The content on this page has been converted from PDF to HTML format using an artificial intelligence (AI) tool as part of our ongoing efforts to improve accessibility and usability of our publications. Note:

- No human verification has been conducted of the converted content.

- While we strive for accuracy errors or omissions may exist.

- This content is provided for informational purposes only and should not be relied upon as a definitive or authoritative source.

- For the official and verified version of the publication, refer to the original PDF document.

If you identify any inaccuracies or have concerns about the content, please contact us at [email protected].

Ernst & Young LLP Audit Quality Inspection and Supervision Report 2025

Using this publication

The Financial Reporting Council (FRC) is responsible for the regulation of UK statutory auditors and audit firms. We assess, via a fair evidence-based approach, whether firms are consistently delivering high-quality audits and are resilient.

This report sets out the FRC's findings on key matters relevant to audit quality at Ernst & Young LLP (EY or the firm). It should be used alongside the FRC's Annual Review of Audit Quality, which contains combined results and themes for all firms[^1] that were inspected this year.

Given our risk-based approach to selecting audits for inspection, it is important that care is taken when extrapolating our findings or assessment of quality to the whole population of audits performed by the firm. Given the sample sizes involved, changes from one year to the next cannot, on their own, be relied upon to provide a complete picture of a firm's performance.

Individual audit and System of Quality Management (SoQM) inspection findings are not the only metrics to assess audit quality. This report also considers other wider measures, such as the results of audit inspections completed by the Institute of Chartered Accountants in England and Wales (ICAEW) and results from the firm's own internal quality reviews. The firm's response to the findings and the actions it plans to take as a result, are included on page five and Appendix B.

This report is for general use by interested parties. However, we expect the following:

- EY to use this report and its peers' reports to facilitate continuous improvement through actions in its Single Quality Plan (SQP).

- Other audit firms of all sizes to use this report for examples of good practice.

- Audit Committees to use this report to help them assess the quality of their audit/auditor and when appropriate as part of the process of appointing a new auditor.

- Investors to use this report in making assessments about the quality of audit, transparency and accountability in the relevant markets.

Throughout this report, the following symbols are used:

- Represents a finding where the firm must take action to improve audit quality.

- Represents an example of good practice we identified in our supervision, and we encourage other firms to consider applying these if appropriate to their circumstances.

- Represents an observation relating to the firm's initiatives to improve audit quality.

Our Supervisory Approach[^2]

The audit supervisory teams in the FRC's Supervision Division work closely together to develop an overall view of the key issues for each firm to improve audit quality. We also collaborate to develop our future supervision work.

Further details on our approach to audit supervision can be found on our website. We also separately publish the findings of our major local audit inspections each year, the latest publication was in July 2025 and can be found on our website.

- Using this publication

- 1. Overview – overall assessment

- 1. Overview – Firm and FRC actions

- Ernst & Young LLP – at a glance

- 2. Inspection of individual audits

- 2. Inspection of individual audits

- 2. Inspection of individual audits

- 2. Inspection of individual audits

- Monitoring review results by the Quality Assurance Department of ICAEW

- 3. Inspection of the firm's system of quality management ISQM (UK) 1 and 2

- 3. Inspection of the firm's system of quality management ISQM (UK) 1 and 2

- 4. Forward-looking supervision

- 4. Forward-looking supervision

- Appendix A – Firm's internal quality monitoring

- Appendix B – EY's responses and actions

- Appendix B – EY's responses and actions

- Appendix B – EY's responses and actions

- Appendix C – ISQM (UK) 1 Glossary

The FRC does not accept any liability to any party for any loss, damage or costs howsoever arising, whether directly or indirectly, whether in contract, tort or otherwise from any action or decision taken (or not taken) as a result of any person relying on or otherwise using this document or arising from any omission from it.

© The Financial Reporting Council Limited 2025 The Financial Reporting Council Limited is a company limited by guarantee. Registered in England number 2486368. Registered Office: 13th Floor, Exchange Tower, 1 Harbour Exchange Square, London, E14 9GE

1. Overview – overall assessment

EY has continued to focus on consistently delivering high audit quality, leading to a number of improvements in the year. The communications from leadership around the importance of audit quality set a strong tone from the top. The audit quality strategy has been refreshed and prioritises key areas such as curious mindset, connected teams and fostering pride in the profession. We will continue to engage with the firm as it embeds the use of effectiveness measures to determine whether the actions taken are working, or whether other actions are needed.

Firm's system of quality management

EY has an established SoQM structure, with robust governance and a strong annual evaluation process. The firm has shown commitment to improving its SoQM and has strengthened its identification and assessment of responses to quality risks. However, the firm needs to increase its review and assessment of the network monitoring performed over the responses operated, and the resources provided to the UK firm, by other entities in the network.

FRC audit quality inspections

The percentage of audits inspected by the FRC requiring no more than limited improvements was 90%, which is an improvement on the prior year. For the FTSE 350, this has improved to 82%. None of the audits we inspected were found to require significant improvements. There were recurring findings related to the audit of impairment and, while less significant this year, the firm should continue to review the effectiveness of its actions in this area. The overall results profile for inspections by the ICAEW is 90% classified as good or generally acceptable (page 11) and the firm's internal quality monitoring results (Appendix A) show a year-on-year improvement for audits with no or minor findings, although the number of audits with material findings increased.

SoQM inspection approach

We assessed the following aspects of the scoped in areas of the firm's SoQM, with each one building upon the next.

- Do the quality risks appear complete and appropriate?

- Have appropriate responses been identified and described to demonstrate how quality risks can be mitigated?

- Was there adequate monitoring of these responses and other relevant information?

- Have deficiencies been identified and individually assessed?

- Was the aggregate impact of deficiencies assessed?

See good practice points and findings in section 3.

FRC audit quality review inspection results at EY

% of audits inspected by the FRC requiring no more than limited improvements (Section 2)

| Year | % |

|---|---|

| 2024/25 | 90% |

| 2023/24 | 76% |

| 2022/23 | 80% |

| 2021/22 | 65% |

| 2020/21 | 79% |

Bar chart showing percentage of audits requiring no more than limited improvements for each financial year. Indicated that 0 audits inspected by the FRC in 2024/25 required significant improvements.

Other audit quality inspection results at EY

The overall results profile for inspections by the ICAEW is 90% classified as good or generally acceptable (page 11) and the firm's internal quality monitoring results (Appendix A) show a year-on-year improvement for audits with no or minor findings, although the number of audits with material findings increased.

1. Overview – Firm and FRC actions

EY's response

At EY we are committed and proud to deliver high-quality audits that serve the public interest. We value the independent perspective of our regulators and the insights that they have provided during our regular interactions, including observations from our Supervisor and recommendations to enhance our SoQM.

We are pleased that 90% of our public interest audits inspected by the FRC were rated as 'good' or requiring 'limited improvements', and that this success is aligned with the ICAEW's QAD results, and our own internal monitoring. This positive outcome, the overall reduction in the extent of findings, and the many good practice examples cited by both regulators are a testament to the hard work of our people. We are learning from what has gone well and sharing and celebrating good practice.

Our root cause analysis[^3] has considered the overarching factors leading to positive grades, good practice and inspection findings, and identified the following contributors to our inspection outcomes:

- The extent and quality of timely involvement from senior team members;

- The extent of upfront planning and appropriate capture of thought processes, including evidencing professional scepticism and challenge or justification of legacy conclusions; and

- Collaboration and communication including good coaching and knowledge sharing within and between engagement teams.

Our Audit Quality Strategy[^4], underpinned by our Purpose-led Culture[^5], has been refreshed with an emphasis on greater consistency of execution. Enhancements include a focus on consistently embedding our strategic priorities; and accelerating change enabled by data, AI and technology.

EY's actions

We continue to assess our SoQM to simplify it where possible and remove duplicate or redundant controls, and make enhancements where appropriate. Actions planned and taken to respond to engagement inspection findings include:

- Communication – Emerging findings have been communicated to the practice, alongside guidance on avoiding similar issues and sharing examples of good practice.

- Standardisation – Enhancing our work programmes, templates and coaching packs to capture new challenges and learnings from regulatory reviews; whilst improving adoption of tools and enablement to help drive consistency.

Further details are included in Appendix B.

FRC's actions

In response to this year's findings, we will take the following action:

- Continue our inspection of completed audits and the firm's SoQM, including how the firm is responding to our findings.

- Maintain our supervision of the SQP using it to monitor the actions taken to improve audit quality. This will include audit quality initiatives relating to the standardisation of work programmes, culture, technology and resourcing.

- Continue to monitor the firm's effectiveness measures used in relation to audit initiatives, the SQP and the updated audit quality strategy.

Ernst & Young LLP – at a glance

Audits within the FRC's inspection scope[^6]

| Inspection cycle | FTSE 100 audits | FTSE 250 audits | Total audits in FRC scope | PIE Auditor Registration data[^7] Public Interest Entity (PIE) audits | Number of PIE Responsible Individuals[^7] |

|---|---|---|---|---|---|

| 2025/26 | 23 | 53 | 259 | 215 | 103 |

| 2024/25 | 23 | 52 | 283 | 238 | 103 |

| 2023/24 | 23 | 50 | 293 | 218 | 100 |

Audit fee income £m[^8]

Bar chart showing Audit fee income and PIE Audit fee income from 2022 to 2024. * Total Audit Fee Income: £626m (2022), £737m (2023), £837m (2024) * PIE Audit Fee Income: £227m (2022), £217m (2023), £266m (2024)

- Total Audits: 9,993[^9]

- Responsible Individuals: 279[^9]

- Professional Staff: 16,889[^9]

- Offices: 22[^9]

Audits inspected by the FRC[^10]

Diagram showing number of audits inspected by the FRC. * 2022-23: 20 * 2023-24: 17 * 2024-25: 20

Local audits[^11]

Pie chart showing breakdown of local audits for 2024-25. * Non-major audits: 73 * Major audits: 45 * Major audits inspected: 1

2. Inspection of individual audits

Our assessment of the quality of audits inspected: All

We inspected 20 individual audits this year and assessed 18 (90%) as requiring no more than limited improvements. These results are an improvement on prior years.

Bar chart showing the percentage of all audits inspected classified by improvement required, from 2020/21 to 2024/25.

| Category | 2020/21 | 2021/22 | 2022/23 | 2023/24 | 2024/25 |

|---|---|---|---|---|---|

| Good or limited improvements required | 15 | 11 | 16 | 13 | 18 |

| Improvements required | 4 | 6 | 4 | 4 | 2 |

| Significant improvements required | 0 | 0 | 0 | 0 | 0 |

The chart shows an increasing trend in 'Good or limited improvements required' and a decreasing trend in 'Improvements required' for all audits. No audits required 'Significant improvements'.

FTSE 350

Of the 11 FTSE 350 audits we inspected this year, we assessed 9 (82%) as requiring no more than limited improvements. These results are an improvement on prior years.

Bar chart showing the percentage of FTSE 350 audits inspected classified by improvement required, from 2020/21 to 2024/25.

| Category | 2020/21 | 2021/22 | 2022/23 | 2023/24 | 2024/25 |

|---|---|---|---|---|---|

| Good or limited improvements required | 9 | 7 | 8 | 9 | 9 |

| Improvements required | 3 | 2 | 1 | 3 | 2 |

| Significant improvements required | 0 | 0 | 0 | 0 | 0 |

The chart shows similar trends to the 'All Audits' chart, with no FTSE 350 audits requiring 'Significant improvements'.

The audits inspected in the 2024/25 cycle had year-ends ranging from June 2023 to March 2024. Changes to the proportion of audits falling within each category reflect a wide range of factors, including the size, complexity and risk of the audits selected for inspection and the individual inspection scope. Our inspections are also informed by the priority sectors and areas of focus. For these reasons, and given the sample sizes involved, changes from one year to the next cannot, on their own, be relied upon to provide a complete picture of a firm's performance and are not necessarily indicative of any overall change in audit quality at the firm. Given our risk-based approach, it is important that care is taken when extrapolating our findings or assessment of quality to the whole population of audits performed by the firm.

Information on how the FRC assesses audit quality and classifies findings between key findings and other findings, on individual inspections is available on our website.

2. Inspection of individual audits

We set out below the findings in areas where, based on our inspections, we believe improvements in audit quality are required. These findings related to key findings on our individual inspections, which impacted our assessment of quality in those audits (as set out on the previous page), as well as other findings in the same areas that occurred frequently.

| Findings | Why it is important |

|---|---|

| Improve the evaluation of short-term assumptions relating to goodwill and other intangible asset impairment | Auditors should adequately assess and challenge management's evaluation of impairment as this often involves significant management judgement and can be subject to management bias or error. |

| Improve the consistency of group audit oversight, including consideration of partner and senior staff rotation | The group audit team is responsible for the oversight of the group audit, including audit work at a component level, and should therefore demonstrate sufficient involvement throughout the audit. The FRC Ethical Standard requires threats to independence through long association, to be assessed and appropriate safeguards to be put in place. |

Analysis of areas with findings by significance

Bar chart showing number of inspections for each area, broken down by Key findings, Other findings, and No findings.

| Area | Key findings | Other findings | No findings | Total |

|---|---|---|---|---|

| Intangible asset impairment | 1 | 3 | 2 | 6 |

| Group audits | 1 | 8 | 1 | 10 |

This chart indicates that 'Other findings' were most prevalent across both areas, with 'Intangible asset impairment' having 1 key finding and 'Group audits' having 1 key finding.

Further details of the above findings, as well as good practice points, are set out on the following pages.

2. Inspection of individual audits

Improve the evaluation of short-term assumptions relating to goodwill and other intangible asset impairment

- Goodwill impairment: On one audit, there was insufficient evaluation and challenge by the audit team of the short-term growth and related discount rate assumptions used in management's goodwill impairment assessment for one Cash Generating Unit (CGU). The audit team also did not sufficiently challenge management on the extent of related sensitivity and significant estimate disclosures.

- Other asset impairment: One audit team, obtained insufficient evidence to conclude on the appropriateness of the impairment charge for an intangible asset; in particular, there was insufficient justification and evidence of challenge over the level of the risk adjustments applied to specific uncertainties. On two other audits, there was insufficient evidence of the audit team's evaluation and challenge of forecast redundancy costs and cost savings used in the impairment assessment of one individual CGU in each entity.

- On another audit, there was insufficient evidence of the oversight procedures for one of the components. Another audit team did not perform sufficient audit procedures for the consolidation adjustments impacting an overseas component.

- Partner and senior staff rotation: On two audits, there was insufficient evidence of assessment of safeguards for the independence threats arising from the long association of certain partners and senior staff. On one of these audits the audit team did not sufficiently communicate the safeguards to the Audit Committee or consider the full period of involvement in its consultations. Another audit team did not adequately demonstrate that appropriate safeguards had been applied for the threat of long association of certain partners and senior staff. On another audit there was insufficient justification for why a component audit partner was not a Key Audit Partner.

Improve the consistency of group audit oversight, including consideration of partner and senior staff rotation

- Group audit oversight: On one audit, there was insufficient evidence of appropriate oversight by the audit team of the component auditors' work in relation to significant components, and inaccurate reporting to the Audit Committee of the scope of work. On two other audits, there was inadequate justification for the extent of group oversight, in one case for oversight of a sub-group audit and, in the other, the scoping of work to be tested by the component auditors.

Other findings leading to improvements required

On one audit, the following findings contributed to the overall assessment of improvements required that are not included in the above findings:

- Deferred revenue: The audit team did not perform sufficient audit procedures, or raise sufficient challenge, in relation to the calculation of deferred revenue.

- Inventory valuation: There was insufficient audit evidence obtained for the valuation of inventory, in particular from the inventory cost testing.

2. Inspection of individual audits

We also identified good practice in the audits we inspected, including:

Risk assessment and planning

- Risk assessment: A group audit team extended its testing of journals to components that were initially out-of-scope due to their size, based on additional risk scanning procedures performed.

- Another audit team performed comprehensive risk assessment procedures over the Expected Credit Loss (ECL) model and demonstrated how this linked to the substantive procedures.

Execution

- Challenge of management: One audit team and its experts performed extensive integrity and logic checks on a pension provision model which resulted in an audit adjustment.

- Another audit team performed extensive procedures, challenging management's going concern assessment and related disclosures, including reviewing the impact of previously disclosed material uncertainties on trading performance against forecasts.

- Use of Specialists: One audit team obtained detailed input from multiple internal specialists, including valuation specialists and debt advisory teams from across the firm's global network, which facilitated a better understanding of going concern and viability risks.

- On another audit, the actuarial specialists enhanced the audit team's challenge of the entity's gross claims reserves by performing independent projections.

- The involvement of a specialist audit partner on another audit contributed to a robust approach to complex aspects of the audit.

- Group audit oversight: On one group audit, the Shared Service Centre staff, who were part of the group audit team, demonstrated comprehensive interactions with the rest of the group audit team and component auditors.

- One group audit team performed a comprehensive stand-back analysis of the correlation of revenue and marketing costs for all in-scope components, challenging the differences as appropriate.

- Extensive oversight procedures were performed on another group audit where an industry specialist was involved as part of the group audit team to review the underlying working papers of a component audit. There was also extensive evidence of the group audit partner's involvement and oversight of that component.

- A group audit team demonstrated effective oversight of the component audits through the use of data analytics tools, including identifying higher risk journal entries across all components and enhanced direction and oversight of the testing by the component audit teams.

- Another group audit team performed enhanced procedures to ensure that the differences between UK and international auditing and ethical standards were fully understood and procedures were in place to ensure compliance. The group audit team also engaged its own credit modelling specialists to challenge and oversee the work performed by the component auditor's credit modelling specialists.

- Ethics and independence: The audit team consulted promptly with the firm's Ethics Function when a perceived independence threat arose. The agreed responses and actions were clearly communicated to the Audit Committee.

Monitoring review results by the Quality Assurance Department of ICAEW

ICAEW undertakes independent monitoring of the firm's non-PIE audits, under delegation from the FRC as the Competent Authority. ICAEW's work covers private companies, smaller AIM listed companies, charities and pension schemes. The FRC is responsible for monitoring the firm's firm-wide controls and ICAEW additionally reviews training records for a sample of the firm's staff involved in the audit work within ICAEW remit.

Of the ten files we reviewed, nine files were either good or generally acceptable and one file required improvement. On the file requiring improvement, there was insufficient evidence to support the firm's conclusion on going concern.

A detailed report summarising the audit file review findings and any follow-up action proposed by the firm will be considered by ICAEW's Audit Registration Committee in July 2025.

Bar chart showing monitoring review results by ICAEW (2022-2024).

| Category | 2022 | 2023 | 2024 |

|---|---|---|---|

| Significant improvement required | 0 | 1 | 1 |

| Improvement required | 0 | 0 | 0 |

| Good/generally acceptable | 10 | 9 | 9 |

The chart indicates consistent performance with most files being classified as 'Good/generally acceptable'.

Good practice

ICAEW identified good practice across most of the files reviewed. Examples included:

- Well designed and clearly documented work on going concern.

- Opening balances work with specific consideration of the impact of a different materiality approach compared to the predecessor auditor.

- Involvement of the component auditors in the primary team's planning procedures.

ICAEW assesses audit quality as 'good', 'generally acceptable', 'improvement required', or 'significant improvement required'. File selection is focused towards higher risk and more complex audits. Given the sample size, changes from one year to the next cannot be relied upon to provide a complete picture of a firm's performance or overall change in audit quality.

3. Inspection of the firm's system of quality management ISQM (UK) 1 and 2

In this section, we set out the findings and good practice identified in our inspection of the firm's SoQM. 2024/25 is the first inspection cycle that we have solely inspected firms under ISQM (UK) 1, as 2023/24 was a transitional cycle from ISQC (UK) 1. In the interests of proportionality, we adopt a rotational approach to inspection, ensuring all components of the SoQM are inspected across a three-year cycle. Details of our ISQM (UK) rotational testing can be found on our website. A glossary of some key ISQM (UK) terms can be found in Appendix C.

Inspection approach in 2024/25 cycle

In this inspection cycle, we inspected the firm's SoQM risk assessment and the design and implementation of responses in the Governance and Leadership (G&L), Information and Communication (I&C), Human Resources (HR), and Relevant Ethical Requirements (RER) components of the firm's SoQM.

For each component we also inspected a small sample of the monitoring procedures performed by the firm to assess the operating effectiveness of responses. This sample focused on responses with significant elements of judgement, including management review controls and processes.

We also inspected the process, evidence, and outcome for the firm's annual evaluation of its SoQM as at 30 June 2024. This included how other sources of information on audit quality and the firm's SoQM were considered, and how the aggregated significance of findings and deficiencies were assessed. We did not independently perform, or reperform, this annual evaluation. As ISQM (UK) 1 is focused on how firms achieve continuous improvement, we assessed how the firm has developed its SoQM, including in response to the findings we shared during the inspection period.

We scoped our inspection of each component based on consideration of risk, including the results of previous monitoring and root cause analysis. We focused on high-risk areas in respect of:

| Component | Focus areas |

|---|---|

| G&L (annual review) | Reporting to leadership on the SoQM and the culture of quality |

| I&C (rotational review) | Promoting and driving two-way communication with and between audit personnel |

| HR (rotational review) | Resource management and allocations for audit engagements and SoQM activities |

| RER (annual review) | Approval of non-audit services (NAS), and the length of involvement, on audit engagements, by key audit partners and the firm |

3. Inspection of the firm's system of quality management ISQM (UK) 1 and 2

EY has an established SoQM structure, with robust governance and a strong annual evaluation process. The firm has shown commitment to improving its SoQM and has strengthened its identification and assessment of responses to quality risks. However, the firm needs to increase its review and assessment of the network monitoring performed over the responses operated, and the resources provided to the UK firm, by other entities in the network.

In this section, we are solely reporting on the specific matters where we have identified that further improvement is needed and areas where we have observed particularly good practice.

Design and implementation of responses to quality risks

- Workload monitoring: The firm did not sufficiently assess the appropriateness of its monitoring thresholds to identify individuals whose workloads may be too high or demonstrate mechanisms for consistent identification of individuals with prolonged periods of high workloads just below this threshold. Therefore, it was not clear how this enabled the firm to identify all individuals where follow-up might be required.

- Reliance on network monitoring of responses and resources: The firm received and reviewed reporting on the monitoring of SoQM responses operated outside the UK, by the network and other member firms, and discussed this reporting with the issuers. However, the firm did not undertake and evidence sufficient monitoring procedures to support its reliance on the monitoring of these responses, including where they provided assurance over the reliability of global resources used by the UK firm.

- Monitoring completeness of relevant UK approvals for non-audit services (NAS) sought by network firms: The global independence testing programme included monitoring of network firms' adherence to global NAS approval policy. However, the UK firm did not assess the design of this monitoring to determine the level of assurance this provided. The UK firm also relies on the global finance system to prevent timecodes for NAS being opened without relevant approvals, but did not map this response to the relevant risk, nor obtain appropriate specific assurance that this global control operated across the network.

Monitoring procedures

- Monitoring procedures over responses: Within the sample reviewed, the procedures undertaken to monitor the operation of certain responses did not consistently assess if all elements of the responses operated robustly and, in particular, how monitoring reviews were undertaken to identify and follow up concerns. In a few instances in the sample, the monitoring did not evidence assessment of whether individuals performing responses fully undertook these as designed.

Good Practice

- Identification of SoQM findings: The firm has established a rebuttable threshold for what audit inspection results, prevalence of root causes, and independence compliance testing results would give rise to a finding in the SoQM. This increased the consistency and clarity of the firm's assessment.

- Performance of the annual evaluation: The support for the firm's annual evaluation clearly demonstrated consideration of numerous inputs, including themes from root cause analysis, individually and alongside other sources of information to support assessments of where findings arose at the SoQM level.

4. Forward-looking supervision

We adopt a risk-focused, outcome-based, and proportionate approach to supervising firms, which complements our inspection programme. We balance holding firms accountable for promptly addressing quality findings with encouraging proactive improvement behaviours and sharing best practices to facilitate improvements across the firm and audit market. Each firm has a dedicated Supervisor who gathers evidence and risk indicators, identifies and prioritises actions firms must take to serve the public interest by enhancing audit quality and resilience. This includes anticipating future challenges and potential issues. Our observations from this year's work, along with updates on what the firm must do regarding previous observations, are set out below. When we identify findings, we require the firm to include actions in their SQP.

Single Quality Plan and other key quality initiatives

We require the largest PIE audit firms to maintain an SQP to drive measurable improvements in audit quality and resilience, and to demonstrate the effectiveness of actions taken. The SQP ensures action is prioritised in the most critical areas and enables firms to be held to account by us and their non-executives.

Observations

- SQP: The SQP is well established and provides clarity and focus on the firm's audit quality strategic priority areas. There is good oversight from the Audit Executive and the Audit Board. EY continues to evolve its SQP and has updated it for the new priorities in the FY25 Audit Quality Strategy, including actions at both a firm-wide and audit engagement level.

- Effectiveness measures: Improvements in the functionality of the SQP tool used allows the firm to assess the effectiveness of its actions at a holistic level, which are in turn used to assess the effectiveness of the SQP as a whole. Several of the actions are currently too early in their implementation to sufficiently assess their effectiveness. The firm must ensure that it has an appropriate balance between general and bespoke effectiveness measures including clearly defined timescales and specific objectives where appropriate.

Reframing work intensity:

Over the past few years the firm has taken specific actions to reduce average hours and promote a more equitable split of work for its auditors. As well as retaining a focus on these areas, the firm focused on understanding the science that leads to feelings of work intensity and how to equip their teams with useful skills for life. These are positive initiatives to improve and sustain audit quality whilst keeping the role fulfilling and rewarding.

4. Forward-looking supervision

Upholding high standards and continuous improvement

We expect firms to take prompt action to address quality findings and to set a tone at the top that prioritises continuous improvement.

Observations

- Tone at the top: The firm remains clear and consistent in its communications around the importance of audit quality. These communications are well linked to EY's strategic priorities. Audit leadership have shared detailed examples of good practice to bring their messages to life.

- Non-financial sanctions (NFS) and constructive engagement: We have engaged on four NFS in the period since the last report, all of which are ongoing. The firm has responded positively. There are no active constructive engagement cases.

- Culture: The firm has continued to roll out initiatives aimed at improving and embedding its culture and desired behaviours, including the launch of an Audit Culture Reporting Tool. Firm-wide culture reporting should be reviewed to ensure it includes sufficient information to enable those charged with governance to effectively oversee culture and behavioural risk.

- RCA: The firm's RCA process has been updated in the period since the last report to reflect updates at the global network level. The firm continues to speed up the completion of RCAs and runs focus groups alongside the RCA process to get a real-time perspective on factors impacting on audit quality.

Emerging risks and trends

Our forward-looking supervision aims to aid firms by anticipating challenges and risks from emerging trends before quality issues occur.

Industry trends:

All firms are impacted by emerging risks and trends in the industry related to:

- The use of technology and AI in the audit; and

- Changes to workforce and staff / partner development needs as a result of the above and other drivers.

These are addressed further in the 2025 Annual Review of Audit Quality. We are working with firms to understand how they are responding to these trends whilst safeguarding audit quality.

Observations

- Financial interest compliance rates: The firm has undertaken an exercise in the year to ensure that its staff's personal independence records are up to date. The firm needs to ensure these records are maintained and regularly updated as part of business as usual to improve compliance results going forward.

- Overseas Delivery Centres: The firm is taking a phased approach to expanding the nature and extent of work performed by its Overseas Delivery Centres. It is important that the firm has effective monitoring procedures in place to assess whether the additional safeguards that have been implemented are effective.

Appendix A – Firm's internal quality monitoring

This appendix sets out information prepared by the firm relating to its internal quality monitoring for individual audit engagements (Audit Quality Review, or internal AQR). We have not verified the accuracy or appropriateness of these results. The appendix should be read together with the firm's Transparency Report for 2024 and its 2025 report (when published) which provide further detail of the firm's internal quality monitoring approach, results, root cause analysis, remediation, and wider system of quality management. Due to differences in how inspections are performed and rated, the results of the firm's internal quality monitoring are not directly comparable to those of other firms or external regulatory inspections.

Results of internal quality monitoring [^12]

The results of the firm's internal AQR process for 2024 and two previous years are set out below. The 2024 internal AQR process comprised inspections of 124 individual corporate audits (2023: 118) with financial year ends between 30 June 2022 and 4 April 2024 inclusive.

Bar chart showing the results of internal quality monitoring from 2022 to 2024.

| Category | 2022 | 2023 | 2024 |

|---|---|---|---|

| No or minor findings | 87% | 90% | 91% |

| Findings that were more than minor but less than material | 11% | 9% | 5% |

| Material findings | 2% | 1% | 4% |

The chart shows a consistent high percentage of 'No or minor findings' and a low percentage of 'Material findings'.

Themes arising from internal quality monitoring

In 2024 91% of audits reviewed had no or only minor findings. Where grade driving findings occurred on more than one engagement, they related to audit areas inspected on most engagements.

Five engagements had grades that were driven by material findings. These findings related to: Specific aspects of substantive testing including insufficient procedures performed in relation to revenue and goodwill and intangible assets (including impairment); going concern procedures; journal entry testing procedures; an error noted in an audit opinion; and lack of evidence of timely and appropriate supervision and review. Insufficient procedures performed in relation to goodwill and intangible assets was also a material finding in the prior year.

Six engagements had grades that were driven by findings that, whilst not concluded as material, were not minor. There was more than one finding in the following areas: substantive testing including revenue procedures; and immaterial audit differences not identified or recorded in the summary of audit differences schedule. The latter was identified as a more than minor finding for the first time in 2024.

Appendix B – EY's responses and actions

A. Review of individual audits and the firm's system of quality management

Our inspection outcomes reflect an improvement on the prior year both in terms of the overall gradings achieved and the number and nature of findings per engagement. For the fifth consecutive year, none of our audits have been assessed as requiring significant improvements by the FRC. The FRC and ICAEW have also identified good practice examples, some of which overlap with findings. Our RCA (see Section B) reinforces this message, that our goal needs to be consistency. Our FY26 Audit Quality Strategy (see Section C) is therefore an evolution rather than a revolution. It is underpinned by our Purpose-led Culture (see Section D), which unites our people around the common purpose of serving the public interest and having a sense of pride in the profession and in the impact of the work that we do.

Our strive for continuous improvement means that we have sought to learn from inspection findings throughout the cycle by further accelerating our RCA process and communicating emerging themes and good practices to our audit teams. A number of responsive actions have therefore already been taken. Each action is captured, and its effectiveness measured, within our SQP. Actions taken and planned include:

- Updating and promoting our Strong Team Culture guide, which illustrates the factors that enabled teams to develop a strong team culture and to achieve good audit quality. Examples include how teams maintain presence, engagement and motivation in an in person and hybrid working environment.

- Using firmwide events, such as our annual Quality Summit, Culture of Audit Quality Roadshows, and quarterly Audit Update webcasts, to share and reinforce quality messages. This has included celebrating success and spotlighting successful audit teams – encouraging them to be proud of what they have achieved and to share their experiences with the rest of the audit practice.

- Our Audit Trust Awards recognise, celebrate and reward those who are modelling the behaviours we know underpin high-quality audits, such as coaching and demonstrating a sceptical mindset.

- Continuing to use our Audit Quality SharePoint and weekly top tips emails to share good practice examples, including sanitised example documents.

- Embedded AI is enhancing accuracy and enabling automated internal consistency checks and standardisation. We are also expanding our use of AI to make our knowledge resources more accessible to teams.

- Enhancing and expanding our repository of standardised workpapers and coaching packs, ensuring that they capture learnings from regulatory interactions and findings.

- Supporting individuals and teams to manage their capacity, including targeted interventions by business leaders to proactively provide additional support to respond to evolving circumstances. As a result, we have seen a reduction in the instances where insufficient resource has been identified as a root cause.

Our actions in response to the FRC's SoQM findings are already showing positive results. Ensuring the right balance of work intensity remains a continued focus for the firm. Within our SoQM we are better defining thresholds and enhancing our monitoring of prolonged periods of high workload. We acknowledge the FRC's finding on the sufficiency of our procedures concerning reliance on network resources and responses. We have already enhanced our interactions, review and challenge of the global SoQM in the FY24 SoQM cycle and continue to collaborate with our Global SoQM teams to facilitate further improvements in this area.

Appendix B – EY's responses and actions

B. Root Cause Analysis

Our RCA process is a well-established tool supporting our drive for continuous improvement. This year we have completed 120 RCAs in total across a number of areas, including all FRC inspections, a sample of ICAEW inspections, all audits with more than minor findings from our own internal monitoring inspections, and other areas from firmwide reviews. We have also enhanced our root cause categorisations to provide a clearer link to our SoQM and better assess whether RCA outcomes are indicative of SoQM findings.

The number of adverse inspection outcomes has reduced this year, as has the number of findings per inspection. Although we are learning from the few examples where the high standards we hold ourselves to have not been met, we have maintained our focus on positive quality outcomes and the behaviours and circumstances that have enabled them.

Consistent with previous years, the key message coming from our RCA has been the importance of senior team members fostering a strong team culture, working together well from the outset of the audit and using the enablement to support the delivery of high-quality audits:

| Theme | RCA Insights | FY26 Strategy Response |

|---|---|---|

| Senior Team Member Involvement | A high degree of partner/executive engagement remains the top driver for positive quality outcomes. Conversely, insufficient upfront involvement from senior team members has been seen to have a negative impact on audit quality. | We are encouraging teams to continuously enhance their engagement, motivation and development of others. |

| Communication and Collaboration | Effective communication and collaboration result in well-informed team members who are benefiting from live coaching and regular interactions. | We are emphasising communication through in-person interactions and other effective channels to enable engaging coaching. |

| Upfront Planning | Setting clear expectations on strategy and timelines, reinforced by management buy-in and proactive communication has a positive impact on audit quality. Conversely, insufficient planning and challenge of the approach adopted has a negative impact on the ability to evidence professional scepticism in the audit. | We are expanding our repository of industry-specific examples and encouraging a curious mindset to support teams in applying an appropriate level of challenge, consistently. |

| Standardised Work Programmes | Audit teams using existing guidance and standardised work programmes evidence professional scepticism more clearly and consistently and see fewer findings in regulatory reviews. | We are taking steps to accelerate the adoption of standardised work programmes and sharing best practice. |

Appendix B – EY's responses and actions

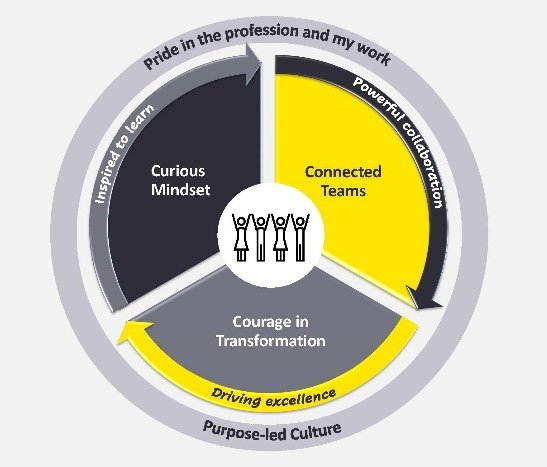

C. Audit Quality Strategy (AQS)

Our FY25 AQS was anchored in having pride in the profession and in the difference that the work of auditors makes, supported by a purpose-led culture. This was fully aligned with and enhanced by our new EY Global strategy 'All in', which includes an unwavering commitment to audit quality and significant investment in innovation.

Our focus areas were:

- Curious mindset – we are developing curious and confident individuals with strong commercial acumen who are inspired to learn.

- Connected teams – we are fostering greater collaboration between our people, teams and specialists; harnessing the full power of EY. This is further enabled by proactive coaching.

- Continuous improvement – individually and in teams we are striving for continuous improvement and driving excellence, supported by an increased focus on standardisation and simplification.

FY26 strategy enhancements:

The core of our strategy remains unchanged with a continued focus in pride in our profession and the difference our work makes, with refinements to drive further consistency in the behaviours needed to achieve each of these desired outcomes:

We continue to accelerate our progress towards consistency by empowering our people with a renewed focus on transformation. We want our people to be bold in embracing and leveraging AI and technology, and to support each other by sharing insights and best practice.

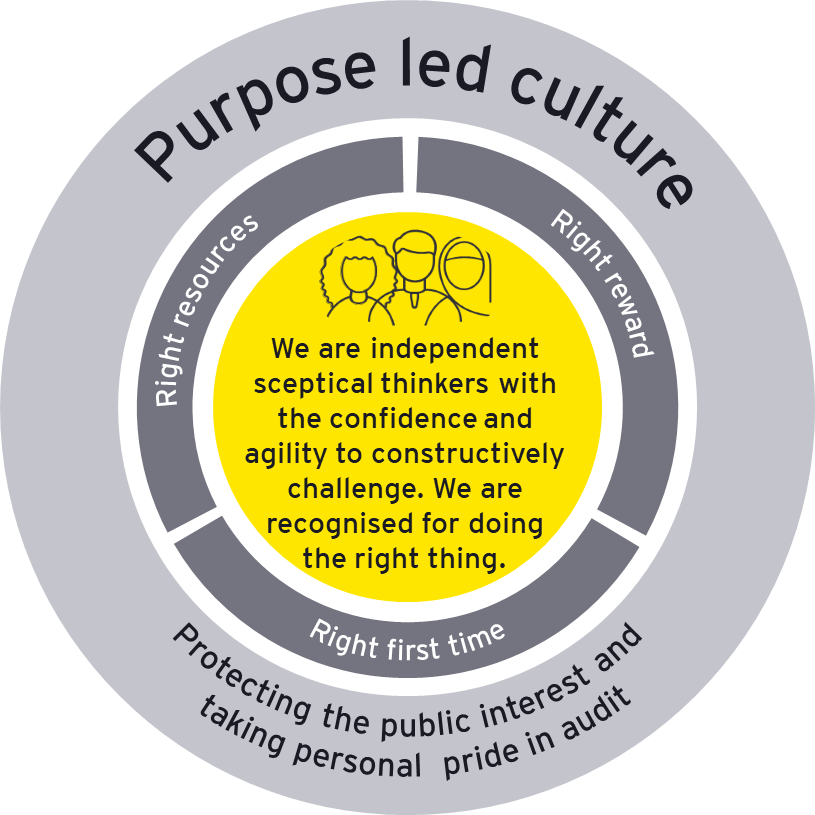

D. Our Purpose-Led Culture

At the heart of our strategy is our Purpose-led culture, which enables our people to embed the right behaviours needed for consistent delivery of quality audits and engenders pride in the profession and the important work that they do.

E. Looking ahead

Delivering consistent high-quality audits that serve the public interest is our priority. We are proud of our people and the role that they play in delivering on this shared purpose.

Circular diagram illustrating three core values: Curious Mindset, Connected Teams, and Courage in Transformation, supported by phrases like Powerful Collaboration and Purpose-led Culture.

Circular diagram detailing a "Purpose led culture" emphasizing "Right resources," "Right reward," and "Right first time," centered on independent, skeptical thinking.

Appendix C – ISQM (UK) 1 Glossary

The following definitions were extracted from ISQM (UK) 1[^13].

| Term | Definition |

|---|---|

| System of quality management (SoQM) | A system designed, implemented and operated by a firm to provide the firm with reasonable assurance that: i. The firm and its personnel fulfil their responsibilities in accordance with professional standards and applicable legal and regulatory requirements, and conduct engagements in accordance with such standards and requirements; and ii. Engagement reports issued by the firm or engagement partners are appropriate in the circumstances. A system of quality management under ISQM (UK) 1 addresses the following eight components: * The firm's risk assessment process; * Governance and leadership; * Relevant ethical requirements; * Acceptance and continuance of client relationships and specific engagements; * Engagement performance; * Resources; * Information and communication; and * The monitoring and remediation process. Firms are required to perform their first annual evaluation of the SoQM by 15 December 2023. |

| Quality objectives | The desired outcomes in relation to the components of the system of quality management to be achieved by the firm. |

| Quality risk | A risk that has a reasonable possibility of: i. Occurring; and ii. Individually, or in combination with other risks, adversely affecting the achievement of one or more quality objectives. |

| Response | Policies or procedures designed and implemented by the firm to address one or more quality risk(s) in relation to its system of quality management: i. Policies are statements of what should, or should not, be done to address a quality risk(s). Such statements may be documented, explicitly stated in communications or implied through actions and decisions. ii. Procedures are actions to implement policies. |

| Findings | Information about the design, implementation and operation of the system of quality management that has been accumulated from the performance of monitoring activities, external inspections and other relevant sources, which indicates that one or more deficiencies may exist. |

| Term | Definition | | Description | A deficiency | Description | | * | *Financial Reporting Council | | * | *Financial Reporting Council | | Description | A | | * | *1. Introduction | Description | | Description | A | | | Description | A | | Description | A | | Description | A | | Description | A | | Description | A | | Description | A | | Description | | | Description | A | | Description | | | Description | | | Description |