The content on this page has been converted from PDF to HTML format using an artificial intelligence (AI) tool as part of our ongoing efforts to improve accessibility and usability of our publications. Note:

- No human verification has been conducted of the converted content.

- While we strive for accuracy errors or omissions may exist.

- This content is provided for informational purposes only and should not be relied upon as a definitive or authoritative source.

- For the official and verified version of the publication, refer to the original PDF document.

If you identify any inaccuracies or have concerns about the content, please contact us at [email protected].

FRS 102 Factsheet 3 - Statement of cash flows

This factsheet has been prepared by FRC staff to aid preparers in applying Section 7 'Statement of Cash Flows' of FRS 102. It should not be relied upon as a definitive statement on the application of the standard nor is it a substitute for reading the detailed requirements of FRS 102.

The FRC does not accept any liability to any party for any loss, damage or costs howsoever arising, whether directly or indirectly, whether in contract, tort or otherwise from any action or decision taken (or not taken) as a result of any person relying on or otherwise using this document or arising from any omission from it.

This document contains copyright material of the IFRS® Foundation (Foundation) in respect of which all rights are reserved.

No rights are granted to third parties other than as permitted by the Terms of Use (www.frc.org.uk/FRStermsofuse) without the prior written permission of the FRC and the Foundation.

Material issued in respect of the application of Financial Reporting Standards in the UK and the Republic of Ireland has not been prepared or endorsed by the International Accounting Standards Board.

© The Financial Reporting Council Limited 2024

The Financial Reporting Council Limited is a company limited by guarantee. Registered in England number 2486368. Registered Office: 8th Floor, 125 London Wall, London EC2Y 5AS

1. Introduction

This factsheet has been prepared to illustrate the format of the statement of cash flows prepared in accordance with Section 7 'Statement of Cash Flows' of FRS 102, and to provide guidance on the preparation of the statement of cash flows and the associated disclosures. Note, however, that in a full set of financial statements, comparatives would be provided.

2. Background and scoping

Statement of cash flows

A statement of cash flows prepared under FRS 102:

- reconciles the movement in cash and cash equivalents (not just cash) year on year;

- groups cash flows into three headings - cash flows from operating, investing and financing activities;

- requires the reconciliation of a measure of profit to cash flows from operating activities; and

- requires the preparation of three main supporting notes a breakdown of the components that make up cash and cash equivalents, an analysis of changes in net debt, and disclosures about supplier finance arrangements.

Periodic review 2024 amendments

As part of the 'Periodic Review 2024 amendments', Section 20 'Leases' was revised to eliminate the distinction between operating leases and finance leases for lessees, and require recognition of more leases on the balance sheet.

Cash flows from operating leases would previously have been included within operating activities, whereas cash flows from finance leases would have related to payment of interest (classified either as a financing or an operating cash flow) and repayment of capital (classified as a financing cash flow).

Under the new requirements of Section 20, cash flows from leases for which a recognition exemption has been taken are included within operating activities, whereas cash flows from leases recognised on the balance sheet relate to payment of interest (classified either as a financing or an operating cash flow) and repayment of capital (classified as a financing cash flow).

Whilst the changes to Section 20 did not require significant consequential changes to Section 7, the result is that cash flows for the payment of interest and the repayment of capital will be more prevalent in the statement of cash flows.

Other topics covered by Section 7

As well as the topics covered in this factsheet, Section 7 also covers topics including the treatment of foreign currency cash flows, income tax cash flows and cash flows associated with hedging contracts.

Exemptions from presenting a statement of cash flows

Certain entities applying FRS 102 can take an exemption from presenting a statement of cash flows and related notes:

- Paragraph 3.1B allows an entity that qualifies as small (regardless of the reporting regime it applies) to take an exemption unless an applicable SORP, law or other relevant regulation requires it to present a statement of cash flows.

- Paragraph 1.12(b) allows a qualifying entity (i.e. an entity included in publicly available consolidated financial statements which are intended to give a true and fair view, as set out in the Glossary to FRS 102) to take an exemption, provided that it complies with certain conditions set out in paragraph 1.11.

- Paragraph 7.1A allows certain types of entities (mutual life assurance companies, retirement benefit plans, and investment funds meeting certain conditions) to take an exemption.

3. Presentation and disclosure

Presentation

Reporting cash flows from operating activities

Paragraph 7.7 requires cash flows from operating activities to be presented using either the indirect or the direct method. The illustrative statement of cash flows in this factsheet uses the indirect method, which is the method most commonly applied in the UK. The reconciliation of profit or loss to cash from operations can be shown either on the face of the statement of cash flows or in the notes.

Under the indirect method, paragraph 7.8 allows the reconciliation to start with 'a measure of profit or loss disclosed in the statement of comprehensive income'. This means that entities are permitted to use any profit figure (including operating profit) as a starting point for the reconciliation, if that profit figure appears as a subtotal in their statement of comprehensive income. The reconciling items required will vary depending on which profit figure is used. The illustrative statement of cash flows uses operating profit.

Cash and cash equivalents

As set out in paragraph 7.2, cash equivalents are short-term, highly liquid investments that are readily convertible to known amounts of cash and that are subject to an insignificant risk of changes in value.

Overdrafts

As set out in paragraph 7.2, bank overdrafts are normally considered to be financing activities, similar to borrowings. However, if overdrafts are repayable on demand and form an integral part of an entity's cash management, they are a component of cash and cash equivalents, and should be presented as such in the analysis of changes in net debt. This factsheet illustrates the latter presentation.

Interest and dividends

Paragraph 7.14 sets out that cash flows relating to interest paid, dividends paid, interest received and dividends received shall be presented separately.

Paragraphs 7.15 and 7.16 set out that:

- Interest and dividends paid may be classified as either financing cash flows or operating cash flows.

- Interest and dividends received may be classified as either investing cash flows or operating cash flows.

These classifications shall be made consistently from period to period.

Non-cash transactions

Paragraph 7.18 requires that investing and financing transactions that do not require the use of cash or cash equivalents shall be excluded from the statement of cash flows. Examples of such transactions include the acquisition of an asset by means of a lease, the acquisition of an entity by means of an equity issue, and the conversion of debt to equity. Disclosure may be required of such items in the analysis of changes in net debt (see below).

Disclosures

Components of cash and cash equivalents

Paragraph 7.20 requires an entity to present the components that make up the cash and cash equivalents balance, and a reconciliation of this amount to the amounts shown in the statement of financial position if they are different.

Paragraph 7.21 requires the disclosure of cash held by the entity but which is not available for use (including amounts sometimes referred to as 'restricted cash'). There is no such cash in the illustrative statement of cash flows.

Analysis of changes in net debt

Paragraph 7.22 requires an entity to present a net debt reconciliation. This analysis does not need to be presented for prior periods.

Net debt (as defined in FRS 102) consists of the borrowings of an entity, together with any related derivatives and obligations under leases, less any cash and cash equivalents.

Supplier finance arrangements

Paragraph 7.20C sets out disclosure requirements in respect of supplier finance arrangements.1 The exemption for qualifying entities from the requirements of this paragraph, as set out in paragraphs 1.11 and 1.12(b), is conditional on disclosures equivalent to those required by paragraph 7.20C being included in the consolidated financial statements in which the qualifying entity is included.

This factsheet does not illustrate the supplier finance arrangements disclosures.

4. Illustrative statement of cash flows

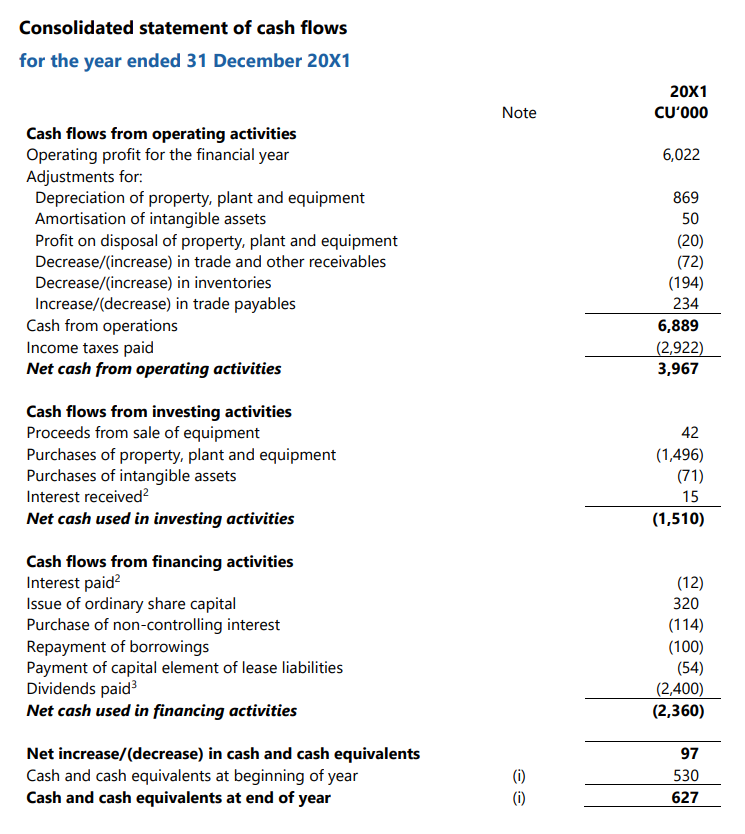

Consolidated statement of cash flows for the year ended 31 December 20X1

Screenshot of the Consolidated statement of cash flows. Accessible tables of the data are in the next section.

Cash flows from operating activities

| Item Description | Note | 20X1 CU'000 |

|---|---|---|

| Operating profit for the financial year | 6,022 |

Adjustments for:

| Item Description | Note | 20X1 CU'000 |

|---|---|---|

| Depreciation of property, plant and equipment | 869 | |

| Amortisation of intangible assets | 50 | |

| Profit on disposal of property, plant and equipment | (20) | |

| Decrease/(increase) in trade and other receivables | (72) | |

| Decrease/(increase) in inventories | (194) | |

| Increase/(decrease) in trade payables | 234 | |

| Cash from operations | 6,889 | |

| Income taxes paid | (2,922) | |

| Net cash from operating activities | 3,967 |

Cash flows from investing activities

| Item Description | Note | 20X1 CU'000 |

|---|---|---|

| Proceeds from sale of equipment | 42 | |

| Purchases of property, plant and equipment | (1,496) | |

| Purchases of intangible assets | (71) | |

| Interest received2 | 15 | |

| Net cash used in investing activities | (1,510) |

Cash flows from financing activities

| Item Description | Note | 20X1 CU'000 |

|---|---|---|

| Interest paid2 | (12) | |

| Issue of ordinary share capital | 320 | |

| Purchase of non-controlling interest | (114) | |

| Repayment of borrowings | (100) | |

| Payment of capital element of lease liabilities | (54) | |

| Dividends paid3 | (2,400) | |

| Net cash used in financing activities | (2,360) |

Net increase/(decrease) in cash and cash equivalents

| Item Description | Note | 20X1 CU'000 |

|---|---|---|

| Net increase/(decrease) in cash and cash equivalents | 97 | |

| Cash and cash equivalents at beginning of year | (i) | 530 |

| Cash and cash equivalents at end of year | (i) | 627 |

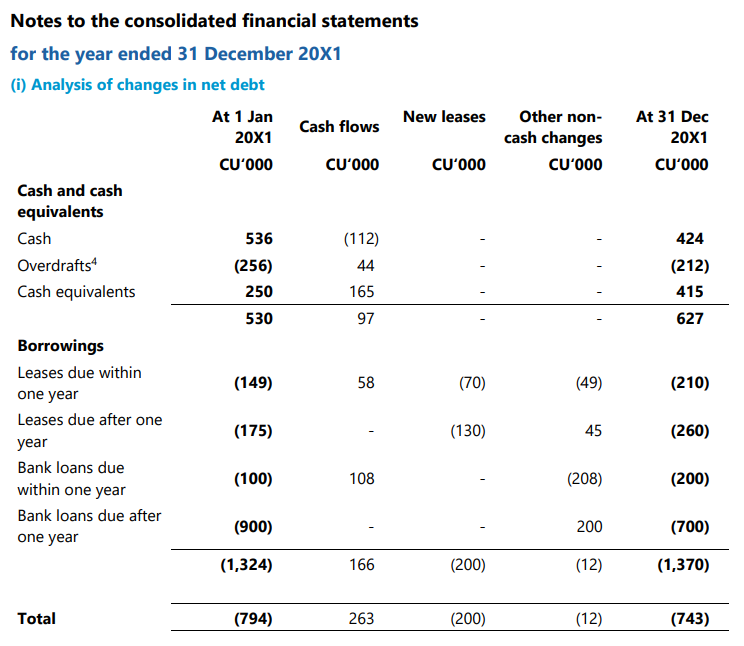

Notes to the consolidated financial statements for the year ended 31 December 20X1

(i) Analysis of changes in net debt

Screenshot of the Notes to the consolidated financial statements. Accessible tables of the data are in the next section.

Cash and cash equivalents

| At 1 Jan 20X1 CU'000 | Cash flows CU'000 | New leases CU'000 | Other non-cash changes CU'000 | At 31 Dec 20X1 CU'000 | |

|---|---|---|---|---|---|

| Cash | 536 | (112) | - | - | 424 |

| Overdrafts4 | (256) | 44 | - | - | (212) |

| Cash equivalents | 250 | 165 | - | - | 415 |

| Total | 530 | 97 | 627 |

Borrowings

| At 1 Jan 20X1 CU'000 | Cash flows CU'000 | New leases CU'000 | Other non-cash changes CU'000 | At 31 Dec 20X1 CU'000 | |

|---|---|---|---|---|---|

| Leases due within one year | (149) | 58 | (70) | (49) | (210) |

| Leases due after one year | (175) | - | (130) | 45 | (260) |

| Bank loans due within one year | (100) | 108 | - | (208) | (200) |

| Bank loans due after one year | (900) | - | - | 200 | (700) |

| Total | (1,324) | 166 | (200) | (12) | (1,370) |

Total

| At 1 Jan 20X1 CU'000 | Cash flows CU'000 | New leases CU'000 | Other non-cash changes CU'000 | At 31 Dec 20X1 CU'000 | |

|---|---|---|---|---|---|

| Total | (794) | 263 | (200) | (12) | (743) |

The columns in the example illustrate items (a), (c) and (d) from the analysis requirements of paragraph 7.22, but the illustration assumes that the entity has nothing to disclose in respect of (b) the acquisition and disposal of subsidiaries or (e) the recognition of changes in market value and exchange rate movements.

Financial Reporting Council

8th Floor 125 London Wall London EC2Y 5AS +44 (0)20 7492 2300

www.frc.org.uk

Follow us on Linked in or X @FRCnews

-

These disclosure requirements were introduced by the Periodic Review 2024 amendments and are effective for accounting periods beginning on or after 1 January 2025, with early application permitted. ↩

-

Paragraph 7.15 gives an entity the choice to include interest paid and received either in operating cash flows, or (respectively) as financing and investing cash flows. ↩↩

-

Paragraph 7.16 gives an entity the choice to include dividends paid either in operating cash flows, or as financing cash flows. ↩

-

See note above regarding the presentation of overdrafts. ↩