The content on this page has been converted from PDF to HTML format using an artificial intelligence (AI) tool as part of our ongoing efforts to improve accessibility and usability of our publications. Note:

- No human verification has been conducted of the converted content.

- While we strive for accuracy errors or omissions may exist.

- This content is provided for informational purposes only and should not be relied upon as a definitive or authoritative source.

- For the official and verified version of the publication, refer to the original PDF document.

If you identify any inaccuracies or have concerns about the content, please contact us at [email protected].

Audit Quality Inspection Report May 2014: Deloitte LLP

The FRC is responsible for promoting high quality corporate governance and reporting to foster investment. We set the UK Corporate Governance and Stewardship Codes as well as UK standards for accounting, auditing and actuarial work. We represent UK interests in international standard-setting. We also monitor and take action to promote the quality of corporate reporting and auditing. We operate independent disciplinary arrangements for accountants and actuaries; and oversee the regulatory activities of the accountancy and actuarial professional bodies.

The FRC does not accept any liability to any party for any loss, damage or costs howsoever arising, whether directly or indirectly, whether in contract, tort or otherwise from any action or decision taken (or not taken) as a result of any person relying on or otherwise using this document or arising from any omission from it.

© The Financial Reporting Council Limited 2014 The Financial Reporting Council Limited is a company limited by guarantee. Registered in England number 2486368. Registered Office: 5th Floor, Aldwych House, 71-91 Aldwych, London WC2B 4HN.

1. Background information and key messages

1.1 Introduction

This report sets out the principal findings arising from the inspection of Deloitte LLP ("Deloitte” or “the firm") carried out by the Audit Quality Review team of the Financial Reporting Council (“the FRC"), in respect of the year to 31 March 2014 (“the 2013/14 inspection"). We inspect Deloitte annually. Our inspection was conducted in the period from April 2013 to December 2013 (referred to as "the time of our inspection"). The objectives of our work are set out in Appendix A.

Our inspection comprised reviews of individual audit engagements and a review of the firm's policies and procedures supporting audit quality.

We reviewed 17 audit engagements undertaken by the firm, of which one was a further review of an audit reviewed in our last inspection. These related to FTSE 100, FTSE 250, other listed and other major public interest entities, with financial year ends between June 2012 and March 2013. Our reviews were selected on a risk basis, utilising a risk model; each review covered only selected aspects of the relevant audit. The further review included an assessment of the extent to which our previous findings on that audit had been addressed.

Our responsibility is to monitor and assess the quality of the audit work performed by the UK firm. Accordingly, our reviews of group audits covered the planning and control of the audit by the group engagement team, including their evaluation of the adequacy of the work performed by component auditors, and selected aspects of other work performed by the UK firm at group and/or component level. Our review did not cover audit work relating to components undertaken by other firms, within or outside the Deloitte international network.

Our review of the firm's policies and procedures supporting audit quality covered the following areas:

- Tone at the top and internal communications

- Transparency report

- Independence and ethics

- Performance evaluation and other human resource matters

- Audit methodology, training and guidance

- Client risk assessment and acceptance/continuance

- Consultation and review

- Audit quality monitoring

- Other firm-wide matters

We exercise judgment in determining which findings to include in our public report on each inspection, taking into account their relative significance in relation to audit quality, both in the context of the individual inspection and in relation to any areas of particular focus in our overall inspection programme for the relevant year. Where appropriate, we have commented on themes arising or issues of a similar nature identified across more than one audit.

Further information on the scope of our work and the basis on which we report is set out in Appendix A.

All findings requiring action set out in this report, together with the firm's proposed action plan to address them, have been discussed with the firm. Appropriate action may have already been taken by the date of this report. The adequacy of the actions taken and planned will be reviewed during our next inspection.

The firm was invited to provide a response to this report for publication. The firm's response is set out in Appendix B.

We acknowledge the co-operation and assistance received from the partners and staff of Deloitte in the conduct of our 2013/14 inspection.

1.2 Background information on the firm

Deloitte is a UK limited liability partnership and is the UK member firm of Deloitte Touche Tohmatsu Limited (“DTTL”). The firm operates from 24 locations in the UK through four service lines, being Audit, Tax, Consulting and Corporate Finance. In addition, the firm owns 100% of the shares of Deloitte AG, based in Switzerland. All statutory audit work is conducted through the Audit service line which comprises thirteen groups, based on geography and industry sectors.

For the year ended 31 May 2013, the firm's turnover was £2,515 million, of which £742 million related to the Audit service line, and there were 740 equity partners. There were 197 individuals who were authorised to sign audit reports, of whom 158 were equity partners, 18 were non-equity partners and 21 were employees (directors) 1.

We estimate that the firm audited 367 UK entities within the scope of independent inspection as at 31 December 2012. Of these entities, our records show that 154 had securities listed on the main market of the London Stock Exchange, including 17 FTSE 100 companies and 66 FTSE 250 companies.

The UK firm audits a number of entities incorporated in Jersey, Guernsey or the Isle of Man whose securities are traded on a regulated market in the European Economic Area. These are inspected by us under separate arrangements agreed with the relevant regulatory bodies in those jurisdictions. The results of these reviews are included in this report. Our records show that, at the time of our inspection, the firm had 43 such audits, including three FTSE 100 companies and four FTSE 250 companies.

1.3 Overview

We focus in this report on matters where we believe improvements are required to safeguard and enhance audit quality. We set out our key messages to the firm in this regard in section 1.4. While this report is not intended to provide a balanced scorecard, we highlight certain matters which we believe contribute to audit quality, including the actions taken by the firm to address findings arising from our prior year inspection.

The firm places considerable emphasis on its overall systems of quality control and, in most areas, has appropriate policies and procedures in place for its size and the nature of its client base. Nevertheless, we have identified certain areas where improvements are required to those policies and procedures. These are set out in this report.

Our file review findings, as set out in section 2, largely relate to the application of the firm's procedures by audit personnel, whose work and judgments ultimately determine the quality of individual audits. The firm took a number of steps in response to our prior year findings to achieve improvements in audit quality. This included enhanced guidance, technical communications and audit training on the recurring themes. However, issues continued to arise in some of these areas.

A number of our more significant findings relate to audit work performed by the firm, at component level, in relation to listed groups. More attention should, therefore, be paid by the firm to the quality of work at component level on group audits.

1.4 Key messages

The firm should pay particular attention to the following areas in order to enhance audit quality or safeguard auditor independence:

- Improve the approach in relation to the audit of collective and individual loan loss provisions in financial services entities.

- Ensure more attention is given to the quality of work performed by the firm at component level on group audits.

- Improve the audit approach in relation to the testing of journals, including the selection of journals based on characteristics of fraud risk.

- Ensure audit teams pay more attention to the audit of revenue, including the risk assessment and substantive analytical review procedures.

- Improve the audit approach and guidance in relation to the testing of IT controls and reports.

- Further embed a culture where achieving high quality audit work is recognised and rewarded.

2. Principal findings

The comments below are based on our reviews of individual audits and the firm's policies and procedures supporting audit quality.

2.1 Reviews of individual audits

We reviewed and assessed the quality of selected aspects of 17 audits (2012/13: 14 audits), of which one was a further review of an audit reviewed in our last inspection, which included an assessment of how findings previously raised had been addressed (2012/13: two follow-up reviews were also undertaken).

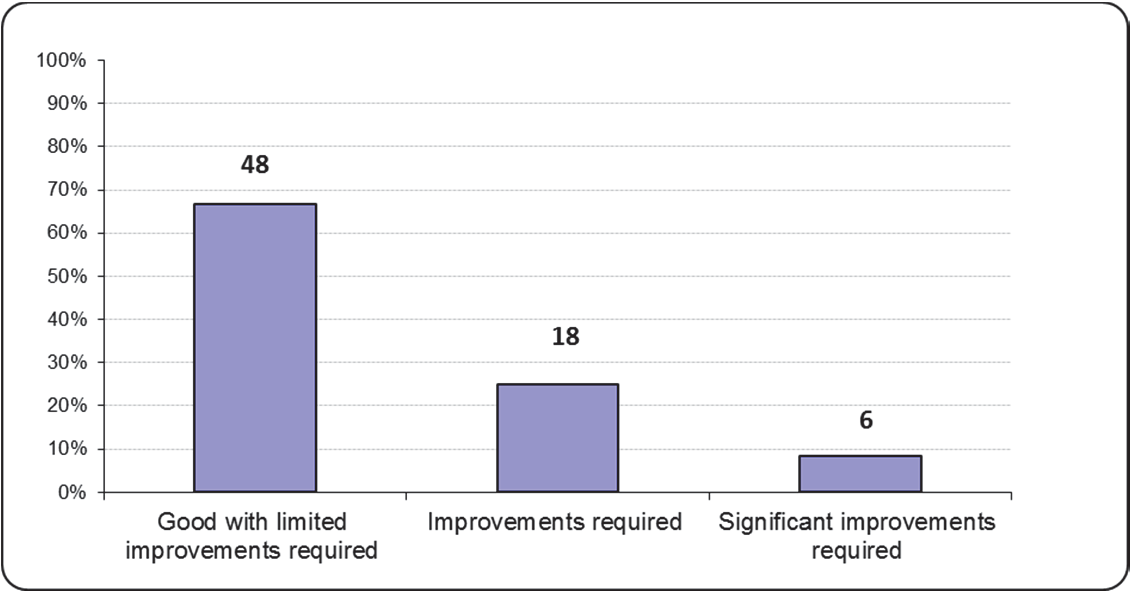

Of the audits we reviewed, 12 (2012/13: 11) were performed to a good standard with limited improvements required and four audits (2012/13: two) required improvements. One audit (2012/13: one) required significant improvements in relation to the testing of the collective and individual loan loss provisions. Further details are set out below.

An audit is assessed as requiring significant improvements if we had significant concerns in relation to the sufficiency or quality of audit evidence, or the appropriateness of significant audit judgments in the areas reviewed, or the implications of other matters are considered to be individually or collectively significant. This assessment does not necessarily imply that an inappropriate audit opinion was issued.

The bar chart below shows the percentage of the audits we reviewed in 2013/14, falling within each grade, with comparatives for 2012/13 and 2011/12. The numbers at the top of each bar relate to the number of audits for each grade.

Changes to the proportion of audits reviewed falling within each grade from year to year reflect a wide range of factors, which may include the size, complexity and risk of the individual audits selected for review and the scope of the individual reviews. For this reason, and given the sample sizes involved, changes in gradings from one year to the next are not necessarily indicative of any overall change in audit quality at the firm. In the bar chart above, we have therefore provided summary information over a longer period and, consequently, based on a larger number of audits. This shows the proportion of audits reviewed falling within each grade in the five years up to and including 2013/14. The number of audits within each grade is shown at the top of each bar.

Findings in relation to audit evidence and judgments

Our reviews focused on the audit evidence and related judgments for material areas of the financial statements and areas of significant risk. We draw attention below to findings which the firm should ensure are addressed appropriately in future audits.

The significance of these findings in the context of an individual audit reviewed, and therefore the implications for our grading of that audit, will vary. However, whatever the implications for the specific audits reviewed, we nevertheless include the relevant findings in this report if we consider them important in the broader context of improving audit quality at the firm.

Audit of loan loss provisions

We reviewed the audit of loan loss provisions for two financial services entities.

In both audits we identified issues relating to testing of the collective and individual provisions. These issues included the approach to testing the controls over the identification of impaired loans and other aspects of testing the completeness of the provisions. There were weaknesses in the testing of the loan impairment models and assumptions, used as the basis for the collective provisions, and in the testing of the property valuations used in determining the individual provisions.

Journals testing

Auditing Standards require the auditor to test the appropriateness of journal entries in order to respond to fraud related risks.

We reviewed the testing of journals on 17 audits. In eight of the audits reviewed, the journals were selected manually. In the other nine audits, computer assisted audit techniques were used to select the journals to be tested. We identified weaknesses on 14 of these audits in relation to the selection of journals or the adequacy of the testing, as described below.

In one audit there was no testing of journals for a significant UK component and, in four audits, the journals selected did not cover the full year.

In 10 audits there was insufficient evidence that the selection of journals for testing was appropriately based on fraud risk characteristics or that the journal testing was responsive to the identified fraud risks. In five of these audits, the sample sizes had been pre-determined and did not always include all journals that had been identified as demonstrating fraud risk characteristics. The firm's guidance on journal testing does not adequately cover the selection of journals on the basis of fraud risk, for example whether journals with multiple fraud risk characteristics should be selected for testing.

In addition, for seven of the audits, there was insufficient evidence that the journals selected had been adequately agreed to supporting documentation.

Audit of revenue

We reviewed the audit of revenue on 15 audits. We identified weaknesses on nine of these audits, relating to risk assessment (five audits), substantive analytical review (five audits) and other substantive procedures (six audits).

On one audit the presumed significant risk relating to revenue recognition was rebutted by the audit team, but there was no internal consultation on the matter, as required by the firm's policies. In four other audits the identified significant risk was limited to the recognition of revenue in the correct accounting period and did not adequately consider other fraud related risks relating to revenue recognition.

On two audits the same substantive analytical review was used as the basis of evidence for both sales and cost of sales. On these audits cost of sales was used as the basis for setting an expectation for sales and vice versa and insufficient audit procedures were undertaken for these areas of the financial statements.

The firm issued detailed guidance on the audit of revenue in September 2013, which was after the audits we reviewed were completed. The application of this guidance in practice will be reviewed during our 2014/15 inspection.

Testing of IT controls and reports

We reviewed the audit work relating to IT controls or reports on 15 audits.

In four audits there was no involvement of IT specialists in the audit, as there was no reliance placed on the controls. Unless the audit team assesses the IT environment as "complex”, or identifies a significant system change, the firm only requires there to be a discussion with an IT specialist every three years, to assess whether they need to be involved in the audit. The firm should consider amending this policy in order to ensure that proper consideration is given to whether IT specialists should be involved in the audit.

We identified weaknesses on 10 of these audits relating to the reliance on management's reports or spreadsheets or the testing of IT controls. Auditors often place reliance on management's reports and spreadsheets, where the information has been generated by the IT system, for example to calculate stock valuations or bad debt provisions. On 10 audits there was insufficient testing of those reports or spreadsheets. In addition, on five audits, weaknesses were identified in the audit testing of certain IT general and/ or application controls.

Although the firm has expanded its guidance on both the testing of IT generated reports and IT application controls in the year, the guidance is still limited in a number of respects. The guidance should also be expanded to assist audit teams in respect of the additional audit procedures to be performed where the IT general controls testing was performed at the interim stage of the audit.

Stock count procedures

We reviewed the audit of the stock count procedures on four audits. On all four audits there were weaknesses in relation to the extent of attendance at stock counts, or the audit procedures performed, where the stock was held at multiple locations or where management was undertaking perpetual counts. On one audit, in addition to attending the stock counts at the distribution centres, only two out of 1,200 stores were visited by the audit team to observe and test the stock count procedures. At one of these stores the audit team did not attend at the appropriate time and was, therefore, unable to observe and test the count.

The firm has no guidance on the extent of audit testing required for multiple stock locations or for perpetual counts. Such guidance should be developed by the firm.

Other findings

Errors in the financial statements

On one audit we reviewed, we identified errors in the cash flow statement and in certain notes to the financial statements, which had not been identified by the audit team, nor by the firm's quality control reviews. We requested the firm to investigate the reasons for this, and were informed that the factors included the quality control reviews being undertaken on insufficiently advanced drafts of the financial statements.

2.2 Review of the firm's policies and procedures

The firm's policies and procedures are largely developed globally and the UK firm puts significant resources into implementing them; in particular independence compliance and monitoring procedures, risk assessment, the technical review (Professional Standards Review (“PSR")) function, audit training and technical communications. During the year, the firm continued the implementation of its new audit system, which is due to be substantially completed in 2014.

While emphasising the importance of maintaining or improving quality, the firm's strategy also focuses on revenue growth and cost reduction. The audit strategy was revised in the year and "the Distinctive Audit" was launched. This consists of a package of activities that the firm encourages audit teams to use. The key objectives are stated to be "to improve the quality, distinctiveness and efficiency of audits". The activities include the use of data analytical tools to improve the effectiveness of those procedures, the use of onshore and offshore centres (referred to as "Centres of Excellence" by the firm) and the provision of "enhanced assurance” services to audited entities. We comment separately on the use of offshore centres and the provision of enhanced assurance services below.

Improvements made during the year

The firm has taken a number of actions to address our prior year findings and enhanced its procedures in a number of areas.

The firm's whistleblowing procedures were strengthened.

The firm implemented detailed guidance to respond to the requirements of the revised Auditing Standard on audit reports (ISA UK&I 700) and was the first firm to issue an enhanced audit report, incorporating a more detailed commentary about the audit.

The annual audit training, which is mandatory for audit partners and qualified audit staff, was enhanced, with more input from audit partners.

The annual practice review process, which monitors the quality of audits, was improved. There was an enhancement of the review of the firmwide procedures, with all areas reviewed every year, rather than on a rotational basis.

Prior year findings not adequately addressed

The following prior year findings, both of which have been raised on our last two inspections, had not been adequately addressed by the firm. We expect the firm to take appropriate action to address these matters.

Technical reviews of financial statements

The output of internal technical (“PSR”) reviews of financial statements is not retained and we were, therefore, not able to review this output as part of our inspection of completed audits.

In early 2013, the firm amended its policy, such that any outstanding disclosures and other financial reporting deficiencies identified in the internal technical reviews should be noted on the audit file. However, we have seen little or no evidence that this change is being applied in practice, and more needs to be done to embed this policy.

Methodology - materiality of account balances

The firm's methodology allows account balances, classes of transactions and disclosures higher than overall materiality, if assessed as low risk, to be excluded from audit testing. In 2012, the firm issued some guidance on limiting the extent of this and required these situations to be communicated to Audit Committees. In 2013, the firm added a requirement for the Engagement Quality Control Reviewer (EQCR) to review the rationale for such situations. However, we continue to believe that this aspect of the firm's methodology is inconsistent with the requirements of UK Auditing Standards.

Current year findings

We identified certain further areas, as set out below, where improvements to the firm's policies and procedures are required. In addition, section 2.1 sets out methodology related findings identified in our review of individual audits, in relation to the adequacy of the firm's guidance for the testing of journals, IT controls and reports, and stock-count procedures, which should also be addressed.

Use of offshore centres

The UK firm has recently started to use Deloitte's offshore centre, which is a joint venture between the US and Indian firms (known as “USI”). While this was used on a pilot basis only in 2013, involving less than 1% of UK audit hours, the extent of use is planned to increase in the future.

The firm requires the USI staff to be integrated into the UK audit teams. However, unlike other audit firms, there is no restriction on the nature of the audit work that the USI staff can be involved in, and the firm allows USI staff to be involved in areas of significant risk and those involving audit judgment. We understand that the firm is intending to encourage audit teams to allocate USI staff full sections of the audit, in order to give them a better understanding of the work. Care is needed in adopting such an approach, given that the USI staff do not visit the audited entity and, therefore, may not always have the necessary understanding of the specific risks associated with the audited entity.

The firm's policy and audit manual does not make any reference to the use of the USI centre. While the firm has issued guidance to audit teams, to date this has been limited. There are also aspects of the quality control procedures of the USI centre that require improvement, such as the training and guidance on specific UK requirements. In addition, while the individual audits are within the scope of the firm's practice review, the quality control procedures of the USI centre are not separately assessed as part of the firm's monitoring procedures.

Transparency report – description of the second partner review role

We reviewed the firm's transparency report for the year to 31 May 2013, which was published in August 2013, to assess whether the information in the report was consistent with our understanding of the firm's quality control and independence procedures. Except for the matter set out below, we did not identify any inconsistencies with our understanding of the firm's quality control and independence procedures.

The transparency report (page 8) states that the quality control procedures include "the strategically focused second partner role providing second partner review (focusing on significant risks, significant components and other important audit issues), consultation and audit service support and the IRP acting as a third partner review”. The description of the second partner review role should be clearer. The scope of the role is, in fact, decided by each individual audit engagement partner and can be limited to specific components or areas of the audit.

Independence – enhanced assurance services

Audit teams are being encouraged to identify additional assurance services for audited entities, with an objective being to enhance the value of the audit process to stakeholders. The firm's intranet states that "audit teams will work with clients to assess whether the existing assurance model is sufficient to meet the expectations of stakeholders. They will identify assurance offerings in response to any assurance gaps identified." The services include reviewing the narrative reporting in the front section of the annual report, but also include some advisory related services, such as reviewing an audited entity's governance structure and pre-implementation reviews of systems and controls.

These additional services may create independence threats. While the firm's intranet includes some guidance on the potential independence threats, this is brief. The firm should expand its guidance to audit teams, including distinguishing between audit related services, as defined in the Ethical Standards, and other assurance services, for which appropriate safeguards need to be applied. The guidance should also explain the independence implications for audit personnel introducing these services to audited entities.

Independence – other non-audit services

In cases where the level of non-audit fees for a listed entity, in the financial year, exceeds audit fees, the Ethical Standards require the audit partner to discuss the circumstances with the Ethics Partner. On one audit reviewed by us this was not done, on the basis that the non-audit services were provided before the firm's appointment as auditors. In another case, the discussions were not concluded until after the date of the audit report.

On another audit we reviewed, the firm provided tax advisory services to a listed audited entity, which included advice on transfer pricing arrangements and correspondence with the tax authorities, including defending the entity's position in relation to certain tax disputes. The significance of the independence threats arising, and the effectiveness of the available safeguards, were not adequately assessed by the audit team.

The firm requires the safeguards applied for tax advisory services, where permitted under the Ethical Standards, to include the use of separate tax audit and advisory teams. However, the firm's guidance states that this only applies to staff at senior manager level and above. As a result, audit teams may consider it appropriate to use more junior staff in both the advisory and audit work, even in situations where they are performing the majority of the audit procedures or are taking judgments in the advisory or audit work.

The Ethical Standards require an assessment as to whether informed management exists where there is a potential management threat. The firm's standard audit work programme for consideration of independence matters does not specifically cover this requirement. In addition, there was little or no evidence of this assessment, where relevant, for the audits we reviewed.

Partner performance evaluation – impact of quality review findings

Partner remuneration is based on a standard value per unit. The number of units for each partner increases in line with their progression in the firm, based on the consideration of a number of factors, including quality.

The firm's guidance states that a negative contribution to audit quality should adversely affect partner remuneration. From 2013, the firm introduced a penalty system, in relation to adverse quality review findings for audit partners, in order to formalise the impact on individual partner's remuneration for audits with the lowest grades arising from quality reviews (internal and external).

In addition to this, the firm's policies require further action to be taken for partners with the lowest grades in the firm's internal practice review, such as a review of the partner's portfolio. However, this policy does not apply to partners with the lowest grades arising from external reviews, including any audit partners with recurring adverse findings from AQR reviews.

In 2013, the firm started to require exceptional contributions to audit quality to be recognised through the partner evaluation process. However, we were informed that the impact of this policy was limited to increasing the remuneration of just one UK audit partner. This is partly due to there being no mechanism to identify high quality audit work as part of the firm's practice review, given that the top grade awarded is “compliant”. The firm should do more to recognise high quality audit work, in line with the statement in the transparency report that "we strive to create an environment where achieving high quality is valued, invested in and rewarded".

Partner performance evaluation – review of partner appraisals

During the year the firm issued detailed guidance on appraisals to audit partners and has put significant effort into monitoring partner appraisals. While we have seen an improvement, continued effort is needed to ensure consistency in this area.

Partner promotions – consideration of quality

As part of the partner promotion process, candidates are assessed under a number of categories, including quality. While the partner candidate file requires details of attendance at national training courses (not audit specific), it does not include other standard reports to support the ratings for quality, such as the results of quality reviews, attendance at specific mandatory audit training or other quality metrics. In this respect, the process is not as robust as the annual partner appraisal process.

Staff performance evaluation – review of staff appraisals

The staff appraisal forms focus on the achievement of individual objectives. In our sample of staff appraisals, the objectives in relation to audit quality were often unclear, there was no reference to situations where adverse quality ratings had been given, and most did not refer to other audit quality metrics, such as attendance at mandatory training. The appraisal forms should better facilitate an evaluation of overall performance in relation to audit quality.

Following the firm's internal review of audit staff appraisals, a number were required to be amended to comply with the firm's requirements.

Staff performance evaluation – calculation of staff bonuses

Each office or business unit is allocated a share of the bonus pool and bonuses are then determined by the performance grades. While there are guidelines in respect of the range of bonuses for each grade, these are not comprehensive.

We reviewed the level of bonuses for a sample of staff. This included four individuals who had been involved on audits where adverse AQR findings had been communicated during the appraisal period. Three of these individuals had received an increase in their bonus compared with the prior year. It was not possible to determine if, or how, the level of bonuses were affected by audit quality considerations.

Engagement Quality Control Review (EQCR) - UK component audits

Last year, we assessed one of the audits reviewed by us as requiring significant improvements. The findings largely related to the audit work for a significant UK component of a UK listed group. This had no impact on the EQCR's performance evaluation in this year's appraisal process as he did not consider the component audit to be within the scope of the EQCR's review.

This year, we also assessed one audit as requiring significant improvements, again on the basis of the audit work for certain significant UK components of a UK listed group. There was no evidence that the EQCR had reviewed the relevant audit work for these components. The firm should require EQCRs for group audits to include the work at component level within the scope of their reviews.

Methodology - Letterbox companies

In May 2013, we wrote to the major audit firms regarding concerns arising from our reviews of audits of "letterbox companies" 2 and the need for them to take action to achieve improvements in their approach to such audits.

Deloitte subsequently communicated this to audit personnel and updated its existing guidance and standard work programme. The firm did this by adapting existing guidance, dealing with situations where the audit fieldwork is performed by another Deloitte member firm. However, the amended guidance does not fully address the requirements of relevant Auditing Standards. For example, while the guidance explains that the UK audit team is responsible for the planning and review of the audit, it does not make it clear that it should also be appropriately involved in the performance of the audit work. Clearer guidance needs to be developed for the audit of letterbox companies.

We reviewed the audit of three letterbox companies, which took place before the above mentioned communications. On one of these audits, the audit engagement partner did not visit the country of the entity's head office at the planning stage of the audit. While we were informed that he was involved in planning the audit, there was limited evidence of this. In another audit, the group audit team did not audit the group consolidation, as required by Auditing Standards, as the procedures were performed by the overseas component audit team, with their work reviewed by the group audit team.

Methodology – materiality

The firm's guidance indicates that overall materiality for listed entities should normally be based on a percentage of profit before tax, within a specified range. Auditing Standards allows this to be "normalised” for non-recurring items. However, on five audits we reviewed, the profit before tax was adjusted for items that were recurring in nature, such as the amortisation of intangibles, which appeared to be normal items. The firm's guidance does not specifically cover these types of adjustments and should only permit adjustments to profit for which there is an adequate justification.

Performance materiality is used to determine the extent of audit work undertaken, such as in determining sample sizes, and Auditing Standards require it to be lower than overall materiality. Performance materiality was generally set at a high level, in comparison with overall materiality, on the audits we reviewed this year, as allowed by the firm's methodology. The firm has revised its guidance from 2014 to require consultation for levels of performance materiality above a certain percentage of overall materiality.

Methodology - substantive testing sample sizes for provisions

The firm's methodology does not specifically cover determining samples sizes for provisions. On four audits we reviewed, the sample sizes for the substantive testing of certain provisions were based on the size of the provision. Therefore, a reduction in the provision would have resulted in a smaller sample size, even though the objectives of the testing included assessing the completeness of the provision.

Audit quality monitoring – timing of practice review report

The internal practice review findings were communicated to the global Deloitte team in September 2013, and subsequently to audit personnel, when the process was substantially complete. However, the overall practice review report and individual office reports had not been finalised or provided to us at the time of our inspection. These reports should be completed more promptly.

Audit quality monitoring – practice review of component audits

Deloitte global guidance specifies that the largest component should be included in the practice review when the same partner leads the audits of both the group and largest component.

On the AQR review of one audit, which was also reviewed as part of the practice review, we identified findings concerning the audit of revenue and journals in the largest UK component of this UK listed group, which accounted for over 50% of group revenue. The practice review did not identify these matters, as it had been restricted to the audit work at group level. We were informed that the relevant team leader and reviewer were unaware of the requirement to also cover the audit work for the largest component.

Team leaders and reviewers should be reminded of the Deloitte global policy regarding the review of components, and the practice review database should adequately evidence the review of any components. This would also improve any root cause analysis of the practice review findings.

Andrew Jones Director Audit Quality Review FRC Conduct Division May 2014

Appendix A – Objectives, scope and basis of reporting

Scope and objectives

The overall objective of our work is to monitor and promote improvements in the quality of auditing. As part of our work, we monitor compliance with the regulatory framework for auditing, including the Auditing Standards, Ethical Standards and Quality Control Standards for auditors issued by the FRC and other requirements under the Audit Regulations issued by the relevant professional bodies. The standards referred to in this report are those effective at the time of our inspection or, in relation to our reviews of individual audits, those effective at the time the relevant audit was undertaken.

Our reviews of individual audit engagements and the firm's policies and procedures supporting audit quality cover, but are not restricted to, the firm's compliance with the requirements of relevant standards and other aspects of the regulatory framework. Our reviews place emphasis on the appropriateness of key audit judgments made in reaching the audit opinion together with the sufficiency and appropriateness of the audit evidence obtained. We also assess the extent to which the firm has addressed the findings arising from our previous inspection.

We seek to identify areas where improvements are, in our view, needed in order to safeguard audit quality and/or comply with regulatory requirements and to agree an action plan with the firm designed to achieve these improvements. Accordingly, our reports place greater emphasis on weaknesses identified which require action by the firm than areas of strength and are not intended to be a balanced scorecard or rating tool.

Our inspection was not designed to identify all weaknesses which may exist in the design and/or implementation of the firm's policies and procedures supporting audit quality or in relation to the performance of the individual audit engagements selected for review and cannot be relied upon for this purpose.

The professional accountancy bodies in the UK register firms to conduct audit work. Their monitoring units are responsible for monitoring the quality of audit engagements falling outside the scope of independent inspection but within the scope of audit regulation in the UK. Their work, which is overseen by the FRC, covers audits of UK incorporated companies and certain other entities which do not have any securities listed on the main market of the London Stock Exchange and whose financial condition is not otherwise considered to be of major public interest. All matters raised in this report are based solely on the work which we carried out for the purposes of our inspection.

Basis of reporting

We exercise judgment in determining those findings which it is appropriate to include in our public report on each inspection, taking into account their relative significance in relation to audit quality, in the context of both the individual inspection and any areas of particular focus in our overall inspection programme for the year. Where appropriate, we have commented on themes arising or issues of a similar nature identified across more than one audit.

While our public reports seek to provide useful information for interested parties, they do not provide a comprehensive basis for assessing the comparative merits of individual firms. The findings reported for each firm in any one year reflect a wide range of factors, including the number, size and complexity of the individual audits selected for review which, in turn, reflects the firm's client base. An issue reported in relation to a particular firm may therefore apply equally to other firms without having arisen in the course of our inspection fieldwork at those other firms in the relevant year. Also, only a small sample of audits are selected for review at each firm and the findings may therefore not be representative of the overall quality of each firm's audit work.

The fieldwork at each firm is completed at different times during the year and rigorous quality control procedures are applied. These procedures include a peer review process at staff level and a final review by independent non-executives who approve the issue of all reports. These processes are designed to ensure both a high quality of reporting and that a consistent approach is adopted across all inspections.

We also issue confidential reports on individual audits reviewed during an inspection. While these reports are addressed to the relevant audit engagement partner or director, they are copied to the chair of the relevant entity's audit committee (or equivalent body).

Purpose of this report

This report has been prepared for general information only. The information in this report does not constitute professional advice and should not be acted upon without obtaining specific professional advice.

To the full extent permitted by law, the FRC and its employees and agents accept no liability and disclaim all responsibility for the consequences of anyone acting or refraining from acting in reliance on the information contained in this report or for any decision based on it.

Appendix B – Firm's response

The firm's response is on the following page

Deloitte LLP 2 New Street Square London EC4A 3BZ

Tel: +44 (0) 20 7936 3000 Fax: +44 (0) 20 7583 1198 www.deloitte.co.uk

Direct: +44 (0) 20 7007 3337 Direct Fax: +44 (0) 20 7007 0157 [email protected]

Andrew Jones Audit Quality Review FRC Conduct Division Aldwych House 71-91 Aldwych London WC2B 4HN

14 May 2014

Dear Mr Jones

Public report on the FRC's 2013/14 Audit Quality Inspection: Deloitte response

We are pleased to respond to the public report arising from the FRC Audit Quality Review team's inspection of Deloitte for the year ended 31 March 2014.

We consider that the FRC's report provides a balanced view of the focus and results of its inspection, and we are therefore pleased to record our agreement with its overall conclusions and findings.

Our strategic objective is to execute high quality, distinctive audits. As part of our agenda of continuous improvement we have given careful consideration to each of the FRC's comments and recommendations. This has included investigation of the root causes of each finding. This has enabled us to develop, in conjunction with findings arising from our own quality review procedures, an effective response to the themes arising.

Deloitte's Audit Transparency Reports provide further information regarding our approach to delivering quality and are available on our website.

Yours sincerely

Panos Kakoullis Managing Partner, Audit Deloitte LLP

Deloitte LLP is a limited liability partnership registered in England and Wales with registered number OC303675 and its registered office at 2 New Street Square, London EC4A 3BZ, United Kingdom.

Deloitte LLP is the United Kingdom member firm of Deloitte Touche Tohmatsu Limited ("DTTL"), a UK private company limited by guarantee, whose member firms are legally separate and independent entities. Please see www.deloitte.co.uk/about for a detailed description of the legal structure of DTTL and its member firms.

Member of Deloitte Touche Tohmatsu Limited

Financial Reporting Council 5th Floor, Aldwych House 71-91 Aldwych London WC2B 4HN

+44 (0)20 7492 2300 www.frc.org.uk

-

As disclosed in the annual return to the ICAEW as at October 2013. ↩

-

Letterbox companies are those groups or companies that have little more than a registered office in their country of registration, with management and activities being based elsewhere. In such situations, the auditor is usually based in the country of legal registration, rather than where management is based. ↩