The content on this page has been converted from PDF to HTML format using an artificial intelligence (AI) tool as part of our ongoing efforts to improve accessibility and usability of our publications. Note:

- No human verification has been conducted of the converted content.

- While we strive for accuracy errors or omissions may exist.

- This content is provided for informational purposes only and should not be relied upon as a definitive or authoritative source.

- For the official and verified version of the publication, refer to the original PDF document.

If you identify any inaccuracies or have concerns about the content, please contact us at [email protected].

Citizens' Juries Final Report

- Executive summary

- Background to the research

- Methodology

- Citizens' Juries

- Reconvened workshop

- Citizens' background views on business

- Citizens' views on corporate reporting, corporate governance and audit

- Citizens' criteria for effective regulation

- Citizens' vision for corporate reporting, corporate governance and audit

- 1. Introduction

- 2. Findings

- 3. Views on corporate reporting

- 4. Views on corporate governance

- 4.5. Stewardship of companies

- 5. Views on audit and audit quality

- 5.2. Awareness and spontaneous perceptions

- 5.3. Benefits of audit

- 5.4. Limitations of audit

- 6. Citizens' criteria for effective regulation

- 6.1. Chapter overview

- 6.2. Providing the Regulator with enhanced power and ‘teeth’

- 6.3. Holding individuals as well as companies to account

- 6.4. Defining and operating clearly in the public interest

- 6.5. Keeping the principle of independence as a priority

- 6.6. Citizens' vision for corporate reporting, corporate governance and audit

- 7. Conclusion

- 8. Appendix

Executive summary

Background to the research

Financial Reporting Council (FRC) regulates auditors, accountants and actuaries, and sets the UK's Corporate Governance and Stewardship Codes.

As a public body, the FRC wanted to better understand the views of the general public who, as investors in shares, on their own account or in ISAs or pensions, or as customers or employees of businesses, have a stake in the work of the Regulator.

The FRC therefore commissioned BritainThinks to conduct research with the public to understand citizens' views on the development and strategy of the FRC, how the FRC can best operate in the public interest and identify any gaps in expectations between what the public perceives to be important and what the Regulator delivers and can deliver.

In particular, the research has focused on three key areas of regulation:

- corporate reporting

- corporate governance, and

- audit

Methodology

To ensure that members of the public were able to meaningfully participate in conversations about the work and strategy of the FRC, a deliberative research approach was used.

BritainThinks conducted three Citizens' Juries in London, Edinburgh and Coventry. Each Jury comprised 18-20 members of the public, recruited to reflect the local population and ensure that a broadly representative and diverse sample of the general public were consulted. Each Citizens' Jury lasted two days in order to ensure that there was enough time for participants to be presented with, discuss and interrogate information about corporate reporting, corporate governance and audit, before discussing their views and developing recommendations.

These Citizens' Juries were followed by a reconvened workshop in London with a selection of 24 jurors from across all three locations. This workshop lasted for half a day and provided an opportunity for participants to develop their thinking and co-create recommendations for the future with representatives from the FRC.

Figure 1: Diagram providing an overview of the research methodology and material covered in both the Citizens' Juries and reconvened workshop.

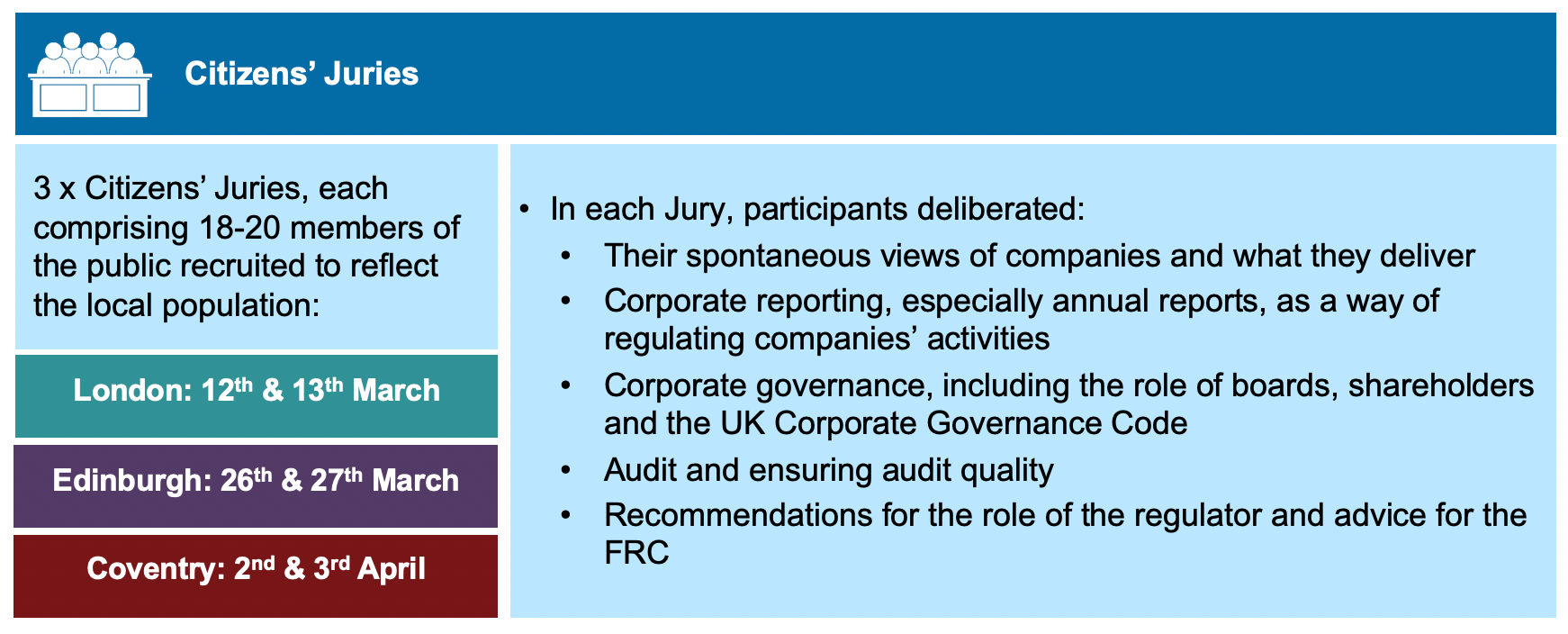

Citizens' Juries

3 x Citizens' Juries, each comprising 18-20 members of the public recruited to reflect the local population:

- London: 12th & 13th March

- Edinburgh: 26th & 27th March

- Coventry: 2nd & 3rd April

In each Jury, participants deliberated:

- Their spontaneous views of companies and what they deliver

- Corporate reporting, especially annual reports, as a way of regulating companies' activities

- Corporate governance, including the role of boards, shareholders and the UK Corporate Governance Code

- Audit and ensuring audit quality

- Recommendations for the role of the regulator and advice for the FRC

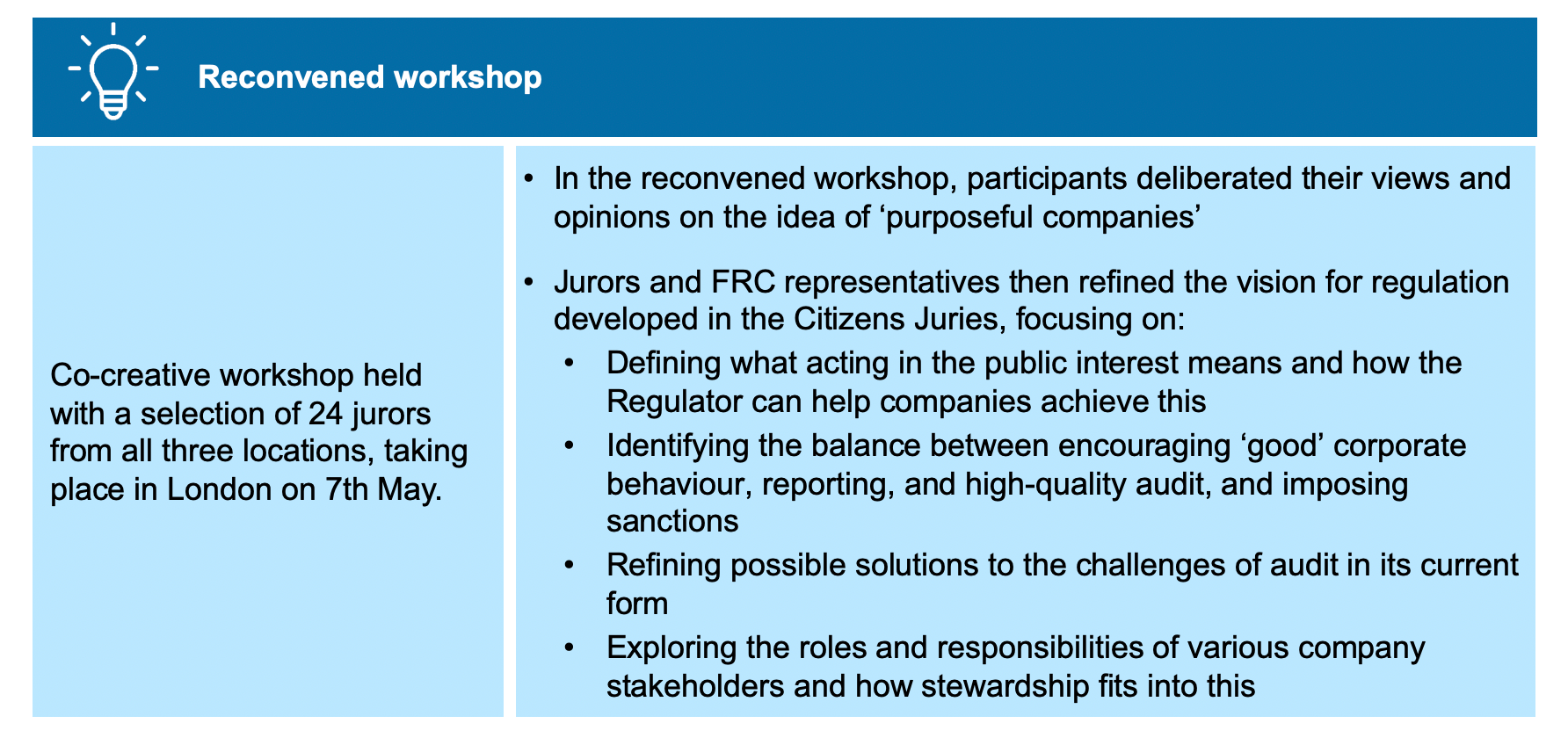

Reconvened workshop

Co-creative workshop held with a selection of 24 jurors from all three locations, taking place in London on 7th May.

- In the reconvened workshop, participants deliberated their views and opinions on the idea of ‘purposeful companies’

- Jurors and FRC representatives then refined the vision for regulation developed in the Citizens Juries, focusing on:

- Defining what acting in the public interest means and how the Regulator can help companies achieve this

- Identifying the balance between encouraging ‘good’ corporate behaviour, reporting, and high-quality audit, and imposing sanctions

- Refining possible solutions to the challenges of audit in its current form

- Exploring the roles and responsibilities of various company stakeholders and how stewardship fits into this

Citizens' background views on business

Spontaneously, citizens' overarching views of companies tended to be negative, with greed and corporate misdemeanors front of mind. However, when considering the impact companies can have on the UK, particularly on the economy and local areas, jurors had more positive perceptions. In particular, jurors highlighted the importance of companies in providing employment, products and services, and investing in the UK.

Participants were then given a presentation with a brief overview of what a company is and were introduced to the four key ways members of the public interact with companies: as customers, employees, investors, and citizens.

Following this presentation, jurors discussed each of the ways the public interacts with companies in more detail, focusing on what companies deliver for each audience and the information they would want to know about companies' activities as a result. When exploring the key relationships that members of the public have with companies, jurors felt that:

- As customers, they wanted to know about the prices and products companies offer

- As employees, they mostly considered wages, opportunities and progression as the information they would need to know about companies' activities

- Acting as investors, their concerns and priorities surrounded the return and safety of investments

- As citizens, participants wanted to know information that would enable them to hold companies to account on issues including taxes, environmental policy and investing in their local area

Given the general focus of jurors on how companies' activities have an impact on society and the environment more broadly, the FRC decided to explore one of the potential ways in which companies can reflect these broader concerns as part of their business models, “purposeful companies”, in the reconvened workshop.

The concept of purposeful companies was viewed positively, with all participants feeling it to be important that companies work to create long-term value by serving the needs of society. However, there were some concerns over the ease with which the principles of purposeful companies could be integrated into the day-to-day running of a company.

Citizens' views on corporate reporting, corporate governance and audit

During the Citizens' Juries, participants explored corporate reporting, corporate governance and audit in turn. For each, they listened to a presentation that introduced the area of regulation and an overview of the benefits and limitations of it. Following each presentation, jurors listed any outstanding questions they had and asked these of an FRC representative, to clarify any issues prompted by the presentation and aid with knowledge building for each topic.

Participants were also given information about one of three different FTSE 350 companies (a large pharmaceutical, large retail company, and a large entertainment company) to use as a case study. This included looking at the company's most recent annual report, including the auditor's report, and publicly-available information about the company's board of directors.

Corporate reporting

Spontaneous awareness of corporate reporting was low amongst participants overall. While some jurors were aware that companies do produce a public, end of year report, the majority were not aware that large companies are required to publish certain information in these annual reports by law.

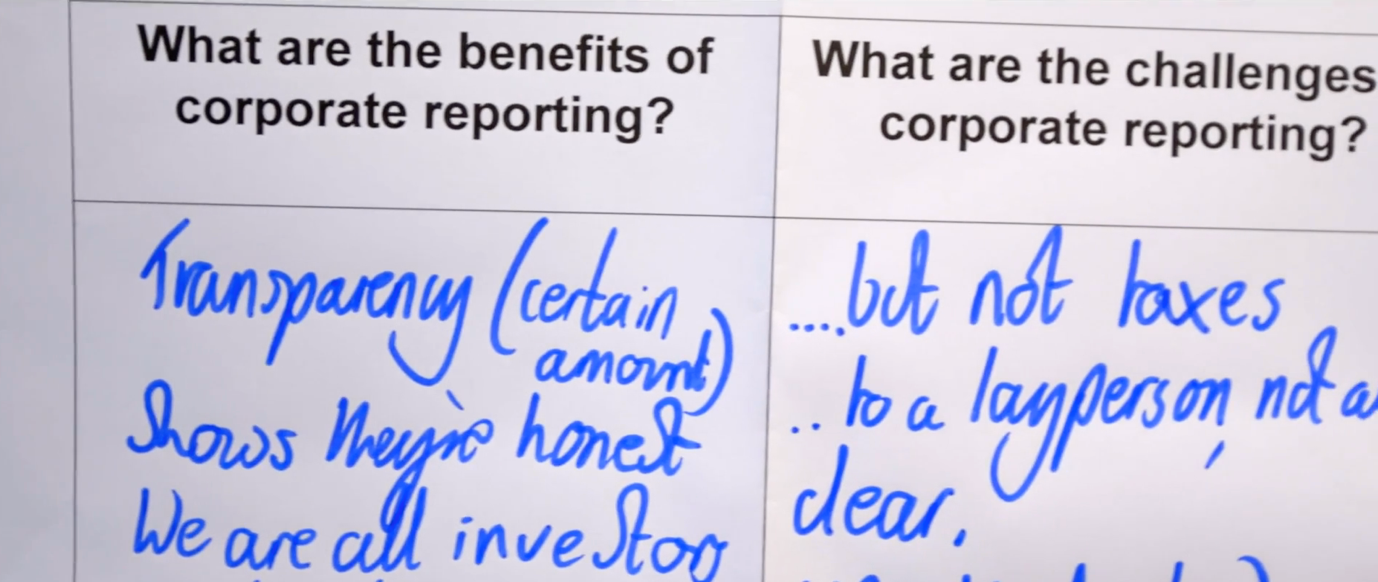

After learning more about and discussing corporate reporting in detail, jurors felt that it was a relatively effective check on business in its current form. They identified a number of benefits of corporate reporting, including:

- Promoting transparency in companies' activities, through making detailed information available in the public domain

- Making it mandatory for companies to report on important information, especially financial information in annual reports as well as, more recently, publishing gender pay gap information

- Providing a basis for comparability between different companies and industries to contextualise analysis of their performance and financial stability

However, jurors also identified a number of limitations to corporate reporting as a mechanism for regulating company activity. These included:

- Corporate reports are inaccessible for non-expert audiences, including the language used, format and length of annual reports specifically.

- Information jurors identified as important, including information about environmental sustainability and company values, was not mandatory for companies to report on.

- The information presented in annual reports was largely to be taken at face value and trusted to be accurate.

Corporate governance

Spontaneously, there was little awareness and understanding of corporate governance amongst the majority of participants. Jurors were more familiar with the existence of non-executive directors and the role of a board of directors to some extent, but most had not heard of the UK Corporate Governance Code, nor the FRC's role in setting and maintaining the standards of UK corporate governance.

Jurors were pleased to learn that a framework outlining best practice for corporate governance was in place. They identified a number of benefits of corporate governance as a mechanism for regulating company activity. These benefits included:

- The UK Corporate Governance Code promotes good practice in corporate behaviour, setting guidelines for companies to follow.

- Non-executive directors act as an independent voice on a board, allowing them to challenge company directors and bring a fresh perspective.

- Non-executive directors also bring a variety of skills and experience to a board of directors.

However, on balance, participants had concerns that the UK Corporate Governance Code did not go far enough to consistently prevent non-compliance, and voiced fears about the independence of non-executive directors being compromised. Jurors identified a number of limitations of corporate governance as a mechanism for regulating company activity. These included:

- The UK Corporate Governance Code is applied on a “comply or explain" basis rather than enshrined in law (the Regulator does not have the powers to enforce the Code) which challenges the Regulator's ability to hold companies to account.

- The Code is also felt to lack definitive metrics and measures by which to determine levels of compliance, making it harder to implement consistently.

- Jurors expressed concerns about the independence of non-executive directors, with few checks or processes in place to prevent the appointments of non-executive directors with potential conflicts of interest.

- Jurors also had doubts about the effectiveness of shareholders in holding companies and directors to account through their ability to vote at general meetings.

In the reconvened workshop, jurors developed these conversations by exploring the roles and responsibilities of different stakeholders involved in the successful running of a company. Participants also discussed the concept of stewardship to assess levels of awareness and gauge initial views:

- Company directors were felt to have the greatest responsibility for ensuring a company's success – from ensuring the profitability and stability of a company to setting a company's mission and purpose. However, jurors felt that the success of a company also depends heavily on its workforce. Customers and consumers are seen to have the potential to play an important role in holding companies to account, but jurors felt these stakeholders often don't have the necessary information to do so.

- Participants initially found the concept of stewardship confusing, but, on reflection, did understand the idea of ‘stewards' as individuals or groups who have some responsibility for the running of a company and ensuring its stability. Whilst they could see how stewardship was a key responsibility for shareholders, they felt it could have a wider application to incorporate other stakeholders including company directors, employees and members of the public. Jurors also voiced concerns about stewardship falling exclusively to shareholders.

Audit

Participants did have some spontaneous awareness of audit, although jurors' understanding of what an audit entails tended to be quite vague and related to a rough idea of “checking” companies' accounts or “audit” in its broadest sense, as the inspection or examination of something if not necessarily accounts.

There was also evidence of a gap between participants' expectations of audit and the purpose and basic process of audit. Jurors tended to voice an expectation that audit would take a broader judgement on whether companies were operating in a financially viable way, which would include forward-looking as well as historic information, with consideration of their impact on the environment and society as a whole, rather than simply verifying financial information to ensure its material accuracy and that the entity has complied with legal and regulatory requirements. In addition, participants tended to assume that audit would take a full and detailed view of a company and its accounts.

On balance, participants viewed audit as the check on companies' activities which should, in theory, be the strongest and most robust. They identified several key benefits:

- Promoting transparency and assurance of company financial activity.

- Auditors and audit firms providing an independent check on companies' accounts.

- The expertise of individual auditors and audit firms with a high bar for who can undertake audit.

- The Regulator's role in ensuring quality and standards are maintained through spot-checks – the programme of audit quality reviews.

While participants could identify benefits to the way in which audits are conducted, awareness of recent high-profile failures, including Carillion and BHS, severely limited confidence in how successful audits can truly be. Their confidence was also undermined by concerns about areas where companies did not conform with their understanding of the law, but are in fact operating legally. They identified several limitations, focused on the following three areas:

- The gap in participants' expectations for audit and what it can achieve.

- Whether independence can be guaranteed in practice, especially in the context of the 'Big Four' audit firms dominating the market.

- The Regulator is currently limited in its powers to both encourage high quality audits and sanction auditors and companies.

Citizens' criteria for effective regulation

After discussing corporate reporting, corporate governance and audit in depth, participants developed four overarching criteria they felt the Regulator needs to meet when thinking about these checks on company activities:

- The Regulator should be given enhanced power and ‘teeth' to hold companies to account. Participants wanted to see the Regulator given greater powers to hold companies to account but were somewhat divided over how best to achieve this. A number of jurors called for the introduction of legislative changes to enable this to happen, but some did acknowledge that any increase in regulation should not ‘stifle' companies' ability to operate and flourish.

Participants explored this balance – and how the Regulator can best achieve this – in more detail in the reconvened workshop. Upon further reflection and discussion, participants identified two ways in which the Regulator can reduce the risk of non-compliance with the codes and standards in corporate reporting, governance and audit, whilst encouraging growth and innovation in companies and engagement in the relevant professions:

- The Regulator needs to have more power to interact with companies 'early on'. Jurors felt that early interventions in the event of any issues arising would help the Regulator avoid imposing stricter punishments, by preventing more major issues from developing. There was support for these interventions taking the form of both announced and unannounced ‘Ofsted-style' spot checks.

- The Regulator needs to not be seen as ‘scary', but as a ‘critical friend'. Jurors saw a clear role for the Regulator in being more proactive in contacting companies to provide advice, support and encouragement.

-

The Regulator should hold individuals (and other than those who are members of a professional body, as at present) as well as companies to account to deter wrong-doing. Jurors felt strongly that individuals acting against the public interest should not be able to escape their misconduct with few personal ramifications. As a result, they felt that the Regulator should be able to 'sanction' individual board members and sanctions for audit partners should be borne by the individuals concerned rather than their firms.

-

The Regulator should define and operate clearly in the public interest. Across all three Juries, participants implicitly called for companies to act in their interest. However, they felt the concept itself is hard to define. The term 'public interest' feels vague and can mean different things to different people.

In the reconvened workshop, jurors discussed the principle of operating in the public interest in more detail. Participants felt that, to act in the public interest, companies should:

- Take into account wider audiences and types of stakeholders outside of shareholders, including employees. The views of local communities in particular should be taken into account.

- Ensuring and improving diversity on boards. Jurors felt the Regulator should encourage diversity, perhaps even setting minimum quotas for boards – but felt it was important this didn't become a ‘box-ticking' exercise.

- Improving openness and transparency to improve accessibility for the public. Re-addressing the balance between “sticks” (sanctions) and “carrots” (incentives) so that the emphasis is more on the latter was felt to work towards this, helping foster an environment based on open dialogue and transparency.

- The Regulator should keep the principle of independence as a key priority. Jurors agreed that the Regulator should ensure that independence is retained at all costs. Participants felt it was particularly important to ensure the independence of non-executive directors and audit partners.

Citizens' vision for corporate reporting, corporate governance and audit

Building on the challenges they identified with corporate reporting, corporate governance and audit, participants developed a vision for each that meets their criteria for effective regulation. Their recommendations and ideas were also deliberated in further detail during the reconvened workshop.

Corporate reporting

Jurors identified a need for companies' reports to be made more accessible to the public. To achieve this, some participants suggested implementing a rating system or ranking for annual reports to help identify which companies are producing the most straightforward, clearly written and well-structured reports. Participants also suggested that, to better enable comparability between companies, a more standardised report template, including clear guidelines over the language to use, could be implemented.

Many jurors were overwhelmed by the length of corporate reports and felt that technology could be used to better effect to help make this easier to navigate. Participants suggested having an 'interactive' online version of corporate reports to make it easier to select information of interest.

Finally, the majority of participants felt it should be made mandatory for companies to report on environmental sustainability and company values (for example, how staff are treated).

Corporate governance

On corporate governance, jurors' key stipulation was ensuring the Regulator is better able to enforce the UK Corporate Governance Code. In London and Edinburgh, jurors wanted the Code to become legislation, therefore giving the Regulator the legal powers needed to enforce it. In Coventry however, several participants felt it would be more effective for the Regulator to reward best practice rather than turning the Code into legislation, to ensure it still provides the flexibility needed for companies to remain innovative and competitive.

Ensuring diversity on boards was felt to be critical in enabling companies to act in the public interest. Participants suggested setting stricter rules on the gender and BAME balance of boards as well as reviewing recruitment processes as a way of reaching beyond the 'old boys club'. They also felt that it would be useful to ensure that there is an employee representative on boards, to make sure that people actively involved in the day-to-day running of the company are also involved in decision-making.

Finally, jurors suggested measures to ensure non-executive directors retain their independence. They felt this could be achieved by implementing enforced turnover rates of three years for non-executive directors, so they remain independent and offer real challenge.

Audit

For audit, jurors identified a need for making sure audit and ethical standards are being followed in order to prevent misconduct and drive high-quality work. Jurors felt that there should be more focus on holding individuals to account for their actions, for example fining individual audit partners. By focusing on individual accountability, participants felt that the Regulator would create an effective disincentive to poor quality audit, conflicts of interest and fraud, without having a negative impact on the audit firm itself.

Ensuring independence was also felt to be key. As part of this, jurors suggested that the maximum length of an audit contract with individual audit firms is reassessed. Jurors suggested that the current maximum of 20 years be reduced to a 5-10-year term limit, with individual auditors and audit partners required to rotate every 2 - 3 years within this. Finally, jurors also felt the audit system could do more to act in the public interest by assessing and ensuring the long-term success of a company. Jurors felt that auditors could have more of a role in assessing how economically or financially sustainable a company might be, in the medium

- as well as short-term. However, jurors did recognise that this might require legislative change and would also only provide reasonable, not absolute, assurance.

In the reconvened workshop, jurors worked with FRC representatives to refine possible solutions to the challenges of audit in its current form, as identified in the Citizens' Juries:

- Participants called for the Regulator to be given more power to apply sanctions in the event of wrong-doing, but for these sanctions to be applied as a last resort. Jurors felt that one of the ways in which the Regulator could achieve this balance was by having more open lines of communication and transparency with companies and audit firms, to help identify issues early on.

- Jurors also deliberated how the Regulator could ensure that sanctions are applied fairly to avoid scapegoating within firms and expressed a need for a clearly defined list of roles and responsibilities, to make it clear who is accountable for what.

- Jurors also suggested that the Regulator accompany or shadow auditors as they carry out audits, in order to ensure standards are being met and to provide expert support and advice. Participants did acknowledge that this would require significant resource on the part of the Regulator.

- There was also support for the idea of entirely separating the audit and consultancy services functions within the 'Big 4' firms, to ensure independence is retained.

1. Introduction

1.1. Background to the research

The Financial Reporting Council (FRC) regulates auditors, accountants and actuaries, and sets the UK's Corporate Governance and Stewardship Codes. The FRC promotes transparency and integrity in business and its work is aimed at investors and others who rely on company reports, audit and high-quality risk management.

As a public sector body, the FRC wanted to better understand the views of the general public who, as investors in shares, on their own account or in ISAs or pensions, or as customers or employees of businesses, have a stake in the work of the Regulator. The FRC recognised that it would be important to reach beyond the industry stakeholders who typically engage with their necessarily technical consultations on proposed and actual changes to regulations and guidance.

The FRC wanted to engage with citizens directly to ensure that the concerns and views of the general public are represented in the conduct of its work and development of its strategy to reflect the economic and social significance of the listed and large businesses that the FRC works with in the lives of many people in the UK.

The FRC therefore commissioned BritainThinks to conduct research with the public to understand citizens' views on the development and strategy of the FRC, how the FRC can best operate in the public interest and identify any gaps in expectations between what the public perceives to be important and what the Regulator delivers and can deliver. In particular, the research has focused on three key areas of regulation:

- corporate reporting

- corporate governance, and

-

audit

-

This research comes at a moment of transition for the FRC, following an independent review of the Regulator led by Sir John Kingman, 1 and the findings and conclusions of the research will feed into the future shape and strategy of the Regulator.

1.2. Research objectives

The research aimed to directly engage members of the public about the work of the Financial Reporting Council. It sought to gain insight into citizens' views of corporate reporting, corporate governance and audit, and their recommendations for how the Regulator can best operate in the public interest in the future.

Within this overarching aim, there were five key areas of focus:

- Gain insight into citizens' spontaneous perceptions of businesses and what they deliver for the UK

- Understand citizens' perspectives on how businesses operate and the duties of directors

- Gain insight into citizens' expectations regarding what an audit is, does, and what they think it should do

- Understand citizens' views on the benefits and challenges of the checks on companies currently delivered by the FRC: corporate reporting, corporate governance and audit

- Develop a set of recommendations with citizens outlining their future vision for the Regulator to ensure that it is operating in the public interest.

1.3. Methodology

To ensure that members of the public were able to meaningfully participate in conversations about the work and strategy of the FRC, a deliberative research approach was used. BritainThinks conducted three Citizens' Juries in London, Edinburgh and Coventry between 12th March and 3rd April

- Each Jury comprised 18-20 members of the public, recruited to reflect the local population and ensure that a broadly representative and diverse sample of the general public were consulted. Each Citizens' Jury lasted two days in order to ensure that there was enough time for participants to discuss and interrogate information about corporate reporting, corporate governance and audit, before discussing their views and developing recommendations.

These Citizens' Juries were followed by a reconvened workshop in London on 8th May 2019 with a selection of 24 jurors from across all three locations. This workshop lasted for half a day and provided an opportunity for participants to develop their thinking and co-create recommendations for the future with representatives from the FRC.

1.3.1. What is a Citizens' Jury?

A Citizens' Jury is an opportunity to understand where members of the public get to when they are given the time, space and information to consider an issue or policy debate in real depth, especially, as in this case, where public awareness of the issues and work under consideration is very low. The central objective of this type of consultation approach is to move participants from thinking only about 'me and mine' to a citizen's mindset, where they are considering the broader societal implications of complex trade-offs.

Citizens' Juries tend to take place over a reasonably long period of time (often two or more days), and involve a small group of citizens, recruited to reflect society more broadly.

Through a series of presentations, small group exercises and plenary debates, participants receive briefings on the issue from experts and have the opportunity to debate the issues in depth. They are then asked to work together to develop their own recommendations for the way forward.

1.3.2. Structure of the Citizens' Juries

Each Jury followed the same agenda, summarised in the table below.

Figure 2: Table providing an overview of the Citizens' Jury agenda