The content on this page has been converted from PDF to HTML format using an artificial intelligence (AI) tool as part of our ongoing efforts to improve accessibility and usability of our publications. Note:

- No human verification has been conducted of the converted content.

- While we strive for accuracy errors or omissions may exist.

- This content is provided for informational purposes only and should not be relied upon as a definitive or authoritative source.

- For the official and verified version of the publication, refer to the original PDF document.

If you identify any inaccuracies or have concerns about the content, please contact us at [email protected].

TAC Public Meeting November 2025 Paper 8: GHG Scope 2 Initial analysis

Executive summary

| Field | Value |

|---|---|

| Date | 11 November 2025 |

| Paper reference | 2025-TAC-052 |

| Project | GHG Protocol Revisions |

| Topic | Scope 2 Guidance consultation – initial analysis |

Objective of the paper

This paper provides a summary and an initial analysis of the proposed revisions to the GHG Protocol's Scope 2 Guidance (2015). This paper also notes a second consultation that is requesting feedback on consequential accounting methods for the electricity sector.

Decisions for the TAC

The TAC is asked to provide views on the initial analysis of the proposed revisions to the Scope 2 Guidance.

The TAC is asked whether it agrees to not respond to the second consultation regarding consequential accounting methods for the electricity sector.

Appendices

Appendix 1 - Consultation questions for the proposed revisions to the Scope 2 Guidance

Committee (TAC) to discuss in a public meeting. This paper does not represent the views of the TAC or any individual TAC member.

This publication contains copyright material of the IFRS Foundation® (Foundation). All rights reserved. Reproduced and distributed by the Financial Reporting Council (FRC) in its role as the secretariat for the UK Sustainability Disclosure Technical Advisory Committee (TAC) with the permission of the Foundation. No rights granted to third parties without permission of the Foundation and the TAC. For more information about the Foundation and the rights to use its materials please visit www.ifrs.org

Context

1On 20 October 2025, the GHG Protocol released proposed revisions to the Scope 2 Guidance (2015) for a 60-day public consultation. The deadline for responses is 19 December 2025. This is the first publication of an ongoing process to update the Scope 2 Guidance1. A second public consultation on additional Scope 2 related topics will follow in 2026, with final publication of the new document expected in 2027.

2On the same day, the GHG Protocol also released a request for feedback on consequential accounting methods for estimating avoided emissions from electricity-sector actions. This deadline for these responses is also 19 December 2025.

3The TAC is asked to consider providing feedback to the GHG Protocol on the proposed revisions to the Scope 2 Guidance and its request for views on consequential accounting methods, especially as they relate to the implementation of UK SRS S2.

4Some of the questions in the consultation are designed specifically for preparers of GHG inventories with deep technical knowledge, and it may not be appropriate for the TAC to comment. The Secretariat is continuing to engage with appropriate UK stakeholders to develop the response to the GHG Protocol and therefore some of the points in this paper might evolve as we receive stakeholder feedback.

5This paper is split into four parts so that the TAC can systematically address all the relevant points in the consultation.

Scope 2 guidance update

Summary of revisions

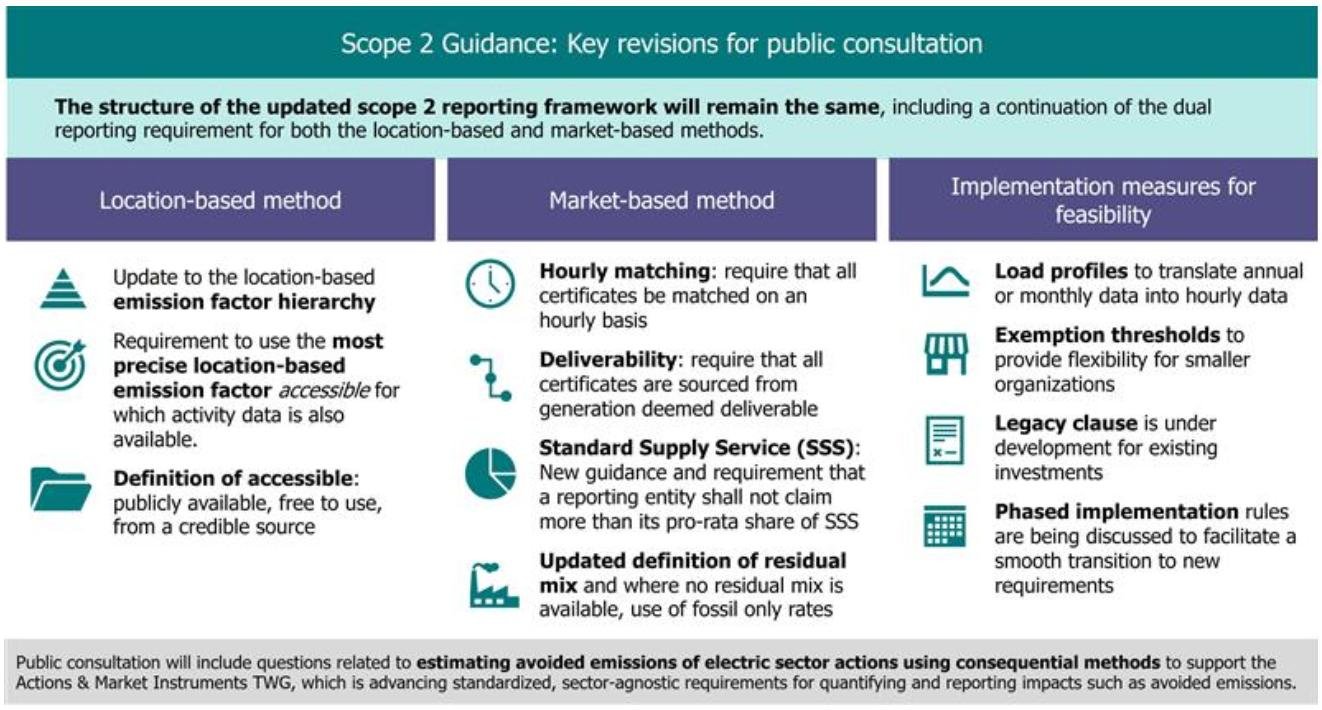

6The GHG Protocol have proposed a number of revisions to the Scope 2 Guidance relating to the location-based method (LBM) and market-based method (MBM) which includes implementation measures for feasibility. These amendments are summarised in the diagram below.

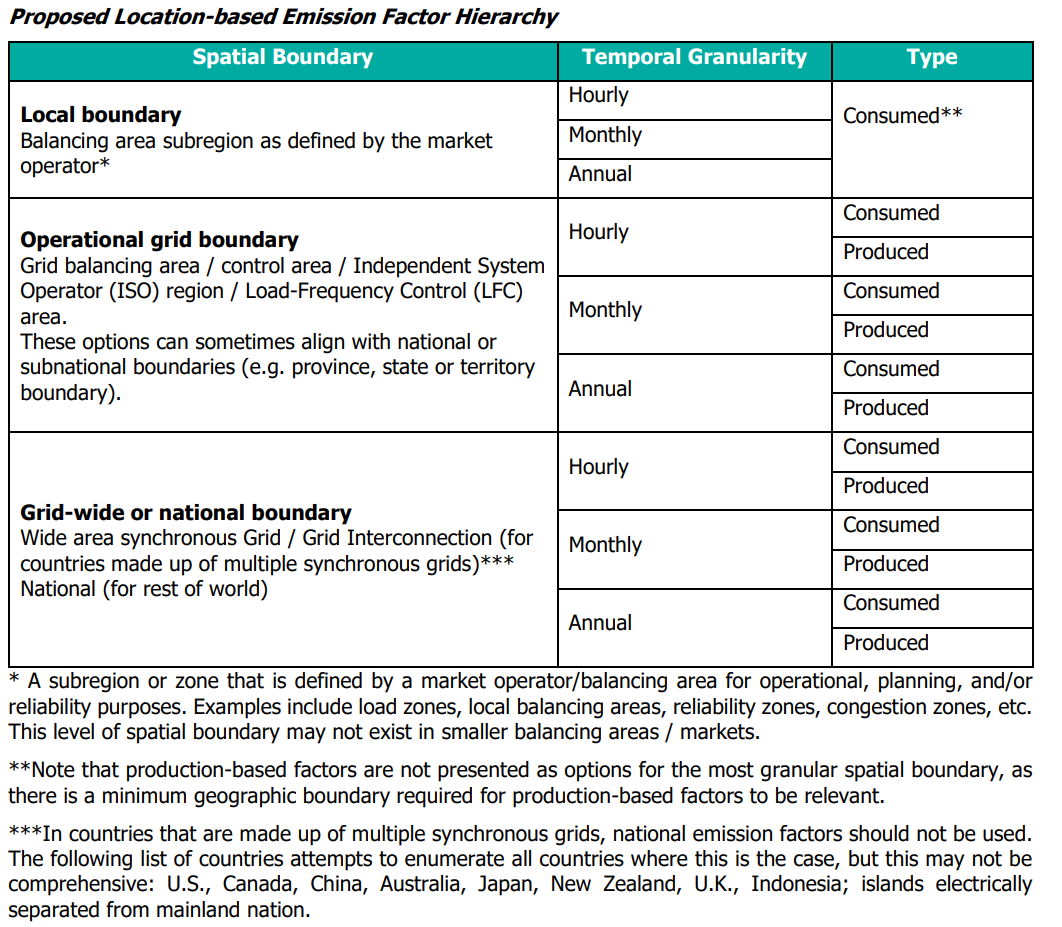

Source: GHG Protocol, Upcoming Scope 2 Public Consultation: Overview of Revisions

Source: GHG Protocol, Upcoming Scope 2 Public Consultation: Overview of Revisions

| GHG Protocol

7The dual location-based and market-based methods have been retained, and the proposed revisions are expected to introduce targeted improvements to enhance the accuracy and transparency of both the LBM and MBM.

8Notably, one of the key proposed revisions is a new hourly matching and deliverability requirement for MBM which is designed to align claims with the time and place electricity is consumed. This proposal is intended to reduce double counting and provide a more accurate depiction of the power grid and energy consumption.

9The proposed revisions also include multiple measures to help companies manage the changes to the Scope 2 Guidance, if they are ultimately approved. These measures include permitting the use of load profiles to approximate hourly data, exemption thresholds, a legacy clause for existing contractual arrangements, and a multi-year phased implementation timeline.

Impact on implementation of UK SRS S2

10It is important to note that whilst IFRS S2 and draft UK SRS S2 require the use of the GHG Protocol Corporate Standard (2004), they don't reference or require the use of the Scope 2 Guidance. However, companies that use the GHG Protocol Corporate Standard are likely to use the Scope 2 Guidance when collecting and disclosing their Scope 2 emissions. Additionally, there is an assumption that companies that apply the Corporate Standard will also need to apply the supplementary guidance and standards to be compliant with the Corporate Standard (although this is not specifically stated). Despite not being required to be used, the Scope 2 Guidance is an important document in the calculation of Scope 2 emissions, and therefore the TAC should strongly consider providing feedback to the GHG Protocol, especially in relation to its expected use with IFRS S2 and draft UK SRS S2.

11Although it is not referenced in IFRS S2, the ISSB decided to incorporate, as requirements, the two calculation methods in the Scope 2 Guidance. Notably, IFRS S2 requires the disclosure of Scope 2 location-based data. However, rather than requiring the disclosure of Scope 2 market-based data, IFRS S2 requires companies to 'provide information about any contractual instruments that is necessary to inform users' understanding of the entity's Scope 2 greenhouse gas emissions' (IFRS S2 Paragraph 29(a)(v)). Although feedback from the IFRS S2 Exposure Draft suggested that stakeholders would prefer the disclosure of both LBM and MBM, the ISSB decided not to require market-based data due to the significant variations in the mechanisms that could be used, and the range of maturity of the market in which a company operates. (IFRS S2 Basis for Conclusions Paragraph BC 109). It is assumed that requiring the disclosure of market-based data is unnecessary, as a company that enters into an agreement is likely to want to disclose its market-based data to demonstrate the actions it has taken to reduce its Scope 2 emissions.

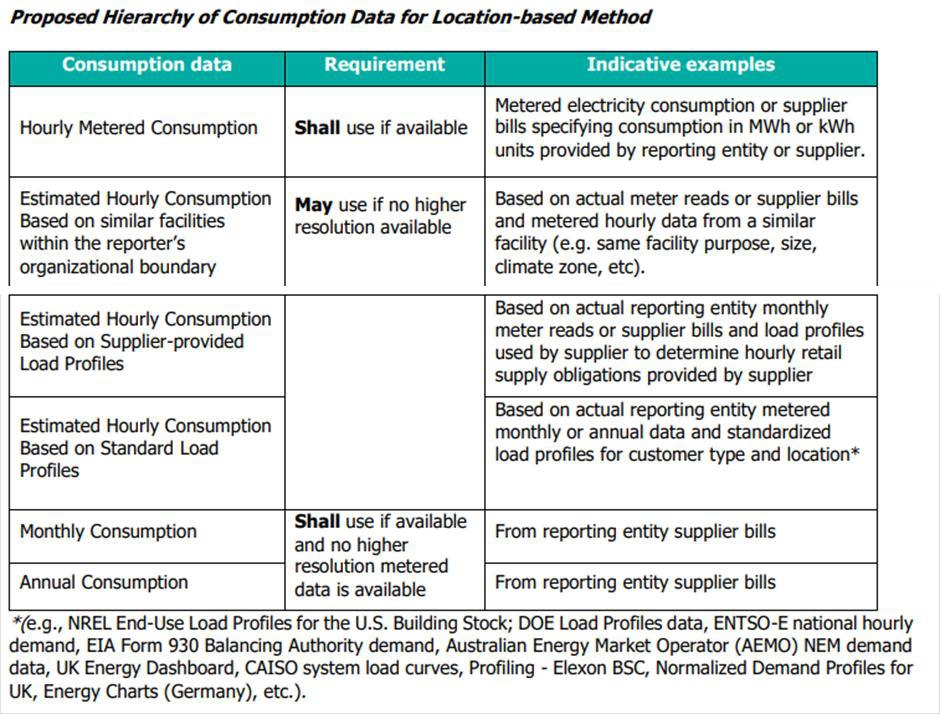

12Generally, the proposed revisions to the Scope 2 Guidance are designed to provide greater rigour in the way Scope 2 emissions are calculated. This should ultimately improve the accuracy and reliability of the data which is a positive step. In general, an evolution of the methodologies is welcomed, especially to reflect updated scientific understanding and to improve the quality of disclosure.

13However, as we learnt when providing endorsement recommendations on IFRS S1 and IFRS S2, there are already concerns from stakeholders around the availability and cost of data. The proposed revisions to the Scope 2 Guidance are likely to increase costs for companies, and there may be some concerns about market readiness and whether there are sufficient technological solutions that make the proposals feasible.

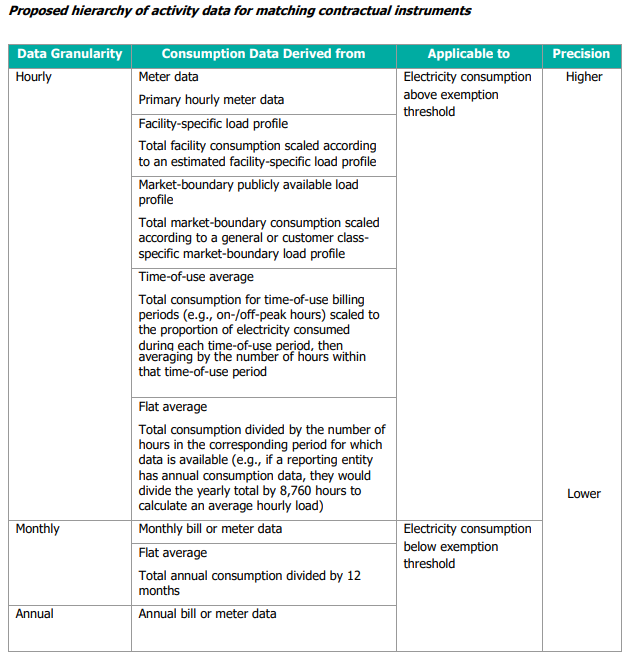

14The Secretariat will continue to engage with stakeholders to better understand any concerns regarding feasibility and cost of the proposed revisions.

Other UK considerations

15The UK has mandatory GHG emissions requirements through the Streamlined Energy and Carbon Reporting (SECR) regulations, including:

- The Companies Act 2006 (Strategic and Directors' Reports) Regulations 2013 quoted companies have been required to report their annual emissions in their Directors' Report since October 2013.

- The Companies (Directors' Report) and Limited Liability Partnerships (Energy and Carbon Report) Regulations 2018 impose obligations for what must be included in the Directors' Report for quoted and large unquoted companies as well as imposing an obligation on large LLPs to prepare an 'Energy and Carbon Report'.

16Alongside the SECR regulations, the Governments Environmental Reporting Guidelines provides specific guidance on the disclosure of GHG emissions.

There is no prescribed methodology, but this guidance recommends the use of widely recognised independent standards, including the GHG Protocol.

17In relation to the disclosure of renewable energy usage, Page 48 of the guidance states that:

Organisations are encouraged to use location-based grid average emission factors to report the emissions from electricity, including those consumed from the grid. Where available, time specific (e.g. hour-by-hour) grid average emission factors should be used in order to accurately reflect the timing of consumption and the carbon-intensity of the grid.

Where organisations have entered into contractual arrangements for renewable electricity, e.g. through Power Purchase Agreements or the separate purchase of Renewable Energy Guarantees of Origin (REGOs), or consumed renewable heat or transport certified through a Government Scheme and wish to reflect a reduced emission figure based on its purchase, this can be presented in the relevant report using a “market-based” reporting approach. It is recommended that this is presented alongside the “location-based” grid-average figures and in doing so, you should also look to specify whether the renewable energy is additional, subsidised and supplied directly, including on-site generation, or through a third party. A similar “dual reporting” approach should be taken for biogas and biomethane (including “green gas”).

18Given the direct reference to both the location-based and market-based methods, the Government should consider updating its guidance once the GHG Protocol has completed its revisions.

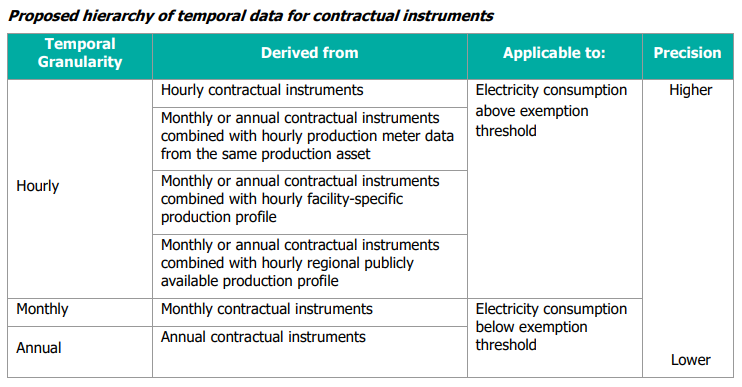

Part 1 – General points of feedback to provide the GHG Protocol

19When completing stakeholder engagement for the IFRS S1 and IFRS S2 endorsement recommendations, stakeholders indicated that disclosure of Scope 2 emissions using both the LBM and MBM were useful. Therefore, the TAC might welcome the GHG Protocol's plan to maintain the dual requirement to disclose location-based and market-based emissions data.

20Most of the proposed revisions to the Scope 2 Guidance are aimed at improving accuracy and comparability of the data by requiring a more granular data collection methodology. The TAC might welcome this approach as it will likely result in better quality data from companies using the GHG Protocol materials.

21Once the revision process has been completed, the GHG Protocol could work with the ISSB to improve transparency of the methodology applied by companies. Currently, the ISSB Standards require companies to disclose their methodology, but in practice this disclosure can be limited and vary by entity. For example, some companies disclose their methodology by referencing the GHG Protocol with no further information about how the methodology was applied. Given the proposed revisions in this consultation to the methodology of Scope 2 emissions, it could be helpful for users to have further standardised information about how GHG emissions were calculated.

22As a minor point, the GHG Protocol are inconsistent in how they refer to this document. Although it is 'guidance', some of the materials that accompany this consultation referred to it as a ‘standard'. There is a standard for Scope 3 emissions, and therefore the GHG Protocol should consider the status of this document and whether its name needs to be updated.

23A number of the proposals are presented as hierarchies to allow companies to prioritise more precise and granular data that is available to them. However, given the number of hierarchies in these proposals, the GHG Protocol might consider alternative presentation, especially when there are hierarchies within hierarchies.

24The feasibility measures are designed to help companies apply the proposed requirements. For example, the data hierarchies and the introduction of the concept 'accessible' requires companies to use data that is publicly available, free to use, and from credible sources. The ISSB introduced a similar proportionality mechanism in their standards with the concept of 'reasonable and supportable information that is available to the entity at the reporting date without undue cost or effort' which can be applied to specific requirements in IFRS S1 and IFRS S2. Although the concepts are similar, there are notable differences that could present challenges for companies. The concept of 'reasonable and supportable...' recognises that there may be costs associated with the collection of certain data and requires a company to apply judgement as to whether the cost is undue and whether the information is reasonable and supportable. On the other hand, the GHG Protocol's concept of accessible is more binary – that the information is either publicly available and free to use, or it is not. The TAC might consider encouraging the GHG Protocol to use similar language to that used by the ISSB throughout their standards and documents in a consistent manner, or at the very least to agree that in substance they amount to the same thing.

25Some of the consultation questions ask for feedback about whether the proposed revisions change (improve) the comparability of information. Given the amount of feasibility measures, including the number of hierarchies, it is unclear whether comparability of data will be improved. There are many options available to companies when calculating Scope 2 emissions, and comparability wouldn't be improved if, for example, one company uses hourly data whereas another company uses annual data. However, as noted in Paragraph 21, it would be useful for users of this information to have clearer disclosures about how the methodologies were applied.

Proposed revisions to the definitions of Scope 2, location-based method and market-based method

Proposals

26The following is a summary of the proposed revisions to the definitions within the Scope 2 Guidance.

26.1Update the current Scope 2 definition in both the Corporate Standard and Scope 2 Guidance, to clarify that Scope 2 must only include emissions from electricity generation processes that are physically connected to the company's value chain, and therefore to exclude any unrelated emissions.

26.2Location-based method (LBM) was previously defined by average generation factors across defined geographic boundaries. The proposed revision specifies that emissions should reflect generation physically delivered at the times and locations where consumption occurs. Additionally, the proposed revision explicitly recommends that imported electricity should be included in location-based emission factor calculations.

26.3The proposed revision to the market-based method (MBM) definition retains the contractual instrument as the basis for allocation, while specifying temporal correlation and deliverability requirements for matching the underlying electricity to the reporter's consumption.

TAC consideration

27The definition of Scope 2 in IFRS S2 and draft UK SRS S2 is aligned to the definition in the current GHG Protocol materials. The TAC might not have specific views on this amendment, but should note that any change to the definition would then need to be reflected in UK SRS S2.

28There is currently no definition for ‘location-based' Scope 2 emissions in IFRS S2 and draft UK SRS S2. The TAC might suggest that the proposed definitions be included in a future version of IFRS S2 and UK SRS S2 when they are next updated.

29IFRS S2, and therefore draft UK SRS S2, purposefully does not use the term 'market-based' in its requirements, but does permit companies to disclose 'any contractual instruments that is necessary to inform users' understanding of the entity's Scope 2 greenhouse gas emissions'. By retaining the term 'contractual instruments' in the proposed revision to the MBM as the basis for allocation, the revisions are unlikely to affect the requirement in IFRS S2 and draft UK SRS S2.

Proposed revisions to purpose of the location-based method and market-based method

Proposals

30The following is a summary of the proposed revisions.

Stakeholder feedback identified ambiguity in how the purposes of the LBM and MBM are defined in the Scope 2 Guidance.

The proposed revisions do not include specific wording that will be included in the updated guidance, but it might include:

| Proposed purposes of the location-based method include: | Proposed purposes of the market-based method include: |

|---|---|

| allocating emissions based on a reporter's contribution to aggregate physical demand for grid electricity; | estimating emissions based on physical and contractual relationships to electricity supply; |

| risk and opportunity assessment related to consumption of grid electricity; | influencing electricity suppliers and generation resource supply mix across the grid; |

| enabling abatement planning and reduction target-setting; and | risk and opportunity assessment related to contractual relationships; |

| improving comparability. | enabling abatement planning and reduction target setting; and |

| incentivising policy engagement. |

TAC considerations

31The initial analysis did not surface any considerations for the TAC to discuss. Ongoing stakeholder engagement might provide further insight and views on this proposal.

Questions for the TAC on Part 1

- Does the TAC agree with the general points of feedback in paragraphs 19-31?

- Does the TAC agree with the observations made about the proposed changes to the definitions of Scope 2, location-based method and market-based method, including the purpose of these methods?

Part 2 – Updates to the location-based methodology

Emission factor hierarchy

Proposals

32The most significant proposed change to the LBM requirements is the introduction of a new emission factor hierarchy that provides more guidance on the spatial and temporal granularity of location-based data.

33In this hierarchy, companies will be required to prioritise emission factors that use the most precise location information (spatial boundary) first, followed by the most precise time matching (temporal granularity). The hierarchy also requires companies to prioritise consumption-based averages (what electricity users receive) above production-based averages (what generators produce). Consumption-based averages include electricity imports, exports and stored electricity, and is therefore more reflective of the grid and a company's consumption.

34The table below demonstrates the proposed hierarchy.

Source: GHG Protocol Scope 2 Public Consultation Overview Document

TAC considerations

35Requiring companies to use more precise data will likely result in disclosures that are more accurate and decision-useful. By presenting this requirement as a hierarchy, companies will be able to select emission factors that are most appropriate whilst encouraging the use of more granular data.

36IFRS S2 and draft UK SRS S2 include a Scope 3 measurement framework that requires companies to prioritise data inputs that have specific characteristics. For example, companies are required to prioritise direct measurement and timely data. Whilst it is not presented as a hierarchy, the Scope 3 measurement framework in IFRS S2 and draft UK SRS S2 is similar to the hierarchy proposed for the Scope 2 LBM. The GHG Protocol may engage with the ISSB on ensuring any similar or overlapping requirements are not overly complex and confusing for companies to apply.

Addition of definition for 'accessible'

Proposal

37The proposals include a new concept of 'accessible' which does not require a company to use emission factors that are not accessible. This means that companies are only required to use emission factors that are publicly available, free to use, and from credible sources. There is planned guidance and definitions for what constitutes a 'credible source' which is currently being developed.

38The concept of 'accessible' is used in conjunction with the proposed LBM emission factors hierarchy, meaning that a company need only use the more granular emission factors if they are accessible. If a higher-quality emission factor exists but is not publicly available or requires payment, the company can use a different emission factor. For example, if hourly emission factors are not accessible, the company can use monthly or annual emission factors.

TAC considerations

39As noted in Paragraph 24, the proposed revisions for the Scope 2 Guidance might benefit from the concept of 'reasonable and supportable' throughout the document. However, the introduction of the concept of 'accessible' in relation to LBM, especially only requiring the use of 'free to use' emission factors goes beyond the ISSB's concept of 'without undue cost'. The concept of 'undue cost’ recognises that there may be costs associated with the collection of certain data and requires a company to apply judgement. This is notably different to 'free to use' which is binary. The TAC might consider encouraging the GHG Protocol to use similar language to that used by the ISSB throughout their standards and documents in a consistent manner, or at the very least to agree that in substance they amount to the same thing.

40It is noted that further discussion is to be had on what constitutes a 'credible' source. The consultation specifically asks respondents to provide views on which entities should qualify as credible sources, and asks respondents to select from a list including:

- Government agency;

- system operator;

- recognised registry;

- accredited statistics body;

- independent methodology meeting minimum criteria; and

- other.

The TAC might suggest that any definition or guidance on what source is 'credible' should focus on characteristics of credibility rather than providing a list of possible entities that might be considered 'credible'.

Requirement to use the most precise location-based emission factor accessible

Proposals

41Alongside the proposed LBM hierarchy, there is also a proposal to clarify that companies must use the most precise location-based emission factors on the hierarchy accessible to them matched to the same precision as available activity data.

42For example, if a company is only able to source annual activity data, it is only required to calculate its location-based emissions using annual emission factors. If a company has access to hourly activity data, then it is required to use hourly emission factors.

43The proposed revisions also include a proposed hierarchy of consumption data to help companies select the most precise data that is available to them. This hierarchy is presented below.

(e.g., NREL End-Use Load Profiles for the U.S. Building Stock; DOE Load Profiles data, ENTSO-E national hourly demand, EIA Form 930 Balancing Authority demand, Australian Energy Market Operator (AEMO) NEM demand data, UK Energy Dashboard, CAISO system load curves, Profiling - Elexon BSC, Normalized Demand Profiles for UK, Energy Charts (Germany), etc.).

TAC considerations

44The proposed clarification that companies should use the most precise location-based emission factor that is accessible to them matched to available activity data is helpful.

45However, it is unclear how the proposed hierarchy of consumption data should be used with the LBM emission factor hierarchy. For example, is the hierarchy of consumption data specifically designed to be used when collecting activity data, or it is a hierarchy that sits within the LBM emission factor hierarchy? The GHG Protocol should clearly explain how this hierarchy should be used in conjunction with the LBM emission factor hierarchy.

Feasibility measures for location-based method updates

Proposals

46To support the implementation of the proposed revisions to the LBM, the consultation presents feasibility options including the option to use load profiles and an option to phase implementation over a number of years.

47Load profiles are commonly used by grid planners to estimate how much electricity demand is expected during specific hours of the day. The proposals in this consultation would allow load profiles to be used in a similar way by companies to approximate hourly data when actual data is not available or accessible.

48There is no specific proposal for phased implementation. It is noted in the consultation document that phased implementation that stage effective dates for any new requirement could help organisations prepare for the changes. This will likely be discussed as the guidance is finalised.

TAC considerations

49Whilst appreciating the need to update the requirements for LBM to reflect updated scientific understanding and technological capabilities, feasibility and cost-effectiveness are key factors for the GHG Protocol to consider when finalising the proposals.

50Although there is no specific proposal for phased implementation, the TAC might welcome this as companies will need time to adjust to the new approaches. Ongoing stakeholder engagement might provide further insight and views on feasibility, including the measures included in the proposals.

Questions for the TAC on Part 2

- Does the TAC have any views on the proposed revisions to the location-based method (LBM)?

Part 3 – Updates to the market-based method

51The most notable proposals in the consultation are related to the market-based method (MBM). The current approach allows companies to claim the use of clean energy through any contractual instruments that are matched to their consumption. However, this approach has been seen by some as controversial as the accuracy and comparability of the data can be challenged. For example, some companies use contractual instruments (e.g. renewable energy certificates) to ‘offset' their Scope 2 emissions, which is not the intention of the MBM. Some companies purchase renewable energy certificates from a source that is not in the jurisdiction it operates in and then claim 100% renewable energy use even if that energy is not physically delivered to its operations. This means that there is often a temporal and geographical misalignment between the certificates and the actual energy use.

52The proposed revisions to the MBM are intended to ensure reported Scope 2 market-based emissions are aligned more closely with the time and place the electricity is actually consumed.

Update to Scope 2 Quality Criteria 4 – Hourly matching

Proposals

53A significant proposal is the requirement for companies using contractual instruments to match them to hourly electricity consumption. This would only apply to contractual instruments and not to the totals reported using residual mix. This requirement would ensure that all contractual instruments are issued and redeemed for the same hour as the energy consumption to which the instrument is applied.

54The proposals include a hierarchy of options (presented in the tables below) that a company can use to ensure the data is a precise as possible. The proposal also allows companies to use load profiles and hourly curves to make this requirement practical and accessible.

55This revision also includes exemption thresholds so that smaller companies that meet a defined eligibility threshold are not required to use an hourly accounting interval for Quality Criteria 4, and can instead use monthly or annual accounting intervals. The consultation proposes four options which could be used to set the exemption eligibility:

- Option 1. Companies with annual consumption up to [X] GWh/year in a deliverable market boundary may use a monthly or annual accounting interval for Criteria 4 for all operations within that market boundary in accordance with Proposed hierarchy of temporal data for contractual instruments.

- Option 2. Companies that meet the small and medium company2 categorisation may use a monthly or annual accounting interval for Criteria 4 for all operations within that market boundary in accordance with the Proposed hierarchy of temporal data for contractual instruments.

- Option 3. Companies with annual consumption up to [X] GWh/year in a deliverable market boundary, or meet the small and medium company categorization, may use a monthly or annual accounting interval for Criteria 4 for all operations within that market boundary in accordance with the Proposed hierarchy of temporal data for contractual instruments.

- Option 4. Companies with annual consumption up to [X] GWh/year in a deliverable market boundary, and which meet the small and medium company categorization, may use a monthly or annual accounting interval for Criteria 4 for all operations within that market boundary in accordance with the Proposed hierarchy of temporal data for contractual instruments.

56Initial analysis from CDP suggests that most companies would be exempt, whilst the majority of electricity load on the grid would still be subject to hourly matching requirements.

TAC considerations

57Ensuring that any contractual instruments used by companies to claim renewable energy usage are matched to actual energy consumption is an important update to the Scope 2 Guidance. This proposal will enable Scope 2 market-based disclosures to be more faithfully representative of the actual energy usage.

58The exemption thresholds could be helpful to support smaller companies with less energy consumption to apply the proposed revisions. The TAC might not have a view on which of the options is most appropriate, but might welcome the approach.

59Ongoing stakeholder engagement might provide further insight and views on this proposal.

Update to Scope 2 Quality Criteria 5 – Deliverability

Proposals

60The proposed updates to the Scope 2 Quality Criteria 5 redefine the market boundary to ensure that all contractual instruments are sourced from generation that is deliverable to the consuming load. In some cases, national borders will approximate the deliverable boundary, but there are other cases where grid operations or interconnections differ from national borders. To support this, companies will be expected to disclose the geographic location of the generation facility from which the associated attributes are derived. Companies will also be required to use a consistent and recognised mechanism for tracking and retiring certificates to prevent double counting across market boundaries.

61The proposals also include a list of proposed methodologies, and alternative methodologies, that can be used to demonstrate deliverability.

TAC considerations

62The initial analysis did not surface any considerations for the TAC to discuss. Ongoing stakeholder engagement might provide further insight and views on this proposal.

New guidance for Standard Supply Service (SSS)

Proposals

63New guidance is proposed for Standard Supply Service (SSS) which formalises existing concepts in the current Scope 2 Guidance. This guidance is intended to provide globally applicable rules for how companies account for their rightful share of electricity from publicly funded, mandated, or shared resources e.g. default utility service or government clean energy programs.

64Multiple customers financially contribute to these resources, and SSS seeks to ensure that each customer can only claim its proportional share based on electricity use. If a share is not claimed by a customer, it can't be used by other customer to substantiate its claims.

TAC considerations

65The initial analysis did not surface any considerations for the TAC to discuss. Ongoing stakeholder engagement might provide further insight and views on this proposal.

Updated definition of residual mix emission factors

Proposals

66The proposals include an updated definition of residual mix emission factors that seek to address that SSS should be excluded from the residual mix along with contractual instruments voluntarily claimed. Additionally, the proposed update would clarify that while residual mix emission factors should reflect the highest temporal precision available for the relevant market boundary, hourly matching is not required.

TAC considerations

67The initial analysis did not surface any considerations for the TAC to discuss. Ongoing stakeholder engagement might provide further insight and views on this proposal.

Provide new requirement for use of fossil-based emission factors

Proposal

68The proposals include an update to the requirement that currently allows companies to apply a grid average emission factor when activity data is not matched with either contractual instruments or a residual mix. The update removes the option to use a grid average emission factor and proposes that for any consumption not matched with the SSS or voluntary contractual instruments companies would be required to use either a residual mix emission factor (that excludes all claimed and SSS contractual instruments) or default to either a fossil-only grid-average or fossil emission factor.

TAC considerations

69The initial analysis did not surface any considerations for the TAC to discuss. Ongoing stakeholder engagement might provide further insight and views on this proposal.

Feasibility measures for market-based method updates

Proposals

70Alongside the proposed changes to the MBM that are described above, the proposals also include feasibility measures including:

- the use of load profiles to approximate hourly data when this information isn't accessible;

- exemption thresholds that exempt certain companies (either based on size of company and/or the volume of electricity consumed) from hourly matching requirements; and

- an anticipated phased implementation period.

71The consultation is requesting feedback about a possible legacy clause which would allow companies to continue to count contractual instruments from existing arrangements for a transition period even when those instruments do not meet the proposed hourly matching and deliverability requirements. This proposal is intended to maintain some continuity in Scope 2 market-based reporting for qualifying legacy investments. The consultation requests feedback on the appropriateness of including a legacy clause and on its potential design which includes eligibility criteria.

TAC considerations

72Whilst appreciating the need to update the requirements for MBM to improve the accuracy and reliability of the data, feasibility and cost-effectiveness are key factors for the GHG Protocol to consider when finalising the proposals.

73Although there is no specific proposal for phased implementation, the TAC might welcome this as companies will need time to adjust to the new approaches. If including phased implementation, the GHG Protocol should require companies to be transparent about what approach has been applied during the transition phase to allow users to understand the basis used calculate the emissions. Ongoing stakeholder engagement might provide further insight and views on this feasibility, including the measures included in the proposals.

Questions for the TAC on Part 3

(iv) Does the TAC have any views on the proposed revisions to the market-based method (MBM)?

Part 4 – Consequential accounting methods

74Alongside the consultation on the proposed revisions to the Scope 2 Guidance, the GHG Protocol is also looking for feedback regarding consequential accounting methods. Also known as 'avoided emissions', consequential accounting methods estimate the system-wide impacts of actions and interventions (such as installation of clean energy projects). The major difference between Scope 2 MBM and consequential accounting methods is that the latter accounts for emissions beyond the organisation's operational boundaries.

75Complementary requirements are being developed for quantifying and reporting GHG impacts from projects and market instruments outside of corporate GHG inventories. This is intended to clarify the difference between GHG inventory (attributional) accounting (which is used in the Corporate Standard) and project accounting to ensure projects and other market instruments are not used to 'offset' Scope 2 emissions.

76This consultation is focused on the electricity sector. The questions in the consultation ask for feedback relating to:

- the potential benefits, challenges, or unintended consequences of developing and using consequential accounting methods for electricity-sector;

- proposed formulas that could be used to quantify emissions impacts

- the treatment of additionality;

- approaches for determining marginal emission rates; and

- how to balance or weight operating margin and build margin impacts when estimating the emissions effects of electricity projects.

TAC considerations

77Given the sector-specificity and the technical expertise required to respond to the questions on consequential accounting methods, the Secretariat recommends that the TAC does not provide any feedback on this consultation.

Questions for the TAC on Part 4

(v) Do you agree that the TAC will not provide feedback to the GHG Protocol in relation to its consultation on consequential accounting methods for the electricity sector?

Appendix 1 – Consultation questions for the proposed revisions to the Scope 2 Guidance

For reference, the questions from the Scope 2 Guidance consultation are presented here. To help navigate the questions, the same headings that are used in the paper are used to separate the corresponding questions.

Proposed revisions to the definitions of Scope 2, location-based method and market-based method

18Please provide any feedback on the proposal to refine the definition of scope 2, to emphasize its role within an attributional value chain GHG inventory and clarify that scope 2 must only include emissions from electricity generation processes that are physically connected to the reporter's value chain, excluding any emissions from unrelated sources?

19Please provide any feedback on the proposal to clarify the LBM definition to reflect scope 2 emissions from generation physically delivered at the times and locations of consumption, with imports included in LBM emission factor calculations where applicable?

20Please provide any feedback on the proposal to clarify the MBM definition to retain its existing basis, quantifying scope 2 from contractually purchased electricity via contractual instruments, while specifying temporal correlation and deliverability when matching instruments to consumption?

Proposed revisions to purpose of the location-based method and market-based method

21Please provide any feedback on the proposed purposes of the location-based method.

22Please provide any feedback on the proposed purposes of the market-based method.

Update to the location-based emission factor hierarchy

23On a scale of 1-5, do you support the update to the location-based emission factor hierarchy to identify the most precise location-based emission factor accessible according to spatial boundaries, temporal granularity, and emission factor type (consumption or production)?

- Scale of 1 (no support) – 5 (full support)

24Please provide your reasons for support, if any (select all options that apply)

- Agree that guidance on selecting location-based emission factors should be presented as a hierarchy

- Enhances the accuracy and relevance of the location-based method

- Enables use of emission factors that support abatement planning and target-setting

- Improves use of location-based method to provide risk and opportunity assessment related to consumption of grid electricity

- Aligns with emission factors used by your organization for location-based emissions reporting

- Aligns with emission factors used for mandatory or voluntary reporting in your region

- Prioritizes consumption-based factors that include imports/exports over production-based factors

- Clarifies application of the EF hierarchy (spatial > temporal > consumption-based > production-based)

- Agree with listing the most precise temporal granularity as “hourly”

- Agree with listing the most precise spatial boundary as “local boundary"

- Agree that the proposed spatial boundaries reflect electricity deliverability in your region

- Other (please provide)

25Please provide comments regarding your reasons for support.

26Please provide your concerns or reasons for why you are not supporting, if any (select all options that apply)

- Prefer guidance on selecting location-based emission factors to be identified as a single globally applicable option to increase comparability

- Concern about increased administrative burden and complexity from identifying the most precise emission factors accessible

- Concern that the most precise temporal granularity “hourly“ is too detailed

- Concern that the most precise spatial boundary, “local boundary”, is too narrow

- Concern that the proposed spatial boundaries do not reflect electricity deliverability in your region

- Concern hierarchy does not align with emission factors used by your organization for location-based emissions reporting

- Concern hierarchy does not align with emission factors used for mandatory or voluntary reporting in your region

- Prefer a different order (e.g., consumption-based first, then spatial boundary, then temporal granularity)

- Unclear how the changes will affect your GHG emissions reporting

- Other (please provide)

27Please provide comments regarding your reasons for why you are not supporting (if any).

28For different views on the order the hierarchy should be applied (e.g. preference for consumption-based emission factors, then spatial boundary, then temporal granularity) please explain the preferred order.

29Regarding regions that you operate in or have experience in, please provide comments on whether the LBM emission factor hierarchy allows you to identify an accessible emission factor that appropriately reflects how electricity is delivered in that region (please clearly identify the region you are referring to in your answer).

30Regarding regions that you operate in or have experience in, please provide comments on whether the LBM emission factor hierarchy is likely to cause any region-specific challenges in its application (provide specific examples, and clearly identify the region you are referring to in your answer).

31Do you agree that “local boundary” should be listed as the most precise spatial boundary for LBM emission factors? If not, select which should be listed as the most precise spatial boundary?

- Yes, I support local boundary as the most precise spatial boundary

- No, a more precise spatial boundary should be added

- No, a less precise spatial boundary should be used. Use Operational grid boundary

- No, a less precise spatial boundary should be used. Use Grid-wide or national boundary

- Other (describe)

32If you selected “Other” in question 31, please describe.

33Should the LBM emission factor hierarchy be adjusted to include the deliverable market boundaries outlined in the proposed MBM Methodologies for demonstrating deliverability where they do not already overlap? If so, should they be included in addition to, or as a replacement for, the spatial boundaries currently proposed in the hierarchy?

- No, different spatial boundaries are appropriate for the location-based and market-based methods

- Yes, include the MBM deliverability market boundaries in addition to the proposed LBM hierarchy (explain why they should be added)

- Yes, include the MBM deliverability market boundaries as a replacement for the proposed LBM hierarchy (explain why they should replace the current hierarchy)

- Other (explain)

- Do not support boundaries as proposed in either method (explain alternative boundaries for the location-based emission factor hierarchy and how they support integrity, impact, and feasibility for a value chain inventory

34Please provide additional explanations or further details regarding your answer to question 33.

Addition of definition for “accessible"

35On a scale of 1-5 do you support the new definition of accessible: publicly available, free to use, and from a credible source?

- Scale of 1 (no support) – 5 (fully support)

36Please provide your reasons for support, if any. Select all options that apply.

- Definition supports feasibility and lower-cost reporting

- Supports transparency and public verifiability of emission factors

- Implements a common comparability baseline across reporters

- Creates data equity for smaller reporters and underserved regions

- Encourages open publication of emission factors

- High quality accessible emission factors already exist for most markets globally today

- Ensures reporters can immediately apply the updated LBM hierarchy

- Clarifies reporting requirements

- Other (please explain)

37Please provide comments regarding your reasons for support.

38Please provide your concerns or reasons for why you are not supporting (if any). Select all options that apply

- Definition needs further clarification about what is recognized as a credible source

- Definition should not exclude emission factors that are publicly available and credible even if they have a reasonable associated cost (i.e. not free)

- A list of suitable location-based emission factors should be published for each region, rather than requiring reporters to individually determine what is accessible in their region

- Definition should also consider level of administrative effort in addition to external costs for emission factor data

- Another criterion should be added to the definition

- Other (please explain)

39Please provide comments regarding your reasons for concern (if any).

40Which entities should qualify as credible sources (select all options that apply)

- Government agency

- System operator

- Recognized registry

- Accredited statistics body

- Independent methodology meeting minimum criteria (outlined in question 42)

- Other (please specify and explain)

41Please provide additional comments concerning your selected credible sources, including at least one example per region you operate in or have experience with, if possible.

42If you selected independent methodologies in question 40, please describe what documentation or assurance (if any) is needed for it to be recognised as a credible source? (select all that apply, then add brief detail):

- Publicly documented methods and system boundaries

- Update cadence (e.g., annual) and version control

- QA/QC procedures and uncertainty disclosure

- Governance/independence and conflict-of-interest safeguards

- Geographic/system boundary and temporal coverage fit for use

- Other (please explain)

43Please provide any additional comments concerning your selected minimum criteria in question 42

Requirement to use the most precise location-based emission factor accessible

44On a scale of 1-5 do you support the update to the requirement to use the most precise location-based emission factor accessible for which activity data is also available?

Scale of 1 (no support) – 5 (fully support)

45Please provide your reasons for support, if any (select all that apply).

- Improves accuracy and scientific integrity of LBM results

- Strengthens transparency and public verifiability

- Enhances comparability across reporters and frameworks

- Better reflects grid operation in time and space, reduces misallocation

- Enables emission changes from storage and demand-flexibility to be reflected more accurately

- Prioritizes consumption-based factors that include imports/exports

- Aligns emission factor precision with available activity data

- Aligns positively with mandatory or voluntary reporting requirements in your region

- Enables use of load profiles when hourly activity data are unavailable

- Provides a common, accessible baseline for inventories

- Supports phased improvement as data availability expands

- Improves decision-usefulness for external disclosures

- Other (please provide)

46Please provide any additional comments regarding your reasons for support.

47Please provide your concerns or reasons for why you are not supporting (select all that apply).

- Concern about negative impact on comparability, relevance and/or usefulness of LBM inventories

- Concern that administrative, data management, and audit challenges posed by this approach would place an undue burden and costs on reporters

- Concern that the most precise spatial boundary in the LBM emission factor hierarchy, "local boundary', is too narrow to require even when accessible

- Accessible factors may be less accurate than non-accessible options and primary users of emission reporting data may expect the most representative factors

- Material differences to inventory accuracy are too small to justify cost

- Concern about the update cadence or representativeness of datasets (hourly/monthly)

- Other (please provide)

48Please provide any additional comments regarding your concerns or reasons why you are not supporting (if any).

49For concerns or support for alignment with mandatory or voluntary reporting requirements in your region, please provide an example of the programmatic requirements and the impacts of these changes on alignment.

50For concerns that the most precise spatial boundary (local boundary) is too granular to be required even if emission factors are accessible, please outline why and identify whether reporting at this level of granularity should be a “may”, “should” or "shall not" requirement?

51For concerns that choosing an accessible factor over a more accurate “non-accessible” one can reduce accuracy and decision-usefulness please describe the conditions when a non-accessible factor should be required to be used over an accessible one (e.g., material difference threshold, investor relevance), and what transparency/assurance is needed (public methods, QA/QC, independent assurance). Please note any cost/effort implications.

Feasibility measures for location-based method updates

52Considering investor and assurance needs, how do the proposed location-based method revisions change the extent to which information is decision-useful to users relative to incremental cost and complexity for preparers?

- No meaningful improvement (unlikely to change decisions/interpretations)

- Minor improvement (noticeable but unlikely to change decisions)

- Moderate improvement (could change some decisions/assessments)

- Substantial improvement (likely to change decisions benchmarks)

- Not sure / no basis to assess

53Please provide additional context for your answer to question 52.

54Considering investor and assurance needs, how do the proposed location-based revisions change the comparability of information relative to incremental cost and complexity for users?

- No meaningful improvement (unlikely to change comparability/interpretations)

- Minor improvement (noticeable but unlikely to change comparability)

- Moderate improvement (could change some comparability/assessments)

- Substantial improvement (likely to change comparability benchmarks)

- Not sure / no basis to assess

55Please provide additional context for your answer to question 54.

56For questions 52-55, please provide the basis for your assessment.

- Direct empirical analysis (e.g., back-testing with hourly factors)

- Operational experience (e.g. applying hourly LBM emission factors)

- Professional judgment informed by literature/briefings

- General awareness (no direct analysis)

- Prefer not to say

57At the Operational Grid Boundary level (of the proposed location-based emission factor hierarchy), what share of your load has hourly emission factors accessible: (select one)

- 0%

- 1–25%

- 26–50%

- 51–75%

- 76–100%

- Unsure

- Not applicable

58Please provide additional context for the data sources included in your answer to question 57.

59Please indicate the share of your load with hourly activity data available: (select one)

- 0%

- 1–25%

- 26–50%

- 51–75%

- 76–100%

- Unsure

- Not applicable

60If your answer to questions 57 & 59 includes significant geographical differences (some regions with hourly emission factor and higher volumes of hourly activity data, other regions with minimal hourly activity data and/or no hourly emission factors), please include additional context.

61When actual hourly activity data are unavailable, and solely to enable use of more precise LBM emission factors, the proposed revisions allow a reporter to use load profiles to approximate hourly data from monthly or annual load data. How would the use of load profiles affect the comparability, relevance, and usefulness of LBM inventories relative to your current practice? Please describe potential advantages, limitations, and any conditions under which impacts may differ.

62On a scale of 1-5, please indicate the incremental preparer cost/effort to implement the proposed revisions to the location-based method

- Scale of 1 (minimal) – 5 (high)

- Not applicable (not a preparer)

63Please select the main drivers of cost/effort (select all that apply).

- Data access/rights to granular emission factors

- Hourly activity data availability/metering rollout

- Tooling/IT integration or data pipelines

- Assurance/internal controls readiness

- Staffing/capacity/training

- Contracting/procurement or budget cycle constraints

- Third-party publication cadence (emission factors)

- Multi-jurisdiction complexity (many grids/regions)

- Policy/regulatory or commercial terms

- Other (specify)

64Please provide additional context on the main drivers of cost/effort.

65Which two measures would most reduce burden in your context? (select up to 2)

- Standardized publication of consumption-based emission factors by grid/system operators

- Load profile hierarchy/templates to approximate hourly activity data when meters are unavailable

- Phased implementation (staged effective dates)

- API/automated access to emission factor datasets

- Example calculations and disclosure templates

- Assurance safe-harbors for estimates

- Other (specify)

66Please provide additional context on the measures that would most reduce burden in your context.

67For which reporting year would your organization be ready to apply the revised Scope 2 Standard based on these proposed changes in its GHG inventory? For example, if the Standard is published in 2027, the reporting year 2027 inventory is typically prepared and reported in 2028:

- Earlier than reporting year 2027 (already aligned)

- Reporting year 2027 (inventory prepared in 2028)

- Reporting year 2028 (inventory prepared in 2029)

- Reporting year 2029 (inventory prepared in 2030)

- Reporting year 2030 (inventory prepared in 2031) or later

- Later than Reporting year 2030

- Not applicable

68Please provide additional context regarding how this timeline could be shortened and note any region or sector-specific context.

Update to Scope 2 Quality Criteria 4 – Hourly matching

71On a scale of 1-5 do you support an update to Quality Criteria 4 to require that all contractual instruments used in the market-based method be issued and redeemed for the same hour as the energy consumption to which the instrument is applied, except in certain cases of exemption.

- Scale of 1 (no support) – 5 (fully support)

72Please provide reasons for support, if any (select all that apply)

- Improves accuracy and scientific integrity of MBM results

- Strengthens transparency and supports public verification

- Enhances comparability across reporters and frameworks using GHG Protocol data

d. API/automated access to emission factor datasets e. Example calculations and disclosure templates f. Assurance safe-harbors for estimates g. Other (specify)

66. Please provide additional context on the measures that would most reduce burden in your context.

67. For which reporting year would your organization be ready to apply the revised Scope 2 Standard based on these proposed changes in its GHG inventory? For example, if the Standard is published in 2027, the reporting year 2027 inventory is typically prepared and reported in 2028: a. Earlier than reporting year 2027 (already aligned) b. Reporting year 2027 (inventory prepared in 2028) c. Reporting year 2028 (inventory prepared in 2029) d. Reporting year 2029 (inventory prepared in 2030) e. Reporting year 2030 (inventory prepared in 2031) or later f. Later than Reporting year 2030 g. Not applicable

68. Please provide additional context regarding how this timeline could be shortened and note any region or sector-specific context.

Update to Scope 2 Quality Criteria 4 – Hourly matching

71. On a scale of 1-5 do you support an update to Quality Criteria 4 to require that all contractual instruments used in the market-based method be issued and redeemed for the same hour as the energy consumption to which the instrument is applied, except in certain cases of exemption. a. Scale of 1 (no support) – 5 (fully support)

72. Please provide reasons for support, if any (select all that apply) a. Improves accuracy and scientific integrity of MBM results b. Strengthens transparency and supports public verification c. Enhances comparability across reporters and frameworks using GHG Protocol data d. Better reflects grid operation, reduces misallocation of generation (e.g., "solar at night") e. Reduces risk of greenwashing/time-shifting claims by aligning claims to time of use f. Improves decision-usefulness for external disclosures g. Helps create price signals for times and places where renewables are not already abundant h. Helps accelerate the development of technologies that will be needed at scale for fully decarbonized grids i. Enables emission changes from storage and demand-flexibility to be reflected more accurately j. Improves risk and opportunity assessment related to contractual relationships k. Other (please explain)

73. Please provide comments regarding your reasons for support.

74. Please provide concerns or reasons for why you are not supporting, if any (select all that apply) a. More information is necessary to understand how investments not matched on an hourly basis will be accounted for and reported via the framework under development by the Actions & Market Instrument TWG b. Hourly matching should follow an optional ‘may' rather than a required 'shall' approach c. Hourly matching should follow a recommended ‘should' rather than a require 'shall' approach d. Concern about negative impact on comparability, relevance and/or usefulness of MBM inventories e. Concern that a phased implementation would be insufficient for development of the infrastructure necessary (e.g., registries, trading exchanges, etc.) to support hourly contractual instruments f. Concern that administrative, data management, and audit challenges posed by this approach would place an undue burden and costs on reporters g. Concern that requiring hourly matching does not create meaningful improvements to inventory accuracy h. Concern that a requirement for hourly contractual instruments could discourage global participation in voluntary clean energy procurement markets i. Other (please explain)

75. Please provide comments regarding your concerns or reasons for why you are not supportive.

76. Load profiles enable organizations without access to hourly activity data or hourly contractual instruments to approximate hourly data from monthly or annual data. How would the use of load profiles affect the comparability, relevance, and usefulness of MBM inventories relative to your current practice? Please describe potential advantages, limitations, and any conditions under which impacts may differ.

The following set of questions (77-82) applies to sites or business units above the exemption threshold, assume the default exemption conditions selected in Section 5.3.1.

Who should answer: This item is optional and intended primarily for reporters (or service providers responding on behalf of a reporter/client) with direct knowledge of implementation effort and spend. They seek to understand how hourly matching would change your workload and implementation costs relative to current MBM practice after applying feasibility measures (load profiles, phased implementation, legacyclause). If you are not preparing or overseeing a scope 2 inventory for a specific organization, you may skip this item or answer only where relevant. Note: This section is about administrative implementation (internal effort and external service costs). Please do not include procurement price differences for hourly EACs/PPAs; those are covered in the “combined questions for updates to MBM” section 5.4.

77. What is the approximate share of your organization's total load that would be subject to hourly matching, excluding any exemptions: a. 0% b. 1-25% c. 26–50% d. 51–75% e. 76–100% f. Unsure

78. Please indicate your best estimate of the internal administrative effort (people/process/controls) of the proposed hourly matching requirement relative to your current MBM process using annual matching. Assume 3 is your current level of effort. a. Scale of 1 (much less) – 5 (much more)

79. Please indicate your best estimate of the external service cost (cash outlays to vendors, data, assurance) of the proposed hourly matching requirement relative to your current MBM process using annual matching. Assume 3 is your current external cost. a. Scale of 1 (much less) – 5 (much more)

80. What are the feasibility measures you would anticipate relying on (select all that apply): a. Load profiles for activity data (facility-specific) b. Load profiles for activity data (utility/customer-class or regulator-approved) c. Load profiles for activity data (time-of-use averages) d. Load profiles for activity data (flat average across hours) e. Load profiles for contractual instruments (same production asset) f. Load profiles for contractual instruments (facility-specific) g. Load profiles for contractual instruments (regional publicly available) h. Phased implementation i. Legacy clause

81. What are the assumed main drivers affecting internal workload and external service costs after applying feasibility measures (select all that apply): a. Registry/market access for hourly EACs b. Vendor/platform upgrades or new tools c. Data integration (profiles, APIs), system configuration d. Assurance/internal controls and evidence trails e. Staff capacity/training f. Contracting/sourcing changes for hourly instruments g. Metering/interval data access arrangements h. Other (specify)

82. Please provide any additional comments regarding your response to questions 77-81.

Update to Scope 2 Quality Criteria 5 – Deliverability

83. On a scale of 1-5 do you support an update to Scope 2 Quality Criteria 5, to require that all contractual instruments used in the market-based method be sourced from the same deliverable market boundary in which the reporting entity's electricity-consuming operations are located and to which the instrument is applied, or otherwise meet criteria deemed to demonstrate deliverability to the reporting entity's electricity-consuming operations? a. Scale of 1 (no support) – 5 (fully support)

84. Please provide reasons of support, if any (select all that apply). a. Improves accuracy and scientific integrity of MBM results b. Strengthens transparency and public verifiability c. Enhances comparability across reporters and frameworks using GHG Protocol data d. Improves decision-usefulness for external disclosures e. Better reflects grid operation, reduces misallocation f. Provides sufficiently flexible options for organizations to demonstrate deliverability outside of the defined deliverable market boundaries g. Defined market boundaries reflect a boundary your organization already uses for procuring contractual instruments h. Agree that the proposed market boundary for my region(s) accurately reflects deliverability i. Agree that the defined market boundaries align with mandatory or voluntary reporting requirements in your region j. Improves risk and opportunity assessment related to contractual relationships k. Helps create price signals for times and places where renewables are not already abundant l. Other (please explain)

85. Please provide comments regarding your selected reasons for support.

86. Please provide reasons of concern or why you are not supporting, if any (select all that apply) a. Proposed deliverability requirements do not improve alignment with GHG Protocol Principles b. Concern that narrower market boundaries restrict companies' abilities to invest in areas where renewable energy development could yield the greatest decarbonization impact c. Concern that narrower market boundaries could prompt a shift away from long-term agreements (i.e., PPAs) to spot purchases (unbundled certificates) d. Sourcing contractual instruments within deliverable market boundaries should follow an optional “may” rather than a required “shall” approach e. Sourcing contractual instruments within deliverable market boundaries should follow a recommended “should” rather than a required “shall” approach f. Concern that the defined market boundaries do not align with mandatory or voluntary reporting requirements in your region g. Support deliverability in principle, but the proposed market boundary for my region does not reflect deliverability h. Market boundaries should be defined as the geographic boundaries of electricity sectors, which align with national, and under certain circumstances, multinational boundaries i. Exemptions to matching within deliverable market boundaries should be allowed for markets lacking sourcing options j. Other (please explain)

87. Please provide comments regarding your selected reasons for why you are not supporting. Please answer the following questions 88-91 in regard to regions that you operate in or have experience in.

88. For the United States, which of the following market boundaries would best uphold the principle of deliverability and align with the decision-making criteria? (Please see the table Proposed methodologies for demonstrating deliverability above for references to these options): a. The US Environmental Protection Agency's Emissions & Generation Resource Integrated Database (eGRID) b. DOE Needs Study Regions (45V) c. Wholesale Market/Balancing Authority d. Unsure e. Other

89. If you selected options (a), (b) or (c) for question 88 please explain why this option best upholds the principle of deliverability and balances integrity, impact, and feasibility of the MBM. Please also provide comments on the relative feasibility challenges of applying the other options.

90. For deliverable market boundaries (outside of the United States) identified in the table Proposed methodologies for demonstrating deliverability: Deliverable Market Boundaries, please provide comments on whether these market boundaries: - appropriately reflect the deliverability of electricity in that region - align with mandatory or voluntary reporting requirements in that region, please provide an example of the programmatic requirements and the impacts of these proposed changes on alignment - are likely to cause any region-specific feasibility challenges (provide specific examples) - If you prefer a different deliverable market boundary than identified in the table Proposed methodologies for demonstrating deliverability: Deliverable Market Boundaries, please describe this boundary. Please clearly identify the region you are referring to in your comments.

91. For regions not specified in the table Proposed methodologies for demonstrating deliverability: Deliverable Market Boundaries, please provide examples of market boundaries that uphold the principle of deliverability and balance integrity, impact, and feasibility of the MBM.

The following questions concern how a requirement to use deliverable market boundaries would change your workload and implementation costs relative to current MBM practice after applying feasibility measures (e.g., phased timing and legacy clause)? Please answer with respect to the deliverable boundary requirement only, the combined impact of market-based method changes on feasibility will be evaluated in the “combined questions for updates to MBM” section. Please also assume the default exemption conditions selected in Section 5.3.1. Note: This section is about administrative implementation (internal effort and external service costs). Do not include procurement price differences for EACs/PPAs; those are covered in the “combined MBM questions" section 5.4. Who should answer: This item is optional and intended primarily for reporters (or service providers responding on behalf of a specific reporter/client) with direct knowledge of implementation effort and spend. If you are not preparing or overseeing a scope 2 inventory for a specific organization, you may skip this item or answer only where you have direct experience.

92. Please estimate the anticipated internal administrative effort (people/process/controls) of the proposed deliverability requirement relative to your current MBM process using broad market boundaries. Assume 3 is your current level of effort. a. Scale of 1 (much less) – 5 (much more)

93. Please estimate the anticipated external service cost (cash outlays to vendors, data, assurance) of the proposed deliverability requirement relative to your current MBM process using broad market boundaries. Assume 3 is your current external cost. a. Scale of 1 (much less) – 5 (much more)

94. What are the feasibility measures you would anticipate relying on to report using deliverable market boundaries (select all that apply): a. Phased implementation b. Legacy clause

95. What are the assumed main drivers affecting internal workload and external service costs after applying feasibility measures (select all that apply): a. Data access/rights for EACs/registries aligned to deliverable market boundaries b. Vendor/platform upgrades or new tools c. Data integration (profiles, APIs), system configuration d. Assurance/internal controls and evidence trails e. Staff capacity/training f. Contracting/sourcing changes for hourly instruments within deliverable market boundaries g. Metering/activity data reporting configured to match deliverable market boundaries h. Other (specify)

96. Please provide any additional comments regarding your response to questions 92-95.

New guidance for Standard Supply Service (SSS)

97. On a scale of 1-5 do you support the new guidance for Standard Supply Service (SSS) and requirement that a reporting entity shall not claim more than its pro-rata share of SSS. a. Scale of 1 (no support) – 5 (fully support)

98. Please provide reasons of support, if any (select all that apply). a. Helps ensure that SSS resources are fairly allocated to all consumers and prevents procurement by specific organizations b. Clarifies the order of operations so that organizations may claim SSS first and then make voluntary procurements c. Supports consistent treatment of shared supply across different market structures d. Protects the integrity of market-based accounting by avoiding double counting of attributes from SSS e. Other (please explain)

99. Please provide comments regarding your selected reasons for support.

100. Please provide concerns or why you are not supporting, if any (select all that apply). a. Markets should self-determine how resources that fall under SSS are allocated to customers b. Concern of regionally applicable challenges to implementation c. Unclear how partial subsidies affect SSS classification d. Unclear rules/definition of SSS e. All contractual instruments should be eligible for voluntary procurement. f. Other (please explain)

101. Please provide comments regarding your selected reasons for why you are not supportive.

102. Are there resources in your region that do not fit clearly within the outlined examples of SSS but should be allocated to all customers under this framework? If so, please provide examples and explanations for each.

103. Are there resources in your region that fit within the outlined examples of SSS but should not be allocated to all customers under this framework? If so, please provide examples and explanations for each.

104. Proposed examples of SSS include 'facilities and/or supply that are subject to regulated cost recovery from a monopoly supplier as part of default service in a particular service area and are not part of a resource-specific supplier product (e.g. a green tariff)'. In this context, should a monopoly supplier include: (select all that apply) a. Vertically integrated investor-owned utility b. Government entity operating in a service area without supplier choice c. Distribution utility in a restructured market where certain electricity supply and/or contractual instrument purchases are subject to non-by passable, regulated cost recovery d. Other (please explain) e. Unsure

105. Please provide any additional comments regarding your response to question 104.

106. Allocation of SSS requires either suppliers allocating their SSS resources to customers or the development of a credible centralized registry or third-party registries that track SSS in order for organizations to claim their share. Is it acceptable that some reporters may be unable to claim SSS prior to a credible centralized registry or third-party registries being established? If not, how else might SSS be allocated in the absence of a registry?

107. Would you support a default option in cases where SSS data is not supplied by electricity providers, and no third-party registry is available, to designate certain resources as automatically qualifying as SSS? a. Yes b. No c. Unsure

108. If you answered “No” to question 107, please provide any additional comments on why you would not support a default option.

109. If you answered “yes” to question 107, which of the following criteria, if any, would you support as a method of designating resources as SSS. (select all that apply) a. Project age b. Technology or fuel type c. Project ownership (e.g. government owned projects) d. Projects tracked in compliance registries e. Combination of above criteria f. Other (please specify)

110. If you answered ‘Other' please provide additional feedback.

111. If SSS is not uniformly available across regions, how would this affect comparability of scope 2 MBM reporting? What interim solutions or disclosures would reduce inconsistency?

112. Please provide any additional feedback on SSS.

Updated definition of residual mix emission factors

113. On a scale of 1-5 do you support the updated definition of residual mix emission factors to reflect the GHG intensity of electricity, within the relevant market boundary and time interval, that is not claimed through contractual instruments, including voluntary purchases or Standard Supply Service allocations? a. Scale of 1 (no support) – 5 (fully support)

114. Please provide reasons of support, if any (select all that apply). a. Establishes clear definition for residual mix emission factors b. Improves accuracy and relevance of market-based reporting c. Protects the integrity of market-based accounting by avoiding double counting of attributes within the MBM d. Clarifies the market boundary a residual mix emission factor should be calculated for e. Improves comparability and transparency across organizations and regions f. Helps incentivize voluntary sourcing of contractual instruments g. Provides an option for reporters without access to an hourly residual mix emission factor h. Other (please explain)

115. Please provide comments regarding your selected reasons for support.

116. Please provide reasons of concern or why you are not supporting, if any (select all that apply). a. Requiring a residual mix emission factor to be calculated per market boundary will further reduce availability of residual mix emission factors b. Allowing reporters to use different temporal precision of residual mix emission factors within a deliverable market boundary will negatively impact comparability c. Market boundaries used for calculating a residual mix emission factor should be defined as the geographic boundaries of electricity sectors, which align with national, and under certain circumstances, multinational boundaries d. Markets should self-determine if Standard Supply Service is included in a residual mix emission factor e. Increases administrative complexity of calculating a residual mix emission factor f. Other (please explain)

117. Please provide comments regarding your selected reasons for why you are not supporting.

The following questions refer to the availability of residual mix emission factor data in global markets. Who should answer: Respondents with direct operational knowledge (users, operators, vendors, auditors): Please answer for up to three registries/markets you know well.