The content on this page has been converted from PDF to HTML format using an artificial intelligence (AI) tool as part of our ongoing efforts to improve accessibility and usability of our publications. Note:

- No human verification has been conducted of the converted content.

- While we strive for accuracy errors or omissions may exist.

- This content is provided for informational purposes only and should not be relied upon as a definitive or authoritative source.

- For the official and verified version of the publication, refer to the original PDF document.

If you identify any inaccuracies or have concerns about the content, please contact us at [email protected].

FRS Factsheet 12 - Presentation of the financial statements

This factsheet has been prepared by FRC staff to aid preparers in applying certain requirements of Section 4 'Statement of Financial Position' and Section 5 'Statement of Comprehensive Income and Income Statement' of FRS 102 'The Financial Reporting Standard applicable in the UK and Republic of Ireland', as well as certain requirements of FRS 101 'Reduced Disclosure Framework' and FRS 105 'The Financial Reporting Standard applicable to the Micro-entities Regime'. It should not be relied upon as a definitive or complete statement on the application of the standards and legislation, nor is it a substitute for reading the detailed requirements of the standards and legislation.

The FRC does not accept any liability to any party for any loss, damage or costs howsoever arising, whether directly or indirectly, whether in contract, tort or otherwise from any action or decision taken (or not taken) as a result of any person relying on or otherwise using this document or arising from any omission from it.

This document contains copyright material of the IFRS® Foundation (Foundation) in respect of which all rights are reserved.

No rights are granted to third parties other than as permitted by the Terms of Use (http://www.frc.org.uk/FRStermsofuse) without the prior written permission of the FRC and the Foundation.

Material issued in respect of the application of Financial Reporting Standards in the UK and the Republic of Ireland has not been prepared or endorsed by the International Accounting Standards Board.

© The Financial Reporting Council Limited 2025

The Financial Reporting Council Limited is a company limited by guarantee. Registered in England number 2486368. Registered Office: 13th Floor, 1 Harbour Exchange Square, London, E14 9GE

1. Introduction

Purpose and scope

This factsheet is primarily aimed at entities applying FRS 102 'The Financial Reporting Standard applicable in the UK and Republic of Ireland'. It also refers briefly to considerations for entities applying FRS 101 Reduced Disclosure Framework or FRS 105 'The Financial Reporting Standard applicable to the Micro-entities Regime'.

The purpose of this factsheet is to set out the options available for presenting the financial statements when applying the above standards. The relevant presentation requirements are set out in Section 4 'Statement of Financial Position' and Section 5 'Statement of Comprehensive Income and Income Statement' of FRS 102; the corresponding sections in FRS 105 are 'Section 4 Statement of Financial Position and Section 5 Income Statement'.

This factsheet contains references to UK company law. Republic of Ireland company law contains similar requirements to UK company law; corresponding legal references to those set out in this explainer are detailed in Appendix IV 'Republic of Ireland legal references' to FRS 102 and FRS 105.

The primary statements

References in company law to 'balance sheet' correspond to the 'statement of financial position' in accounting standards, and references in company law to 'profit and loss account' correspond to either the 'statement of comprehensive income' (if taking the 'single-statement approach') or the 'income statement' (if taking the 'two-statement approach') in accounting standards. Accounting standards may also require the presentation of a 'cash flow statement', a 'statement of changes in equity' or 'statement of income and retained earnings', but these are not addressed in company law and are not covered in this factsheet.

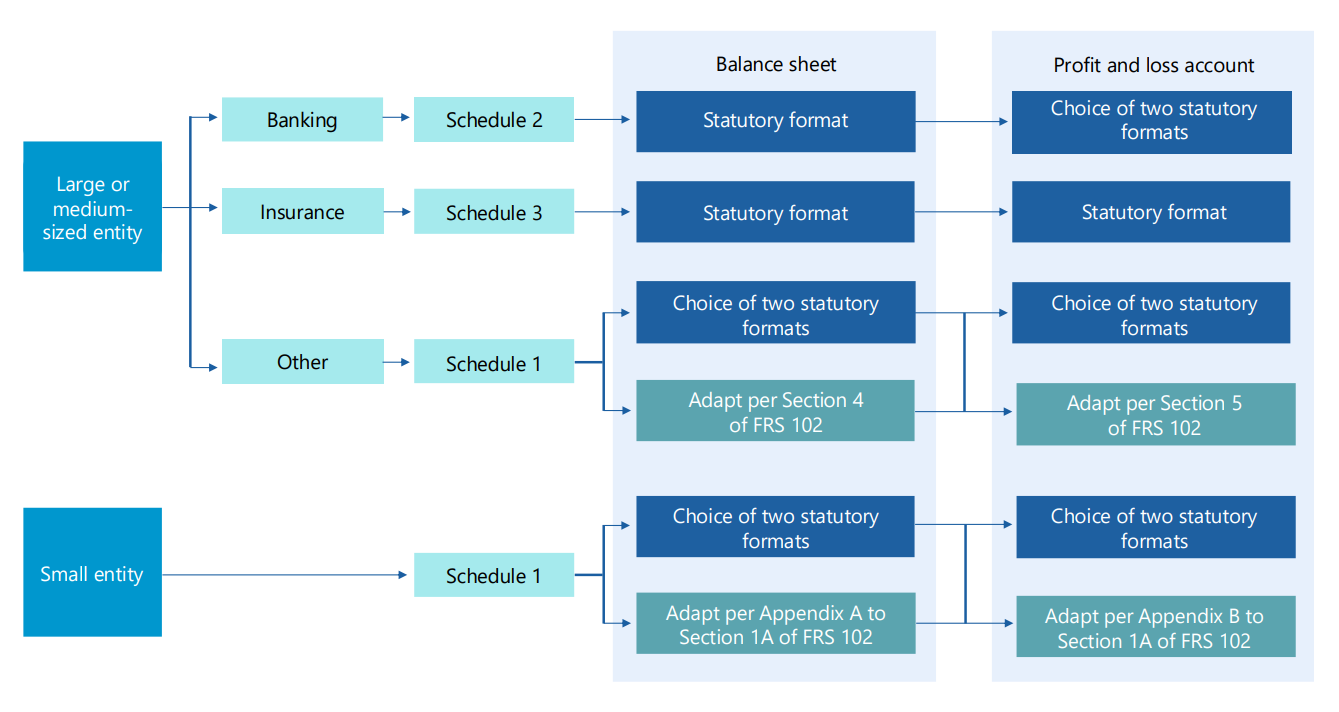

2. Presentation options under FRS 102

Presentation options for Balance Sheet and Profit and Loss Account

- Large or medium-sized entity

- Banking:

- Schedule 2

- Balance sheet: Statutory format

- Profit and loss account: Choice of two statutory formats

- Schedule 2

- Insurance:

- Schedule 3

- Balance sheet: Statutory format

- Profit and loss account: Statutory format

- Schedule 3

- Other:

- Schedule 1

- Balance sheet: Choice of two statutory formats OR Adapt per Section 4 of FRS 102

- Profit and loss account: Choice of two statutory formats OR Adapt per Section 5 of FRS 102

- Schedule 1

- Banking:

- Small entity

- Schedule 1

- Balance sheet: Choice of two statutory formats OR Adapt per Appendix A to Section 1A of FRS 102

- Profit and loss account: Choice of two statutory formats OR Adapt per Appendix B to Section 1A of FRS 102

- Schedule 1

Banking and insurance companies

Banking and insurance companies (for which the requirements are set out in Schedules 2 and 3 respectively of 'The Large and Medium-sized Companies and Groups (Accounts and Reports) Regulations 2008'1 (SI 2008/410)) have no option to apply an adapted format and must follow the statutory formats set out in those Schedules.

Other large and medium-sized entities

FRS 102 requires a preparer to present its financial statements in accordance with Part 1 of Schedule 1 to SI 2008/4102.

Schedule 1 sets out specific formats for presenting the balance sheet and the profit and loss account, which are generally referred to as the 'statutory formats'.

Schedule 1 also offers the option of 'adapting' the format of the profit and loss account and/or of the balance sheet. An entity can choose to adapt the format of just one of those statements or both of them. These are generally referred to as the 'adapted formats'.

Statutory formats

Schedule 1 sets out the statutory formats available for use – Formats 1 and 2 for the balance sheet and Formats 1 and 2 for the profit and loss account. These formats also include a set of headings, sub-headings and subtotals that must be presented.

What flexibility is available?

The following provisions apply when using any of the statutory formats:

- Items may be shown in greater detail than required by the particular format used.

- Additional items may be included if not already covered by the standard formats.

- The arrangement, headings and sub-headings must be adapted if the special nature of the company's business requires it.

Applying any of these provisions is not the same as choosing to adapt the formats of the balance sheet or profit and loss account. An entity applying these provisions is still applying the statutory formats, even if they look different to the standard formats set out in Schedule 1.

Adapted formats

An entity choosing to adapt the format of the balance sheet and/or of the profit and loss account must follow the requirements of FRS 102 in relation to the adapted formats. Certain paragraphs in FRS 102 apply, and certain glossary definitions differ, when choosing to adapt the formats.

For the balance sheet, the purpose specified in Schedule 1 for adapting the format of the balance sheet is to allow an entity to distinguish between current and non-current items in a different way to that provided by the statutory formats; no specific purpose is identified in Schedule 1 for adapting the format of the profit and loss account.

The statutory formats include groupings in the balance sheet for fixed assets, current assets, creditors falling due within one year and creditors falling due after one year; the adapted formats group the balance sheet into current and non-current assets, and current and non-current liabilities. These groups of terms are not interchangeable – for example, the definition of fixed assets is not the same as the definition of non-current assets.

What is the source of the adapted format requirements?

The ability to adapt the format of the balance sheet and/or of the profit and loss account is set out in Schedule 1 and requires that:

- the information given is 'at least equivalent to that which would have been required by the use of such format had it not been thus adapted'; and

- 'the presentation is in accordance with generally accepted accounting principles or practice'.

FRS 102 addresses both of these points, by setting out:

- the presentation and disclosure required when choosing to adapt the presentation of the balance sheet or profit and loss account (paragraphs 4.2B and 5.5B); and

- the minimum line items required in the balance sheet and profit and loss account of an entity which chooses to adapt the formats (paragraphs 4.2A and 5.5B).

Given the FRC's principle of seeking IFRS-based solutions, the requirements have been based on the requirements of IAS 1 'Presentation of Financial Statements'.

IAS 1 will be replaced by IFRS 18 'Presentation and Disclosure in Financial Statements' from 1 January 2027, subject to endorsement in the UK by the UK Endorsement Board3. In July 2025 the FRC proposed amendments4 to FRS 102 to reflect the replacement of IAS 1 with IFRS 18 for entities that choose to adapt the formats of the balance sheet and/or the profit and loss account.

Is there further flexibility available when adapting the formats?

Yes - just as with the statutory formats, the descriptions, ordering and aggregations set out in paragraphs 4.2A, 4.2B and 5.5B may be amended (as set out in paragraphs 4.2C and 5.5C), provided that the information given is still 'at least equivalent' to that required had the format(s) not been adapted.

If choosing to adapt, do I have to adapt both statements?

No – the ability to adapt the presentation of the balance sheet is separate from the ability to adapt the presentation of the profit and loss account, so a preparer can adapt either, both, or neither.

Small entities

Under the small entities regime, set out in 'The Small Companies and Groups (Accounts and Directors' Report) Regulations 2008'5 (SI 2008/409) there is again a choice between the statutory formats and the adapted formats.

A small entity that chooses to apply the small entities regime (and is therefore following the presentation and disclosure requirements of Section 1A 'Small Entities' of FRS 102), and that chooses to adapt the formats, is required to apply the presentation requirements set out in Appendix A 'Guidance on adapting the balance sheet formats' and Appendix B 'Guidance on adapting the profit and loss account formats' to Section 1A. These appendices state the line items that should be presented when choosing to adapt the formats, similar to Section 4 'Statement of Financial Position' and Section 5 'Statement of Comprehensive Income and Income Statement for large and medium-sized entities'.

Small entities also currently have the option of drawing up a less detailed 'abridged' balance sheet and/or profit and loss account. This option may be removed in due course, in accordance with the 'Economic Crime and Corporate Transparency Act 2023'6.

Consolidated financial statements

Schedule 6 of SI 2008/410 imposes additional requirements for the presentation of consolidated financial statements, but the requirements of Schedules 1-3 still apply and so the formats available are effectively identical.

3. Presentation options under FRS 101

An entity applying FRS 101, and within the scope of Schedule 1, has the option of adapting the formats of either or both of the balance sheet and the profit and loss account.

An entity that chooses to adapt the formats is required to apply the relevant requirements of adopted IFRS7. At present these presentation requirements are set out in IAS 1; subject to endorsement, the requirements of IFRS 18 will be effective from 1 January 2027. For an entity that chooses not to adapt the formats, or is not permitted to, the statutory formats are the same as for an FRS 102 preparer.

4. Presentation under FRS 105

There is no option to adapt the formats for micro-entities which apply FRS 105. Such entities must follow the statutory formats for micro-entities, which are set out in Section C of Part 1 of Schedule 1 to SI 2008/409 and reproduced in Sections 4 and 5 of FRS 105.

Financial Reporting Council

London office: 13th Floor, 1 Harbour Exchange Square, London, E14 9GE

Birmingham office: 5th Floor, 3 Arena Central, Bridge Street, Birmingham, B1 2AX

+44 (0)20 7492 2300 www.frc.org.uk

Follow us on LinkedIn

Footnotes

-

The Large and Medium-sized Companies and Groups (Accounts and Reports) Regulations 2008 ↩

-

Or, for a limited liability partnership, 'The Large and Medium sized Limited Liability Partnerships (Accounts) Regulations 2008' (SI 2008/1913). ↩

-

In the Republic of Ireland, by the European Commission ↩

-

FRED 87 Draft amendments to FRS 102 The Financial Reporting Standard applicable in the UK and Republic of Ireland - Adapted formats ↩

-

The Small Companies and Groups (Accounts and Directors' Report) Regulations ↩

-

See paragraphs AG1(h) and AG1(i) of the Application Guidance to FRS 101 ↩