The content on this page has been converted from PDF to HTML format using an artificial intelligence (AI) tool as part of our ongoing efforts to improve accessibility and usability of our publications. Note:

- No human verification has been conducted of the converted content.

- While we strive for accuracy errors or omissions may exist.

- This content is provided for informational purposes only and should not be relied upon as a definitive or authoritative source.

- For the official and verified version of the publication, refer to the original PDF document.

If you identify any inaccuracies or have concerns about the content, please contact us at [email protected].

An evolved audit supervision approach

The FRC does not accept any liability to any party for any loss, damage or costs howsoever arising, whether directly or indirectly, whether in contract, tort or otherwise from any action or decision taken (or not taken) as a result of any person relying on or otherwise using this document or arising from an omission from it.

© The Financial Reporting Council Limited 2026 The Financial Reporting Council Limited is a company limited by guarantee. Registered in England number 2486368. Registered Office: 13th Floor, 1 Harbour Exchange Square, London E14 9GE

Foreword – Anthony Barrett, Executive Director of Supervision

The Financial Reporting Council's (FRC) supervision of audit firms plays a vital role in the audit and financial reporting ecosystem that underpins confidence in UK capital markets. Audit quality and high standards of reporting support the credibility of financial information relied upon by investors, lenders, and other stakeholders when allocating capital. Effective supervision upholds high standards and ensures continued access to audit services, a globally respected audit profession, and a resilient, well-functioning audit market. This establishes trust in corporate reporting and supports the UK's ability to attract investment and provide organisations with reliable access to capital.

Our supervision of audit firms is rooted in strengthening audit quality and ensuring accountability, in support of the public interest across the audit system. Since 2018, in response to public and political concerns following a series of high-profile corporate failures, our supervisory work has been focused on driving improvements in audit quality and challenging firms to address significant failures that undermined trust in the UK audit market and profession. Our work with firms and Recognised Supervisory Bodies (RSBs) has delivered sustained improvements in audit quality.

The audit market has evolved further since 2018, shaped by technological advancements, changing ownership structures and broader shifts in the business environment. Our regulatory model must remain responsive to changes across the audit market and reflect each firm's impact and risks.

Our revised audit supervision approach is right for the UK audit and financial reporting ecosystem. It enhances and modernises our work so that it remains effective for the current and future audit landscape. Its built-in ability to evolve with firm and market developments delivers a more effective, integrated and future-proof framework.

Central to this approach is placing firms' Systems of Quality Management (SoQM) at the heart of supervision, focusing on how firms operate their SoQMs in line with the International Standard on Quality Management (ISQM) (UK) framework. Effective SoQMs are fundamental to delivering high-quality audit engagements, helping firms identify and respond to risks to audit quality and supporting consistent performance across engagements.

Our revised approach to supervision will begin in April 2026 with a phased year of implementation and development for the twelve largest audit firms during 2026/27, to inform further enhancements to the approach for 2027/28. Throughout this period, we will continue to work closely with stakeholders to refine and enhance the model.

Our public reporting is an important part of how we communicate our work to the market, ensuring stakeholders have clear, decision-useful insight into developments in audit quality and the wider audit ecosystem. As our approach evolves, our reporting will continue to develop accordingly, moving from initial implementation in 2026 towards a more comprehensive model for 2027 and beyond. This evolution will support more meaningful, timely and relevant communication and engagement with users of audit, reinforcing transparency and strengthening confidence in the audit market.

We recognise that we may not get everything right immediately, but we are committed to listening, learning and further evolving our approach to remain proportionate to firms' impact and risk, and responsive to developments in the profession and the market. Those subject to our supervision can expect a robust, consistent, professional and transparent regulatory process based on principles of fairness, proportionality and clarity.

Introduction

This statement sets out the FRC's revised audit supervision approach, designed to ensure the UK maintains a high-quality, resilient and trusted audit market and profession. It explains how the model has evolved in response to developments in the audit ecosystem, and the feedback the FRC received from extensive engagement during 2025. It outlines how the new approach will work, setting out how the FRC will review each firm's impact, assess risks and report to the market. Alongside this, the document outlines how the FRC will be phasing its implementation from April 2026 and how the revised approach will impact stakeholders. Finally, the statement sets out how we will leverage wider initiatives and gather ongoing feedback from firms, investors, audit committee chairs and RSBs to shape the final model.

Feedback from stakeholders

Over the past year, extensive engagement with stakeholders took place through one-to-ones, roundtables and a discussion paper issued in August 2025. Stakeholder feedback was constructive and has directly informed the development of the revised approach to audit supervision. We are grateful for stakeholders' time, engagement and consideration.

Support for a systems-based supervisory approach

Stakeholders supported a supervisory approach rooted in SoQM. They emphasised the importance of proportionality and scalability and cautioned against a one-size-fits-all model. Smaller firms stressed the need for a framework to reflect the needs of the whole market, not just the largest firms. Users highlighted the importance of independent assurance through file inspections and reinforced that engagement performance remains a core component of ISQM (UK) 1.

Inspection frequency and processes

Feedback on inspection frequency and process was more varied. Stakeholders welcomed the proposal to phase in corroboratory, follow-up and thematic reviews to enable more targeted inspection of particular risks. However, smaller firms warned against reducing inspection activity at larger firms in ways that could shift the supervisory burden onto them. Across the ecosystem, stakeholders called for clearer definitions and guidance on how proportionality should be applied within a coherent framework. RSBs emphasised embedding cultural change and learning over continued emphasis on audit quality grading.

Public reporting and transparency

Firms recognised the value of public reporting but raised concerns about reputational risk and the potential for media misinterpretation. Users sought more explicit quality indicators and comparative reporting to support decision-making. Overall, stakeholders preferred balanced reporting that combines qualitative insight with contextual quantitative data, underpinned by the firms' SoQM.

How will the FRC deliver this revised approach?

Through a revised risk-based approach, the FRC will strengthen the capabilities of audit firms in operating and continually enhancing their SoQM to deliver sustained audit quality. The revised supervisory approach will be grounded in SoQMs:

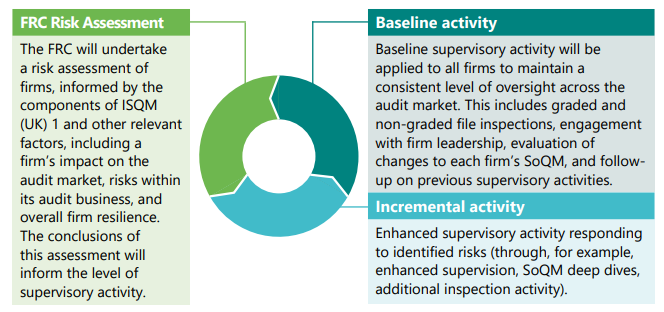

Visual representation of the approach, described in the following paragraphs

FRC Risk Assessment

The FRC will undertake a risk assessment of firms, informed by the components of ISQM (UK) 1 and other relevant factors, including a firm's impact on the audit market, risks within its audit business, and overall firm resilience. The conclusions of this assessment will inform the level of supervisory activity.

Baseline activity

Baseline supervisory activity will be applied to all firms to maintain a consistent level of oversight across the audit market. This includes graded and non-graded file inspections, engagement with firm leadership, evaluation of changes to each firm's SoQM, and follow-up on previous supervisory activities.

Incremental activity

Enhanced supervisory activity responding to identified risks (through, for example, enhanced supervision, SoQM deep dives, additional inspection activity).

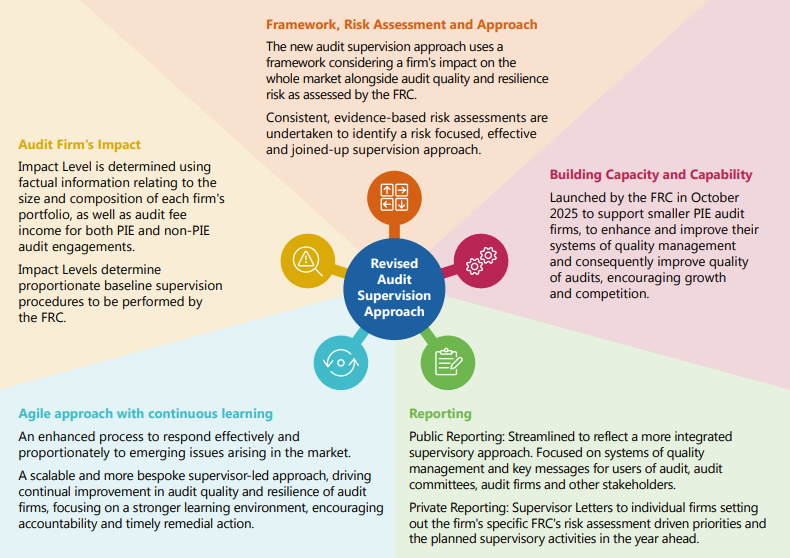

Visual representation of the Revised Audit Supervision Approach, described in the following paragraphs

Framework, Risk Assessment and Approach

The new audit supervision approach uses a framework considering a firm's impact on the whole market alongside audit quality and resilience risk as assessed by the FRC. Consistent, evidence-based risk assessments are undertaken to identify a risk focused, effective and joined-up supervision approach.

Building Capacity and Capability

Launched by the FRC in October 2025 to support smaller PIE audit firms, to enhance and improve their systems of quality management and consequently improve quality of audits, encouraging growth and competition.

Agile approach with continuous learning

An enhanced process to respond effectively and proportionately to emerging issues arising in the market. A scalable and more bespoke supervisor-led approach, driving continual improvement in audit quality and resilience of audit firms, focusing on a stronger learning environment, encouraging accountability and timely remedial action.

Reporting

Public Reporting: Streamlined to reflect a more integrated supervisory approach. Focused on systems of quality management and key messages for users of audit, audit committees, audit firms and other stakeholders.

Private Reporting: Supervisor Letters to individual firms setting out the firm's specific FRC's risk assessment driven priorities and the planned supervisory activities in the year ahead.

Audit firm's impact

Led by the appointed FRC firm Supervisor, our assessment begins with a consistent framework to review a firm's impact in the market. This will be determined by using factual information relating to the size and composition of each firm's portfolio, as well as audit fee income for both Public Interest Entity (PIE) and non-PIE audit engagements.

This information, coupled with macro factors reflecting market-wide conditions that influence all audit firms' operations, will be assessed to provide context for a firm's position relative to the broader audit landscape. The impact level will determine proportionate baseline supervision procedures to be performed by the FRC.

Framework, risk assessment and approach

Consistent, evidence-based risk assessments will be undertaken using a comprehensive assessment, in line with the SoQM framework, to ascertain where there are firm-specific risks. All conclusions will reflect the evidence obtained by the FRC, and the appropriate professional body, through engagement with the relevant firm. The output of this risk assessment for each firm will summarise a collective view of the FRC's identified audit quality and resilience risks and will support a bespoke, risk-focused, effective and joined-up supervision approach.

The framework is designed to promote consistency in our approach to supervision. Our risk assessment process considers the quality and resilience risk rating which is based on the level of confidence the FRC considers it may take from the firm's SoQM.

Where we have confidence in the effectiveness of a firm's SoQM, we will reduce our ongoing ISQM (UK) 1 inspection work to primarily focus on key changes to that system.

Recognising the confidence that can be obtained from the operation of robust and effective SoQMs, the FRC will reduce the number of graded file inspections for firms where audit quality is consistently delivered to a high standard. As a consequence, the FRC will no longer aim to inspect the FTSE 350 audits over a five-year period.

The FRC will phase in specific targeted (ungraded) file inspections to respond to identified areas of risk. These will include follow up and thematic based reviews. The FRC will also develop a framework for corroboratory inspections to obtain comfort over firms' internal quality monitoring programmes.

Building Capacity and Capability For Smaller Firms

The revised audit supervision approach aligns with the FRC's Building Capacity and Capability For Smaller Firms initiative, which was introduced in October 2025. This was established to provide support for continuous quality improvements and effective systems of quality management across smaller firms, starting with those operating in the PIE audit market. This initiative has been designed to improve quality and encourage growth and competition. As the Competent Authority, the FRC is working with the RSBs to develop a scalable, risk-focused approach for supervision which can be applied across the whole audit market.

Reporting

Public reporting: The FRC will continue to publish a public report on significant matters and key audit quality messages affecting the firms and the broader audit market, with the aim of providing useful information to users of audit. Although the work undertaken in the 2025/26 cycle predates full implementation of our evolved approach, we are beginning to update our public reporting accordingly.

This year we plan to publish the Annual Review of Audit Quality (ARAQ), accompanied by individual firm-specific appendices. These appendices will replace, and be shorter than, the standalone firm reports published in previous years. For the 2025/26 ARAQ (expected to be published in July 2026), firm-specific appendices will only be produced for the six largest firms, based on their impact on the audit market. Inspection results for the other firms will be aggregated. We will engage with stakeholders across the ecosystem following this publication to further understand views and develop our 2027 reporting, which will consider individual appendices for each of the largest 12 firms.

Private reporting: Supervisor letters will be issued each year to the largest 12 firms and as appropriate to other firms auditing PIEs. These will highlight the key areas of focus and FRC risk assessment driven priorities for the firm for the coming year and the proposed approach to supervision in response.

Priorities will continue to evolve and develop, and our approach will adapt in a timely manner. An annual risk assessment will be carried out to ensure this is captured and the appropriate supervision work continues.

Agile approach with continuous learning

The revised approach introduces an enhanced process for us to respond effectively and proportionately to emerging issues across the market. This is combined with the flexibility to adapt our supervisory activity as risks and circumstances evolve at an individual firm or across any number of firms. It establishes a scalable and more bespoke supervisor-led approach, that drives continuous improvement in audit quality and resilience of audit firms. Central to this approach is a commitment to open, timely engagement with firms, fostering greater accountability and transparency. By embedding these principles, the model supports a stronger learning environment and ensures that remedial actions are taken promptly and constructively.

What does this mean for our stakeholders?

The revised approach to audit supervision is an evolution designed for the future UK audit landscape. The approach will be agile, responsive to learnings and insights from stakeholders and continue to evolve.

For audit firms

The revised supervision approach will provide audit firms with a risk-based, effective, proportionate approach, aligned with the needs of a modern audit market. Where we have confidence in a firm's SoQM, our work will focus on changes identified by the firm in its SoQM and areas where our risk assessment indicates heightened attention is warranted. The revised approach builds on the concept of continual learning for both us and the firms we regulate in line with the principles of ISQM (UK) 1, to improve audit quality and the resilience of the profession.

We will continue structured engagement with firm leadership and their Independent Non-Executives. The frequency of this engagement will, as with all our work going forward, be based on the audit firm's impact and risks. Firms should continue to engage responsively with us in an open and timely manner, proactively notifying us of changes and matters that could impact on the reputation of the firm and/or the audit profession.

Graded file inspections, proportionate to the firm's impact, will remain an essential element of our approach. These inspections provide an independent perspective on the audit work undertaken to support the audit opinion and corroborate the effectiveness of the firm's SoQM. We will complement these with follow-up inspections (targeting previously identified issues), thematic inspections (in some cases targeting topics or procedures across multiple files), and piloting corroboratory inspections.

For users of audit services

Audit Committee Chairs: The revised audit supervision approach will provide Audit Committee Chairs with succinct reporting and wider relevant information on audit firms to enable audit committees to challenge auditor performance and support decisions on appointments and reappointments.

Investors: The evolved supervisory approach strengthens the systems within audit firms that support the delivery of consistent, high-quality audits. By focusing on firms' SoQM and adopting a more risk-based approach, we aim to improve the resilience and reliability of the audit market by building confidence in audit quality and in turn, the credibility of corporate reporting that investors rely on.

For Recognised Supervisory Bodies

Throughout the development of our supervisory approach we have engaged with the RSBs to drive a more consistent and coordinated approach across the entire audit market (PIE and non-PIEs).

Perspectives of the RSBs and findings arising from their inspection activity have been, and will continue to be, included within our annual risk assessment process for those firms where we have mutual regulatory oversight. We are committed to continue our close working with the RSBs to develop a scalable, risk focused approach for supervision of the whole audit market.

Alignment with other FRC initiatives

The FRC's three-year strategy is clear: to serve the public interest while actively supporting UK growth and investment through regulation that is smart, targeted and proportionate. Alongside a revised audit supervision approach, this means modernising other key elements of the regulatory system. This includes a robust and transparent enforcement process that has a range of tools to take more proportionate and timely action, and direct action to strengthen the small and medium-sized enterprises audit market. Across all these programmes, the objective is the same: a system that maintains high standards while working better in practice for businesses, professionals and investors.

A relentless focus on clear and easily navigable regulation is essential to building confidence, encouraging collaboration and ensuring that regulation supports both trust and long-term economic growth. Insights from supervision, along with improved processes and data, will feed into wider regulatory activities, ensuring that FRC's interventions are coordinated and targeted at supporting a healthy, resilient and high-performing audit market.

Financial Reporting Council

London office:

13th Floor,

1 Harbour Exchange

Square, London,

E14 9GE

Birmingham office:

5th Floor,

3 Arena Central,

Bridge Street,

Birmingham, B1 2AX

+44 (0)20 7492 2300

www.frc.org.uk

Follow us on LinkedIn