support comparability. A few preparers in the bilateral interviews also commented on difficulties with benchmarking SASB Standards disclosures due to the lack of widespread use of the SASB Standards by similar entities.

15A preparer stressed the importance of interoperability and alignment across standards and frameworks, flagging the difficulty caused by similar, but not identical, disclosures. One preparer noted the challenges of using the SASB Standards across multiple jurisdictions (for example, differing definitions of what is considered to be waste). Another preparer noted the challenges of the divergence in reporting requirements across different jurisdictions.

16A number of preparers commented that their SASB Standards disclosures were standalone, but with cross-references to the relevant disclosures in their annual report. They also indicated that their disclosures would evolve over the next few years with UK SRS, as well as reporting under the EU's Corporate Sustainability Reporting Directive (CSRD). One preparer commented that it would not make sense for them to continue using the SASB Standards with CSRD reporting due to the overlap between the standards and as the SASB Standards are voluntary and CSRD reporting is mandatory. Other preparers commented that they expected to refer to the SASB Standards to support them with identifying appropriate disclosures for UK SRS and CSRD reporting.

Specific points

Agricultural Products

18No specific stakeholder feedback was obtained for this SASB Standard due to its limited adoption in the UK.

Electric Utilities & Power Generators

19Bilateral interviews were conducted with five preparers operating across the electricity value chain, including generation, transmission and distribution, vertically integrated operations, retail and service provision (smart metering and energy storage).

20Stakeholder engagement on the Electric Utilities & Power Generators Standard indicates broad support for the proposed amendments. Respondents confirmed that several of the proposed new metrics including those relating to capital strategy, ecological impacts, community relations, supply chain management; and employee recruitment and retention are relevant to the sector. Climate-related disclosures were noted to be largely aligned with existing reporting under TCFD. Stakeholders also welcomed the expansion of the Critical Incident Risk Management disclosure topic beyond nuclear operations, as well as revisions to the Workforce Health & Safety metrics.

21Stakeholders identified several areas where further consideration by the ISSB would be beneficial. These include:

- differences in reporting methodologies between UK and US operators, with UK entities applying frameworks that differ from the Standard's approach, for example in the calculation of the system average interruption duration index;

- the need for guidance on what constitutes a ‘vulnerable' asset for the purposes of the physical risk exposure metric, given that in some countries all assets could be considered vulnerable by virtue of their location;

- concerns regarding the commercial sensitivity of disclosing generation asset availability factors for certain generation assets in competitive electricity wholesale markets;

- the omission of biomass as a named energy source within the industry description; and

- the need for greater clarity regarding the treatment of import-dependent utilities that source the majority of their supply via interconnector cables rather than owned generation assets;

22Detailed responses on the disclosure topics, metrics and technical protocols are set out in the table in Appendix 1.

Meat, Poultry & Dairy

23Stakeholder engagement included a bilateral interview with a UK-listed company operating a vertically integrated pork and poultry business. This business spans pig and poultry breeding, rearing and finishing, supported by in-house feed milling and genetics, as well as downstream manufacturing.

24Feedback received indicates that the proposed amendments are broadly considered appropriate, including support for revisions to the Animal Health Care & Welfare topic, its renaming (from Animal Welfare) and the introduction of a third-party certification metrics.

25A consistent observation across multiple topics was concern regarding the shift in the Exposure Draft from quantitative and comparable metrics towards more qualitative, narrative-based disclosures. The stakeholder noted that this may contribute to increased length in annual reports at a time when preparers are seeking opportunities to streamline reporting and reduce length.

26Additional areas highlighted include:

- the limited applicability of the deforestation-free direct farming metric for UK pork and poultry producers, where deforestation risk primarily arises within the feed supply chain; and

- the view that disclosures relating to labour conditions management processes are overly generic for inclusion within a sector-specific standard.

27Detailed feedback on disclosure topics and metrics for Meat, Poultry & Dairy is summarised in Appendix 2.

Appendix 1: Electric Utilities & Power Generators stakeholder feedback

This table summarises stakeholder feedback received during the TAC Secretariat's outreach and does not constitute a complete extract of all proposed amendments in SASB/ED/2026/1 for the Electric Utilities & Power Generators Standard. Topics and metrics for which no stakeholder feedback was received are not reflected in the table. For reference, the following amendments proposed in the Exposure Draft are not covered in this table:

- Activity metrics: Revisions to activity metric IF-EU-000.D and addition of two new workforce composition activity metrics.

- GHG Emissions & Energy Resource Planning: Deletion of IF-EU-110a.3 (coal combustion products impoundment volumes).

- Hazardous Waste Management (renamed from Coal Ash Management): Deletion of old coal ash metrics IF-EU-150a.1 and IF-EU-150a.3; retention of surface impoundment metric IF-EU-150a.2; addition of hazardous waste incidents metric IF-EU-150a.5.

- Ecological Impacts (new topic): Addition of IF-EU-160a.3 (description of environmental management policies for operational facilities).

- Energy Affordability: Deletion of IF-EU-240a.1 (typical residential bill), IF-EU-240a.3 (disconnection rate) and IF-EU-240a.4 (external affordability factors discussion); retention of IF-EU-240a.2 (typical customer bills by category).

- Demand-side Management (renamed from End-Use Efficiency & Demand): Deletion of IF-EU-420a.2 and IF-EU-420a.3 (old demand-side efficiency metrics)

| Disclosure topic | Metric code, description and nature of change | Stakeholder feedback summary |

|---|---|---|

| GHG Emissions & Energy Resource Planning [RETAINED TOPIC] | [REVISED] IF-EU-110a.1 (1) Gross Scope 1 GHG emissions; & (2) % subject to emissions-limiting regulations; | A FTSE 100 Transmission & Distribution Lines (T&D) operator and integrated utilities entity confirms it reports Scope 1 emissions and views this as a core, established metric. The entity notes SF6 (sulphur hexafluoride) is an important Scope 1 emissions source for T&D operators, tracked separately for Ofgem reporting purposes. However, given its predominantly transmission and distribution business model, generation-related GHG emissions metrics carry less operational relevance than for integrated generators. An operator of dispatchable low-carbon generation assets, including bioenergy-based capacity welcomes the Scope 1 requirement noting they have already been reporting this under TCFD and SECR. They highlighted the absence of any explicit reference to bioenergy in the industry description, noting that the standard lists coal, gas, nuclear, hydro, solar and wind but omits this generation source despite its significance. |

| GHG Emissions & Energy Resource Planning [RETAINED TOPIC] | [REVISED] IF-EU-110a.2 GHG emissions associated with (1) T&D losses and (2) net electricity purchased (Scope 3 Category 3 – newly added) | A major UK electricity retailer notes Scope 1 is of limited relevance for a primarily electricity retail business, but is relevant for its small gas plants, heat networks and biomass plants. Confirms these would fall under Scope 1 and that reporting is already established under existing UK rules. A small island integrated electricity operator confirms Scope 1 is minimal for its operations, consisting mainly of fuel for company vehicles and refrigerant gases, given the large majority of its electricity supply is sourced through interconnector subsea cables from an overseas low-carbon generator. A FTSE 100 T&D operator and integrated utilities entity notes that it currently reports transmission and distribution losses as Scope 2. It however notes metric IF-EU-110a.2 seems to require such emissions under Scope 3 and not clear of rationale for such proposal. A major UK electricity retailer strongly supports the inclusion of Scope 3, particularly Category 11 (use of sold products), as a significant disclosure for electricity retailers. It notes Scope 3 for electricity sold is straightforward to compute using published carbon factors. An operator of dispatchable low-carbon generation assets strongly supports Scope 3 requirements, noting that working with supply chains on decarbonisation is a global sustainability imperative. A small island integrated electricity operator treats its imported electricity as Scope 3, on the basis that it is purchased for resale rather than direct consumption. |

| GHG Emissions & Energy Resource Planning [RETAINED TOPIC] | [NEW] IF-EU-110a.4 Installed capacity (MW) disaggregated by (1) major energy source and (2) energy storage | An operator of dispatchable low-carbon generation assets, including bioenergy-based capacity, confirms it already discloses installed capacity disaggregated by energy source and also discloses renewable versus non-renewable percentage in its reporting. The stakeholder does not see sensitivity in disclosing this further. The stakeholder also notes that the ED does not mention biomass as an energy source in the installed capacity context. A FTSE 100 T&D operator and integrated utilities entity notes that for a predominantly network business, connections of new renewable capacity is the operationally relevant metric rather than installed generation capacity. A small island integrated electricity operator confirms it would treat contracted import capacity via subsea interconnector cables as the functional proxy for installed generation capacity. Notes that the standard's metric was not designed with import-dominant utilities in mind. A smart metering and battery storage company supports the proposed disclosure as indicative of supporting the energy transition. The stakeholder notes that its installed capacity would be its battery infrastructure. |

| GHG Emissions & Energy Resource Planning [RETAINED TOPIC] | [NEW] IF-EU-110a.5 Planned capacity (MW) disaggregated by (1) major energy source and (2) energy storage | An operator of dispatchable low-carbon generation assets notes that capital deployment at board level is significantly influenced by climate transition, with renewable investment driving strategic decisions. The stakeholder views that the planned capacity metric is sensible and consistent with the entity's capital planning. |

| GHG Emissions & Energy Resource Planning [RETAINED TOPIC] | [NEW] IF-EU-110a.6 Description of how climate-related transition risks and opportunities influence capital strategy and investments | A small island integrated electricity operator confirms it already produces climate-related transition risk and opportunity disclosures aligned to TCFD in its annual report, including scenario analysis. It notes the entity has a published net zero target and that its capital investments in solar are directly influenced by transition risk. An operator of dispatchable low-carbon generation assets confirms that climate transition is highly influential at board level in capital allocation decisions. A FTSE 100 T&D operator and integrated utilities entity references the EU Taxonomy voluntary reporting as a related disclosure and notes the capital strategy narrative would complement existing TCFD work. |

| Air Quality [RETAINED TOPIC] | [REVISED] IF-EU-120a.1 Air pollutant emissions of: (1) NOx, [excluding N2O] (2) SOx, (3) hazardous air pollutants, and (4) particulate matter % of each in or near areas of dense population. | A smart metering and battery storage company indicates its business model is centered on the energy transition and fully supports this disclosure. An operator of dispatchable, low-carbon generation assets, notes that it already provides extensive air quality reporting. This reflects both the nature of its renewable thermal generation assets and the requirements of local regulatory permits, as well as ongoing community scrutiny. The operator confirms that data on NOx, SOx and other air pollutants is routinely reported. The stakeholder also observes that reporting emissions by proximity to densely populated areas may be of limited material relevance, as its facilities are typically located in rural or sparsely populated regions. A FTSE 100 T&D operator and integrated utilities entity indicates air quality is primarily relevant for its generation business. A major UK electricity retailer considers air quality a generation-side metric, well-established and not particularly relevant for retail operations. The stakeholder notes some relevance through its gas Combined Heat Plants and other heat networks. A small island integrated electricity operator notes minimal air quality relevance given import-dominant supply. Confirms the energy-from-waste plant generates some air emissions, but the entity purchases from the plant rather than owns it. Company vehicles generate some emissions, but these are insignificant. |

| Water Management [RETAINED TOPIC] | [REVISED] IF-EU-140a.1 (1) Total water withdrawn, (2) total consumed; % from water-stressed locations | A FTSE 100 T&D operator and integrated utilities entity notes water is not a material topic given its use is primarily for cooling its generation plant in the US. The entity stopped previous CDP water reporting as water is not significant at group level. The stakeholder notes that the company's main water disclosure is seawater used for cooling which passes through and is returned so not entirely consumed. An operator of dispatchable, low-carbon generation assets confirms that water reporting is already undertaken and broadly aligns with the proposed metrics. A small island integrated electricity operator notes that water does not represent a significant risk to its business. Backup diesel generation relies on seawater for cooling. However, this is used only on a contingent basis. |

| Water Management [RETAINED TOPIC] | [DELETED] IF-EU-140a.2 Number of incidents of non-compliance with water quality permits, standards and regulations | A FTSE 100 T&D operator and integrated utilities entity notes the removal of the old water compliance incident metric (previously in the standard) and welcomes it as the entity found it difficult to apply consistently and had to add a footnote to explain its measurement approach. |

| Water Management [RETAINED TOPIC] | [NEW] IF-EU-140a.4 Total water discharged by (1) destination and (2) level of treatment | An operator of dispatchable, low-carbon generation assets notes that water discharge by level of treatment is not currently reported but is likely achievable. However, further consideration may be required regarding data availability and feasibility, although this is not expected to present a significant challenge. A FTSE 100 T&D operator and integrated utilities entity indicates water discharge is the primary water disclosure given seawater cooling usage and would confirm this metric is feasible. |

| Hazardous Waste Management [REVISED TOPIC] | [NEW] IF-EU-150a.4 (1) Hazardous waste generated; (2) stored; (3) recycled (metric tonnes; coal combustion products (CCPs) s and radioactive waste separately in m³) | An operator of dispatchable, low-carbon generation assets confirms that data on hazardous waste generated from bioenergy material, is relatively easy to obtain and disclose, and therefore raises no issue with the proposed disclosures. However, the preparer notes that the third sub-disclosure, relating to waste recycled, would require the development of internal policies before disclosure. |

| Hazardous Waste Management [REVISED TOPIC] | [NEW] IF-EU-150a.6 | An operator of dispatchable, low-carbon generation assets confirms it has various policies but needs to develop an overarching hazardous waste management policy and considers this metric achievable. |

| Ecological Impacts [NEW TOPIC] | [NEW] IF-EU-160a.1 (1) Total spatial footprint (km²); (2) area disturbed; (3) area restored | A FTSE 100 T&D operator and integrated utilities entity notes very different approaches between UK (restoration focus) and US (protection focus) for nature and ecological management. Has conducted a TNFD LEAP assessment for its UK electricity distribution business as a pilot, but has not adopted TNFD group-wide. Would initially report a subset of business rather than group-wide. An operator of dispatchable, low-carbon generation assets notes that the company is moving towards TNFD reporting. Has reported one spatial footprint metric in its most recent annual report. Clarifies that biomass sourcing forests are not owned by the entity. Considers the metric achievable over time but currently in development. A small island integrated electricity operator confirms it has ArcGIS (Geographic Information System) mapping capability, enabling spatial analysis and asset area calculations. It considers spatial footprint reporting achievable, although this is not currently undertaken. A smart metering company indicated its battery infrastructure fits into the spatial footprint and the information can easily be determined and disclosed. |

| Ecological Impacts [NEW TOPIC] | [NEW] IF-EU-160a.2 % of total spatial footprint in or near environmentally sensitive locations | A small island integrated electricity operator confirms that it references coastal asset proximity in its annual report and is undertaking work to map assets against ecologically sensitive and designated sites of special interest. It considers this disclosure achievable. A FTSE 100 transmission and distribution (T&D) operator and integrated utilities entity notes that it conducts TNFD LEAP assessments at the project level as part of its planning processes and is developing group-level metrics. However, it has not yet formalised group-wide disclosures relating to sensitive locations. |

| Community Relations & Rights of Indigenous Peoples [NEW TOPIC] | [NEW] IF-EU-210a.1 Processes used to manage risks and opportunities associated with community rights and interests | A FTSE 100 T&D operator and integrated utilities entity confirms extensive project level community engagement for large transmission projects and Nationally Significant Infrastructure Projects (NSIPs), but does not currently aggregate this into standardised metrics. Considers this a significant step change from current practice. A small island integrated electricity operator confirms active community engagement for solar farm developments, including local consultations and planning processes. It notes that solar farm developments generates significant community interest. |

| Community Relations & Rights of Indigenous Peoples [NEW TOPIC] | [NEW] IF-EU-210a.2 (1) Number of non-technical delays and (2) total days idle | A FTSE 100 T&D operator and integrated utilities entity acknowledges underlying non-technical delay exposure in large UK transmission infrastructure projects, but does not currently track this in a format suited to IF-EU-210a.2 quantitative disclosure. Considers this a significant new data requirement. |

| Community Relations & Rights of Indigenous Peoples [NEW TOPIC] | [NEW] IF-EU-210a.3 % of operations in or near Indigenous Peoples' land | An operator of dispatchable, low-carbon generation assets (including electricity generation from bioenergy) confirms a full indigenous peoples engagement and policy, noting active engagement with indigenous communities in North America biomass sourcing regions. Considers this captured through supply chain due diligence rather than direct operations in indigenous lands. A FTSE 100 T&D operator and integrated utilities entity considers that indigenous peoples metrics are not applicable to its UK domestic operations. US operations involve engagement processes, but the entity does not currently report aggregated indigenous peoples metrics. |

| Community Relations & Rights of Indigenous Peoples [NEW TOPIC] | [NEW] IF-EU-210a.4 Description of engagement and due diligence processes relating to Indigenous Peoples' rights including FPIC | An operator of dispatchable, low-carbon generation assets confirms that it conducts due diligence on Indigenous Peoples in relation to bioenergy materials, including across the biomass sourcing supply chain. This is addressed within broader supply-chain policies rather than disclosed as a direct operational practice. The operator also maintains a standalone Indigenous Peoples policy. |

| Energy Affordability [RETAINED TOPIC] | [NEW] IF-EU-240a.5 | A major UK electricity retailer confirms energy affordability is a key topic and supports the narrative metric. The stakeholder notes the energy trilemma (security, affordability, sustainability) as central to the business. Highlights the importance of including innovative financial models (e.g. warm home discount or battery storage) as part of the affordability strategy narrative, as these go beyond simple discount programmes. A FTSE 100 T&D operator and integrated utilities entity confirms affordability is a key disclosure topic with increasing investor focus over the last 24 months. The stakeholder notes the entity uses different affordability measurements in the UK (network cost component on consumer bill) versus the US (full customer bill), creating comparison challenges. A small island integrated electricity operator notes affordability is managed as a business practice (self-regulated monopoly) rather than under regulation. Confirms RPI increases are considered under customer affordability lens. Entity does not operate disaggregated affordability programmes by residential/commercial/industrial customer category in the same way as mainland UK retailers. |

| Energy Affordability [RETAINED TOPIC] | [NEW] IF-EU-240a.6 (1) Number of active and (2) eligible participants in energy affordability programmes, by (a) residential, (b) commercial, (c) industrial | A major UK electricity retailer confirms programme participation data is largely already in the public domain through government scheme reporting (smart meters, insulation schemes) so consider this an achievable disclosure. However, the stakeholder notes that more granular commercial tariff participation disclosure could be commercially sensitive. Suggests focusing disclosure on smart meter installation counts and insulation programme participation as easier data points. A FTSE 100 T&D operator and integrated utilities entity notes programme participant counting may be difficult where affordability support is routed through NGOs or charitable funds rather than directly to customer bills. |

| Workforce Health & Safety [RETAINED TOPIC] | [REVISED] IF-EU-320a.1 Revised to: (1) Number of fatalities; (2) Total recordable incident rate for (a) direct employees and (b) non-employee workers; (3) average hours of health, safety and emergency response training. | A FTSE 100 T&D operator and integrated utilities entity welcomes the move from near miss frequency rate to actual incidents (TRIR and fatality rate), noting near miss definitions vary significantly across companies and create comparability problems. The entity already reports TRIR and fatality rate disaggregated for employees and non-employee workers. The entity notes the importance of distinguishing injuries to employees/contractors from injuries to members of the public caused by company assets - a category not captured in the proposed metrics but tracked by the entity and reviewed by auditors. An operator of dispatchable, low-carbon generation assets considers TRIR, fatality rate and NMFR standard H&S metrics. Notes the entity reports a broader metric called NMHIR (Near Miss and Hazard Identification Rate), which is broader than a pure near miss count. A major UK electricity retailer notes that Workforce Health & Safety (WHS) is primarily relevant for field workers; office-based staff are the larger workforce for the entity with driving being the main safety risk. Considers the proposed metrics standard and appropriate. Notes culture-related metrics are absent but acknowledges these would be too burdensome to mandate. A small island integrated electricity operator confirms safety data is captured including lost time injuries. Notes the entity still has overhead power line work creating field safety exposure despite its predominantly distribution model. Confirms WHS data is already tracked and reported. The smart metering company had no issues with the deletion of Near Miss Frequency Rate with the replacement by actual fatality incident. The view is that near miss is a leading indicator while actual fatalities (the new metric) show the actual crystallised risk. |

| Workforce Health & Safety [RETAINED TOPIC] | [NEW] IF-EU-320a.2 Description of management systems used to foster a safe working environment | A FTSE 100 T&D operator and integrated utilities entity welcomes the safety management systems narrative metric as it provides context for quantitative rates. Notes the entity has specific safety-related targets and Ofgem incentive arrangements related to safety performance. The entity also observed that SASB benchmarking data has limited usefulness as an internal management tool, having previously attempted to use SASB safety data for benchmarking and found the exercise of limited practical value. |

| Employee Recruitment, Development & Retention [NEW TOPIC] | [NEW] IF-EU-330a.1 Description of employee recruitment, development and retention risks, opportunities and strategies to manage them | A FTSE 100 T&D operator and integrated utilities entity considers employee skill retention relevant, and specifically highlights skills and technical workforce retention as an important investor-relevant topic given the delivery requirements of Ofgem's RIIO-T3 (Revenue = Incentives + Innovation + Outputs) regulatory framework. An operator of dispatchable, low-carbon generation assets confirm it currently voluntarily discloses voluntary and involuntary turnover rates separately in its ESG reporting, in advance of any formal requirement to do so. A small island integrated electricity operator notes workforce retention is important for the entity given it operates in a geographically constrained market, creating niche technical roles with limited alternative employment options. A smart metering company supports the introduction of this topic, noting skills shortage as a significant industry-wide risk. |

| Employee Recruitment, Development & Retention [NEW TOPIC] | [NEW] IF-EU-330a.2 (1) Voluntary and (2) involuntary turnover rate for (a) all employees and (b) occupational categories with skill shortages | A major UK electricity retailer considers demand-side management a key topic but notes the metrics primarily work for direct customer-facing retailers. The entity highlights the growing role of energy aggregators (which are companies that manage customer assets such as EV chargers and batteries to shift demand) as a market participant whose demand management activity may not be captured by the metric as currently framed, given that it is the aggregator rather than the energy supplier that manages the demand response. An operator of dispatchable, low-carbon generation assets notes demand-side management metrics are not directly applicable as a generator. Notes the entity does have supply-side management capabilities (pumped storage) which are not captured in the demand-side framing of this topic. Suggests supply-side flexibility metrics could complement demand-side metrics for a fuller picture. |

| Demand-side Management [REVISED TOPIC] | [REVISED] IF-EU-420a.4 Description of demand-side management risks, opportunities and strategies, including targets | A major UK electricity retailer welcomes this metric in principle but raises a structural concern: the metric as currently framed assumes that peak demand savings are delivered directly by the energy supplier. This does not adequately capture the growing role of third-party energy aggregators, which manage customer assets such as EV chargers and batteries to shift demand independently of the supplier. The entity considers this a gap that may become increasingly significant as aggregator-led demand response continues to grow. |

| Demand-side Management [REVISED TOPIC] | [NEW] IF-EU-420a.5 (1) Active and (2) eligible participants in demand-side management programmes, by (a) residential, (b) commercial, (c) industrial | As noted in IF-EU-420a.4, a major electricity retailer stakeholder observed that the proposed demand-side disclosures are generally welcomed but do not fully reflect certain emerging market developments. In particular, they do not account for the growing role of demand management initiatives delivered through aggregator platforms. Under these arrangements, an independent aggregator separate from the energy supplier provides demand management services. However, the current disclosure framework appears to assume that demand-side savings are managed solely by the retailer (energy supplier) and do not adequately capture situations where these services are delivered by third-party aggregators. |

| Supply Chain Management [NEW TOPIC] | [NEW] IF-EU-420a.6 Peak demand savings from demand-side management strategies | A UK biomass operator confirms extensive supply chain sustainability management processes covering biomass sourcing: SBP certification, FSC and PEFC chain of custody certification, biomass carbon calculator, and forest carbon mapping. Notes these processes go substantially beyond what the proposed metrics require, but are disclosed voluntarily through the company's digital biomass tracker. Supports the principle of supply chain disclosure but suggests the metric should specifically accommodate biomass-sourcing credibility disclosures (certification frameworks, deforestation-free verification) as the most material supply chain sustainability question for biomass generators. |

| Supply Chain Management [NEW TOPIC] | [NEW] IF-EU-430a.1 Description of processes to manage supply chain sustainability risks (HRDD, codes of conduct, audit practices) | A small island integrated electricity operator identifies its overseas electricity supplier as its primary and most strategically significant supplier, and notes that for hardware inputs such as cables and switchgear, the supplier base is likewise highly concentrated. Given this highly concentrated supply chain profile, the entity questions the decision-usefulness of this metric in its context. An operator of dispatchable, low-carbon generation assets notes that CDP already requires extensive supply chain management disclosure, suggesting coordination with CDP data requirements. It further notes that the proposed percentage of high-risk suppliers audited could be supplemented by disclosing certification status of key inputs (analogous to the FB-MP standard's approach for animal feed). |

| Supply Chain Management [NEW TOPIC] | [NEW] IF-EU-430a.2 % of high-risk suppliers subject to independent audit/verification in previous 3 years; non-conformances and corrective actions | A small island integrated electricity operator questions the definition of high-risk supplier in its context and suggests disclosure may produce limited investor-useful information given the entity's small and concentrated supplier base. |

| Critical Incident Risk Management (renamed from Nuclear Safety & Emergency Management) [REVISED TOPIC] | [DELETED] IF-EU-540a.2 Description of efforts to manage nuclear safety and emergency preparedness | The broadening of this topic from narrow nuclear safety management to all critical incident types was broadly welcomed by stakeholders, who considered the prior nuclear-only framing too restrictive for entities without nuclear generation operations. |

| Critical Incident Risk Management (renamed from Nuclear Safety & Emergency Management) [REVISED TOPIC] | [NEW] IF-EU-540a.3 Description of management systems used to identify and mitigate serious accidents [all critical incident types – dam failure, gas explosion, earthquake, wildfire] | An operator of dispatchable, low-carbon generation assets identifies wood pellet dust explosion risk, a classified hazardous substance under UK regulations as the most relevant critical incident risk for its operations. The entity notes that its fire and emergency management framework is described in its ESG reporting but has not yet been structured in the format required by IF-EU-540a.3. |

| Operational Resilience & System Reliability (renamed from Grid Resiliency) [REVISED TOPIC] | [REVISED] IF-EU-550a.1 Number of cybersecurity incidents causing disruption to the electrical power system [changed from compliance-based to incident-based] | A small island integrated electricity operator confirms cybersecurity risk is discussed extensively in the annual report. Notes the entity does not currently call out specific cyber incidents in its public report, but captures this information internally. A major UK electricity retailer notes cybersecurity disclosures are already queried by auditors in its annual disclosures and considers an emerging area moving towards established reporting. Notes physical asset vulnerability and operational resilience are more relevant for grid operators than for retailers. |

| Operational Resilience & System Reliability (renamed from Grid Resiliency) [REVISED TOPIC] | [REVISED] IF-EU-550a.2 SAIDI, SAIFI and CAIDI both (a) including and (b) excluding major event days (IEEE Std 1366) | A FTSE 100 T&D operator and integrated utilities entity notes SAIDI and SAIFI are reported for its US operations but its UK operations apply Ofgem's Customer Interruptions (CI) and Customer Minutes Lost (CML) framework, which uses a different methodology that is not directly compatible with IEEE Std 1366. The entity considers this a significant international applicability issue and recommends the ISSB acknowledge non-IEEE frameworks as permissible alternatives in the technical protocol. |

| Operational Resilience & System Reliability (renamed from Grid Resiliency) [REVISED TOPIC] | [NEW] IF-EU-550a.3 Average availability factor (%) for generation assets, by major energy source | An operator of dispatchable, low-carbon generation assets confirms it would have generation availability data but is uncertain whether it would be commercially sensitive to disclose at asset level. Notes the entity's biomass generation availability is a key operational metric internally. |

| Operational Resilience & System Reliability (renamed from Grid Resiliency) [REVISED TOPIC] | [NEW] IF-EU-550a.4 Amount (presentation currency) and % of assets vulnerable to climate-related physical risks, by asset type and risk type (acute/chronic) | An operator of dispatchable, low-carbon generation assets confirms it has already disclosed physical risk asset vulnerability in its annual report and considers this feasible. A small island integrated electricity operator raises a fundamental challenge with the vulnerable assets metric: for an island utility, virtually all assets could be considered vulnerable (the entity was hit by a 180mph tornado that affected the entire network). Conversely, a narrow interpretation could identify only one or two coastal substations. Questions what threshold distinguishes ‘vulnerable' from 'exposed.' The entity already models its assets against the government flood risk mapping (using IPCC 8.5 scenario) and sea level rise projections. Strongly suggest the need for the ISSB to clarify the 'vulnerable' definition and the counting methodology. A major UK electricity retailer notes physical asset vulnerability metrics and insurance considerations are already embedded in TCFD disclosures and business cases for grid infrastructure. Considers the disclosure sensible for grid operators though less relevant for retailers. |

| Operational Resilience & System Reliability (renamed from Grid Resiliency) [REVISED TOPIC] | [NEW] IF-EU-550a.5 Description of strategies to manage operational resilience and system reliability risks and opportunities, including targets | A FTSE 100 T&D operator and integrated utilities entity confirms operational resilience and reliability are key investor topics, with increased focus. SF6 management and interconnector availability are flagged as important resilience metrics already disclosed. Notes the strategy narrative metric is consistent with existing TCFD-aligned resilience disclosures. A small island integrated electricity operator notes it has been systematically undergrounding overhead transmission lines to improve storm resilience, with very few overhead lines remaining. Notes the subsea cables remain the primary resilience risk but consider this well-managed. |

Appendix 2: Meat, Poultry & Dairy stakeholder feedback

This table summarises stakeholder feedback received during the TAC Secretariat's outreach activities and does not constitute a complete extract of all proposed amendments in SASB/ED/2026/1 for the Meat, Poultry & Dairy Standard. Topics and metrics for which no stakeholder feedback was received are not reflected in the table. For reference, the following amendments proposed in the Exposure Draft are not covered in this table:

- Activity metrics: Revision to activity metric FB-MP-000.B and addition of two new workforce composition activity metrics.

- Land Use & Ecological Impacts: Deletion of old metrics FB-MP-160a.1 (animal litter and manure managed under a nutrient management plan) and FB-MP-160a.2 (percentage of livestock production in water-stressed regions).

- Food Safety: Addition of FB-MP-250a.4 (description of food safety risk management practices and processes throughout the value chain).

- Environmental & Social Impacts of Animal Supply Chain: Old topic replaced by new Environmental Supply Chain Management and Social Supply Chain Management topics. All old metrics under this topic are removed and replaced by new metrics covered in the table below.

| Disclosure topic | Metric code, description & nature of change | Stakeholder feedback summary |

|---|---|---|

| Greenhouse Gas Emissions | [REVISED] FB-MP-110a.1 (1) Gross global Scope 1 GHG emissions; (2) % methane; (3) % subject to emissions-limiting regulations | A UK FTSE-listed integrated pork and poultry operator considers the GHG metrics broadly reasonable. The entity raises a concern that calling out the GHG metric on methane may be too narrow, given that many businesses in the sector have now submitted and validated Forest, Land and Agriculture (FLAG) targets through the Science Based Targets initiative (SBTi), which incorporate methane as part of a broader set of land-use-related emissions. The entity suggests the metric could benefit from alignment with FLAG guidance. |

| Greenhouse Gas Emissions | [REVISED] FB-MP-110a.2 Description of Scope 1 GHG emissions targets [replaces old long/short-term strategy discussion; now targets-focused] | The entity considers the description of Scope 1 GHG emissions targets to be sensible in principle but questions whether this is the right vehicle for it, noting that target disclosure should be embedded in mainstream sustainability reporting regardless of SASB adoption. The entity is concerned about overlap with broader S1/S2 requirements. The entity raises the absence of Scope 3 emissions requirements as a significant omission, noting that its Scope 3 emissions are approximately ten times its combined Scope 1 and 2 emissions, consistent with Dr Barker's Alternative View documented in the Basis for Conclusions. |

| Energy Management | [REVISED] FB-MP-130a.1 (1) Total energy consumed; (2) % grid electricity; (3) % renewable from (a) self-generation and (b) direct contracts | The entity raises two specific points: (i) the reference to 'direct contracts' for renewable electricity is unclear, and the entity seeks clarification on whether this refers to power purchase agreements (PPAs) or a broader category of procurement arrangements. (ii) the entity notes that gigajoules (GJ) is not a unit commonly used in its operations, where kilowatt hours (kWh) or megawatt hours (MWh) are standard. |

| Water Management | [REVISED] FB-MP-140a.1 (1) Total water withdrawn; (2) total consumed; (3) % from water-stressed locations | The entity raises a conceptual point on the distinction between water withdrawal by source. The entity withdraws water from boreholes across multiple sites and questions whether borehole withdrawal should be perceived differently from mains abstraction, noting that mains water is itself often sourced from local boreholes. Considers the metric reasonable in concept but requests clearer guidance on the environmental distinction intended between sources. |

| Water Management | [REVISED] FB-MP-140a.2 Description of water-related risks, opportunities and strategies to manage them | The entity raises a general concern that the revised FB-MP Standard introduces significantly more subjective, narrative-based disclosure across multiple topics. The entity prefers metrics that are factual, comparable and concise, and is concerned that narrative requirements risk producing voluminous, non-comparable disclosures without tight guidance. |

| Water Management | [DELETED] FB-MP-140a.3 Number of incidents of non-compliance with water quality permits, standards and regulations | The entity considers the deletion of the water quality non-compliance incident metric understandable, but notes it had no objection to disclosing this information previously. The entity notes the compliance-based framing of the deleted metric was more about transparency than anything else. |

| Water Management | [NEW] FB-MP-140a.4 Total water discharged by (1) destination and (2) level of treatment | The entity identifies this as one of the more challenging new metrics. The entity discharges water either through on-site effluent treatment plants or directly to mains under permit from water companies, with treatment levels varying across 20+ manufacturing sites and farms. Explains that different sites may have primary, secondary or tertiary treatment levels and that creating a single coherent disclosure across all of these would require disclosure effectively for each level of treatment, which could complicate rather than clarify the metric. |

| Land Use & Ecological Impacts | [DELETED] FB-MP-160a.1 Amount of animal litter and manure generated; % managed according to a nutrient management plan | The entity has no objection to the deleted metrics on animal litter and manure management and conservation plan criteria. These were previously useful compliance-based disclosures. |

| Land Use & Ecological Impacts | [REVISED] FB-MP-160a.4 % of animal protein production from confined animal feeding operations [renumbered from old 160a.3] | Considers this metric reasonable. The entity's view is that, as far as it is aware, none of its direct operations would meet the definition of a confined feeding operation. |

| Land Use & Ecological Impacts | [NEW] FB-MP-160a.5 (1) Total spatial footprint (km²) of operations; (2) area disturbed; (3) area restored | Considers the spatial footprint metric for owned operations reasonable as its operations are predominantly UK based. |

| Land Use & Ecological Impacts | [NEW] FB-MP-160a.6 % of total spatial footprint of operations in or near environmentally sensitive locations | Considers the intent of the metric appropriate, but implementation-ready only with tighter guidance. |

| Land Use & Ecological Impacts | [NEW] FB-MP-160a.7 % of livestock produced from direct farming operations determined to be deforestation- or conversion-free, including targets | The entity is uncertain what this metric is intended to achieve and questions whether 'deforestation-free direct farming operations' refers to the physical farms (none of which in the UK have involved deforestation in recent history) or to deforestation in the feed ingredients used by those farms. For UK-based pork and poultry producers, direct farming operations would by definition be deforestation-free. Deforestation risk is primarily a supply chain concern (soy, corned beef from Brazil) rather than a direct farming concern for UK operators. |

| Land Use & Ecological Impacts | [NEW] FB-MP-160a.8 Priority products from direct farming operations sensitive to nature- and climate-related physical risks [qualitative] | The entity notes that TNFD-aligned nature risk assessment is still at an early stage for most UK businesses and this TNFD-aligned metric assumes a level of nature risk assessment maturity that is not yet widespread. The ISSB should not assume all preparers have completed nature-related risk assessments. |

| Land Use & Ecological Impacts | [NEW] FB-MP-160a.9 % of livestock production from direct farming operations implementing a written nutrient management plan | Finds the metric confusing and perceives it as a compliance-level requirement rather than a strategic sustainability indicator. Nutrient management plans are required in the UK under Environment Agency regulations above certain land thresholds and the data therefore exists, but notes the entity views this as baseline compliance rather than a meaningful differentiator. Considers the metric as proposed does not capture these more meaningful indicators and risks producing binary 'yes/no' responses that are of limited investor utility. |

| Food Safety | [DELETED] FB-MP-250a.1 GFSI audit (1) non-conformance rates and (2) corrective action rates for (a) major and (b) minor non-conformances | Notes it had no problem with the deleted GFSI audit non-conformance rate and supplier certification metrics and considered them useful compliance-based disclosures. Expresses mild disappointment at their removal, noting these provided a transparent and factual framework that was not onerous to report against. |

| Food Safety | [DELETED] FB-MP-250a.2 % of supplier facilities certified to a GFSI food safety certification programme | No objection to the deletion, but considers the objective GFSI certification percentage was preferable to the more subjective replacement metrics. |

| Food Safety | [REVISED] FB-MP-250a.3 (1) Description of recalls issued for food safety reasons and (2) total weight of products recalled | The entity has mixed views on the change from a number-of-recalls metric to a descriptive format. It questions whether SASB is the appropriate vehicle for describing what may have caused a recall, noting that causes can be within or outside the entity's control and that the tone and level of detail expected in a strategic annual report does not naturally accommodate product-specific recall descriptions. The entity notes it would likely disclose recall causes regardless, but is concerned the metric format elevates this to a level of detail out of place with the overall report. The entity also observes this represents a broader trend in the revised standard away from quantitative, comparable disclosure towards narrative description, which it considers less aligned with the original purpose of SASB. |

| Food Safety | [NEW] FB-MP-250a.6 Processes, controls and procedures to ensure food safety throughout the value chain [qualitative] | The entity considers this metric challenging to populate in a decision-useful manner. Operating across 20+ manufacturing sites and multiple farm operations spanning multiple proteins at different stages of the processing chain, a comprehensive description of processes, controls and procedures across the entire value chain would be highly voluminous. The entity raises a structural concern: processes and controls requirements appear across multiple sections of the revised standard (food safety, animal health and welfare, supply chain management), creating fragmented and potentially duplicative narrative disclosure. |

| Antibiotic Use in Animal Production | [REVISED] FB-MP-260a.1 % of animal production receiving (1) medically important antibiotics and (2) non-medically important antibiotics, by type of livestock | Agrees with the metric in principle but raises a concern about the decision-usefulness of the medically important versus non-medically important antibiotics distinction. The entity's view is that it only ever uses antibiotics when medically indicated, which means it would report 100% medically important and 0% non-medically important. This would make the metric non-differentiating for entities with strong antibiotic stewardship. The entity currently discloses antibiotic use in mg/PCU (milligrams per population correction unit) aligned to RUMA targets. A more granular and differentiated unit that provides better insight into antibiotic stewardship trends over time. Suggests the ISSB consider whether units or additional sub-disclosures could make the metric more informative, and requests clarity on the intended definition of 'medically important' to avoid inconsistent self-assessment across reporters. |

| Workforce Health & Safety | [REVISED] FB-MP-320a.1 (1) TRIR and (2) fatality rate for (a) direct employees and (b) non-employee workers [expanded scope; formula: count x 1,000,000 / hours worked] | Considers workforce health and safety changes largely fine. Notes the expansion to non-employee workers and the shift to TRIR and fatality rate is broadly appropriate. |

| Animal Health Care & Welfare (topic renamed from Animal Welfare) | [DELETED] FB-MP-410a.1 % of pork produced without use of gestation crates | The entity raises no objection to the deletion of the gestation crate metric, which it considered a legitimate and transparent compliance-based disclosure. The entity acknowledges the industry may have moved to a point where this metric is less relevant as a differentiator, but considers the deletion illustrative of the broader shift from objective quantitative metrics to subjective narrative disclosures in the revised standard. |

| Animal Health Care & Welfare (topic renamed from Animal Welfare) | [DELETED] FB-MP-410a.2 % of cage-free shell egg sales | The entity notes it does not sell eggs, meaning the cage-free shell egg sales metric was never applicable to its operations so has no issue with the deletion. |

| Animal Health Care & Welfare (topic renamed from Animal Welfare) | [NEW] FB-MP-410a.3 % of production certified to a third-party animal welfare standard, by type of livestock and certification | Agrees with the intent of this metric. Notes it is consistent with the entity's existing approach of applying recognised welfare standards and considers it an appropriate replacement for the deleted metrics, subject to clear definitions of which certification schemes qualify. |

| Animal Health Care & Welfare (topic renamed from Animal Welfare) | [NEW] FB-MP-410a.4 Description of animal welfare strategy, including targets, procedures and value chain integration [qualitative] | Expressed concern that this metric, alongside FB-MP-410a.5 on biosecurity, represents a significant expansion in narrative disclosure requirements and will substantially increase the length and complexity of the annual sustainability disclosure. The entity notes its sustainability section in the annual report is already the longest section of the document. |

| Animal Health Care & Welfare (topic renamed from Animal Welfare) | [NEW] FB-MP-410a.5 Description of risks and opportunities related to biosecurity, including disease management strategies [qualitative] | Notes biosecurity strategy description is complex to disclose comprehensively given the breadth of the topic across multiple species, farming stages, processing sites and geographic locations. Views this alongside FB-MP-410a.4 as potentially generating very extensive disclosure. Notes positively that the renaming of the topic from 'Animal Welfare' to 'Animal Health Care & Welfare' is a constructive change, as it is more aligned with how the industry itself discusses animal health management. |

| Product Innovation [NEW TOPIC] | [NEW] FB-MP-410b.1 Use of innovation in food products to address sustainability-related risks and opportunities [qualitative] | Considers product innovation a broad and complex topic for a business with tens of thousands of stock keeping units. The entity notes it would discuss innovation in the context of its transition plan (being released soon) and considers the metric not impossible to populate, but expresses concern about the move from quantitative to qualitative disclosure that this metric exemplifies. Notes that it is difficult to isolate product-level innovation from the entity's much broader manufacturing sustainability programme. The entity questions the metric's scope: whether it refers only to environmental product innovation or extends to health and nutritional product innovation. |

| Environmental & Social Impacts of Animal Supply Chain (renamed from Animal Supply Chain Management) | [RETAINED] FB-MP-430a.1 % of livestock from suppliers implementing conservation plan criteria | No objection to the retained metrics. The entity had found these useful previously and considers them appropriate to retain. |

| Environmental & Social Impacts of Animal Supply Chain (renamed from Animal Supply Chain Management) | [RETAINED] FB-MP-430a.2 % of supplier and contract production facilities verified to meet animal welfare standards | No specific stakeholder concerns on the retained animal welfare verification percentage. |

| Environmental Supply Chain Management [NEW TOPIC] | [NEW] FB-MP-430b.1 % of sourced (1) livestock and (2) animal feed determined to be deforestation- or conversion-free, including targets | Considers feed sourcing deforestation disclosure more relevant and workable than the equivalent direct farming metric (FB-MP-160a.7) as the deforestation risk genuinely sits in the supply chain (soy from South America) rather than in direct UK farming operations. The entity uses certifications such as Roundtable on Responsible Soy (RTRS) for soy sourcing and direct monitoring for higher-risk commodities. Considers the metric appropriate and consistent with existing supply chain due diligence work. |

| Environmental Supply Chain Management [NEW TOPIC] | [NEW] FB-MP-430b.2 Priority sourced livestock and animal feed sensitive to nature- and climate-related physical risks in the supply chain [qualitative] | Notes that TNFD-aligned nature risk work is at an early stage for most businesses and the standard should not assume completion of nature risk assessments. |

| Environmental Supply Chain Management [NEW TOPIC] | [NEW] FB-MP-430b.3 % of sourced livestock from farms implementing a written nutrient management plan | Consider this metric for sourced livestock more readily than for direct operations (FB-MP-160a.9), noting that nutrient management plans are a regulatory requirement in the UK above certain land thresholds and data should therefore be obtainable from contract farmers. However, reiterates that the metric risks producing binary responses and prefers a framing that captures more meaningful sustainable farming practice indicators. |

| Environmental Supply Chain Management [NEW TOPIC] | [NEW] FB-MP-430b.4 % of animal protein sourced from confined animal feeding operations | Expects its own sourced livestock would score 0% or very low on this metric. |

| Social Supply Chain Management [NEW TOPIC] | [NEW] FB-MP-430c.1 Processes, controls and procedures for managing labour conditions and impacts on local communities in the supply chain, including HRDD [qualitative] | The entity questions whether SASB is the appropriate vehicle for disclosing labour conditions and HRDD processes in the supply chain, arguing this requirement is relevant to any business with a supply chain regardless of sector and should sit within a broader sustainability reporting framework rather than a sector-specific standard. The entity considers this metric introduces generic corporate responsibility content that dilutes the sector-specificity of SASB. Suggests reference to the entity's Modern Slavery Act statement or equivalent human rights due diligence policy should be sufficient. |

| Social Supply Chain Management [NEW TOPIC] | [NEW] FB-MP-430c.2 % of sourced animal feed certified to internationally recognised standards that trace the path of products through the supply chain | Consider this metric as consistent with existing supply chain management work, noting certifications such as RTRS for soy are already tracked. |

| Social Supply Chain Management [NEW TOPIC] | [NEW] FB-MP-430c.3 % of high-risk suppliers subject to independent third-party audit/verification in previous 3 years; non-conformances and corrective actions | The entity notes it uses multiple dimensions of supplier risk (sustainability risk, dependency risk, ingredient risk). Notes that describing non-conformances could require extensive detail given a large supplier base. The entity interprets the metric as requiring the percentage of high-risk suppliers subject to audit processes that incorporate non-conformance management, rather than a list of every non-conformance, which would be operationally feasible. |

| Animal & Feed Sourcing | [RETAINED] FB-MP-440a.1 % of animal feed sourced from regions with High or Extremely High Baseline Water Stress | The entity notes with minor disappointment that some animal and feed sourcing metrics are being removed or scaled back from the previous standard, considering them relevant to investor decision-making. The entity raises no specific objection to the metrics that have been retained. |