The content on this page has been converted from PDF to HTML format using an artificial intelligence (AI) tool as part of our ongoing efforts to improve accessibility and usability of our publications. Note:

- No human verification has been conducted of the converted content.

- While we strive for accuracy errors or omissions may exist.

- This content is provided for informational purposes only and should not be relied upon as a definitive or authoritative source.

- For the official and verified version of the publication, refer to the original PDF document.

If you identify any inaccuracies or have concerns about the content, please contact us at [email protected].

FRC Guidance the objective reasonable and informed third party test

The FRC does not accept any liability to any party for any loss, damage or costs howsoever arising, whether directly or indirectly, whether in contract, tort or otherwise from any action or decision taken (or not taken) as a result of any person relying on or otherwise using this document or arising from any omission from it.

© The Financial Reporting Council Limited 2024 The Financial Reporting Council Limited is a company limited by guarantee. Registered in England number 2486368. Registered Office: 8th Floor, 125 London Wall, London EC2Y 5AS

State of play – the objective, reasonable and informed third party test

The FRC's Ethical Standard includes requirements for audit and assurance practitioners to consider threats to independence from the perspective of an Objective Reasonable and Informed Third Party (ORITP).

Such a person is informed about the respective roles and responsibilities of an auditor (or reporting accountant as applicable), those charged with governance and management of an entity, and is not another practitioner. The perspective offered by an informed investor, shareholder or other public interest stakeholder best supports an effective evaluation required by the third-party test, with diversity of thought being an important consideration.1

The FRC observed that firms have struggled to operationalise this test, and in particular have found it difficult to find an appropriate mechanism to identify and prioritise the non-practitioner perspective. We therefore brought together a group of audit firm and investor representatives, in our Audit & Assurance Sandbox, to seek to identify areas of good practice, and ideas for measures that might enhance the test.

This document sets out measures which some firms have in place to enhance their judgements in this field, as well as some extensions of the ideas present in these measures. This may be beneficial to firms who have not yet implemented such measures, or who want to learn more about the merits of alternative strategies. It is a matter of professional judgement2 as to which, if any, of these measures should be implemented. Firms should continue to consult with the FRC or audit committees about ORITP matters as they see fit – the strategies in this document should complement, not replace, such communication.

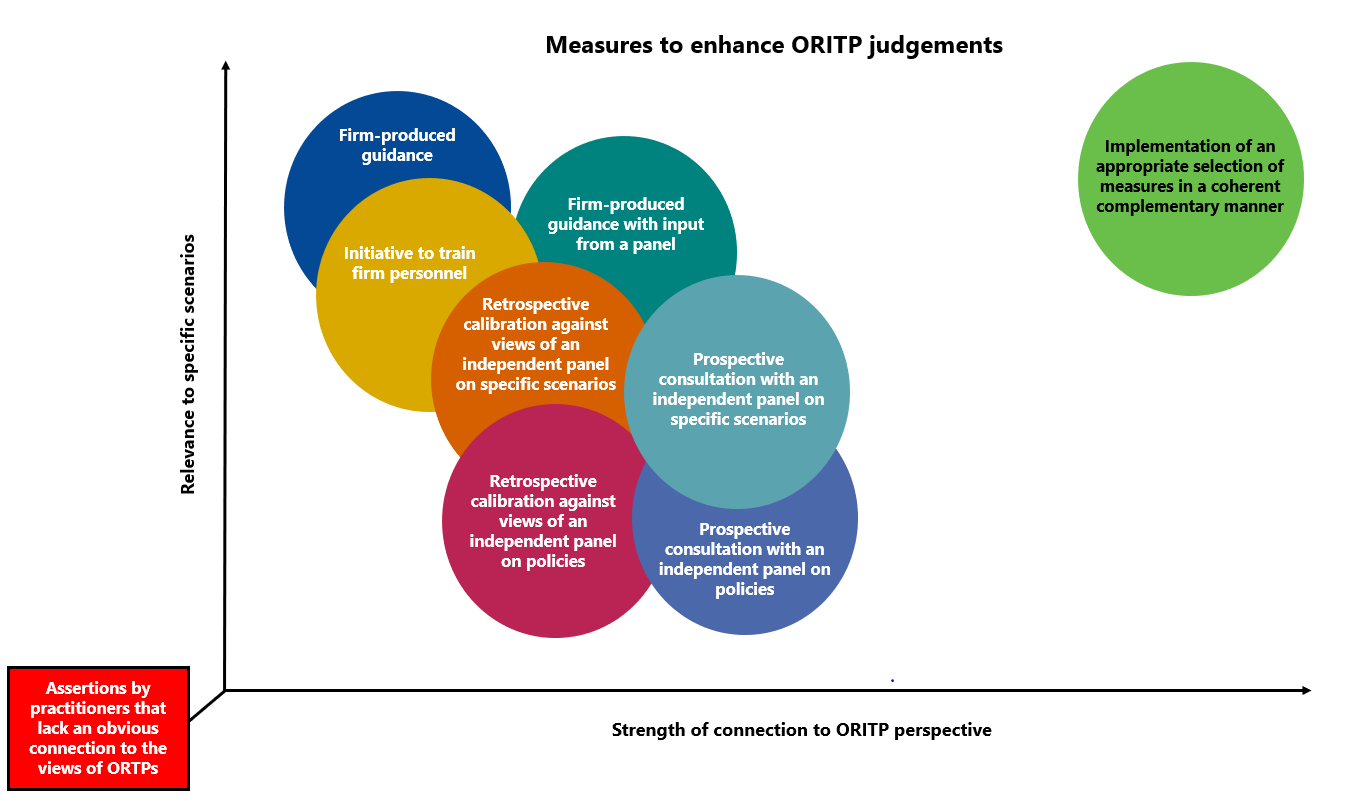

Measures to enhance ORITP judgements

This diagram shows some measures that might enhance ORITP judgements – some of these are currently implemented at firms, though none are consistently seen across the profession.

We evaluate each measure along two dimensions – the strength of connection to ORITP perspectives, and their relevance to specific scenarios that a firm may encounter. We see a stronger connection to ORITP perspectives as the main way to enhance how firms currently carry out the ORITP test. The practicalities of consulting with parties who can offer that perspective, however, often mean that such consultations commonly occur only at the firm policy level and may consequently be less relevant for granular situations.

We show the measures as regions rather than points, as firms can implement each in a variety of ways that score more or less highly against the criteria.

The "origin" represents what we see at many firms – assertions by practitioners that often lack an obvious connection to the views of ORITPs.

Firm-produced guidance

The production of a series of guidance on factors that teams might want to think about in common ORITP-relevant situations. May prompt teams to think more comprehensively about scenarios. Offers teams on the ground some insight into the perspective of an ORITP, without the operational complexity of consulting a panel.

Pros and cons

| Pros | Cons |

|---|---|

| Can be tailored to topics or situations that have caused issues in the past | May lose relevance as time passes, unless updates occur often |

| Scalable, as each piece of guidance is modular | Bias may be an issue, as no calibration against independent parties if this is the only enhancement |

| Likely to be easier to implement than a panel | Unless ORITPs consulted about the guidance, may not accurately reflect their perspectives |

Ways the measure can be strengthened along both dimensions

| Relevance to specific scenarios | Strength of connection to ORITP perspective |

|---|---|

| Guidance produced on more granular topics | Consult with those in the firm with relevant experience of the ORITP perspective, when creating the guidance |

| If a panel is in place – see below – they can offer a view on how accurately the guidance reflects ORITP perspectives |

Initiative to train firm personnel

The launch of an initiative to train certain partners and staff on how to accurately reflect the perspectives of an ORITP in their judgements. Could include strategies on how to protect against biases3 – many judgements that call for an ORITP perspective will concern commercial situations with heightened risks to objectivity.

Pros and cons

| Pros | Cons |

|---|---|

| Can be tailored to topics or situations that have caused issues in the past | May lose relevance as time passes, unless updates occur often |

| Scalable | Bias may be an issue, as no calibration against independent parties if this is the only enhancement |

| Likely to be easier to implement than a panel | Unless ORITPs consulted about the guidance, may not accurately reflect their perspectives |

Ways the measure can be strengthened along both dimensions

| Relevance to specific scenarios | Strength of connection to ORITP perspective |

|---|---|

| Train personnel on more granular topics | Obtain input from those in the firm with relevant experience of the ORITP perspective |

| Ensure kept up-to-date, as the views of ORITPs may change |

Retrospective calibration against views of an independent panel

Retrospective consultation with an independent panel as a calibration mechanism – this may be about judgements on policies or on a selection of more granular ORITP judgements or both.

The implementation of this measure could take many different forms. One option that we see currently implemented at some firms is that this panel is formed from a subset of the firm's independent non-executives – governance structures that could play this role may already be in place, such as public interest committees.

It will be important to refresh the population of the panel to ensure the perspectives of the panel remain independent.

Pros and cons

| Pros | Cons |

|---|---|

| Facilitates calibration of how personnel at the firm make ORITP judgements against the perspectives of ORITPs – for example, this may identify if ORITP judgements are consistently overly commercially aggressive | May be costly to implement |

| Confidentiality issues are less likely to be a concern than for prospective consultation | For firms that lack requisite governance structures, sourcing people who meet the relevant criteria to form the panel may be a challenge |

Ways the measure can be strengthened along both dimensions

| Relevance to specific scenarios | Strength of connection to ORITP perspective |

|---|---|

| Consulting on policies that will be relevant for a range of situations or consulting on a larger sample of more granular ORITP judgements | The population of the panel will impact on this parameter significantly, based on how well they can represent the ORITP perspective |

| Consulting the panel more often |

Prospective consultation with an independent panel

Prospective consultation with an independent panel – this may be at the policies level or on a selection of more granular ORITP judgements or both, though we recognise that prospective consultation on specific scenarios may not be possible in some cases, for example because of confidentiality conflict of interest concerns. Such consultations should not be a substitute for the exercise of professional judgement by audit teams or central technical or ethical functions. The ORITP perspective brought by a panel may support a robust judgement, but the judgement should not be outsourced to the panel.

The implementation of this measure could take many different forms. One option that we currently see implemented at some firms is that this panel is formed from a subset of the firm's independent non-executives – governance structures that could play this role may already be in place, such as public interest committees.

It will be important to refresh the population of the panel to ensure the perspectives of the panel remain independent.

Pros and cons

| Pros | Cons |

|---|---|

| Facilitates direct communication from those who may be able to represent ORITPs, which may make ORITP judgements much more robust | May be costly to implement |

| Benefits to the quality of judgements may be seen as soon as consultations start | For firms that lack requisite governance structures, sourcing people who meet the relevant criteria to form the panel may be a challenge |

| Likely to be easier to implement than a panel | In many scenarios, it may simply not be feasible to consult a panel in a timely manner |

Ways the measure can be strengthened along both dimensions

| Relevance to specific scenarios | Strength of connection to ORITP perspective |

|---|---|

| Consulting on policies that will be relevant for a range of situations or consulting on a larger sample of more granular ORITP judgements | The population of the panel will impact on this parameter significantly, based on how well they can represent the ORITP perspective |

Implementation of an appropriate selection of measures in a coherent, complementary manner

A strategic combination of measures is most likely to enhance the quality of ORITP judgements.

Financial Reporting Council 8th Floor 125 London Wall London EC2Y 5AS +44 (0)20 7492 230

Visit our website at www.frc.org.uk

Follow us on Twitter @FRCnews or Linked in