The content on this page has been converted from PDF to HTML format using an artificial intelligence (AI) tool as part of our ongoing efforts to improve accessibility and usability of our publications. Note:

- No human verification has been conducted of the converted content.

- While we strive for accuracy errors or omissions may exist.

- This content is provided for informational purposes only and should not be relied upon as a definitive or authoritative source.

- For the official and verified version of the publication, refer to the original PDF document.

If you identify any inaccuracies or have concerns about the content, please contact us at [email protected].

SME Audit Market Study: Final Report

The FRC does not accept any liability to any party for any loss, damage or costs howsoever arising, whether directly or indirectly, whether in contract, tort or otherwise from any action or decision taken (or not taken) as a result of any person relying on or otherwise using this document or arising from any omission from it.

© The Financial Reporting Council Limited 2026

The Financial Reporting Council Limited is a company limited by guarantee.

Registered in England number 2486368.

Registered Office: 13th Floor, 1 Harbour Exchange Square, London, E14 9GE

Foreword from Director, Strategy and Change

In February 2025, we launched our market study to better understand how effectively the audit market serves the needs of small and medium-sized enterprises (SMEs) and any challenges they may face in securing appropriate audit services. Following engagement with more than 500 stakeholders, across a range of SMEs, capital providers and auditors, we are now publishing our final report.

Overall, our findings present a positive picture. The audit market for SMEs is, in our view, broadly functioning well. In 2024, more than 2,600 audit firms delivered audit services to SMEs, with nearly nine in ten of these audits undertaken by firms outside of the largest six audit firms in the UK. Most SMEs have reported no issues finding an auditor, and those we interviewed described the audit fees they paid as representing good value for money.

This is important because access to high-quality audit helps businesses secure the funding they need to start up, scale up and succeed. For the system to work, investors and lenders must be able to trust the financial information they rely on. Strong audit and reporting standards play a key role in building that trust.

At the same time, these same SMEs feel there are opportunities to make SME audits more efficient and proportionate. In line with the Emerging Findings we published in the summer, we have found there are concerns that the regulatory requirements for delivering SME audits, combined with the supervisory environment for the auditors delivering these services, can lead to more work being done than is necessary relative to the complexity of these businesses.

As new and emerging technologies play an ever greater role in how audits are delivered, we also heard how there can be barriers which inhibit the adoption of these technologies by smaller audit firms, or a lack of clarity on how they can add clear value to SMEs.

In undertaking this study, we looked at the system end-to-end, from how SMEs prepare their accounts to the challenges auditors face in delivering audit services. Addressing the issues identified in this report is not solely for the FRC. The Recognised Supervisory Bodies (RSBs) play an important role in overseeing SME audits, and some aspects of the market will naturally be shaped by competition and commercial dynamics.

However, the FRC can take steps to support the proportionate audit of SMEs through our regulatory role as a standard-setter. Alongside our Emerging Findings, we consulted on guidance to support auditors make full use of the flexibility within auditing standards when auditing smaller and less complex entities. We are publishing this final guidance alongside this report and will be engaging with audit firms to support its implementation, as well as with the RSBs to ensure it is reflected in their inspection approaches.

Stakeholders also expressed interest in the Less Complex Entities (LCE) auditing standard issued by the International Auditing and Assurance Standards Board (IAASB). We will shortly be launching a call for views to understand stakeholders' views on this standard, including on how it could be improved to address concerns which have prevented its adoption in the UK by the FRC. This comes ahead of the IAASB's project to maintain the standard, providing an opportunity for UK stakeholders to influence its future development.

The overwhelming majority of SMEs are not Public Interest Entities (PIEs) and are therefore regulated by the RSBs on the FRC's behalf. We expect the RSBs to take a proportionate and risk-based approach to the supervision of these audits. To support this, we will establish a new working group with the RSBs focused on promoting greater consistency in supervisory approaches to enable proportionate audits. This will also include identifying where steps taken to enhance audit quality in the PIE market may have unintended consequences for smaller audits.

To help smaller audit firms as they explore the adoption of technologies to improve audit quality, later this year we will launch a Technology Sandbox as part of the FRC's Innovation and Improvement Hub. We envisage this Sandbox as providing an opportunity to support them explore, test and critically evaluate new technology within our existing regulatory frameworks.

The publication of this report marks the conclusion of this market study, but does not mark the end of our work. A well-functioning audit market is essential so that SMEs, as engines of innovation and job creation, can continue accessing the audit services they need to secure investment and succeed. While our report has found that this market is functioning well, we have identified issues that, if resolved, can result in meaningful improvements for SMEs and those who provide audit services to them. Our focus therefore turns to implementing those remedies within our remit and continuing to work with others across the system to ensure that the SME audit market continues to work effectively into the future.

Miranda Craig

Director, Strategy and Change

Summary

The audit market for SMEs is, in our view, broadly functioning well with a large number of audit firms providing choice for SMEs, but users and providers feel there are opportunities to deliver SME audits more efficiently. The FRC can support this through our regulatory role as a standard-setter but the RSBs are responsible for supervising the delivery of audits to SMEs and will need to take action too.

The statistics and table below summarise the main findings and remedies by theme for the market study.

At a glance

- c.76,000 SME audits carried out in 202416

- 9 in 10 SME audits were delivered by firms outside the six largest UK audit firms in 2024.16

- £21,200 was the average SME audit fee in 2024, a 4.5% decrease from 2023.16

- 2,638 audit firms active in the SME audit market

- 1,761 completed ten or fewer SME audits : 579 completed one16

- 61% of surveyed SMEs thought their audit fee was fair17 and

- 65% of SMEs considered the audit fee to be reflective of the audit quality (i.e. good value for money).17

| Theme | Finding | Remedies |

|---|---|---|

| Regulatory requirements | There is a perceived lack of scalability of auditing standards and a belief that further support would be useful to aid proportionality in auditing standards. | We have published Practice Note 28: Guidance for audits of small and medium-sized entities, launched a call for views on the LCE auditing standard, and we are undertaking an Audit and Assurance Sandbox project to help in supporting the development of more proportionate scaling of audit requirements to SME audits. |

| Regulatory requirements | The Ethical Standard might impact the ability of SME auditors to provide additional services to their audited entities; but some audit firms may not be taking advantage of the existing exemptions to the Standard's requirements. | We will release further supporting guidance relating to the application of the Ethical Standard and options under the PAASE to enhance better understanding of the standard amongst SME auditors and encourage greater utilisation of these options. |

| Regulatory supervision of SME audits | The existing supervisory framework for SME audits may discourage some auditors from adopting a more proportionate approach to audits leading to additional work being performed. | We will, in collaboration with the RSBs, establish a working group to identify and implement changes to the supervisory approach so there is a more consistent, risk-based and proportionate approach to audit inspection activities across the SME audit landscape. |

| Technology | Smaller audit firms may lack resources and technical knowledge to implement and customise technology. This can limit smaller audit firms' ability to invest in audit-related technology, and if they do, they rely on "off-the-shelf” third-party solutions. | We will, through an upcoming Technology Sandbox, as part of the Innovation and Improvement Hub and other mechanisms, convene discussions relating to technology and its impact on the SME audit market. |

| The audit product | While audits offer value to SMEs, they may not always represent the most proportionate course of action for all SMEs. | We will, through the established working group and in collaboration with the RSBs, develop further supporting materials highlighting the value of audit to SMEs and how best they can utilise and prepare for the audit process to derive further benefits (including efficiencies). |

| Knowledge and resource constraints | Understanding and knowledge of audit varies across the SME audit market. | We will, through the established working group and in collaboration with the RSBs, develop further supporting materials highlighting the value of audit to SMEs and how best they can utilise and prepare for the audit process to derive further benefits (including efficiencies). |

1. Introduction

1This final report presents the findings and remedies from the SME audit market study which was launched in February 2025. This study forms part of our broader campaign to support UK SMEs to access audit services and secure the capital they need for growth.

2The market study focused on understanding: any challenges faced by SMEs in relation to audit and reporting, where audit firms (including smaller firms) have difficulties in auditing SMEs, and the decision-making process for SMEs who procure audit services when otherwise exempt.

3For the purpose of the market study, SMEs in scope are those corporate entities that qualify as small or medium-sized under the Companies Act 2006 definition, as of 6 April 2025, that have not elected to apply any legislative exemptions from audit.1 The thresholds that apply as of 6 April 2025 are:

- Small: turnover of £15m or less, balance sheet total of £7.5m or less, 50 employees or less (meets two of three).

- Medium: turnover of £54m or less and balance sheet total of £27m or less, 250 employees or less (meets two of three).

4We provide further information on SMEs and their auditors in the market overview section but it is important to note that the vast majority of SMEs are not Public Interest Entities (PIEs) and the FRC has therefore delegated oversight authority of these non-PIE audits to the RSBs in the UK. For this reason, the RSBs are key to addressing any issues in the SME audit market.

5This final report builds on the Emerging Findings published in July 2025, drawing on further evidence gathered since then – we refer to this as 'phase two' in this report. Specifically, information was obtained through:

- 17 written responses to the SME Audit Market Study Emerging Findings consultation,

- Nine roundtables and numerous individual meetings with stakeholders, and

- 400 telephonic surveys of SMEs that have undergone an audit, conducted by a commissioned external researcher, with 30 follow-up interviews. Whilst we cannot extrapolate the findings to the entire SME population, this research has provided the FRC with an opportunity to obtain the views of companies not directly within its remit and has been an invaluable source of insight for this study.

6We would like to thank all stakeholders who engaged with us and contributed to the market study.

2. Market overview

7This section presents key data and insights2 related to the SME audit market from 2021 to 2024. The main findings are set out below.

- SME audits make up a significant proportion of all audits carried out in the UK.

- The number of SME audits increased over the period, rising each year from 2021 to 2024.

- The data available to us indicates a large and stable pool of audit firms in the SME audit market between 2021 and 2024, but we are aware that recent growth in private equity investment in audit firms and consolidation may result in fewer audit firms.

- Most surveyed SMEs did not report difficulties in finding an auditor.

- Average SME audit fees appeared to rise steadily from 2021 to 2023 but then decreased between 2023 and 2024.

Overview of the SME audit market including why SMEs have audits

8SME audits comprise a significant proportion of all audits carried out in the UK, with approximately 76,000 SME audits carried out in 2024.3 The number of SME audits has increased year-on-year, from approximately 62,500 in 2021.

9However, the majority of the circa 1.3 million SMEs, namely most micro and small entities, are able to use an exemption from the requirement to obtain a statutory audit. Therefore, any audit these SMEs obtain would be on a voluntary basis.

10The reasons an SME may seek a voluntary audit include, but are not limited to, specific requests from shareholders or stakeholders, in anticipation of growth, and raising capital.

11The SME audit market is diverse. SME auditors range in size and resources, from sole practitioners to some of the largest audit firms in the market. SMEs also vary considerably in size and resources.

SME audit market shares

12Between 2021 and 2024 there was a large and stable pool of audit firms supplying SME audits. Our analysis indicates that 2,638 audit firms were active in the SME audit market in 2024 – a figure that has remained broadly steady between 2021 and 2024. These firms range from the six largest UK audit firms4 to small, local practitioners.

13We are aware that recent developments relating to growing private equity investment in audit firms and consolidation may result in fewer audit firms supplying SME audits. However, we did not gather detailed data and information on these developments during the market study.

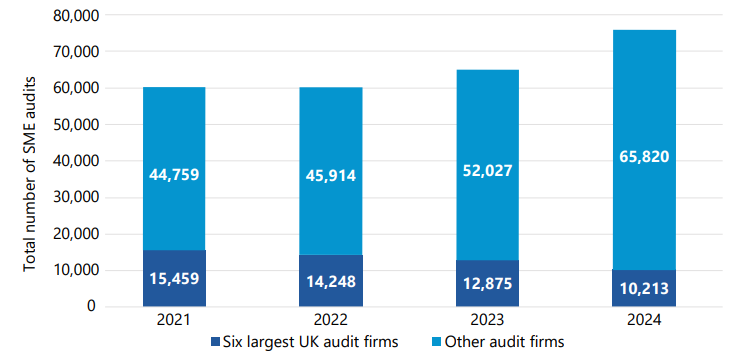

14As shown in Figure 1, the proportion of SME audits carried out by firms from outside the six largest UK audit firms has consistently increased since 2021. Their share of SME audits grew from 74% in 2021 to 87% in 2024.

Figure 1: Number of SME audits completed by the six largest UK audit firms vs other audit firms, 2021-2024

Source: FRC data analysis

SMEs' choice and access to audit

16Our research with SMEs suggests SMEs have good access to audit. Only 10% of SMEs surveyed struggled to find an auditor, of these 2% reported that they faced significant challenges. Conversely, 73% reported no difficulties in finding an auditor (17% of SMEs did not know).

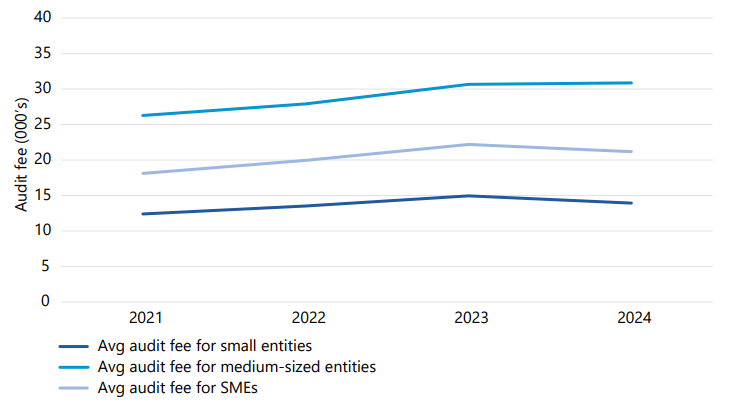

SME audit fees

17According to our data, the average SME audit fee rose between 2021 to 2023 then decreased between 2023 and 2024 (on a nominal basis). In 2024, the average audit fee for SMEs was £21,200. This represents a 4.5% decrease on the previous year.5

18Figure 2 below shows the change in the average SME audit fee between 2021 and 2024 alongside the changes in the average audit fee for small entities and medium-sized entities over this period. While the average audit fee fell for small entities between 2023 and 2024, medium-sized entities continued to see modest audit fee growth in that time, with their average fee rising to £30,900.

Figure 2: Average6 SME audit fees and broken down for small and medium-sized entities, 2021-2024

Source: FRC data analysis

19Our research found SMEs currently consider their audit fees to be fair and largely represent good value for money. To identify their views on audit fees, SMEs were asked to take into account factors such as business complexity, regulatory requirements and company size

3. Findings

20In this section, we set out our key findings. These are broadly consistent with our Emerging Findings, but have been refined to take into account further evidence obtained during phase two of the market study.

21The five themes and key findings are summarised below.

A. Regulatory requirements:

There is a perceived lack of scalability of auditing standards and a belief that further support would be useful to aid proportionality in auditing standards.

The Ethical Standard might impact the ability of SME auditors to provide additional services to their audited entities but some audit firms may not be taking advantage of the existing exemptions to these requirements.

B. Regulatory supervision of SME audits:

The existing supervisory framework for SME audits may discourage some auditors from adopting a more proportionate approach to audits leading to additional work being performed.

C. Technology:

Smaller audit firms may lack resources and technical knowledge to implement and customise technology. This can limit smaller audit firms’ ability to invest in audit-related technology, and if they do, they rely on “offthe-shelf” third-party solutions.

D. The audit product:

While audits offer value to SMEs, they may not always represent the most proportionate course of action for all SMEs.

E. Knowledge and resource constraints:

Understanding and knowledge of audit varies across the SME audit market.

A. Regulatory requirements

Finding: There is a perceived lack of scalability of auditing standards and a belief that further support would be useful to aid proportionality in auditing standards.

22Our Emerging Findings publication noted that audit firms, smaller practitioners and RSBs believed that International Standards on Auditing ('ISAs') are drafted in reference to larger, more complex corporate audits.7 We heard that many stakeholders felt, as a result, auditors struggle to use the scalability provisions in those standards to 'scale' their work when auditing SMEs, and therefore may ‘over-audit'.

23At the same time as we published our Emerging Findings, we also published a draft Practice Note (PN) aimed at assisting auditors to scale audit requirements proportionately for SMEs.8

Evidence we gathered during phase two

24Our research with SMEs indicated that many SMEs desire audits that are faster, simpler and more efficient. Nearly a third of the SMEs surveyed (29%) wanted quicker and more efficient audits. Additionally, about half (52%) of SMEs surveyed believed that existing company law requirements relating to financial audit resulted in excessive costs for their organisations.

25However, as highlighted earlier, our research also indicated that SMEs generally held the view that current audit fees are considered fair; and a large majority (82%) of the SMEs surveyed felt that audit regulations were necessary for stakeholder confidence.

26We received mixed views on the support required to aid proportionality in auditing standards. Many audit firms and some RSBs expressed support for the adoption of the LCE auditing standard.9 However, some expressed concerns over the creation of a two-tier audit system and the effect this would have on the market.

27Many audit firms told us that the market would need greater support in order to ensure the effective implementation of the PN.

-

Some audit firms suggested there is a need for better alignment between regulators (including RSBs), methodology providers and auditors – particularly in relation to the supervision of audits utilising the PN. Without a shared understanding of what is 'proportionate' the PN will be unable to deter 'over-auditing'.

-

Some audit firms suggested that auditors, especially those in smaller firms, may not implement the PN due to concerns over penalisation if their approaches do not align with those of the RSB inspection teams.

- Some audit firms raised concerns that smaller firms may need greater support to fully engage with the PN. They felt smaller audit firms may struggle to devote resources to implementing the PN, in addition to the already lengthy and complex ISAs.

- Some audit firms noted some small firms rely heavily on external methodology providers to interpret and implement auditing standards. Unless these methodology providers updated their methodologies to reflect the PN, it would not achieve its intended effect.

Finding: The Ethical Standard10 might impact the ability of SME auditors to provide additional services to their audited entities but some audit firms may not be taking advantage of the existing exemptions to these requirements.

28Our Emerging Findings noted that many stakeholders consider that the Ethical Standard restricts choice and provision of services to SMEs that are disproportionate to the risk, but there may be a lack of understanding of the Ethical Standard by audit firms.

29We were told that many SMEs face knowledge and resource constraints that may mean they wish to use their auditor for a range of services. SMEs may have small management teams struggling to balance the competing pressures of running their businesses and meeting reporting requirements and auditor expectations. This can often result in SMEs having a preference for their auditor to carry out services beyond a typical audit, given their existing knowledge of their businesses.

Evidence we gathered during phase two

30Audit firms, and those representing audit firms, told us SMEs often expect a broader range of services from their auditors. They said restrictions in the Ethical Standard and the RSB's own Codes of Ethics limit the ability of the auditor to provide these services. However, many of the restrictions that apply are as a result of requirements in UK Company Law and those set by the fundamental principles of the RSB's own Codes of Ethics based on the International Ethics Standards Board for Accountants' (IESBA) Code of Ethics.

31However, our independent research showed SMEs had mixed views on using their auditors for non-audit services. Some SMEs favoured using their existing auditor, due to the efficiencies related to the auditor's strong understanding of their business, and their established relationships. Other SMEs preferred using alternative third-parties, highlighting that separation of services helps preserve audit integrity, reflects existing relationships with alternative providers, and allows access to specialist expertise.

32Many audit firms and RSBs noted that the Ethical Standard creates challenges for small entity auditors when providing additional services to their audited entities. However, views on the scale of these challenges were mixed. Some stakeholders suggested that long association11 and fee dependency12 rules disproportionately affect SME audits; with some suggesting, as a result, there should be significant changes to the standards themselves.13 However, others noted that these challenges could be adequately managed by firms to ensure they can both meet the requirements under the standard, and continue to be flexible in the services they provide to their audited entities.

33Many audit firms, RSBs and an audit methodology provider suggested there was a need for education – particularly for smaller firms – on the Ethical Standard, including the exemptions and alternative provisions available to them. It was also suggested by some audit firms that these exemptions were difficult to understand and there was a need for practical examples.

B. Regulatory supervision of SME audits

Finding: The existing supervisory framework for SME audits may discourage some auditors from adopting a more proportionate approach to audits leading to additional work being performed.

34In our Emerging Findings, we reported many smaller audit firms believe that regulators expect them to do more work for SME audits than may be necessary. Some stakeholders shared their perception that the supervisory framework prioritised compliance and exhaustive documentation over an auditor's professional judgement.

Evidence we gathered during phase two

35We heard RSB-led audit inspections could be made more proportionate. Stakeholders noted that RSBs are responsible for the majority of inspections relating to SMEs.

36Some audit firms, an RSB and a methodology provider noted that the RSB inspections approach is influenced by FRC oversight activities. There was a commonly held view that supervisory inspections utilise checklist-driven reviews which can focus on relatively minor elements of an audit, which do not necessarily have a bearing on audit quality.

37Some audit firms, an RSB and an audit methodology provider suggested further co-ordination between the FRC, RSBs, methodology providers and practitioners to enable a standardised view on what constitutes 'proportionate'. These stakeholders also suggested ensuring inspection feedback be more consistent and focus on ISA (UK) and Ethical Standard requirements rather than subjective expectations focused on better practice associated with larger audits.

38Some audit firms and an RSB emphasised the role of the FRC as an 'improvement regulator' and suggested FRC facilitate further support to enhance SME audit quality. For example, working with RSBs to share thematic insights and examples of good practice to help educate market participants. However, some audit firms noted that the FRC should seek to avoid any guidance forming de facto expectations of firms during audit inspections.

39As part of a potential change in supervisory approach, we also asked stakeholders about a proposal that voluntary audits be exempt from RSB inspections. Most stakeholders, including some RSBs, suggested that it would have a minimal impact on decreasing burden. This is because, in their opinion, there are few 'truly' voluntary audits (most audits of small entities are due to group requirements) and therefore account for a relatively small number of audit inspections.

C. Technology

Finding: Smaller audit firms may lack resources and technical knowledge to implement and customise technology. This can limit smaller audit firms' ability to invest in audit-related technology, and if they do, they rely on “off-the-shelf” third-party solutions.

40In our Emerging Findings, we noted smaller audit firms may lack resources and technical knowledge to implement and customise technology for SME audits. This can result in the firms being highly reliant on third-party technology and may limit innovative approaches to delivering SME audits. It could also reduce the ability of firms to achieve cost efficiencies and fully capitalise on technological advancements.

Evidence we gathered during phase two

41We heard more about how smaller audit firms making use of technology for SME audits rely heavily on third-party software solutions. These third-party providers are an important part of the SME audit market.

42A range of stakeholders reported potential cost barriers for smaller firms to implement technological solutions.

- Smaller audit firms generally have fewer audited entities and engagements than larger audit firms, meaning the return on investment in technology is lower.

- Larger audit firms are more likely to benefit from "volume discounts” offered by software providers, whereas smaller audit firms do not always have the negotiating power or access to such discounts.

- SMEs generally do not expect such technology unless it reduces audit costs or adds clear value.

43A range of stakeholders reported barriers for smaller firms in adopting and customising technology.

- Smaller audit firms often lack the time, desire (based on perceived need), resources, and technical expertise required to tailor these tools effectively, leading many to rely on ready made, off-the-shelf solutions.

- Where customisation does occur, it is typically limited in scope and not sustained over time, with some firms only maintaining tailored methodologies for a single audit cycle.

- Technology available to smaller audit firms is limited, undifferentiated and often of lower service quality or customisation capability than tools used by larger firms.

44In addition, we heard that updates to standards can take several months to be incorporated by technology providers, after which audit firms may need to undertake further internal IT work to ensure full and effective implementation. Many stakeholders, including RSBs, audit firms and methodology providers, also noted concerns around operational disruption, additional costs and the risk that outputs from new tools may be challenged by regulators. Confidence that regulators will accept these tools was said to be critical.

45Our research with SMEs showed that SMEs predominantly rely on Microsoft Office or off-the-shelf tools such as Sage, and prefer cost effective, familiar systems over more advanced functionality. Despite this, SMEs anticipated growth in their use of AI for financial reporting. Some larger SMEs mentioned plans for new reporting and analytics technology.14

D. The audit.15 product

Finding: While audits offer value to SMEs, they may not always represent the most proportionate course of action for all SMEs.

46In our Emerging Findings, we reported that stakeholders had suggested that the costs of an audit could often be disproportionate for smaller SMEs. As such, the cost could outweigh the value added by the audit. Some stakeholders spoke of audits as purely a compliance cost or suggested there should be further exploration of alternatives to audits for SMEs, especially for the smallest of these entities.

Evidence we gathered during phase two

47A range of audit firms and RSBs told us audits were widely viewed as delivering clear value to SMEs. This may be particularly true where financial information is relied upon for lending, capital raising or debt restructuring.

48Some audit firms emphasised that audits provide confidence in the reliability of financial information and internal processes and systems, including for covenant assessments that depend on audited figures. In addition, audits were seen as supporting business resilience and competitiveness and strengthening shareholder confidence in the company's financial position and management.

49We heard that audits were considered more familiar and better understood by SMEs than any alternatives to audits. Some stakeholders told us other forms of assurance were rarely used, even where the latter (such as bespoke reports and contractually agreed procedures) might be useful.

50A range of stakeholders suggested difficulties in implementing alternatives to audit.

- Low market demand.

- Uncertainty over how the market would interpret alternatives.

- The potential that alternative assurance could increase SMEs' cost of capital if not fully understood.

- The risk of significant costs for firms because developing alternative assurance would require new methodologies, compliance work, and staff training.

51Some audit firms and RSBs said SMEs may not fully appreciate the true value of an audit. They suggested clear communications outlining the value (including, but not limited to, improved internal processes and efficiencies) to SMEs may be useful.

52Our research with SMEs identified potential barriers around alternatives to audits. SMEs said that for alternative assurance engagements to be accepted as a substitute for audits, they must be straightforward, cost-effective, and integrate easily into existing operations without causing too much disruption. SMEs also raised concerns about little understanding of what these alternatives would entail, potential difficulties in finding providers, and whether alternatives to audit would meet stakeholder requirements.

53A broad mix of stakeholders agreed that, if demand emerged, a standardised framework clearly defining how alternative assurance compares with an audit would be helpful. They also emphasised the importance of developing targeted engagements with clear guidance, raising awareness of benefits, and improving users' understanding to support informed decisions.

E. Knowledge and resource constraints

Finding: Understanding and knowledge of audit varies across the SME audit market.

54In the Emerging Findings, we reported stakeholder views that, due to resource and time constraints, SMEs may find it challenging to stay up to date with legislative, financial reporting and audit requirements. We also noted that SMEs' limited resources could adversely affect their ability to prepare for audits and/or engage with audit processes, which may result in inefficiencies with SME audits, resulting in higher audit fees and delays.

Evidence we gathered during phase two

55Some audit firms and a methodology provider told us SME owners and finance teams lack technical knowledge of accounting standards. They said SMEs may struggle to prepare forecasts and management assessments (including how to evidence the development of an estimate). Some stakeholders commented on a knowledge gap between what SMEs expect from their auditor, and the services an auditor is able to provide.

56Many stakeholders suggested there should be more practical guidance tailored specifically for SME finance teams to help them better understand how to prepare for an audit. Also, further guidance for SMEs on accounting standards, particularly when these change. One stakeholder suggested exploring sector-specific challenges amongst SMEs and developing targeted guidance.

57Our research with SMEs indicated that further guidance on audit may be helpful. Respondents said they would prefer not to receive any guidance directly from their external auditor, citing concerns about potentially undermining audit integrity.

4. Remedies and next steps

58In this section, we set out remedies that respond to our findings.

59In identifying and developing these remedies, we have been mindful that the FRC alone cannot address the issues identified in the SME audit market. The RSBs have a critical role to play because the overwhelming majority of SMEs are not PIEs so their audits are regulated by the RSBs on the FRC's behalf. Moreover, some issues in the market may also not be fully in the gift of the FRC or RSBs to address and will be subject to market forces.

60We have also taken into account that SMEs and their auditors vary considerably in size. Some of our remedies may therefore be more applicable to some parts of the SME audit market than others.

61Our suite of remedies is summarised below. In addition to implementing these remedies, we will continue to monitor developments in the market as part of ongoing market monitoring work.

- We have published Practice Note 28: Guidance for audits of small and medium-sized entities, we will shortly launch a call for views on the LCE auditing standard, and we are undertaking an Audit and Assurance Sandbox project to help in supporting the development of more proportionate scaling of audit requirements to SME audits.

- We will release further supporting guidance relating to the application of the Ethical Standard and options under the PAASE to enhance better understanding of the standard amongst SME auditors and encourage greater utilisation of these options.

- We will, in collaboration with the RSBs, establish a working group to identify and implement changes to the supervisory approach so there is a more consistent, risk-based and proportionate approach to audit inspection activities across the SME audit landscape.

- We will, through an upcoming Technology Sandbox, as part of the Innovation and Improvement Hub and other mechanisms, convene discussions relating to technology and its impact on the SME audit market.

- We will, through the established working group and in collaboration with the RSBs, develop further supporting materials highlighting the value of audit to SMEs and how best they can utilise and prepare for the audit process to derive further benefits (including efficiencies).

Remedy 1: We have published Practice Note 28: Guidance for audits of small and medium-sized entities, we will shortly launch a call for views on the LCE auditing standard, and we are undertaking an Audit and Assurance Sandbox project to help in supporting the development of more proportionate scaling of audit requirements to SME audits.

62Alongside this final report, we have published Practice Note 28 Guidance for audits of smaller and medium-sized enterprises with the objective of assisting auditors to scale ISAs (UK) requirements to these smaller entities. This will play an important part in encouraging more proportionate audits.

63Whilst we disagree with the view that ISAs (UK) are not scalable, we believe that more can be done to assist auditors to have the confidence to scale their audits proportionately for less complex SMEs and we are of the opinion that the PN will achieve this objective.

64We will shortly launch a call for views to seek additional views from stakeholders on the LCE auditing standard to inform our response to the IAASB's upcoming consultation on revisions to and maintenance of the standard. This will support our engagement with the IAASB as part of its project, and with other national standards setters and regulators.

65We have also launched an Audit and Assurance Sandbox project on materiality for less complex entities. This will encourage the exploration, with audit firms, of the challenges they face in materiality setting in audits of less complex entities and facilitate improvements in their methodologies. These could include encouraging audit firms to reassess their materiality levels and whether alternative, more efficient, procedures could be used.

66In addition, by the end of 2026, we will establish a working group consisting of representatives of RSBs, including their inspection groups, and the FRC. This will help to facilitate the embedding of the PN into the supervision of SME audits. This working group is discussed further under Remedy 3.

Remedy 2: We will release further supporting guidance relating to the application of the Ethical Standard and options under the PAASE to enhance better understanding of the standard amongst SME auditors and encourage greater utilisation of these options.

67In 2026, we will work with various stakeholders, including the RSBs, to identify misunderstandings relating to the Ethical Standard and, where relevant, application of the PAASE. We will then develop additional supporting and educational materials to address these misunderstandings to help SME auditors understand the options available to them.

68While we recognise that SME auditors face challenges, we do not consider these to be insurmountable. Our Ethical Standard is closely aligned with IESBA's Code of Ethics. Maintaining this alignment is important for strengthening trust in UK audit quality and financial reporting, as well as supporting consistency and comparability across jurisdictions.

69An independent audit is a legal requirement under the Companies Act 2006 and is fundamental to audit quality. The Ethical Standard requirements to address threats to independence play a key role in supporting this objective. Further, some of the issues raised by stakeholders do not actually impact SMEs and may arise from the respective RSBs' Codes of Ethics and the international Code of Ethics set by IESBA. We therefore do not propose to make any amendments to the FRC's Ethical Standard, but do consider that additional supporting guidance may provide further clarification and support to smaller audit firms in applying the PAASE ethical requirements for the audits of smaller entities.

Remedy 3: We will, in collaboration with the RSBs, establish a working group to identify and implement changes to the supervisory approach so there is a more consistent, risk-based and proportionate approach to audit inspection activities across the SME audit landscape.

70In the second half of 2026, we will establish a new working group, consisting of representatives from the RSBs and our Professional Bodies Supervision team. This working group will build on our strong working relationships with RSBs, with a focus on ensuring consistency in supervisory approaches taken by RSBs, particularly in respect to enabling proportionate audits. This will also include identifying, and working to address, where steps taken to enhance audit quality in the PIE audit market may have unintended consequences for smaller audits.

71By the end of 2026, the working group will aim to ensure that the PN is embedded within all RSB inspection methodologies on an ongoing basis. This working group may also identify new areas relating to SME audits where stakeholders need additional support. This information will be shared with relevant policy teams at the FRC and RSBs to help identify any further actions that could be taken.

72In the first half of 2027, we intend to report on the activities of the working group. The report will set out the activities undertaken to date, as well as planned future actions.

73This working group will complement our existing Future of Audit Supervision Strategy ('FASS') project. FASS aims to evolve our supervision approach to be more proportionate, and capable of being applied across the entire audit market. Whilst the initial piloting for FASS will focus on the larger more complex firms in our remit, over time we anticipate that the FASS approach will benefit the entire audit market, including the RSBs' supervision of SME audits.

74Through FASS we have already begun seeking, in collaboration with RSBs, to identify how RSBs may implement a more risk-based approach to their supervision of SME audits. This will focus on how RSBs, working with the FRC's Professional Bodies Supervision team, can make their inspection methodologies more proportionate, with a focus on the more material risks and complex elements of an audit.

Remedy 4: We will, through an upcoming Technology Sandbox, as part of the Innovation and Improvement Hub and other mechanisms, convene discussions relating to technology and its impact on the SME audit market.

75In 2026, we will launch our Technology Sandbox, part of our Innovation and Improvement Hub. We will invite submissions from firms working in the SME audit market who are seeking to adopt technology to improve their audit quality. This will provide opportunities to support smaller audit firms exploring, testing and critically evaluating new technology within our regulatory frameworks. We will publish updates on the progress of this sandbox.

76To date, we have supported the adoption of technology and innovation to support audit quality through our research, supervision and guidance activities, including publishing a thematic review of the certification of automated tools and techniques and our AI in audit guidance in 2025.

77We will continue to monitor and track technological developments, including Artificial Intelligence, to better understand the evolution of the market.

78However, as we have seen, other stakeholders play a crucial market shaping role, as SME audits rely heavily on third-party software solutions. As a result, our role needs to be focused on convening discussions with stakeholders, including these third-party technology suppliers. In our view, based on the findings of these discussions, smaller audit firms may also benefit from further supporting and educational materials. We will, therefore, encourage RSBs to develop these materials.

Remedy 5: We will, through the established working group and in collaboration with the RSBs, develop further supporting materials highlighting the value of audit to SMEs and how best they can utilise and prepare for the audit process to derive further benefits (including efficiencies).

79By the end of 2026, we will encourage RSBs to develop further supporting materials relating to the value of audit. These could help SMEs to better understand what an audit entails, its value, and to better prepare for the audit process.

80Where relevant, we will seek, in collaboration with RSBs, to work with SMEs in developing any materials. We may engage with SMEs after the release of any supporting materials to assess their impact.

81Any further materials would build on our existing supporting material to help SMEs confidently and effectively engage with the annual audit process.

Financial Reporting Council

London office:

13th Floor, 1 Harbour

Exchange Square,

London, E14 9GE

Birmingham office:

5th Floor, 3 Arena

Central, Bridge Street,

Birmingham, B1 2AX

+44 (0)20 7492 2300

www.frc.org.uk

Follow us on LinkedIn

Footnotes

-

The Companies Act 2006 provides exemptions, in certain circumstances, for certain small (as defined) companies and qualifying subsidiaries. See UK Government website. ↩

-

We have obtained data relating to SME audits from a range of sources including from an independent, third-party research firm. Given the nature of the data available to us on SMEs, we are not able to triangulate all datapoints used. As such, some of these data should be interpreted with a degree of caution. ↩

-

While the new thresholds effective from 6 April 2025 have been applied to most of the work in the study, the data analysis relates to the 2024-year end to provide a complete picture of the market over a full year. Therefore, the thresholds in place prior to 6 April 2025 were applied: * Small: turnover of £10.2m or less, balance sheet total of £5.1m or less, 50 employees or less (meets two of three). * Medium: turnover of £36m or less, balance sheet total of £18m or less, 250 employees or less (meets two of three). ↩

-

The FRC categorises the six largest audit firms in the UK based on market share of the UK Public Interest Entity and Major Local Audit markets. The six largest audit firms in the UK in 2024/25 were: BDO LLP, Deloitte LLP, Ernst & Young LLP, KPMG LLP, Forvis Mazars LLP and PricewaterhouseCoopers LLP. ↩

-

For context, audit fees for companies in the FTSE 350 averaged around £3.9 million in 2024. ↩

-

A 2% winsorised mean is used instead of a simple average. This is used because it reduces the influence of extreme outliers, providing a more robust and representative measure when working with large datasets. ↩

-

The ISAs are globally recognised standards for the auditing of financial statements developed by the IAASB. They provide a structured framework for auditors to plan, assess risks, gather evidence and report audit findings; and enable comparability between audits in different jurisdictions. ↩

-

Many stakeholders, inclusive of audit firms, RSBs and methodology providers, shared their views on the PN and its ability to meet stakeholder needs. A detailed overview of stakeholder feedback can be found in the dedicated PN Feedback Statement and Impact Assessment - Practice Note 28: Guidance for audits of small and medium-sized entities here. ↩

-

The LCE auditing standard is an auditing standard developed by the IAASB which is designed for smaller and less complex businesses. We have provided a fuller statement on our position in relation to the LCE auditing standard in our Feedback Statement and Impact Assessment - Practice Note 28: Guidance for audits of small and medium-sized entities, which is available here. ↩

-

Revised Ethical Standard 2024 for auditors. The Ethical Standard sets out the principles and requirements auditors must follow to maintain integrity, independence and objectivity. To achieve this objective, it limits the non-audit services auditors may provide to their audited entities. Section 6 - Provisions Available for Audits of Small Entities (PAASE) - offers additional flexibility for small entity audits. Nonetheless, stakeholder feedback indicates that some SME auditors do not fully use these exemptions. ↩

-

'Long Association' refers to rules within the Ethical Standard which aim to reduce the risk that an auditor becomes overfamiliar with, or insufficiently independent from, management after many years of the same audit. It should be noted that for unlisted SMEs, the only long association requirement is for them to consider threats to independence after an engagement partner has been in place for 10 years as engagement partner and to then identify any relevant safeguards. So, smaller audit firms conducting SMEs gain great benefit from the relevant long association rules. ↩

-

'Fee Dependency' relates to rules which prevents auditors from becoming financially reliant on a single audited entity, because high dependence on one entity's fees can threaten auditor independence. ↩

-

It should be noted that the FRC's Ethical Standard is closely aligned with the IESBA Code of Ethics. Maintaining this alignment is important for strengthening trust in UK audit quality and financial reporting, as well as supporting consistency and comparability across jurisdictions. ↩

-

For the context of this market study, the term "technology" refers to digital tools and systems that improve the quality, efficiency, and consistency of audits by supporting key stages such as planning, risk assessment, evidence gathering, and reporting. Tools include all-in-one engagement platforms, reporting, audit automation & analytics, client collaboration portals and data collection platforms. ↩

-

In the UK, an audit could be a legal requirement (a statutory audit) or obtained voluntarily despite there being no legal requirement for an entity to obtain one. In this section, an 'audit' means one obtained regardless of legal requirement to do so. ↩

-

Data obtained from a third-party research firm; these findings may not be representative of the overall SME audit market. ↩↩