The content on this page has been converted from PDF to HTML format using an artificial intelligence (AI) tool as part of our ongoing efforts to improve accessibility and usability of our publications. Note:

- No human verification has been conducted of the converted content.

- While we strive for accuracy errors or omissions may exist.

- This content is provided for informational purposes only and should not be relied upon as a definitive or authoritative source.

- For the official and verified version of the publication, refer to the original PDF document.

If you identify any inaccuracies or have concerns about the content, please contact us at [email protected].

TAC Public Meeting May 2024 Paper 4: Project plan and target timeline

Executive summary

| Date | 31 May 2024 |

| Paper reference | 2024-TAC-003 |

| Project | Technical assessment of IFRS S1 and IFRS S2 |

| Topic | Project plan and target timeline |

Objective of the paper

This paper provides a proposed overview of the project plan, including a target timeline, to be used by the UK Sustainability Disclosure Technical Advisory Committee (TAC) for the technical assessment of IFRS S1 and IFRS S2 for prospective use in the UK. This paper also includes a discussion of the assumptions, constraints and risks that have been taken into account in developing the project plan.

Decisions for the TAC

The TAC is asked to approve the project plan, including the target timeline and to provide any comments on the assumptions, constraints and risks outlined in this paper.

Appendices

There are no appendices to this paper.

This paper has been prepared by the Secretariat for the UK Sustainability Disclosure Technical Advisory Committee (TAC) to discuss in a public meeting. This paper does not represent the views of the TAC or any individual TAC member.

Context

1The UK Sustainability Disclosure Technical Advisory Committee (TAC) has received a commission from the Minister of State for Enterprise, Markets and Small Business to undertake a technical assessment of the IFRS® Sustainability Disclosure Standards—specifically, IFRS S1 General Requirements for Disclosure of Sustainability-related Financial Information (IFRS S1) and IFRS S2 Climate-related Disclosures (IFRS S2)—to determine their appropriateness for use in the UK.

2The project for the technical assessment of IFRS S1 and IFRS S2 (the standards) is just one of the projects that the TAC is likely to commence. Further project plans will be provided on any future projects as they arise.

3This paper outlines the proposed project plan for the technical assessment of IFRS S1 and IFRS S2. The project plan takes into consideration the assessment approach (paper 2024-TAC-001) and technical work plan (paper 2024-TAC-002) for the technical assessment of IFRS S1 and IFRS S2.

Project overview

4The objective of this project is to provide recommendations to the Secretary of State (SoS) for Department of Business and Trade (DBT) as to whether endorsing an IFRS Sustainability Disclosure Standard, to create UK Sustainability Reporting Standards, would be conducive to the long-term public good in the UK. The TAC is required to provide recommendations to the SoS using the endorsement criteria outlined in the TAC Terms of Reference, taking into account contextual information provided by DBT.

5To advise the SoS on these matters, the TAC is required to conduct outreach to understand the views of UK stakeholders. The TAC is also required to hold public meetings when conducting its analysis of IFRS S1 and IFRS S2, subject to the exceptions specified in Section B of the Terms of Reference.

6The TAC's process for preparing endorsement recommendations will include the following steps:

7To facilitate these steps and support the TAC, the Secretariat will complete the following tasks:

- Publish a call for evidence to collect views on IFRS S1 and IFRS S2.

- Engage with stakeholders on an ongoing basis as necessary for the development of final endorsement recommendations.

- Develop a project plan and review the assessment approach.

- Conduct an initial analysis of the technical areas of IFRS S1 and IFRS S2 for the TAC to prioritise.

- Arrange monthly public meetings, including researching and preparing technical papers for the TAC to discuss.

- Consolidate views from members of the TAC for the finalisation of the endorsement recommendations.

- Engage with the TAC Chair and members on an ongoing basis and as necessary for the development of final endorsement recommendations.

8In addition, the Secretariat will engage with other jurisdictions, keep up to date with the International Sustainability Standards Board's (ISSB) agenda, work plan and meetings, engage with the ISSB, respond to ISSB consultations and requests, and act as a focal point for UK stakeholders to influence the technical development of future IFRS Sustainability Disclosure Standards. A future paper will outline the TAC's influencing and engagement strategy.

Assumptions, constraints and risks

9When developing the project plan, the Secretariat has taken into consideration the following assumptions and constraints:

9.1The capacity of the TAC, including the agenda capacity and recognition that the TAC members are volunteers. The assessment of IFRS S1 and IFRS S2 is a significant project which will require the TAC to consider a large number of complex technical areas. It is anticipated that the TAC will be able to discuss a maximum of four to five technical areas per meeting, depending on the nature of the technical area and level of discussion required. Additionally, the TAC members are volunteers, which means that there is a limited amount of work that they can be expected to complete in the time allocated.

9.2The execution of the plan relies upon the capacity of the TAC Secretariat. Currently about 2.5 full-time equivalent resources and 0.66 full-time equivalent oversight resources are allocated to this project, which is considered very small given the timelines and the significance of this project. The Secretariat will be expected to write papers for public TAC meetings in addition to conducting research and ongoing stakeholder engagement to inform the final endorsement recommendations.

9.3The timelines for assessing IFRS S1 and IFRS S2 may be impacted by the UK's general election. For example, the TAC may be unable to publish its final endorsement recommendations during the pre-election period. The general election will take place before January 2025, but it is unclear exactly when it will take place or the impact it could have on the TAC's work plan. Due to the uncertainty as to when it will take place, the general election has not been taken into account in the target timeline.

9.4During the project, the TAC and Secretariat may identify technical areas that are not in the initial work plan but require detailed discussion in a public meeting. Additionally, some technical areas might need to be discussed more than once, and therefore require more time on the agenda than initial planned. Therefore, the work plan may need to be amended which could delay the finalisation of the endorsement recommendations.

9.5DBT may also commission the TAC to provide further advice on specific matters during the course of the technical assessment, before or after the TAC has issued its recommendations. The work plan may need to be amended to take into account any additional requests.

9.6Although the TAC is not a decision-making body, the technical assessment of the standards still requires a high level of rigour to ensure the recommendations provided to the SoS are of high quality and are evidence-based. Sufficient time is required to ensure both IFRS S1 and IFRS S2 are assessed to a high standard. However, the TAC is required to consider both IFRS S1 and IFRS S2 separately and together taking into account the interactions between the two, which is a significant undertaking. This is the first time that sustainability-related disclosure standards have been assessed in this manner in the UK, which creates unknowns about whether there is enough time to fully debate all the necessary matters.

9.7Unlike the process used to endorse accounting standards, the TAC's final recommendations may go beyond a binary ‘endorse/do not endorse’ decision. In particular, the TAC may suggest amendments to the standards, including insertions and deletions. The TAC must provide the suggested wording to any amendments in the final endorsement recommendations, which will need to be agreed during the course of the work plan.

Project plan and target timeline

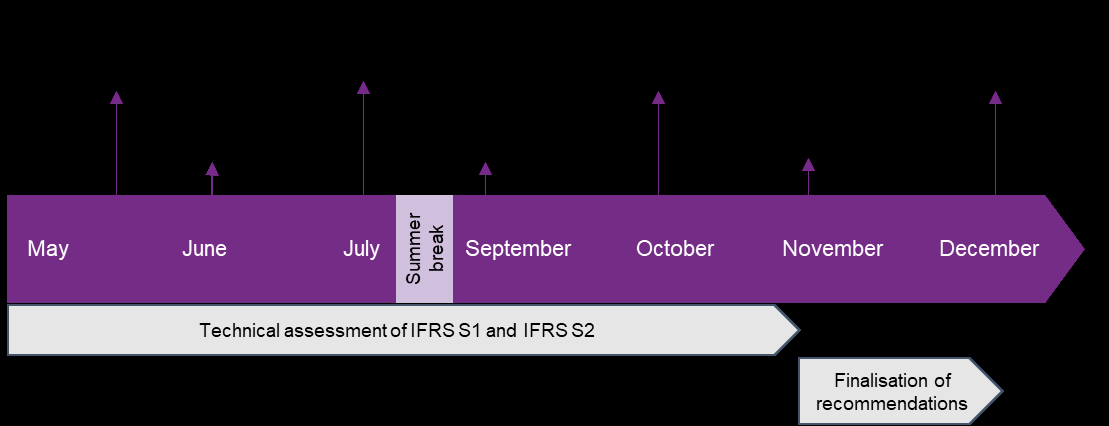

10The UK government has confirmed that it aims to make endorsement decisions on the first two standards by Q1 2025. This will require the TAC to publish its final endorsement recommendations by the end of Q4 2024.

11The target timeline below displays the Secretariat's proposed sequence of events that will lead to the finalisation of the TAC's recommendations. It is expected that all these activities are to be completed whilst going through appropriate due process with the whole committee.

12This target timeline takes into consideration known events that are likely to delay the delivery of the final endorsement recommendations. However, the timeline does not take into consideration the assumptions, constraints and risks that are uncertain. This means that the target timeline may need to be amended during the project.

13The call for evidence is not included in this timeline as it was published on 18 July 2023 and closed on 11 October 2023. This call for evidence was published before the formation of the TAC, in agreement with DBT, to expedite the timeline.

14DBT may commission the TAC to provide further advice after it has issued its recommendations. Additionally, the TAC will be given the opportunity to amend its recommendations following public consultation of the UK Sustainability Reporting Standards.

15It is important to note, the target timeline only relates to the finalisation of the TAC's endorsement recommendations. This timeline does not represent the whole endorsement process, which will be completed by DBT.

Next steps

16Once the project plan and target timeline have been approved by the TAC, the Secretariat will commence its work to enable the TAC's technical assessment of IFRS S1 and IFRS S2.

Questions for the TAC

- Does the TAC approve the project plan and target timeline?

- Does the TAC have any comments on the assumptions, constraints and risks outlined in this paper?