The content on this page has been converted from PDF to HTML format using an artificial intelligence (AI) tool as part of our ongoing efforts to improve accessibility and usability of our publications. Note:

- No human verification has been conducted of the converted content.

- While we strive for accuracy errors or omissions may exist.

- This content is provided for informational purposes only and should not be relied upon as a definitive or authoritative source.

- For the official and verified version of the publication, refer to the original PDF document.

If you identify any inaccuracies or have concerns about the content, please contact us at [email protected].

Supplier finance arrangement disclosures

Appendix 2: Supplier finance arrangement disclosures

Background

Supplier finance arrangements, also called supply chain finance (SCF), are a type of financing transaction, originated by the purchaser, where the seller is able to factor their receivables to a finance provider to receive cash before the purchaser pays. The FRC Lab report: Disclosures on the sources and uses of cash previously noted that investors had expressed concern over the lack of transparency around the use of supplier finance arrangements and called for disclosure of the use of such arrangements, to allow a better understanding of the risks faced by companies.

The IASB has issued Supplier Finance Arrangements (Amendments to IAS 7 and IFRS 7), effective for periods beginning on or after 1 January 2024, which requires additional disclosures about supplier finance arrangements, complementing an earlier IFRS IC agenda decision. 1

The amendments to IAS 7 contain two new disclosure objectives, to provide information to enable users: to assess how supplier finance arrangements affect liabilities and cash flows, and to understand the effect of such arrangements on liquidity risk.

The disclosure objectives are supported by specific disclosure requirements including disclosing the amount of financial liabilities subject to supplier finance arrangements, the amount for which the supplier has already received payment, and the range of payment due dates for both amounts subject to supplier finance arrangements and comparable trade payables not subject to such arrangements.

Disclosure of supplier finance arrangements has been an area of focus for the FRC for some time, with our thematic review of Cash Flow and Liquidity Disclosures (November 2020) providing guidance and examples of better practice. Updated examples of better practice for the new disclosure requirements have been provided in this thematic review.

Scope

We conducted a limited scope review of the supplier finance arrangement disclosures of ten UK companies for compliance with the new IAS 7 and IFRS 7 disclosure requirements.

As our selection was identified through key-word searches of disclosures provided, this review was not able to identify companies that failed to provide any disclosure of SCF arrangements. We therefore remind companies and auditors of the importance of providing high quality disclosures in this area.

We have provided some examples of the better disclosures that we identified from our reviews. Companies will need to consider the materiality of these matters based on their own circumstances in determining what information to disclose, and in how much detail.

Findings

We were pleased to find that of our selection of companies which used SCF, all companies provided information about the use of these arrangements to meet the new disclosure objectives in IAS 7, with the majority of companies providing all required disclosures.

Where particular disclosures were not provided, this appeared to be based on materiality judgements. We recognise that determining the appropriate amount of information to disclose for SCF arrangements may be particularly judgemental, with preparers and users previously stating that information about the use of such arrangements can be material by nature, even if the amounts are not significant. 2

As well as reviewing the current year disclosures for compliance with the IAS 7 and IFRS 7 amendments, we also conducted a comparison of the current year disclosures with the disclosures provided in the prior year, both for our selection and for a further 16 companies.

Examples of better disclosures provided to meet the disclosure objectives of the standard included:

- Descriptions of how and why SCF arrangements are used;

- Clear explanation of the nature and terms of the arrangements, using standardised terminology;

- How the use of such arrangements impacts the cash flows and liquidity position during the period, including the impact on key cash flow metrics; and

- How the use of SCF impacts the liquidity risks of the company and how this is managed.

We were pleased to note that, while the majority of these 26 companies provided additional disclosures to comply with the new disclosure requirements, almost all companies in this extended selection provided disclosure of the use of supplier finance arrangements in the prior year, showing there was already a good standard of transparency and disclosure in this area, supporting user needs and confidence in UK companies.

Key recommendations

When drafting their upcoming annual reports, we encourage companies to consider our key recommendations:

- Continue to provide high quality disclosures of the use of SCF arrangements, proportionate to the risks faced, to meet user needs;

- Explain how SCF impacts the liabilities and cash flows of the company, including disclosing any accounting judgements, if relevant; and

- Describe the impact of SCF arrangements on liquidity risk and explain how this is managed.

Financial review (extract)

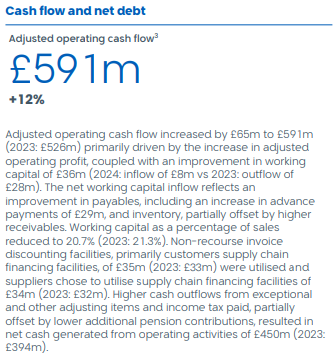

Cash flow and net debt

Adjusted operating cash flow increased by £65m to £591m (2023: £526m) primarily driven by the increase in adjusted operating profit, coupled with an improvement in working capital of £36m (2024: inflow of £8m vs 2023: outflow of £28m). The net working capital inflow reflects an improvement in payables, including an increase in advance payments of £29m, and inventory, partially offset by higher receivables. Working capital as a percentage of sales reduced to 20.7% (2023: 21.3%). Non-recourse invoice discounting facilities, primarily customers supply chain financing facilities, of £35m (2023: £33m) were utilised and suppliers chose to utilise supply chain financing facilities of £34m (2023: £32m). Higher cash outflows from exceptional and other adjusting items and income tax paid, partially offset by lower additional pension contributions, resulted in net cash generated from operating activities of £450m (2023: £394m).

Weir Group PLC, Annual Report and Accounts 2024, p44

The company provides narrative explanation of the usage of SCF schemes in clear language.

Tabular disclosure is provided for the carrying amount subject to SCF, amounts paid and details of payment due dates.

Narrative is also provided on the impact of other factors such as business combinations, FX and non-cash movements.

The company quantifies the impact of supplier finance arrangements on adjusted operating cash flows.

21. Trade and other payables (extract)

Liabilities under supplier finance arrangements Trade payables includes balances due to suppliers that have signed up to a supply chain financing programme, under which all invoices are settled via a partner bank. Supplier finance arrangements are characterised by one or more finance providers offering to pay amounts that an entity owes its suppliers and the entity agreeing to pay according to the terms and conditions of the arrangements at the same date, or a date later than, when suppliers are paid These arrangements provide the entity with extended payment terms, or the suppliers with early payment terms, compared to the related invoice payment due date. The value of the liability payable by the Group remains unchanged.

| 2024 | |

|---|---|

| Range of payment due dates | |

| Liabilities under supplier finance arrangements | 90-120 days after invoice date |

| Comparable trade payables that are not part of the supplier finance arrangements (same line of business) | 0-90 days after invoice date |

| Carrying amount of liabilities under supplier finance arrangement | £m |

| Liabilities under supplier finance arrangement | 99.6 |

| Of which the supplier has received payment from the finance provider | 34.0 |

There were no material business combinations or foreign exchange differences that would affect the liabilities under supplier finance arrangements in the period. There were no non cash transfers from trade payables to liabilities under the supplier finance arrangements.

Weir Group PLC, Annual Report and Accounts 2024, p200

18. Other financial liabilities – group and company (extract)

(a) During 2024, the Group agreed with certain suppliers to extend the payment periods for certain invoices in respect of property, plant and equipment ("PPE") and smart meter installation services. By virtue of the supplier financing arrangements agreed, the suppliers may choose to receive payment from a bank prior to the due date of the invoices. The arrangement does not introduce any additional collateral, guarantees or security.

The payment periods for the PPE invoices were extended from between 30 and 60 days to 180 days compared to normal terms of between 30 and 90 days for similar invoices. The payment periods for the smart meter installation service invoices were extended from 30 days to 90 days compared to normal terms of 30 days for similar invoices.

The Group has determined that, as the extended payment terms negotiated with the suppliers are beyond the normal terms agreed with other suppliers and the Group is required to pay a fee representing the supplier's cost of offering the extended terms, the appropriate presentation of the £68 million (2023 £204 million) outstanding under these supplier finance arrangement is Other financial liabilities in the Consolidated statement of financial position, rather than Trade and other payables. As at 31 December 2024, the suppliers party to these agreements had already received payment of £68m (2023 £204m) from the bank.

The Group had cash outflows in the year in respect of invoices under supplier financing arrangements of £219 million (2023 £5 million).

A description of how the Group manages the liquidity risk inherent in this supplier financing arrangement is set out at Note 11(e)C1.

Scottish Power UK PLC, Annual Report 2024, p122

The company provides narrative disclosure of the reasons for the arrangement, the key terms and payment due dates.

An explanation is provided of the company's assessment of the appropriate accounting presentation within liabilities.

Further information is provided about the cash impact in the year, and a cross reference is provided to further disclosures about liquidity risk and how it is managed.