The content on this page has been converted from PDF to HTML format using an artificial intelligence (AI) tool as part of our ongoing efforts to improve accessibility and usability of our publications. Note:

- No human verification has been conducted of the converted content.

- While we strive for accuracy errors or omissions may exist.

- This content is provided for informational purposes only and should not be relied upon as a definitive or authoritative source.

- For the official and verified version of the publication, refer to the original PDF document.

If you identify any inaccuracies or have concerns about the content, please contact us at [email protected].

BDO LLP Audit Quality Inspection and Supervision Report 2024

The Financial Reporting Council (FRC) is responsible for the regulation of UK statutory auditors and audit firms. We assess, via a fair evidence-based approach, whether firms are consistently delivering high-quality audits and are resilient.

This report sets out the FRC’s findings on key matters relevant to audit quality at BDO LLP (BDO or the firm). It should be used alongside the FRC’s Annual Review of Audit Quality, which contains combined results and themes for all Tier 1 firms1 that are inspected annually.

Given our risk-based approach to selecting audits for inspection, it is important that care is taken when extrapolating our findings or assessment of quality to the whole population of audits performed by the firm. Given the sample sizes involved, changes from one year to the next cannot, on their own, be relied upon to provide a complete picture of a firm’s performance.

This report also considers other, wider measures of audit quality such as results from the firm’s own internal quality reviews. The firm’s response to the findings and the actions it plans to take as a result, are included on page five and Appendix B. The Institute of Chartered Accountants in England and Wales (ICAEW) did not inspect a sample of the firm’s non-PIE audits this year, in accordance with its planned rotational inspection programme and therefore there are no ICAEW results included in this report.

This report is for general use by interested parties. However, we expect the following:

- BDO to use this report and its peers’ reports to facilitate continuous improvement through actions in its Single Quality Plan (SQP).

- Other audit firms of all sizes to use this report for examples of good practice.

- Audit Committees to use this report to help them assess the quality of their audit/auditor and when appropriate as part of the process of appointing a new auditor.

- Investors to use this report in making assessments about the quality of audit, transparency and accountability in the relevant markets.

Throughout this report, the following symbols are used:

- Represents a key finding where the firm must take action to improve audit quality.

- Represents examples of good practice we identified in our supervision, and we encourage other firms to consider applying these if appropriate to their circumstances.

- Represents an observation relating to the firm’s initiatives to improve audit quality.

Our Supervisory Approach

The audit supervisory teams in the FRC’s Supervision Division work closely together to develop an overall view of the key issues for each firm to improve audit quality. We also collaborate to develop our future supervision work.

Further details on our approach to Audit Supervision can be found here. We also publish a separate inspection report on the quality of major local audits, the latest version of which can be found here and was published in December 2023.

The FRC does not accept any liability to any party for any loss, damage or costs howsoever arising, whether directly or indirectly, whether in contract, tort or otherwise from any action or decision taken (or not taken) as a result of any person relying on or otherwise using this document or arising from any omission from it.

The Financial Reporting Council Limited 2024 The Financial Reporting Council Limited is a company limited by guarantee. Registered in England number 2486368. Registered Office: 8th Floor, 125 London Wall, London EC2Y 5AS

1. Overview – overall assessment

BDO must significantly improve its audit quality. The firm has committed to improve and has invested significantly. However, this has not yet resulted in a sustained improvement in audit quality. The firm must continue to consolidate the changes it has made to strengthen its central infrastructure. At the same time, the firm must focus on the composition and mindset of its audit teams and ensure they are supported by effective training and tools. Improving audit quality takes time. However, we may take stronger action, which could include using our PIE Auditor Registration powers, if we do not see improvements in 2025. We will continue to work with BDO to help it succeed, given its strategic importance to the market.

Audit quality inspections

The percentage of audits inspected by the FRC requiring no more than limited improvements was 38%. Two of the 13 audits we inspected (15%) were found to require significant improvements. These results are worse than the prior year and continue to be unacceptable. Over a number of years, we have highlighted recurring findings related to the challenge and testing of estimates and assumptions, the audit of revenue, and quality control procedures. This year we also identified key findings in other areas including the audit of inventory, and impairment of goodwill and intangibles. The firm must urgently re-assess its recurring findings to understand why its previous quality actions have not had the impact on audit quality expected. It should also rigorously assess all other areas where key findings have been identified this year. The results of the firm’s own internal quality monitoring are set out at Appendix A.

Firm's system of quality management (SoQM)

During the inspection period, BDO reported that it was not able to fully implement an effective SoQM as required by ISQM (UK) 1. The firm therefore devised a remediation plan to redesign its system and has discussed with us the progress of this project. Our review has been focused on the firm’s annual evaluation and the appropriateness of the actions taken in response to this.

| Regulatory audit inspection results at BDO |

|---|

| % of audits inspected by the FRC requiring no more than limited improvements (Section 2) |

| 2023/24 |

| 2022/23 |

| 2021/22 |

| 2020/21 |

| 2019/20 |

| 2 audits inspected by the FRC in 2023/24 required significant improvements |

| % of audits inspected by the ICAEW classified as good / generally acceptable |

| 2023 |

| 2022 |

| 2021 |

| 2020 |

| 2019 |

| FRC's firm-wide areas of focus (Section 3) | |

|---|---|

| Area | Good practice |

| International Standard on Quality Management (UK) 1 (ISQM (UK) 1)2 | |

| Compliance with the FRC's Revised Ethical Standard 2019 | |

| ISQC (UK) 1: Training and methodology |

1. Overview – Firm and FRC actions

BDO's response

The firm is deeply disappointed that our AQR results, having improved last year, have deteriorated, and that they contain recurring findings. We recognise that we must make significant progress, particularly in the areas of recurring findings.

We recognised it would take time for our transformation programme to positively impact our results, but we expected that, by now, based on our substantial investments in people, methodologies and training, and the reshaping of our book of business, they would have improved. As indicated by the results, we have not realised the anticipated returns from these investments quickly enough. However, the investments made have allowed us to respond faster and more effectively as issues have arisen, for example implementing the engagement level remediation programme for in-flight PIE audits.

Equally, as part of procedures developed during this period of investment, as we became aware of these results, particularly the recurring findings, we identified a programme of additional interventions required to drive clear improvement in each area. These programmes contain granular actions led and/or scrutinised by senior management. In addition, our Senior Partner, independent of management, has initiated a ‘Standback Review’ of all aspects of audit quality, to be finalised in the autumn. Because audit quality is underpinned by the system of quality management (SoQM), the limitations in the design of our SoQM have limited the effectiveness of the actions we have taken to date. We remain committed to remediating the firm’s SoQM under ISQM (UK) 1. The success of the actions being taken to remediate the SoQM is critical to achieving consistent high-quality audits and the inspection results we expect.

BDO's actions

We have identified a programme of interventions to drive improvement in each of the following areas of recurring findings (Appendix B). These interventions are: extending the remit of the revenue Centre of Excellence to execution, prioritising the Professional Judgement Framework (PJF) for milestones and key judgement stages for all audits; embedding the PJF into impairment methodology through a standardised impairment workbook, and mandating an EQR Documentation Tool. A “Standback Review” is underway to identify the key factors that are holding back our AQR results. We are continuing the remediation programme for in-flight PIE and some high-risk audits.

FRC's actions

In response to this year’s findings, we will take the following action:

- Increase by one the number of audits to be inspected to 14.

- Undertake a number of targeted follow up reviews.

- Maintain a level of intensive supervision in relation to the firm’s audit quality transformation, quality monitoring and implementation of an effective System of Quality Management.

- Hold the firm to account for setting appropriate actions and monitor their effectiveness through the Single Quality Plan (SQP) process.

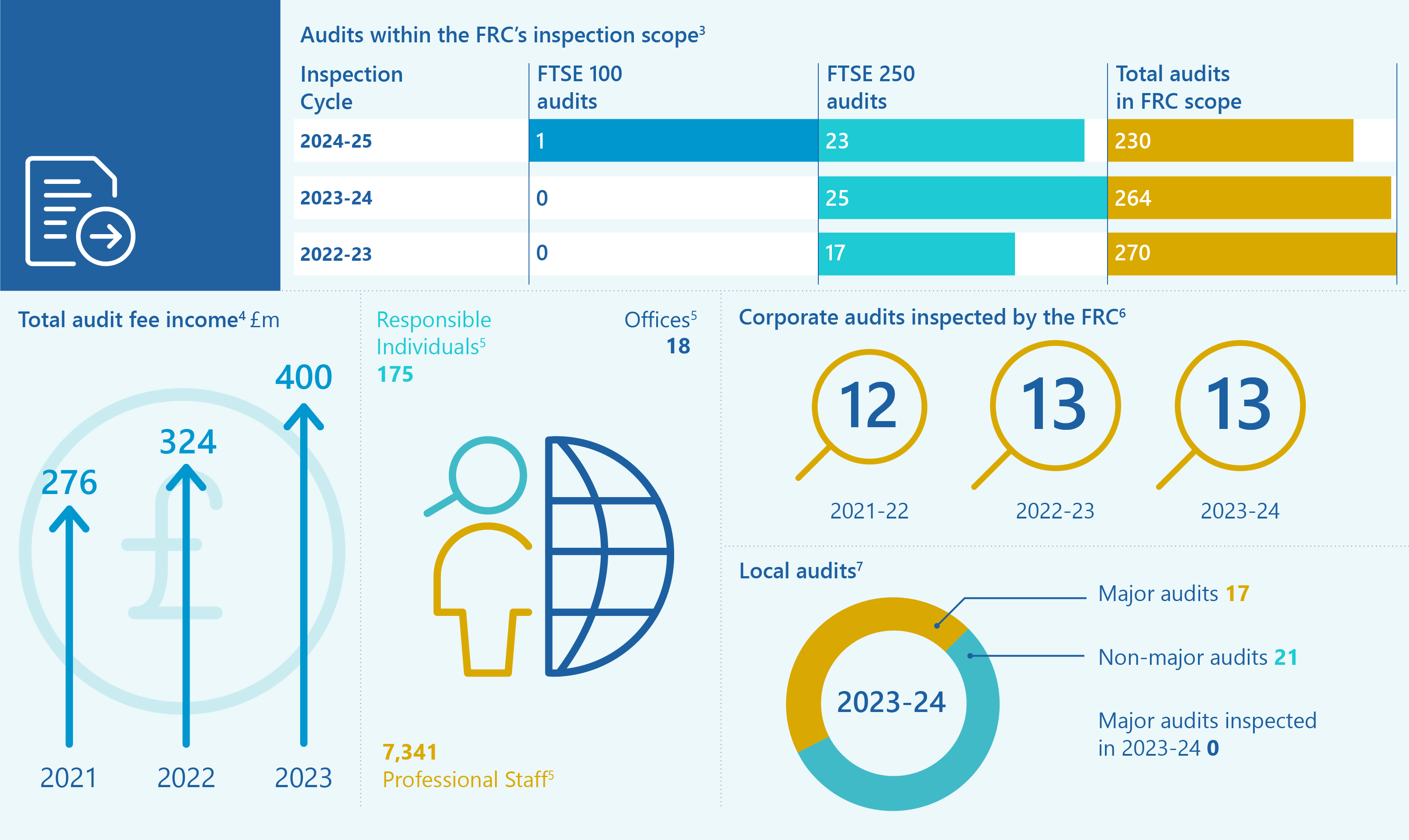

[^3] Source - the FRC's analysis of the firm's PIE audits and other audits included within AQR scope as at 31 December 2023. [^4] Source - the FRC's 2022, 2023 and 2024 editions of Key Facts and Trends in the Accountancy Profession. Audit fee income relates to all audits performed by the firm, and not only those within the FRC's inspection scope [^5] Source - the firm's Annual Return to the ICAEW, dated 8 November 2023. [^6] Excludes the inspection of local audits. [^7] Source - The FRC's inspections of Major Local Audits are published in a separate annual report.

2. Review of individual audits

Our assessment of the quality of BDO audits reviewed

We reviewed 13 individual audits this year and assessed five (38%) as requiring no more than limited improvements. The overall results were significantly worse than the prior year and reversed the more encouraging trend since the 2020/21 cycle.

Bar chart showing percentage of audits requiring good or limited improvements, improvements, or significant improvements by inspection cycle.

The chart displays results for 2019/20, 2020/21, 2021/22, 2022/23, and 2023/24. * Good or limited improvements required: * 2019/20: 5 (50%) * 2020/21: 4 (40%) * 2021/22: 7 (70%) * 2022/23: 9 (90%) * 2023/24: 5 (38%) * Improvements required: * 2019/20: 4 (40%) * 2020/21: 4 (40%) * 2021/22: 1 (10%) * 2022/23: 2 (20%) * 2023/24: 6 (46%) * Significant improvements required: * 2019/20: 1 (10%) * 2020/21: 2 (20%) * 2021/22: 2 (20%) * 2022/23: 2 (20%) * 2023/24: 2 (15%)

The audits inspected in the 2023/24 cycle included above had year-ends ranging from July 2022 to March 2023. Changes to the proportion of audits falling within each category reflect a wide range of factors, including the size, complexity and risk of the audits selected for inspection and the individual inspection scope. Our inspections are also informed by the priority sectors and areas of focus as announced annually. For these reasons, and given the sample sizes involved, changes from one year to the next cannot, on their own, be relied upon to provide a complete picture of a firm’s performance and are not necessarily indicative of any overall change in audit quality at the firm.

Given our risk-based approach, it is important that care is taken when extrapolating our findings or assessment of quality to the whole population of audits performed by the firm.

Any inspection cycle with audits requiring more than limited improvements indicates the need for a firm to take action to achieve the necessary improvements.

| Key findings | Why it is important |

|---|---|

| Urgently assess the actions required to improve the audit team’s challenge and testing of estimates and assumptions in key areas of judgement. | Auditors should adequately assess and challenge the reasonableness of management’s estimates and assumptions to respond to the risk of management bias. |

| Urgently improve the firm’s audit quality control procedures. | Rigorous audit quality control procedures enable auditors to conclude that they have performed an appropriate level of audit work to support their conclusions and their audit report. |

| Improve the audit of impairment of goodwill and non-current assets. | Auditors should adequately assess and challenge management’s evaluation of impairment as this often involves significant judgement and can be subject to management bias or error. |

| Reassess the audit quality plan to reduce the occurrence of issues over the audit of revenue. | Auditors should obtain sufficient and appropriate audit evidence to assess whether revenue is accurately recognised as it is a key driver of the entity’s results. |

| Improve the audit of inventory. | Auditors should perform appropriate procedures to assess the existence and valuation of inventory as it can be significant to an entity’s balance sheet. |

| Improve the evidence supporting the audit of groups, including the oversight of component audit work. | The group audit team is responsible for the oversight of the group audit, including audit work at a component level, and should therefore demonstrate sufficient involvement throughout the audit. |

Further details of the above key findings are set out on the following pages, including the number of audits where we raised findings in these areas.

Urgently assess the actions required to improve the audit team’s challenge and testing of estimates and assumptions in key areas of judgement

For the fifth year in succession, we have findings in this area and the firm has to seek timely measures to address these quality failings. Our inspections have identified findings on eight audits, of which two were assessed as requiring significant improvements and three as requiring improvements.

- Reliance on management experts: On three audits, we identified limited or insufficient challenge of the methodology, assumptions or judgements used by management’s experts. In addition, there was a lack of assessment by the audit team of the objectivity, competency and capability of management’s experts, leading to issues over the ability to rely on the work of the experts for audit evidence. On one of these audits, insufficient procedures were performed to assess the accuracy of source data used by the expert.

- Use of auditor’s expert: Three audit teams did not adequately scope, review or evaluate the work performed by auditor experts in areas of judgement or estimation. On another two audits there was a lack of evidence of the audit team’s review and resolution of matters raised by the expert.

- Provisions: The audit team did not perform adequate procedures to conclude on an expected credit loss provision. The deficiencies were in areas including the evaluation of the modelling and the assessment of management’s multiple economic scenarios. On another audit, there were insufficient procedures performed to challenge management’s judgement surrounding the lack of recognition of a provision.

- Valuation of investments: The audit team did not obtain sufficient, appropriate audit evidence to conclude that the valuation of level 3 financial investments was free from material misstatement. Specifically, there was a lack of challenge over the key assumptions used in their valuation.

- Capitalised development costs: Insufficient audit procedures were performed to corroborate and then challenge key judgements made by management in capitalising software development costs.

Urgently improve the firm’s audit quality control procedures

We have identified issues with the firm’s quality control procedures, a recurring finding for the fourth year in succession. This year, we had findings on seven audits, including two assessed as significant improvements required and one requiring improvements.

- Review by Audit Partner and Engagement Quality Control Reviewer (EQCR): The review processes performed by the audit partner and EQCR on three audits did not provide sufficient challenge and rigour over key areas of the audit including significant risks. On another audit there was insufficient evidence of how the challenges raised by the EQCR had been appropriately addressed and concluded upon.

- Consultations: On one audit, where a material impairment had been identified in the year, the audit team did not consider the potential need to consult internally to conclude on the accuracy and timing of the adjustment processes.

- Overall quality control procedures: On one audit, we identified errors within audit working papers covering key areas of the audit. Across two other audits, the teams did not identify errors in the audited financial statements including errors in key disclosures and the Independent Auditor’s Report.

Improve the audit of impairment of goodwill and non-current assets

We reviewed the audit of impairment on eight audits, and raised findings on five of them, including one assessed as requiring significant improvements and two requiring improvements.

- Impairment forecast assumptions: On four audits, there was inadequate challenge and evaluation by the audit team of the cash flow forecasts used in value in use models especially revenue and margin growth rate assumptions.

- Allocation of assets to CGUs: When assessing potential impairments, some audit teams did not adequately evidence their assessment of the allocation of corporate assets to individual cash generating units.

- Assessment of accounting treatment: On one audit, the audit team performed inadequate procedures and obtained insufficient evidence to conclude that the period in which an impairment was recognised was appropriate.

- Impairment indicator assessment: On the above audit, the audit procedures performed to identify and consider impairment indicators was not commensurate with the risk assessment.

Reassess the audit quality plan to reduce the occurrence of issues over the audit of revenue

Last year we stated that the firm should urgently address the continuing deficiencies in the quality of the audit work over revenue, having reported on issues for five consecutive years. Although we have seen improvements in the number of findings assessed as requiring more than limited improvement, we continue to identify a large proportion of findings relating to the audit of revenue.

We reviewed the audit of revenue on 11 audits this year, and identified findings on eight of them, one of those audits being assessed as significant improvements required.

- Accounting treatment: The audit team did not adequately assess and challenge the accounting treatment for revenue recognition, such that the risk of an undetected material misstatement remained unacceptably high.

- Audit evidence: On three audits, revenue transactions were not vouched to third-party or other appropriate supporting evidence. On another audit, there was insufficient evidence to support the testing of certain manual journals to revenue.

- Integrity of data: Three audit teams obtained insufficient evidence or samples sizes were inadequate to support the integrity or completeness and accuracy of data used in the audit.

- Other findings: On one audit, the audit team did not adequately assess the fraud risk factors in revenue recognition to support the risk assessment conclusions. On another audit, the audit team did not sufficiently evidence its challenge of costs to complete which were used to recognise revenue.

Improve the audit of inventory

We reviewed the audit of inventory on four audits and identified findings on all, including three audits assessed as requiring improvements.

- Evaluation of differences: There was insufficient corroboration and evaluation of differences identified in audit procedures over inventory, specifically in relation to inventory existence and inventory valuation.

- Inventory valuation: On one audit, there was no evidence to support the audit team’s testing of aspects of inventory cost such as freight and duty.

- Inventory provisioning: Insufficient procedures were performed by three audit teams to evaluate aspects of inventory provisioning. Weaknesses were identified in the audit procedures performed over integrity of data and the challenge of loss rates applied in calculating the provisions. On another audit, insufficient procedures were performed to assess and challenge the assessment of the net realisable value for property held as inventory.

- Inventory existence: The audit team did not evaluate the operating effectiveness of sufficient inventory count controls to support the existence of inventory.

- Response to risk assessment: The audit team did not perform sufficient procedures to address a fraud risk identified over the manipulation of inventory system data.

Improve the evidence supporting the audit of groups, including the oversight of component audit work

Four of the audits we reviewed involved significant overseas components, where we inspected the group audit team’s oversight, evaluation and challenge of the work of the component auditors. We identified findings over the group audit procedures on all four audits.

- Evaluation of component auditor substantive testing: There was insufficient evidence of how the group audit teams had evaluated aspects of the component audit team’s work, particularly for areas of significant risk on three audits. We also saw an example where the group audit team did not assess the differences between the auditing standards applied by the component audit team and the International Standards on Auditing (UK) which were applied in the group audit.

- Consolidation procedures: On two audits, the audit teams did not adequately evidence how they had tested the accuracy of the translation of component financial information into the group’s presentation currency and the foreign currency translation reserve. On another audit, there was no evidence of the audit team’s agreement of the audited financial reporting package for a significant component to the consolidation.

We also identified good practice in the audits we reviewed, including:

Risk assessment and planning

- Fraud risk assessment: We identified examples of a robust fraud risk assessment at the audit planning stage. One audit team engaged forensic specialists which provided deeper insight on fraud risk factors and an enhanced audit response as a result. On another audit, fraud risk discussions were granular in assessing the potential risk of material misstatement and demonstrated a high level of professional scepticism.

Execution

- Challenge of management: On one audit, there was clear evidence of the audit team’s thorough challenge of management in an area of high estimation uncertainty. The evidence on the audit file demonstrated good professional scepticism and resulted in changes to management’s models.

- Use of experts: We observed an example of a thorough assessment of the work performed by an auditor expert. The audit team prepared its own analysis to ensure key movements in a financial statement balance were sufficiently addressed by the auditor expert’s work.

- Group oversight: In one audit, the team evidenced an extensive review of the work performed by certain component auditors, covering all account balances above performance materiality. In addition, there was good evidence of a stand-back analysis of inventory balances by overseas components to ensure unusual movements were appropriately supported by component audit procedures.

3. Review of the firm’s system of quality management

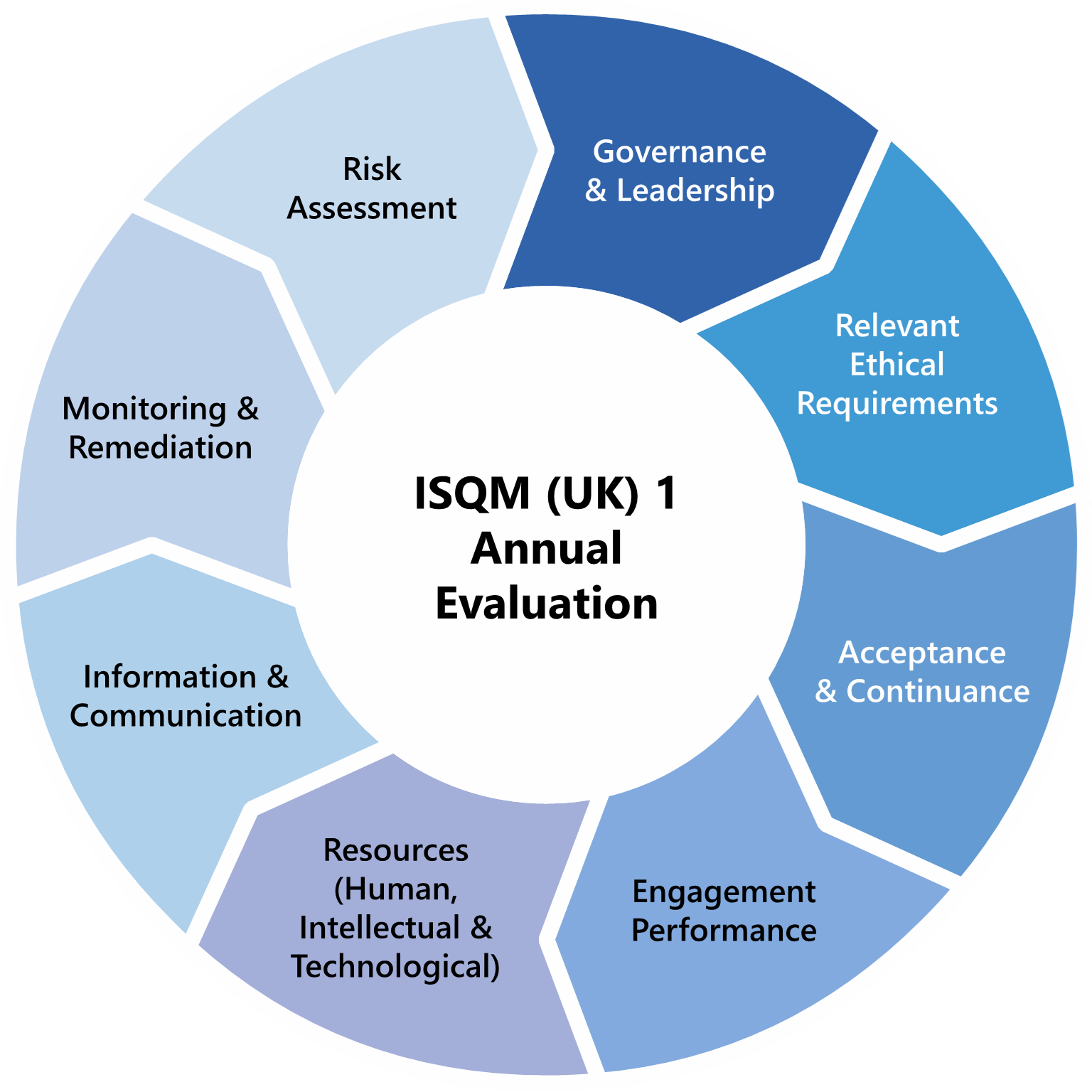

In this section, we set out the key findings and good practice identified in our review of the firm’s system of quality management (SoQM). ISQM (UK) 1 replaced the quality control standard (ISQC (UK) 1), which firms had been applying for many years, and introduced a fundamental change for firms’ quality management approaches. BDO continues to invest considerable effort in implementing and operating the ISQM (UK) 1 requirements and has responded positively to our feedback throughout.

2023/24 was a transitional inspection cycle covering both standards (details of our new ISQM (UK) 1 & 2 rotational testing can be found here). A glossary of some key ISQM (UK) 1 terms can be found in Appendix C.

ISQM (UK) 1 - Risk Assessment, Governance and Leadership, Acceptance and Continuance, Monitoring and Remediation and Annual Evaluation

We reviewed the firm’s implementation of ISQM (UK) 1. During the course of our review, the firm concluded that it needed to redesign its SoQM, so we did not finalise this review. We reviewed the process and evidence for the firm’s annual evaluation of its SoQM. This included how other sources of information on audit quality were considered, and the firm’s process for responding to the outcome of its evaluation.

We did not independently perform, or reperform, the firm’s overall annual evaluation. As ISQM (UK) 1 is focused on how firms achieve iterative improvement, we considered how the firm is redesigning its SoQM, including in response to the findings we shared during the inspection period. Our inspection findings in this area are reflective of our assertive and forward-looking approach as we seek to support firms in their development of effective, proportionate SoQMs.

Key findings

- Implementation of ISQM (UK) 1: The firm did not identify all its quality risks and mitigating responses, perform robust design and implementation assessments of responses, implement and undertake sufficient monitoring processes, or implement all elements of ISQM (UK) 1. The firm independently identified this, reported to the FRC, and concluded therefore that it did not have reasonable assurance over its system of quality management. The firm applied to the FRC and was granted a waiver under PIE Auditor Registration Regulations, to allow the firm time to carry out certain remediation activities to design, implement and test sufficiently controls-based quality management processes. As part of this waiver, the firm has been reporting to the FRC on the progress of this project and additional mitigating measures implemented to support the performance of ongoing audits.

- Accountability of those with ultimate responsibility: Those with ultimate responsibility were not sufficiently held accountable for their oversight and ownership of the SoQM. In particular, none of the individuals’ year-end appraisals or remuneration were appropriately impacted by the ineffective SoQM.

- Communication with external parties: The firm did not take steps, on a timely basis, to ensure that those charged with governance, at all of its audited entities, received sufficient information on the annual evaluation. This communication was of particular importance given the limited information provided in the firm’s Transparency Report published in October 2023.

Relevant ethical requirements - Compliance with the FRC's Revised Ethical Standard 2019

In the current year, we evaluated the firm’s compliance with the Ethical Standard. We focused our work on non-audit services. Our targeted sample testing included: checking for the provision of prohibited services; reviewing independence threats and safeguards assessments; and evaluating the completeness of independence reporting made by component auditors to the group auditors.

No key findings were identified at the firm.

ISQC (UK) 1: Training and methodology

Given the transition to ISQM (UK) 1 we performed our final supervision of training and methodology under ISQC (UK) 1. We reviewed the firm’s processes for identifying methodology updates and training needs. We also considered how the methodology updates and training were then designed, approved, and communicated to the audit practice. We paid specific attention to revisions following changes to ISA (UK) 240 and ISA (UK) 315. We also reviewed the firm’s training processes, including monitoring attendance and evaluation of learning objectives.

No key findings were identified at the firm.

Our SoQM inspection work is undertaken on a risk-focused, cyclical basis. This is supported by targeted thematic work on particular aspects of firms’ SoQMs. In this current year, we conducted four audit thematic reviews on the Tier 1 firms to complement our monitoring of ISQM (UK) 1. The areas covered in these thematic reviews were: Sampling; Hot Reviews; Network Resources and Service Providers; and Root Cause Analysis. Published reviews can be found here.

4. Forward-looking supervision

We take a risk-based, assertive and proportionate approach to the supervision of firms, which is complementary to our programme of inspections. We balance holding firms to account to take prompt action to address quality findings, with acting as an improvement regulator and sharing good practice to facilitate improvements across the sector. A Supervisor dedicated to each firm draws together evidence and indicators of risks, identifying and prioritising what firms must do to improve audit quality and enhance resilience, alongside identifying what could go wrong in the future.

Our observations from the work we have conducted this year, and updates on what more the firm must do in respect of previous observations are set out below. Where we raise key findings, we require the firm to include actions in their Single Quality Plan (SQP).

Single Quality Plan and other quality initiatives

We require all Tier 1 firms to maintain an SQP to drive measurable improvements in audit quality and resilience, and to demonstrate the effectiveness of actions taken. The SQP ensures action in the most critical areas is prioritised and enables firms to be held to account by us and their non-executives.

Observations

The integration of the firm’s Audit Quality Strategy and SQP has been good and included a clear set of strategic priorities which are fundamental to the firm’s audit quality transformation. The firm must ensure that both the new actions it sets, and its existing actions, are appropriate and targeted to the firm’s stage in its audit quality evolution. The firm should leverage the analytic ability of its SQP tool to ensure that it is alert to focus areas including resourcing, technology, and training needs that are embedded within the strategic priorities.

The firm has developed an Audit Quality Improvement Plan specific to Financial Services which includes enhanced risk assessment, better embedding of industry specific risks, detailed consideration of the role of technology in Financial Services audits and how specialists and the audit teams should support each other.

The firm has leveraged its Portfolio Review process to minimise the risks to audit quality through re-shaping its portfolio, re-allocating audit responsibilities, and targeted interventions to support audit quality. Going forward, the firm plans a more granular approach, which should improve their insights.

The firm implemented psychological safety workshops in order to reinforce its importance in promoting continuous improvement and audit quality.

It is imperative that the firm implements effectively the underlying actions across the strategic priorities in the SQP to address the issues that are set out in section 2. The firm must also consider whether the issues identified in section 2 trigger any changes in its priorities.

Emerging risks and trends

Our forward-looking supervision aims to aid firms in mitigating risks from emerging trends before quality issues occur.

Observations

- Offshore Delivery Centres: The firm continues to expand the use of resource from Offshore Delivery Centres. The firm must continue to re-evaluate the risks to audit quality, including those arising from differences in experience and culture particularly as its offshore presence grows.

- ISQM (UK) 1: The firm must use the findings from its ISQM (UK) 1 monitoring and its causal analysis to drive continuous improvement in its SoQM.

Root cause analysis

Root cause analysis (RCA) is an important part of an effective continuous improvement cycle designed to identify the causes of quality issues so that actions can be taken to address the risk of recurrence. Further, ISQM (UK) 1 has made RCA a requirement for all firms when deficiencies are identified in the system of quality management.

Observations

The firm’s RCA process has continued to develop:

- Behavioural analysis: The firm has worked with a behavioural expert and has integrated behavioural analysis into its RCA process at individual review level and in aggregate. Tailored questions support the analysis on individual reviews while aggregated data points on behavioural factors have supported interventions.

- Scope of the RCA process: During this period the firm extended the scope of its RCA process to consider causal factors from prior period adjustments and thematic reviews. In addition, the firm broadened the RCA analysis coverage of internal quality monitoring including those with positive quality findings. The firm has started to consider causal factors resulting from its SoQM.

- Effectiveness of causal analysis: The firm has refined the use of its risk taxonomy and the introduction of its behavioural taxonomy to provide it with a fuller picture of the causal themes at specific engagement level and within the broader audit environment. Comparison of the categories of causal factors driving adverse and positive quality outcomes has confirmed that resources, mindset, and review are the causal factors driving many of the recurring findings including scepticism and challenge of assumptions and estimates, audit of revenue, and quality control. While the firm’s analysis at risk category level is largely consistent with previous years, the collation of data points, analysis of correlations, and granularity of analysis provides improved insights that the firm must leverage to target its actions.

It is critical that the firm now brings together the findings from all aspects of its RCA analysis (engagement level, behavioural, and assessment of its SoQM) to ensure that its actions to address recurring findings are appropriately targeted.

Continuous engagement and holding the firm to account

We hold firms to account to take prompt action to address quality findings and set an appropriate tone from the top. The firm’s incoming Managing Partner has a critical role in maintaining the tone and ensuring there is audit quality improvement.

Observations

- Financial Services methodology: The firm has significantly improved all its banking methodology and its ability to support audit teams through improved granularity, adding illustrative risks, and more clarity on audit evidence. Sector specific content has been added to the audit manual complemented by improved functionality.

- Constructive engagement: We have engaged on five constructive engagement cases through the period, four of which are ongoing. The firm has taken actions including strengthening procedures, guidance and training aimed at preventing future recurrence of findings.

- Internal Quality Monitoring: The firm has cemented the steps it took last year to strengthen the depth and challenge of its internal quality monitoring (IQM) process. The granularity of evidence underlying the current review results has supported improved causal analysis of recurring findings. It is now critical that this translates into improved audit quality outcomes.

- Audit Culture: The firm has made good progress on culture with the introduction of a High Performing Teams framework and audit specific behaviours.

The firm now has to focus on embedding this framework to facilitate a culture that consistently promotes audit quality and the highest ethical standards. To achieve this objective, the firm has developed a clear plan and has strong support from the leadership and the Board.

- Tone at the top: The firm remains clear and consistent in its communications around the importance of audit quality. It responds well to feedback from the regulator.

Senior Leaders held a series of quality and culture roadshows across all offices to engage with staff and hear their perspectives.

Emerging risks and trends

Our forward-looking supervision aims to aid firms in mitigating risks from emerging trends before quality issues occur.

Observations

- Offshore Delivery Centres: The firm continues to expand the use of resource from Offshore Delivery Centres. The firm must continue to re-evaluate the risks to audit quality, including those arising from differences in experience and culture particularly as its offshore presence grows.

- ISQM (UK) 1: The firm must use the findings from its ISQM (UK) 1 monitoring and its causal analysis to drive continuous improvement in its SoQM.

Appendix A – Firm's internal quality monitoring

This appendix sets out information prepared by the firm relating to its internal quality monitoring for individual audit engagements (Practice Review, or PR). We have not verified the accuracy or appropriateness of these results. The appendix should be read together with the firm’s Transparency Report for 2023 and its 2024 report (when published) which provide further detail of the firm’s internal quality monitoring approach, results, root cause analysis, remediation, and wider system of quality control. Due to differences in how inspections are performed and rated, the results of the firm’s internal quality monitoring are not directly comparable to those of other firms or external regulatory inspections.

Results of internal quality monitoring

The results of the 2023 PR and two previous years are set out below. The 2023 PR comprised inspections of 98 individual audits (2022: 96), of which 48 were for periods ending before June 2022 and 50 for periods ending between June 2022 and March 2023.

Bar chart showing internal quality monitoring results by year.

The chart displays results for 2021, 2022, and 2023. * Good and acceptable with limited improvements: * 2021: 72% * 2022: 67% * 2023: 56% * Improvements required: * 2021: 16% * 2022: 17% * 2023: 27% * Significant improvements required: * 2021: 12% * 2022: 16% * 2023: 17%

Themes arising from internal quality monitoring

During 2023 the focus of PRs continued to be aligned to the most significant audit quality risk areas the firm had identified in its AQP: the audit of revenue; going concern; challenge of management; and fraud considerations (particularly around journal testing).

In comparison to 2022, there was a reduction in the number of findings in the first three of these areas. The firm continued to see key themes, in relation to the areas identified above, where there were unidentified errors and omissions in financial statements, weaknesses in the documentation of the audit approach taken, risk assessment and the evidence obtained and/or the conclusions reached. Other recurring matters identified relate to the audit of tax and the audit of inventory. New themes this year have included matters related to the audit of IT general controls and the impact of deficiencies in this area on the overall audit approach.

Appendix B – BDO's responses and actions

ISQM (UK) 1 – The bedrock of audit quality

The firm recognises that its SoQM is the bedrock on which consistent high-quality audit is built.

The limitations in the design of our SoQM have impacted the realisation of the significant investments in audit quality and the effectiveness of the audit quality actions taken to date. We rigorously evaluated our SoQM and reported to the FRC that it did not meet the objectives of ISQM (UK) 1. The conclusion was partly as a result of failing to design a SoQM that could be tested and therefore determine whether our quality management systems were achieving their intended objectives and we have taken significant steps to address this position.

Led by the Leadership Team (LT), we have invested in an additional team of some 30 ISQM (UK) 1 and controls specialists to systematically review and enhance the design of our SoQM with a view to ensuring that not only are appropriate processes and controls in place but they can be tested in a manner that provides the management of the firm with sufficient evidence to be able to conclude our SoQM does meet the objectives of ISQM (UK) 1.

We will report our conclusion in our Transparency Report in October 2024.

The LT recognises that a robust SoQM will drive audit quality and therefore the ISQM (UK) 1 remediation programme is the LT’s top priority for the firm. LT scrutinises progress of the SoQM remediation programme and of the engagement level enhanced supervision programme at every LT meeting.

Accountability for our SoQM is recognised and all LT members and audit leadership have set personal objectives relating to their responsibility for ISQM (UK) 1 and they are measured against these objectives in their performance appraisals.

We revisited our risk assessment to identify the risks to meeting our quality objectives and have analysed and documented every significant process and key control which forms part of our SoQM. This has resulted in enhancements and improvements to our processes and controls which will improve how we manage audit quality.

We have identified the need for additional processes which will have a significant role in managing audit quality and including the implementation of a continuance platform requiring centralised approval of audit continuance based on risk.

A SoQM takes time to embed and mature; we have more work to do, in particular ensuring actions are sufficiently granular, and that the firm’s audit and firm leadership directly engages with their execution.

Systems improvements will provide us with better data driving more targeted actions to drive consistently high-quality audits.

Having applied for and been granted a waiver by the FRC, we have rigorously complied with its terms in order to remediate our SoQM. We regularly engage with our supervisor on our progress. As a result of this we are ambitious with regards to stabilising our SoQM and do not anticipate we will need to request an extension to the waiver.

The firm’s incoming Managing Partner is committed to the audit quality agenda, including the System of Quality Management. He will play a key leadership role in the firm’s tone and culture in this regard once he takes office.

Root Cause Analysis (RCA)

The RCA function has continued to strengthen in the period, building out further on the multi-year plan that was designed in 2022. RCA has played a crucial role in informing the redesign of certain of our processes and controls under our SoQM remediation programme, including specialists and experts, portfolio reviews and continuance processes. The key causal factors of poor audit quality identified through RCA and the related actions in response are set out in the table. All actions noted will be taken within 6 months.

RCA - Behaviours for success

Certain behaviours have been identified in RCA as key factors for success. For example:

- Working together with adequate time for ‘on the job coaching’ with regular senior team members involvement.

- Good project management, including a project plan that allocates the right people to the right task, managing specialists and experts early and setting clear expectations with the audited entity.

- Engagement teams feel comfortable, and are persistent, challenging each other, specialists and experts and the audited entity and this is role modelled.

These behaviours are being actively promoted and embedded into our audit stream through the High Performing Teams programme.

| RESOURCES | MINDSET | REVIEW |

|---|---|---|

| Team composition not being appropriately structured to respond to the risks in these audits, including consideration of the balance of competency, capability and experience across the team, and continuity from one year-end to the next or within the year. | Confirmation and oversimplification bias on these audits. | Ineffective review on these audits as a result of the reviewer being too close to the detail to stand back, lacking knowledge or experience of the areas of the audit or obtaining information over the work performed through discussion, rather than detailed review of the file. |

| ACTIONS | ACTIONS | ACTIONS |

| A ‘Team Skills’ dashboard has been developed to provide RIs with information on their teams to consider if they have the appropriate skills/competence and capacity to deliver a high-quality audit. Resourcing leads will be provided with a resourcing guidance ‘playbook’ to assist in achieving best resourcing outcomes, including maintaining team continuity. Team composition on all PIE audits are subject to central review and monitoring for appropriateness. | A Strategy day has been organised by the Audit People and Culture team in July 2024 to assess the design of appropriate actions to mitigate the causal factors identified in this area, with a focus on embedding the firm’s professional judgement framework into new interventions and ensuring cohesion between culture and methodology. | A working group was established in October 2023 to enhance quality and effectiveness of reviews. This includes the development of practice aids that set out the baseline level of review required by auditors. Summer School 2024 will include a learning session on performing effective reviews. Addressing the causal factors in relation to ‘resources’ will also provide reviewers with the skills/competence and capacity required to perform more effective reviews. |

Interventions arising from our results in the year

As we became aware of these results and in particular the recurring findings, we identified a programme of interventions to drive clear improvement in each area. Specifically, we have looked into the effectiveness of the multiple actions taken to date in four key areas of recurring findings being the audit of revenue, challenge and scepticism, audit quality control, and the audit of impairment.

The Revenue Centre of Excellence (CoE) has now been mandated with approving the execution of revenue-related audit procedures for all higher risk PIE Audit entities where revenue constitutes an enhanced significant risk, supported by additional resource. CoE review and approval will be required prior to the audit opinion being signed.

The CoE is now working far more closely with our Quality Review Support Team (QRST) to ensure knowledge, experience and best practice is shared between the teams under the supervision of an experienced Partner as leader of this first line prevent control.

To embed the mindset of professional scepticism, the Professional Judgement Framework is now being prioritised throughout the milestones and key judgement stages for all audits. This action aims to embed a ‘stop and think’ approach to applying the Professional Judgement Framework, making the application both deliberate and transparent. By overtly and regularly discussing challenge and scepticism as an audit team we will encourage coaching and model the behaviours of a sceptical auditor to more junior team members. By bringing the Professional Judgement Framework to the front and centre of decision making throughout the audit cycle we will embed a consistent culture of challenge in all audit teams. This supplements the mindset action planned in response to RCA. To fortify Quality Control Procedures, a mandatory EQR Documentation Tool is being instituted for all audits.

This tool, completed by the EQR, will facilitate the documentation of evidence pertaining to the minimum areas of EQR review and involvement. In order to enhance auditors’ knowledge of both the expectations and requirements of review, a revised formal training programme is being developed. This supplements the review action planned in response to RCA.

To foster robust challenge of management regarding the audit approach to impairment the Professional Judgement Framework is being embedded into our impairment methodology, facilitated by the introduction of a standardised Impairment Workbook.

Standback Review

In April this year, in response to the known results of the 23/24 FRC cycle, including the recurring findings, a “Standback Review” led by the firm’s Senior Partner was initiated. This review is being performed by a non-audit partner who is independent of the audit stream. Its aim is to identify the key factors impacting audit quality that are holding back our AQR results. This includes the sufficiency of central resource to support the audit portfolio, audit leadership responses to quality issues and barriers to delivering high-quality audits within our audit stream. The overall results of the Standback Review will be ready in autumn 2024.

Actions Committee

In October 2023 we formalised an Actions Committee. This Committee has placed enhanced scrutiny on action setting. Its role is to ensure the actions we set, and take are the right ones, targeted, granular and fit for purpose. These actions are monitored, and the effectiveness is assessed through the Single Quality Plan (SQP). The SQP process is an area of focus for the firm that will evolve as we continue to monitor the effectiveness of actions taken.

Appendix C – ISQM (UK) 1 Glossary

The following definitions were extracted from ISQM (UK) 14.

| System of quality management (SoQM) | A system designed, implemented and operated by a firm to provide the firm with reasonable assurance that:

|

Quality objectives | The desired outcomes in relation to the components of the system of quality management to be achieved by the firm. |

| A system of quality management under ISQM (UK) 1 addresses the following eight components: | Quality risk | A risk that has a reasonable possibility of:

|

|

| - The firm’s risk assessment process; | Response | Policies or procedures designed and implemented by the firm to address one or more quality risk(s) in relation to its system of quality management:

|

|

| - Governance and leadership; | |||

| - Relevant ethical requirements; | |||

| - Acceptance and continuance of client relationships and specific engagements; | Findings | Information about the design, implementation and operation of the system of quality management that has been accumulated from the performance of monitoring activities, external inspections and other relevant sources, which indicates that one or more deficiencies may exist. | |

| - Engagement performance; | |||

| - Resources; | |||

| - Information and communication; and | |||

| - The monitoring and remediation process. | |||

| Firms are required to perform their first annual evaluation of the SoQM by 15 December 2023. |

| Deficiency | A deficiency in a firm’s system of quality management exists when:

|

| Ultimate responsibility | Individual(s) assigned ultimate responsibility and accountability for the firm’s SoQM should evaluate the SoQM, on behalf of the firm, and shall conclude, on behalf of the firm, whether or not the SoQM provides the firm with reasonable assurance that the objectives of the SoQM are being achieved, required under ISQM (UK) 1 paragraph 54. |

-

The six Tier 1 firms in 2023/24 were: BDO LLP, Deloitte LLP, Ernst & Young LLP, KPMG LLP, Mazars LLP, and PricewaterhouseCoopers LLP. With effect from 1 June 2024, Mazars LLP changed its name to Forvis Mazars LLP. We have published a separate report for each of these firms along with a cross-firm Annual Review of Audit Quality. ↩

-

The new standard is a significant change to ISQC (UK) 1, requiring firms to take a more proactive and risk-based approach to managing quality. The standard also required a step change in firms' monitoring, as well as the introduction of a self-evaluation of their SoQM. Page 10 of the Annual Review of Audit Quality sets out the key differences. ↩

-

The grading categories used by the firm are: Good and Acceptable with limited improvements – key findings which are limited in significance and number (if any); Improvements required - weaknesses in audit evidence, documentation and / or significant judgements that are unlikely to have material impact; Significant improvements required – audits that do not provide reasonable assurance that there are no undetected material misstatements, or there are significant concerns over the appropriateness of a significant judgement(s), which are likely to be material. ↩

-

https://media.frc.org.uk/documents/ISQM%20UK%201%20Issued%20July%202021%20Updated%20March%202023.pdf ↩