The content on this page has been converted from PDF to HTML format using an artificial intelligence (AI) tool as part of our ongoing efforts to improve accessibility and usability of our publications. Note:

- No human verification has been conducted of the converted content.

- While we strive for accuracy errors or omissions may exist.

- This content is provided for informational purposes only and should not be relied upon as a definitive or authoritative source.

- For the official and verified version of the publication, refer to the original PDF document.

If you identify any inaccuracies or have concerns about the content, please contact us at [email protected].

Key Facts and Trends in the Accountancy Profession 2013

The FRC is responsible for promoting high quality corporate governance and reporting to foster investment. We set the UK Corporate Governance and Stewardship Codes as well as UK standards for accounting, auditing and actuarial work. We represent UK interests in international standard-setting. We also monitor and take action to promote the quality of corporate reporting and auditing. We operate independent disciplinary arrangements for accountants and actuaries; and oversee the regulatory activities of the accountancy and actuarial professional bodies.

The FRC does not accept any liability to any party for any loss, damage or costs howsoever arising, whether directly or indrectly, whether in contract, tort or otherwise from any action or decision taken (or not taken) as a result of any person relying on or otherwise using this document or arising from any omission from it.

The Financial Reporting Council Limited 2013 The Financial Reporting Council Limited is a company limited by guarantee. Registered in England number

- Registered Office: 5th Floor, Aldwych House, 71-91 Aldwych, London WC2B 4HN.

The content in this publication is provided for general information purposes only. Although the Financial Reporting Council (FRC) endeavours to ensure the accuracy of the information provided by the accountancy firms and bodies listed in the publication, we undertake no detailed checking of the data and therefore cannot guarantee that the content will be current, consistently provided year on year, accurate or complete. The FRC accepts no responsibility for any reliance others may place upon the information provided herein. We shall not be liable for any loss or damage arising from the use of the information contained within this publication nor from any action or decision taken as a result of using such information.

- Foreword

- Section One – Main Highlights

- Section Two – Members of Accountancy Bodies

- Section Three – Students of Accountancy Bodies

- Students Registered in the UK and Republic of Ireland 2008 - 2012

- Students Registered Worldwide 2008 - 2012

- Location of Students 2012

- Profile of Students Worldwide of Seven Accountancy Bodies 2012

- Gender of Students Worldwide 2012

- Age of Students Worldwide of Seven Accountancy Bodies 2012

- Sectoral Employment of Students Worldwide 2012

- Graduate Entrants to Training with Seven Accountancy Bodies

- Pass Rates 2008-2012

- Section Four – Resource Information on Accountancy Bodies

- Section Five – Oversight of Audit Regulation

- Recognised Supervisory Bodies (RSBs)

- Number of Firms Registered with the Recognised Supervisory Bodies

- Application for Registration as a Statutory Audit Firm & the Number Refused 2010 – 2012

- Monitoring of Registered Audit Firms

- Gradings 2010 - 2012

- Association of Chartered Certified Accountants (ACCA)

- Institute of Chartered Accountants in England & Wales (ICAEW)

- Chartered Accountants Ireland (CAI)

- Institute of Chartered Accountants of Scotland (ICAS)

- Complaints about Auditors

- Recognised Qualifying Bodies (RQBs)

- Section Six – Audit Firms

- CONCENTRATION OF LISTED COMPANIES' AUDITS - YEAR ENDED 2012

Foreword

This is the eleventh edition of 'Key Facts and Trends in the Accountancy Profession' and the first produced by the Conduct Division of the Financial Reporting Council (FRC), following the FRC reform in 2012.

The FRC is the UK's independent regulator responsible for promoting high quality corporate governance and reporting to foster investment. It has specific responsibilities for overseeing the regulation of statutory auditors and, more widely, the regulation of the accountancy and actuarial professions in the UK by agreement with their professional bodies.

This document provides statistical information on the accountancy profession as part of the context to the FRC's work. It collates information provided by the accountancy bodies for which the FRC has oversight responsibilities, being the six Chartered Accountancy bodies1 and one other body that offers an audit qualification recognised by the FRC2. The information in Sections One to Four relates principally to membership, students, income, costs and staffing of these bodies. Section Five contains information related to the supervision of statutory auditors that in previous years was included in the report from the Professional Oversight Board to the Secretary of State.

Section Six provides information on thirty six of the largest registered audit firms which collectively audit the vast majority of UK listed companies and other public interest entities. Firms provide this information on a voluntary basis and there were a few firms that declined to do so.

Where appropriate we highlight significant trends and explain possible limitations on the data. However, we do not comment on the possible reasons for particular trends. We would also stress that it is often difficult to make comparisons between the different accountancy bodies or between audit firms. This can be for a number of reasons such as differences in the way data is classified or in the differing regulatory arrangements.

The tables on members of the accountancy bodies show data for the UK and the Republic of Ireland, and separately worldwide data. We include the UK and Republic of Ireland figures together, partly, because members and firms are entitled to practise in both jurisdictions and, partly, because in some cases it is difficult for the bodies to separate the data. However, the Irish Auditing and Accounting Supervisory Authority (IAASA) publishes certain information relating specifically to the Republic of Ireland, which is available at http://www.iaasa.ie.

Overall, the data suggests that the profession continues to attract and remains attractive. The total number of members continues to increase, both in the UK and worldwide. It is notable, however, that although student numbers have also increased worldwide, they fell in the UK in

- The total fee income of the largest firms has also grown in 2011/12, much more markedly for the 'Big Four' than for other firms.

We are grateful to those that took the time to complete our questionnaire on how we could improve this publication. We have changed a number of the tables and charts this year in response to those comments.

We would again welcome your comments on Key Facts and Trends in the Accountancy Profession and should be grateful if you would complete our short questionnaire (see link below):

https://www.surveymonkey.com/s/KeyFactsandTrends2013

Further information about the FRC is available at www.frc.org.uk.

Richard Fleck Chairman of the FRC Conduct Committee June 2013

Section One – Main Highlights

The Accountancy Bodies 2008 – 2012

- Total membership of the accountancy bodies continues to grow steadily. The seven bodies included in the report have over 319,000 members in the UK and Republic of Ireland and over 450,000 members worldwide. The compound annual growth rates for 2008-12 are 2.6% in the UK and Republic of Ireland and 3.5% worldwide. (Tables 1 and 2)

- The number of students has also continued to rise overall with 165,000 students in the UK and Republic of Ireland and just over 500,000 worldwide. There has been a decline in student numbers in the UK and Republic of Ireland, falling on average by 0.7% (2008-12). Average annual growth rates worldwide increased by 4% over the same period. Whilst student numbers increased in 2012 by 2.3% worldwide, there was a fall in UK numbers by 3.3%. (Tables 4 and 5)

- There are significant differences between the bodies in terms of geographical distribution of membership and student populations and in size, growth rate and age profile.

- The number of registered audit firms continues to decline gradually, albeit at a slower rate than previously. The overall number of registered audit firms was 7,239 as at the 31 December 2012, 10.6% below the 31 December 2008 figure. However, the rate of decline was 1.8% in 2012 as compared to 3.2% in 2008. (Table 8)

- The number of audit monitoring visits across all the bodies has remained relatively stable over the last five years ranging between 1,167 and 1,543 annual visits.

The Audit Firms 2008 – 2012

- Table 18 shows the fee income for audit and non-audit services for 36 of the largest registered audit firms for the year ended 2012. Most of these have audit clients which are UK public interest entities. Firms are listed in order of fee income from audit, rather than total fee income.

- This is the first year we have included in Table 18 information on the percentage of female principals whether partners or members.

- Over the past five years, the 'Big Four' firms (PricewaterhouseCoopers, KPMG, Deloitte and Ernst & Young) have experienced a steady increase in the proportion of fee income from non- audit work for non-audit clients. In contrast their fee income from non-audit work to audit clients has been falling. (Chart 16)

- Total fee income increased in 2011-12. The increase for the Big Four firms was 7.7% compared with an average increase of 0.6% for the larger registered firms outside the Big Four. This is the first year since 2009 that firms outside of the Big Four have seen an increase rather than a decline in total fee income. (Table 19)

- Audit fee income for Big Four firms increased by 4.9% in 2011-12 compared with a decrease of 5% for the larger registered firms outside the Big Four that are included in our analysis.

- Audit fee income per Responsible Individual in the Big Four firms has grown in 2012 by 7%. (Table 20)

- There has been little change in recent years in the proportion of listed companies audited by many of the larger registered firms outside the Big Four. (Table 22)

Section Two – Members of Accountancy Bodies

Members in the UK and the Republic of Ireland 2008 - 2012

Table 1 shows the number of members of each of seven accountancy bodies in the UK and Republic of Ireland3 as at 31 December for each of the five years to 31 December 2012.

| ACCA | CIMA | CIPFA | ICAEW | CAI | ICAS | AIA | TOTAL |

|---|---|---|---|---|---|---|---|

| 67,593 | 60,870 | 13,374 | 112,738 | 16,237 | 15,322 | 1,758 | 287,892 |

| 68,907 | 63,513 | 13,440 | 114,468 | 17,076 | 15,858 | 1,734 | 294,996 |

| 72,565 | 66,342 | 13,297 | 115,990 | 18,145 | 16,270 | 1,674 | 304,283 |

| 75,305 | 69,038 | 13,159 | 117,475 | 18,814 | 16,666 | 1,647 | 312,104 |

| 77,269 | 72,053 | 13,140 | 119,179 | 19,414 | 16,933 | 1,607 | 319,595 |

| % growth (11 - 12) | |||||||

| 2.6 | 4.4 | -0.1 | 1.5 | 3.2 | 1.6 | -2.4 | 2.4 |

| % growth (08-12) | |||||||

| 14.3 | 18.4 | -1.7 | 5.7 | 19.6 | 10.5 | -8.6 | 11.0 |

| % compound annual growth (08-12) | |||||||

| 3.4 | 4.3 | -0.4 | 1.4 | 4.6 | 2.5 | -2.2 | 2.6 |

Table 1

- The overall total number of members of these seven accountancy bodies in the UK and Republic of Ireland has continued to grow steadily at a compound annual growth rate of 2.6% for the period 2008 to 2012. Total membership rose 2.4% from 2011 to 2012 compared with 2.6% from 2010 to 2011.

- There are significant differences in growth rates of the individual bodies. CAl and CIMA show the strongest growth at a compound annual rate of 4.6% and 4.3% respectively between 2008 to 2012. Membership of the AIA and CIPFA has declined during this period.

- The ICAEW continues to be the largest of these bodies in the terms of UK and ROI membership.

Members Worldwide 2008-2012

Table 2 shows the number of members worldwide3 of each of seven accountancy bodies as at 31 December for each of the five years to 31 December 2012.

| ACCA | CIMA | CIPFA | ICAEW | CAI | ICAS | AIA 4 | TOTAL |

|---|---|---|---|---|---|---|---|

| 131,398 | 76,368 | 13,697 | 132,411 | 17,843 | 17,671 | 6,064 | 395,452 |

| 137,233 | 79,757 | 13,790 | 134,698 | 18,802 | 18,278 | 6,566 | 409,124 |

| 144,397 | 83,487 | 13,668 | 136,615 | 20,010 | 18,780 | 7,046 | 424,003 |

| 151,283 | 87,316 | 13,544 | 138,464 | 20,905 | 19,334 | 7,300 | 438,146 |

| 158,574 | 91,744 | 13,541 | 140,573 | 21,844 | 19,739 | 7,983 | 453,998 |

| % growth (11 - 12) | |||||||

| 4.8 | 5.1 | 0.0 | 1.5 | 4.5 | 2.1 | 9.4 | 3.6 |

| % growth (08-12) | |||||||

| 20.7 | 20.1 | -1.1 | 6.2 | 22.4 | 11.7 | 31.6 | 14.8 |

| % compound annual growth (08-12) | |||||||

| 4.8 | 4.7 | -0.3 | 1.5 | 5.2 | 2.8 | 7.1 | 3.5 |

Table 2

- The worldwide membership of the seven accountancy bodies continues to grow at a faster rate than the UK and ROI membership (3.5% compared to 2.6% (Table 1) compound annual growth for the period 2008 to 2012).

- ACCA continues to be the largest of these bodies in terms of worldwide membership.

Table 2 shows the number of members worldwide3 of each of seven accountancy bodies as at 31 December for each of the five years to 31 December 2012.

| ACCA | CIMA | CIPFA | ICAEW | CAI | ICAS | AIA4 | TOTAL | |

|---|---|---|---|---|---|---|---|---|

| 2008 | 131,398 | 76,368 | 13,697 | 132,411 | 17,843 | 17,671 | 6,064 | 395,452 |

| 2009 | 137,233 | 79,757 | 13,790 | 134,698 | 18,802 | 18,278 | 6,566 | 409,124 |

| 2010 | 144,397 | 83,487 | 13,668 | 136,615 | 20,010 | 18,780 | 7,046 | 424,003 |

| 2011 | 151,283 | 87,316 | 13,544 | 138,464 | 20,905 | 19,334 | 7,300 | 438,146 |

| 2012 | 158,574 | 91,744 | 13,541 | 140,573 | 21,844 | 19,739 | 7,983 | 453,998 |

| % growth (11 - 12) | 4.8 | 5.1 | 0.0 | 1.5 | 4.5 | 2.1 | 9.4 | 3.6 |

| % growth (08 - 12) | 20.7 | 20.1 | -1.1 | 6.2 | 22.4 | 11.7 | 31.6 | 14.8 |

| % compound annual growth (08-12) | 4.8 | 4.7 | -0.3 | 1.5 | 5.2 | 2.8 | 7.1 | 3.5 |

Table 2

- The worldwide membership of the seven accountancy bodies continues to grow at a faster rate than the UK and ROI membership (3.5% compared to 2.6% (Table 1) compound annual growth for the period 2008 to 2012).

- ACCA continues to be the largest of these bodies in terms of worldwide membership.

Students who became Members

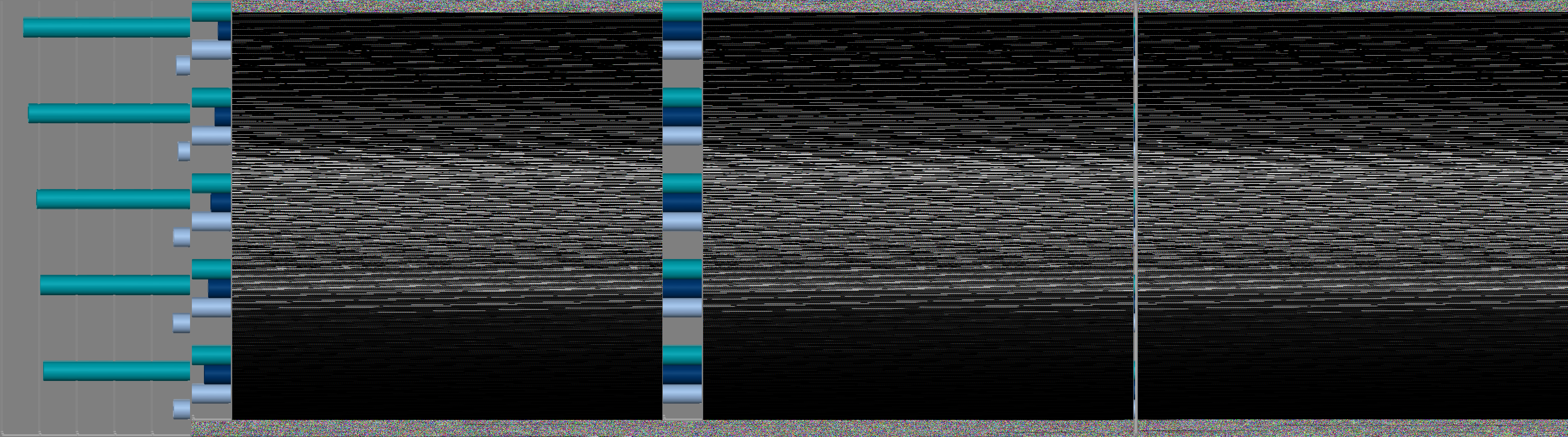

Chart 1 shows the number of students who became members worldwide of each of seven accountancy bodies as at 31 December for each of the four years to 31 December 2012.

Chart 1: Students who became Members for the Years Ending 2009 - 2012

A bar chart showing the number of students who became members worldwide for each of seven accountancy bodies (ACCA, CIMA, CIPFA, ICAEW, CAI, ICAS, AIA) for the years 2009, 2010, 2011, and 2012.

The y-axis represents the number of members, ranging from 0 to 10,000. The x-axis represents the accountancy bodies. Each body has four bars, representing the years 2009 (light blue), 2010 (dark blue), 2011 (teal), and 2012 (green).

- ACCA: Approximately 8,500-9,500 members per year, with 2012 being the highest.

- CIMA: Approximately 4,500-5,800 members per year, showing an increasing trend.

- CIPFA: Approximately 500-600 members per year, with slight fluctuations.

- ICAEW: Approximately 3,500-3,800 members per year, relatively consistent.

- CAI: Approximately 1,200-1,500 members per year, with 2009 being the highest.

- ICAS: Approximately 800-1,000 members per year, relatively consistent.

- AIA: Approximately 100-200 members per year, showing a slight increase.

- The majority of the seven accountancy bodies have a consistent uptake of membership each year, with the exception of CIMA whose intake has continued to increase.

Sectoral Employment of Members Worldwide 2012

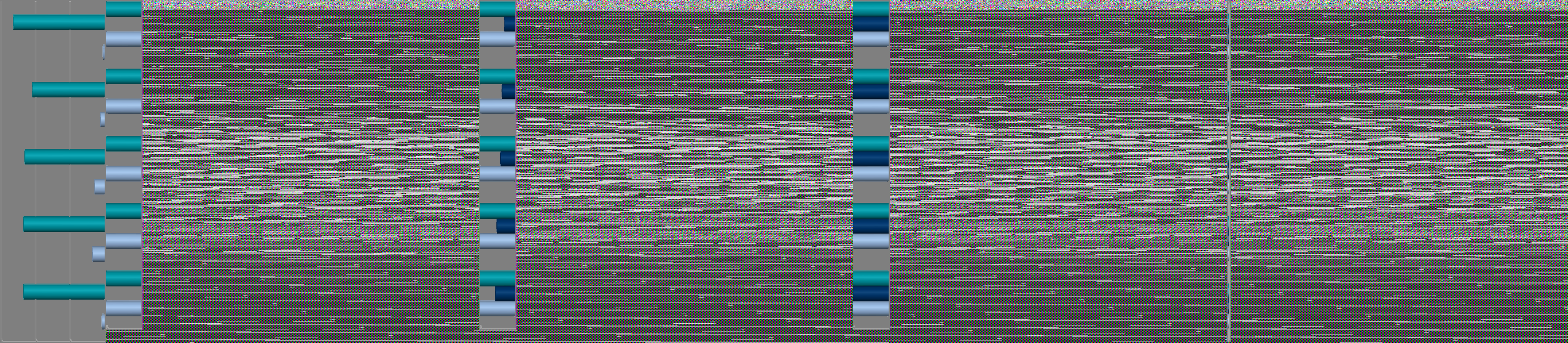

Chart 2 shows the percentages of members worldwide of each of the seven accountancy bodies, according to their sectoral employment5 at the end of 2012.

Chart 2: Sectoral Employment of Members Worldwide 2012

A stacked bar chart showing the percentage of members worldwide of seven accountancy bodies (ACCA, CIMA, CIPFA, ICAEW, CAI, ICAS, AIA) according to their sectoral employment at the end of 2012.

The y-axis represents percentage from 0% to 100%. The x-axis represents the accountancy bodies. The stacked bars show the distribution across "Public Practice" (dark blue), "Industry & Commerce" (teal), "Public Sector" (light blue), "Retired" (light green), and "Other" (dark green).

- ACCA: Large proportion in Industry & Commerce (approx. 60%), followed by Public Practice (approx. 25%).

- CIMA: Dominantly Industry & Commerce (approx. 75%).

- CIPFA: Majority in Public Sector (approx. 60%).

- ICAEW: Substantial portions in Industry & Commerce (approx. 50%) and Public Practice (approx. 30%).

- CAI: Large proportion in Industry & Commerce (approx. 50%), followed by Public Practice (approx. 35%).

- ICAS: Significant portions in Industry & Commerce (approx. 40%) and Public Practice (approx. 35%).

- AIA: Dominantly Industry & Commerce (approx. 85%).

- There are few CIMA, CIPFA and AIA members employed in public practice at 2%, 3% and 4% respectively.

- All bodies apart from CIPFA have more members employed in industry and commerce than in any other category.

- CIPFA is the only body with the majority of its members employed in the public sector.

Gender of Members Worldwide 2008 - 2012

Table 3 shows the percentage of female members worldwide of each of seven accountancy bodies as at 31 December for each of the five years to 31 December 2012.

| ACCA | CIMA | CIPFA | ICAEW | CAI | ICAS | AIA | TOTAL | |

|---|---|---|---|---|---|---|---|---|

| 2008 | 42 | 30 | 29 | 24 | 33 | 28 | 27 | 32 |

| 2009 | 43 | 30 | 30 | 24 | 35 | 29 | 26 | 33 |

| 2010 | 44 | 31 | 30 | 25 | 36 | 30 | 28 | 34 |

| 2011 | 44 | 32 | 31 | 25 | 37 | 31 | 29 | 34 |

| 2012 | 45 | 33 | 31 | 26 | 38 | 31 | 30 | 35 |

Table 3

- The percentage of female members has risen steadily from 32% in 2008 to 35% in 2012.

- ACCA and CAI continue to have the largest proportion of female members.

Age of Members Worldwide 2012

Charts 3 and 4 on the following pages compare the age distribution of members of the seven accountancy bodies as at 31 December, for 2008 and 2012.

- There are significant differences in the age profiles of worldwide members of the seven accountancy bodies. ACCA and CAI have the youngest population of members, with 68% and 67% respectively younger than 45 years. (Chart 3).

- More than 50% of the members of CIPFA, ICAEW, ICAS and AIA are aged 45 or over (Chart 3).

- CIPFA has the oldest age profile of members, with 71% aged 45 or over, compared to 64% in 2008.

Chart 3: Comparison of Age Profile of Members of Accountancy Bodies Worldwide 2012

A stacked bar chart showing the age profile of members of seven accountancy bodies (ACCA, CIMA, CIPFA, ICAEW, CAI, ICAS, AIA) worldwide in 2012.

The y-axis represents percentage from 0% to 100%. The x-axis represents the accountancy bodies. The stacked bars show the distribution across age categories: "Under 25" (light blue), "25-34" (dark blue), "35-44" (teal), "45-54" (light green), "55-64" (dark green), and "65 and over" (light yellow).

- ACCA: Large proportions in 25-34 (approx. 45%) and 35-44 (approx. 40%).

- CIMA: Significant portions in 25-34 (approx. 35%), 35-44 (approx. 35%), and 45-54 (approx. 20%).

- CIPFA: Highest proportion in 45-54 (approx. 30%), followed by 35-44 (approx. 25%) and 55-64 (approx. 25%).

- ICAEW: Highest proportion in 35-44 (approx. 40%), followed by 25-34 (approx. 20%) and 45-54 (approx. 20%).

- CAI: Large proportions in 25-34 (approx. 30%), 35-44 (approx. 30%), and 45-54 (approx. 25%).

- ICAS: Significant portions in 35-44 (approx. 25%), 45-54 (approx. 20%), and 55-64 (approx. 20%).

- AIA: High proportions in 35-44 (approx. 35%) and 45-54 (approx. 25%).

Chart 4: Comparison of Age Profile of Members of Accountancy Bodies Worldwide 2008

A stacked bar chart showing the age profile of members of seven accountancy bodies (ACCA, CIMA, CIPFA, ICAEW, CAI, ICAS, AIA) worldwide in 2008.

The y-axis represents percentage from 0% to 100%. The x-axis represents the accountancy bodies. The stacked bars show the distribution across age categories: "Under 25" (light blue), "25-34" (dark blue), "35-44" (teal), "45-54" (light green), "55-64" (dark green), and "65 and over" (light yellow).

- ACCA: Large proportions in 25-34 (approx. 40%) and 35-44 (approx. 35%).

- CIMA: Significant portions in 25-34 (approx. 35%), 35-44 (approx. 30%), and 45-54 (approx. 20%).

- CIPFA: Highest proportion in 45-54 (approx. 25%), followed by 35-44 (approx. 25%) and 55-64 (approx. 25%).

- ICAEW: Highest proportion in 35-44 (approx. 35%), followed by 25-34 (approx. 20%) and 45-54 (approx. 20%).

- CAI: Large proportions in 25-34 (approx. 30%), 35-44 (approx. 30%), and 45-54 (approx. 20%).

- ICAS: Significant portions in 35-44 (approx. 25%), 45-54 (approx. 20%), and 55-64 (approx. 20%).

- AIA: High proportions in 35-44 (approx. 30%) and 45-54 (approx. 25%).

Section Three – Students of Accountancy Bodies

Students Registered in the UK and Republic of Ireland 2008 - 2012

Table 4 shows the number of students of each of seven accountancy bodies in the UK and Republic of Ireland as at 31 December for each of the five years to 31 December 2012.

| ACCA | CIMA | CIPFA | ICAEW | CAI | ICAS | AIA | TOTAL | |

|---|---|---|---|---|---|---|---|---|

| 2008 | 86,515 | 56,427 | 2,849 | 14,560 | 5,947 | 3,437 | 136 | 169,871 |

| 2009 | 88,082 | 54,373 | 2,913 | 14,206 | 6,171 | 3,075 | 143 | 168,963 |

| 2010 | 91,690 | 54,470 | 2,687 | 14,510 | 5,771 | 2,962 | 151 | 172,241 |

| 2011 | 89,220 | 54,645 | 2,437 | 15,014 | 6,348 | 2,994 | 155 | 170,813 |

| 2012 | 84,058 | 54,010 | 2,244 | 15,321 | 6,265 | 3,056 | 185 | 165,139 |

| % growth (11-12) | -5.8 | -1.2 | -7.9 | 2.0 | -1.3 | 2.1 | 19.4 | -3.3 |

| % growth (08-12) | -2.8 | -4.3 | -21.2 | 5.2 | 5.3 | -11.1 | 36.0 | -2.8 |

| % compound annual growth (08-12) | -0.7 | -1.1 | -5.8 | 1.3 | 1.3 | -2.9 | 8.0 | -0.7 |

Table 4

- Whilst student numbers in the rest of the world have increased by 2.3%, student numbers in the UK and ROI have declined by 3.3% in 2012.

- The ICAEW, CAI and AIA have all seen an increase in student numbers between 2008 and 2012.

Students Registered Worldwide 2008 - 2012

Table 5 shows the total number of students and individuals worldwide including those who have passed their final admittance examination and completed all necessary practical training but have not yet applied for membership.

| ACCA | CIMA | CIPFA | ICAEW | CAI | ICAS | AIA | TOTAL | |

|---|---|---|---|---|---|---|---|---|

| 2008 | 307,457 | 91,524 | 2,885 | 16,165 | 5,958 | 3,466 | 6,514 | 433,969 |

| 2009 | 334,423 | 92,909 | 2,978 | 16,517 | 6,171 | 3,119 | 7,157 | 463,274 |

| 2010 | 357,952 | 99,264 | 2,764 | 17,653 | 5,771 | 3,004 | 7,813 | 494,221 |

| 2011 | 349,325 | 106,612 | 2,550 | 19,073 | 6,361 | 3,024 | 8,431 | 495,376 |

| 2012 | 353,589 | 112,727 | 2,336 | 20,037 | 6,276 | 3,083 | 8,952 | 507,000 |

| % growth (11 - 12) | 1.2 | 5.7 | -8.4 | 5.1 | -1.3 | 2.0 | 6.2 | 2.3 |

| % growth (08 - 12) | 15.0 | 23.2 | -19.0 | 24.0 | 5.3 | -11.1 | 37.4 | 16.8 |

| % compound annual growth (08-12) | 3.6 | 5.3 | -5.1 | 5.5 | 1.3 | -2.9 | 8.3 | 4.0 |

Table 5

- There continue to be wide differences in the numbers and rates of growth in the student membership worldwide.

- Overall student numbers increased by 2.3% in 2012 with an overall compound annual growth of 4%.

- The ACCA, CIMA, AIA and the ICAEW all experienced substantial growth in student numbers of between 2008 and 2012.

Location of Students 2012

Chart 5 shows the location3 (UK and Republic of Ireland, and the rest of the world) of students of seven accountancy bodies as at 31 December 2012.

Chart 5: Location of Students as at 31 December 2012

A stacked bar chart showing the location of students (UK & Republic of Ireland vs. Rest of the World) for seven accountancy bodies (ACCA, CIMA, CIPFA, ICAEW, CAI, ICAS, AIA) as at 31 December 2012.

The y-axis represents percentage from 0% to 100%. The x-axis represents the accountancy bodies. The stacked bars show the distribution between "UK & Republic of Ireland" (dark blue) and "Rest of the World" (light blue).

- ACCA: Approximately 25% UK & ROI, 75% Rest of the World.

- CIMA: Approximately 45% UK & ROI, 55% Rest of the World.

- CIPFA: Over 90% UK & ROI.

- ICAEW: Approximately 75% UK & ROI, 25% Rest of the World.

- CAI: Over 90% UK & ROI.

- ICAS: Over 90% UK & ROI.

- AIA: Approximately 5% UK & ROI, 95% Rest of the World.

- CIPFA, CAI and ICAS have very low proportions of students based outside of the UK and ROI.

- In contrast, the ACCA has 24% of students in the UK and ROI and almost all of the AIA's students are based outside the UK and ROI with only 2% in the UK and ROI.

Profile of Students Worldwide of Seven Accountancy Bodies 2012

Chart 6 sets out on a worldwide basis the length of time that individuals have been registered as students with these accountancy bodies6.

Chart 6: Profile of Students Worldwide of Seven Accountancy Bodies 2012

A stacked bar chart showing the length of time individuals have been registered as students with seven accountancy bodies (ACCA, CIMA, CIPFA, ICAEW, CAI, ICAS, AIA) worldwide in 2012.

The y-axis represents percentage from 0% to 100%. The x-axis represents the accountancy bodies. The stacked bars show the distribution across duration categories: "≤ 1 Year" (dark blue), "> 1-2 Years" (light blue), "> 2-3 Years" (teal), "> 3-4 Years" (light green), "> 4-5 Years" (dark green), and "≥ 5 Years" (light yellow).

- ACCA: Significant proportions in "> 1-2 Years" (approx. 20%), "> 2-3 Years" (approx. 18%), and "≥ 5 Years" (approx. 40%).

- CIMA: Significant proportions in "≤ 1 Year" (approx. 30%), "> 1-2 Years" (approx. 20%), "> 2-3 Years" (approx. 15%), and "≥ 5 Years" (approx. 20%).

- CIPFA: Dominant in "≤ 1 Year" (approx. 30%) and "> 1-2 Years" (approx. 30%).

- ICAEW: Highest proportion in "≤ 1 Year" (approx. 45%), followed by "> 1-2 Years" (approx. 30%).

- CAI: Highest proportion in "≤ 1 Year" (approx. 35%), followed by "> 1-2 Years" (approx. 25%), and "> 2-3 Years" (approx. 20%).

- ICAS: Highest proportion in "≤ 1 Year" (approx. 30%), followed by "> 1-2 Years" (approx. 25%) and "> 2-3 Years" (approx. 20%).

- AIA: Significant proportions in "≤ 1 Year" (approx. 20%), "> 1-2 Years" (approx. 15%), and "≥ 5 Years" (approx. 35%).

- The chart above must be read with caution as there is not a common basis for determining the length of time between registering as a student and achieving the requirements for membership7.

- Students at ACCA, CIMA, and AIA do not typically undertake intensive study and generally take longer to complete the requirements for membership.

- A high percentage of ICAEW, CAI and ICAS students complete their training in 4 years or less with only 8%, 23% and 7% respectively of students as at 31 December 2012 being registered for more than 4 years.

Gender of Students Worldwide 2012

Table 6 shows the percentage worldwide of female students of each of the accountancy bodies as at 31 December 2012.

| ACCA | CIMA | CIPFA | ICAEW | CAI8 | ICAS8 | AIA | TOTAL | |

|---|---|---|---|---|---|---|---|---|

| 2008 | 50 | 45 | 48 | 41 | 53 | 47 | 57 | 49 |

| 2009 | 50 | 44 | 50 | 41 | 53 | 47 | 63 | 49 |

| 2010 | 49 | 44 | 50 | 40 | 52 | 45 | 64 | 49 |

| 2011 | 50 | 44 | 48 | 38 | 51 | 44 | 63 | 48 |

| 2012 | 49 | 44 | 49 | 38 | 50 | 43 | 63 | 48 |

Table 6

- The total proportion of female students worldwide has remained broadly constant between 2008 and 2012.

- The percentage of female students is significantly higher than the percentage of female members (see Table 3).

Age of Students Worldwide of Seven Accountancy Bodies 2012

Charts 7 and 8 on the following pages compare the age distribution of students of the seven accountancy bodies as at 31 December, 2008 and 2012.

- CIPFA and the AIA have a higher proportion of mature students than the other bodies, with 52% and 39% respectively of students aged 35 or over. (Chart 7)

- ICAEW, CAI and ICAS have the highest proportion of students aged 34 or under. (95%, 91% and 81% respectively under 35. (Chart 7)

- 74% of the overall student numbers were under 35, compared to 77% in 2008.

Chart 7: Comparison of Age Profile of Students of Accountancy Bodies Worldwide 2012

A stacked bar chart showing the age profile of students of seven accountancy bodies (ACCA, CIMA, CIPFA, ICAEW, CAI, ICAS, AIA) worldwide in 2012.

The y-axis represents percentage from 0% to 100%. The x-axis represents the accountancy bodies. The stacked bars show the distribution across age categories: "Under 25" (light blue), "25-34" (dark blue), "35-44" (teal), "45 and over" (light green), and "Unknown" (dark green).

- ACCA: Large proportions in "25-34" (approx. 45%) and "Under 25" (approx. 30%).

- CIMA: Significant portions in "25-34" (approx. 45%) and "Under 25" (approx. 30%).

- CIPFA: Significant portions in "25-34" (approx. 25%), "35-44" (approx. 25%), and "45 and over" (approx. 25%).

- ICAEW: Dominant in "Under 25" (approx. 50%) and "25-34" (approx. 35%).

- CAI: Large proportions in "Under 25" (approx. 35%), "25-34" (approx. 35%), and "35-44" (approx. 20%).

- ICAS: Significant portions in "Under 25" (approx. 30%), "25-34" (approx. 30%), and "35-44" (approx. 20%).

- AIA: Significant proportions in "25-34" (approx. 35%), "35-44" (approx. 25%), and "45 and over" (approx. 25%).

Chart 7: Comparison of Age Profile of Students of Accountancy Bodies Worldwide 2012 A bar chart showing the age distribution of students across seven accountancy bodies (ACCA, CIMA, CIPFA, ICAEW, CAI, ICAS, AIA) in

- Each bar represents an accountancy body, segmented by age categories: 'Under 25' (light blue), '25-34' (dark blue), '35-44' (teal), '45 and over' (green), and 'Unknown' (dark green/black). The y-axis ranges from 0% to 100%.

Chart 8: Comparison of Age Profile of Students of Accountancy Bodies Worldwide 2008

A bar chart similar to Chart 7, displaying the age distribution of students across the same seven accountancy bodies in 2008, using the same age categories and color coding. The y-axis ranges from 0% to 100%.

Sectoral Employment of Students Worldwide 2012

Chart 9 shows the sectoral employment of worldwide students of each of the accountancy bodies as at 31 December 2012.

Chart 9: Sectoral Employment of Students Worldwide 2012 A bar chart showing the sectoral employment distribution of students across seven accountancy bodies (ACCA, CIMA, CIPFA, ICAEW, CAI, ICAS, AIA) in

- Each bar represents an accountancy body, segmented by employment categories: 'Public Practice' (light blue), 'Industry & Commerce' (dark blue), 'Public Sector' (teal), and 'Other' (green). The y-axis ranges from 0% to 100%.

- Over 80% of students at ICAEW, CAI and ICAS are in public practice. In contrast only 18% of ACCA's students, and less than 1% of AIA's students, are employed in public practice.

- CIMA has the highest percentage of students in industry and commerce (73%) and CIPFA has the highest percentage in the public sector (87%). Overall, 52% of students are in industry and commerce

- Of the employment sectors there are 18% in public practice and 13% in the public sector.

- ACCA's students are the most evenly dispersed across the different employment sectors.

Graduate Entrants to Training with Seven Accountancy Bodies

Chart 10 shows the percentages of students worldwide of each body who, at the time of registration as students, were (i) graduates of any discipline and, of those, (ii) graduates who held a relevant degree.

Chart 10: Percentage of Students Holding a Degree or a Relevant Degree Worldwide in 2012 A bar chart showing the percentage of students holding 'a Degree' (light blue) and 'a Relevant Degree' (dark blue) for seven accountancy bodies (ACCA, CIMA, CIPFA, ICAEW, CAI, ICAS, AIA) in

- The y-axis ranges from 0% to 100%.

- Comparisons of the percentage of students holding "relevant degrees" are difficult to draw, because the accountancy bodies use different definitions of a "relevant degree"3.

Pass Rates 2008-2012

Chart 11 shows the percentage of candidates who passed the final examination, for the period 2008 to 2012 and chart 12 shows the percentage of those that were first time passes4.

Chart 11: Percentage of Passes at the Final Examination 2008 - 2012 A line chart showing the percentage of passes at the final examination for seven accountancy bodies (ACCA, CIMA, CIPFA, ICAEW, CAI, ICAS, AIA) from 2008 to

- Each body is represented by a distinct colored line and marker. The y-axis ranges from 0% to 100%.

- Comparisons of the pass rates across the bodies and year-on-year are difficult, for example, because of differences in the syllabus and the topics examined at each stage of each body's qualification and because the composition of the student populations across the bodies varies substantially.

Chart 12: Percentage of those Passes that were First Time Passes 2008 - 2012 A line chart showing the percentage of passes that were first time passes for five accountancy bodies (ACCA, CIMA, CIPFA, ICAEW, CAI) from 2008 to

- Each body is represented by a distinct colored line and marker. The y-axis ranges from 30% to 100%.

Section Four – Resource Information on Accountancy Bodies

Analysis of Income of Seven Accountancy Bodies 2008 – 2012

Charts 13 to 15 show the income, surplus/deficit, average income per member/student and analysis of income of seven accountancy bodies worldwide over the period 2008 to 2012.

Chart 13: Income of Seven Accountancy Bodies Worldwide between 2008 - 2012 A line chart illustrating the income in £M for seven accountancy bodies (ACCA, CIMA, CIPFA, ICAEW, CAI, ICAS, AIA) from 2008 to

- Each body is represented by a distinct colored line with markers. The y-axis ranges from 0.0 to 160.0 £M.

- ACCA has the fastest growing income, rising at a compound annual rate of 9.8% over the period 2008 to 2012.

- The compound annual growth rate of the income of all the bodies was 3.5% in the period of 2008 to 2012.

Chart 14: Average Income per Member and Student of Seven Accountancy Bodies Worldwide between 2008 - 2012 A line chart showing the average income per member and student in £ for seven accountancy bodies (ACCA, CIMA, CIPFA, ICAEW, CAI, ICAS, AIA) from 2008 to

- Each body is represented by a distinct colored line with markers. The y-axis ranges from 50 to 1,150 £.

- CAI has seen a drop in the average income per member and student between 2008 and 2012 of 38.1%. This is due to decreases in subscription rates, education fees and CPD rates over this period.

Chart 15: Analysis of the Income for Seven Accountancy Bodies in 2012 A bar chart showing the breakdown of income sources for seven accountancy bodies (ACCA, CIMA, CIPFA, ICAEW, CAI, ICAS, AIA) in

- Each bar represents an accountancy body, segmented by income categories: 'Fees & Subscriptions' (light blue), 'Commercial Activities' (dark blue), 'Education & Exam Fees' (teal), 'Regulation & Discipline' (green), and 'Other (Including Investment Income)' (dark green/black). The y-axis ranges from 0% to 100%.

-

Fees and subscriptions taken together with education and exam fees from members and students are the main sources of income for each of the bodies other than CIPFA.

-

Income from commercial activities includes income from activities such as conferences, training courses and publications.

- The ACCA's income and costs are for the year to 31 March 2013.

Staffing of Seven Accountancy Bodies 2008 – 2012

Table 7 shows the number of staff (full time equivalent) employed worldwide by seven accountancy bodies over the period 2008 to 2012.

| ACCA | CIMA | CIPFA | ICAEW | CAI | ICAS | AIA | TOTAL | |

|---|---|---|---|---|---|---|---|---|

| 2008 | 824 | 283 | 308 | 623 | 135 | 142 | 25 | 2,340 |

| 2009 | 902 | 362 | 304 | 599 | 133 | 129 | 25 | 2,454 |

| 2010 | 981 | 371 | 304 | 619 | 138 | 141 | 25 | 2,579 |

| 2011 | 1,032 | 378 | 272 | 657 | 135 | 135 | 25 | 2,634 |

| 2012 | 1,061 | 415 | 228 | 652 | 134 | 140 | 25 | 2,655 |

| % growth (11-12) | 2.8 | 9.8 | -16.2 | -0.8 | -0.7 | 3.7 | 0.0 | 0.8 |

| % growth (08-12) | 28.8 | 46.6 | -26.0 | 4.7 | -0.7 | -1.4 | 0.0 | 13.5 |

| % compound annual growth (08-12) | 6.5 | 10.0 | -7.2 | 1.1 | -0.2 | -0.4 | 0.0 | 3.2 |

- The total number of staff employed by the bodies has increased by 13.5% in the period 2008 to 2012.

- Only CIMA increased its staff significantly in 2012. CIPFA has seen a decrease in staff levels of 16.2% proportionate with a fall in membership. Staffing at other bodies remains stable.

Section Five – Oversight of Audit Regulation

Recognised Supervisory Bodies (RSBs)

The FRC recognises five bodies, known as Recognised Supervisory Bodies (RSBs)1 to register and supervise audit firms, in accordance with the requirements of Schedule 10 to the Companies Act

- The RSBs meet the requirements of the Act through four main processes; audit registration, audit monitoring, arrangements for the investigation of complaints, and procedures to ensure that those eligible for appointment as a statutory auditor continue to maintain an appropriate level of competence.

Table 8 details the number of registered audit firms for the five RSBs split by number of principals at each firm as at 31 December for each of the five years to 31 December 2012.

Number of Firms Registered with the Recognised Supervisory Bodies

| Number of Principals in Firm | ACCA | AAPA | ICAEW | CAI | ICAS | TOTAL |

|---|---|---|---|---|---|---|

| 1 | 1,329 | 48 | 1,609 | 579 | 78 | 3,643 |

| 2 - 6 | 914 | 1 | 1,841 | 384 | 124 | 3,264 |

| 7 - 10 | 6 | 0 | 164 | 10 | 11 | 191 |

| 11 -50 | 6 | 0 | 97 | 10 | 6 | 119 |

| 50+ | 0 | 0 | 17 | 3 | 2 | 22 |

| Total as at 31.12.12 | 2,255 | 49 | 3,728 | 986 | 221 | 7,239 |

| Total as at 31.12.11 | 2,224 | 57 | 3,864 | 995 | 235 | 7,375 |

| Total as at 31.12.10 | 2,217 | 61 | 3,958 | 986 | 235 | 7,457 |

| Total as at 31.12.09 | 2,436 | 67 | 4,113 | 985 | 242 | 7,843 |

| Total as at 31.12.08 | 2,489 | 80 | 4,279 | 991 | 260 | 8,099 |

Application for Registration as a Statutory Audit Firm & the Number Refused 2010 – 2012

| Applications | New | Refused | |

|---|---|---|---|

| ACCA | 132 | 0 | |

| ICAEW | 270 | 1 | |

| 2010 | CAI | 49 | 3 |

| ICAS | 44 | 0 | |

| TOTAL | 495 | 4 | |

| ACCA | 142 | 2 | |

| ICAEW | 235 | 0 | |

| 2011 | CAI | 73 | 1 |

| ICAS | 10 | 0 | |

| TOTAL | 460 | 3 | |

| ACCA | 138 | 0 | |

| ICAEW | 186 | 1 | |

| 2012 | CAI | 66 | 1 |

| ICAS | 30 | 0 | |

| TOTAL | 420 | 2 |

- The number of firms registered to carry out statutory audit work in the UK continues to fall, although the rate of decrease has slowed. The number of registered audit firms fell by 10.6% between 2008 and 2012 and by 1.8% during 2012.

- The number of sole practitioners fell by 4% in 2012. The number of sole practitioners has declined each year since 20032.

- The decrease in the number of registered audit firms has coincided with an increase in the proportion of companies filing annual accounts at Companies House that are audit exempt, from 69.1% in 2007/08 to 71.4% in 2011/123. This follows increases in the audit exemption threshold in 2004 and 2008.

Monitoring of Registered Audit Firms

Table 10 below gives details of the number of monitoring visits conducted by the RSBs during the years ended 31 December 2008 to 31 December 2012, and the proportion of registered audit firms that were visited during these years. There is a statutory requirement that the RSBs should monitor the activities undertaken by each registered audit firm at least once every six years.

Registered Audit Firms Monitored during the Years Ending 31 December 2008 to 2012

| ACCA4 | ICAEW | CAI | ICAS | TOTAL | ||

|---|---|---|---|---|---|---|

| No | 406 | 988 | 95 | 54 | 1,543 | |

| 2008 | % | 15.8 | 23.1 | 9.6 | 20.8 | 19.1 |

| No | 425 | 757 | 102 | 51 | 1,335 | |

| 2009 | % | 17.0 | 18.4 | 10.4 | 21.1 | 17.0 |

| No | 357 | 751 | 84 | 50 | 1,242 | |

| 2010 | % | 15.7 | 19.0 | 8.5 | 21.3 | 16.7 |

| No | 373 | 716 | 22 | 56 | 1,167 | |

| 2011 | % | 16.4 | 18.5 | 2.2 | 23.8 | 15.8 |

| No | 579 | 691 | 126 | 40 | 1,436 | |

| 2012 | % | 25.1 | 16.8 | 12.8 | 16.5 | 18.3 |

Table 10

Reasons for Monitoring Visits to firms during the Years Ending 31 December 2010 to 2012

| ACCA | ICAEW | CAI | ICAS | TOTAL | ||

|---|---|---|---|---|---|---|

| Requested by the registration/licensing committee | 2010 | 17 | 11 | 5 | 17 | 50 |

| 2011 | 46 | 29 | 3 | 16 | 94 | |

| 2012 | 47 | 8 | 2 | 14 | 71 | |

| Specifically selected due to heightened risk | 2010 | 41 | 68 | 87 | 33 | 229 |

| 2011 | 42 | 59 | 19 | 39 | 159 | |

| 2012 | 27 | 39 | 67 | 24 | 157 | |

| Randomly selected | 2010 | 299 | 617 | 2 | 0 | 918 |

| 2011 | 285 | 579 | 0 | 0 | 864 | |

| 2012 | 505 | 596 | 57 | 0 | 1,158 | |

| Firms with Public Interest Entities visited without AQR10 involvement11 | 2010 | 0 | 59 | 3 | 0 | 62 |

| 2011 | 0 | 49 | 0 | 0 | 49 | |

| 2012 | 0 | 48 | 0 | 1 | 49 | |

| Firms with Public Interest Entities visited with AQR involvement | 2010 | 0 | 0 | 0 | 3 | 3 |

| 2011 | 0 | 0 | 0 | 1 | 1 | |

| 2012 | 0 | 0 | 0 | 1 | 1 |

Table 11

- The majority of Public Interest Entities are audited by firms registered with the ICAEW. These firms are subject to monitoring, independent of the RSBs, by the AQR team.

- CAI increased the number of visits to randomly selected firms and deployed additional resources to monitoring in order to meet the requirement to visit all firms in a 6 year period.

Gradings 2010 - 2012

Tables 12 to 15 show the gradings for the audit monitoring visits conducted by ACCA, ICAEW, CAI and ICAS during the years ended 31 December 2010 to 2012 together with brief explanatory comments from the bodies where available.

The RSBs have undertaken a joint project with the aim of achieving more consistent data on the quality of audit files reviewed across all the bodies. This has been largely achieved although there continue to be some differences in the name of the overall grades used by each body for the visit as a whole and in the monitoring process itself.

The monitoring results for any one year are not typically directly comparable with the results of previous years. This is because the mix of firms selected in each year is likely to vary, as between firms selected as higher risk, those randomly selected and firms selected to meet the six year cycle.

Particular care is needed in interpreting the percentage of "D" outcomes at each body, especially given that the sample of firms inspected in any year will often include a disproportionate number of weaker firms selected because of higher risk.

It should also be noted that outcomes include a number of visits to audit registered firms that currently have no audit clients.

Association of Chartered Certified Accountants (ACCA)

| ACCA | 2010 | 2011 | 2012 | |

|---|---|---|---|---|

| No | 223 | 208 | 417 | |

| A & B Outcomes | % | 62 | 56 | 72 |

| No | 38 | 47 | 48 | |

| C+ Outcomes | % | 11 | 12 | 8 |

| No | 9 | 14 | 18 | |

| C- Outcomes | % | 3 | 4 | 3 |

| No | 87 | 104 | 96 | |

| D Outcomes | % | 24 | 28 | 17 |

Table 12

Those firms that are graded 'A' are judged to comply with all aspects of the Global Practising Regulations (GPRS), Code of Ethics and Conduct (CEC) and relevant auditing standards. Those firms rated 'B' are judged to comply with the GPRs, CEC and auditing standards in all material respects. Firms are graded 'C+' or 'C-' by the ACCA if their quality controls over audit work are either weak or not consistently effective so that the audit work is unsatisfactory and improvements are required. The 'C-' grade indicates that the improvements required are significant. When a firm's work is very poor or if a firm has a second or subsequent unsatisfactory visit and there are no mitigating factors the visit is graded a 'D' and the firm will be referred to a regulatory assessor or the Admissions and Licensing Committee (ALC). A 'D' outcome does not always result from an inadequate standard of audit work; it may also indicate a firm has failed to meet the eligibility requirements to hold a firm's auditing certificate.

The 417 visits with 'A' & 'B' outcomes in 2012 include 217 visits to firms that currently had no audit clients. This has had a significant effect on the overall percentages of satisfactory and unsatisfactory outcomes.

Institute of Chartered Accountants in England & Wales (ICAEW)

| ICAEW | 2010 | 2011 | 2012 | |

|---|---|---|---|---|

| No | 486 | 385 | 422 | |

| A & B Outcomes | % | 64 | 54 | 61 |

| No | 132 | 149 | 137 | |

| C Outcomes | % | 17 | 21 | 20 |

| No | 80 | 71 | 62 | |

| D Outcomes | % | 11 | 10 | 9 |

| No | 57 | 111 | 70 | |

| N Outcomes | % | 8 | 15 | 10 |

Table 13

Visits graded 'A' are those where there are no instances of non-compliance with the Institute's audit regulations and no follow-up action is required. 'B' rated visits are those with evidence of non-compliance with the Audit Regulations, but where the Quality Assurance Directorate (QAD) is confident that the firm's responses, as set out in the closing meeting notes, adequately address all the issues and that no follow up action is required. A 'C' rated report records instances of non-compliance with the Audit Regulations where the QAD considers that there is some doubt about the actions proposed or the firm's competence, resources or commitment, but that there is no need for the Audit Registration Committee (ARC) to impose further conditions or restrictions. 'D' rated visits record cases of non-compliance with the Audit Regulations that need to be referred to the ARC for possible further action. An 'N' visit grading is used for any circumstances that cannot be rated in accordance with the criteria set out above, for example, when a firm wishes to continue with registration but has no audit clients and no audit work has been reviewed or the firm has applied to withdraw from registration and QAD proposes acceptance.

The percentage visit gradings in 2012 remain broadly consistent with 2011.

Chartered Accountants Ireland (CAI)

| Chartered Accountants Ireland | 2010 | 2011 | 2012 | |

|---|---|---|---|---|

| No | 21 | 13 | 31 | |

| A & B Outcomes | % | 20 | 37 | 41 |

| No | 40 | 9 | 24 | |

| C Outcomes | % | 40 | 26 | 32 |

| No | 41 | 13 | 21 | |

| D Outcomes | % | 40 | 37 | 28 |

Table 14

Reports graded 'A' are where no instances of non-compliance have been recorded. Grade 'B' indicates that the firm has the ability and commitment to address the issues identified during the visit. Where reports are graded 'C', firms are required to give undertakings in writing covering the actions they must take and some further follow-up action may be required. There is a considerable difference between a report graded a 'C' and one graded a 'D'. Reports graded a 'D' have significant issues and will always require follow-up action. Those reports will always be considered by the Head of Quality Assurance and by the Quality Assurance Committee (QAC).

Institute of Chartered Accountants of Scotland (ICAS)

| ICAS | 2010 | 2011 | 2012 | |

|---|---|---|---|---|

| No | 30 | 27 | 18 | |

| A & B Outcomes | % | 60 | 48 | 45 |

| No | 11 | 15 | 9 | |

| C2 Outcomes | % | 22 | 27 | 22 |

| No | 6 | 6 | 8 | |

| C1 Outcomes | % | 12 | 10 | 20 |

| No | 3 | 8 | 5 | |

| D Outcomes | % | 6 | 15 | 13 |

Table 15

An 'A' rating indicates that there are no issues to deal with. A 'B' rating indicates there are some regulatory issues but that these have been addressed adequately by the firm's closing meeting responses and no further action is required. 'C' gradings indicate that there are regulatory issues and there is a need for the firm to show that planned changes have occurred by submitting further information. The 'C' grading is split into 'C1' and 'C2' gradings with 'C1' being the more serious. This is used where the issues are considered to be pervasive, whereas 'C2' gradings are used where findings are specific to particular individuals or files and do not indicate systemic problems. A 'D' rating is given when the standard of compliance is such that the Audit Registration Committee (ARC) needs to consider appropriate follow-up action, such as imposition of conditions and restrictions or withdrawal of registration.

Complaints about Auditors

Table 16 shows the number of complaints received by the RSBs between 2010 to 2012 to show (i) number of new cases12, (ii) number of cases passed to the FRC Professional Discipline Team13, (iii) number of cases passed to the committee5, (iv) number of complaints closed in the year6 and (v) average time taken to close a complaint.

| ACCA | ICAEW | CAI7 | ICAS | TOTAL | |

|---|---|---|---|---|---|

| 2010 | 24 | 95 | 20 | 2 | 141 |

| Number of New Cases | 2011 | 31 | 85 | 36 | 8 |

| 2012 | 32 | 84 | 21 | 3 | |

| 2010 | 0 | 0 | 0 | 0 | 0 |

| Number of Cases directly8 passed to the FRC Professional Discipline team | 2011 | 0 | 2 | 0 | 0 |

| 2012 | 0 | 0 | 0 | 0 | |

| 2010 | 8 | 66 | 20 | 2 | 96 |

| Number of Cases passed to the Committee | 2011 | 3 | 71 | 12 | 6 |

| 2012 | 3 | 54 | 5 | 0 | |

| 2010 | 24 | 89 | 13 | 1 | 127 |

| Number of Complaints closed in the year | 2011 | 43 | 89 | 6 | 3 |

| 2012 | 22 | 82 | 3 | 3 | |

| 2010 | 7.8 | 10 | 9 | 3.9 | |

| Average time taken to close a Complaint (in months) | 2011 | 10.3 | 11 | 4.6 | 5.6 |

| 2012 | 12.1 | 11 | 5.3 | 3.4 |

Table 16

- The figures of CAI complaints for 2011 and 2012 are for audit-related complaints only.

- ICAS has explained that the number of new audit-related complaints increased to 8 from 2 in 2010 which had been its lowest level for over five years.

Recognised Qualifying Bodies (RQBs)

There are six bodies9 in the UK recognised to offer the audit qualification in line with the requirements of Schedule 11 to the Companies Act

- RQBs must have rules and arrangements in place to register students and track their progress, administer examinations and ensure that appropriate training is given to students in an approved environment.

Table 17 below shows the number of students registered with each RQB14 as at 31 December 2010 and 2012, and shows the number of members who were awarded the audit qualification and the number of students following the audit route or eligible for the audit qualification.

| ACCA | ICAEW | CAI | ICAS | AIA | ||

|---|---|---|---|---|---|---|

| 2010 | 91,690 | 14,510 | 5,771 | 2,962 | 151 | |

| Number of students in the UK and ROI | 2011 | 89,220 | 15,014 | 6,348 | 2,994 | 155 |

| 2012 | 84,058 | 15,321 | 6,265 | 3,056 | 185 | |

| 2010 | 98 | 1,020 | 846 | 29 | 0 | |

| The number of members who were awarded the audit qualification | 2011 | 106 | 25,73015 | 800 | 980 | 0 |

| 2012 | 147 | 484 | 671 | 1,209 | 0 | |

| 2010 | N/A16 | 9,432 | 4,114 | N/A | 1 | |

| Number of students following the audit route or eligible for the audit qualification | 2011 | N/A | 13,258 | 3,925 | N/A | 8 |

| 2012 | N/A | 13,332 | 4,332 | N/A | 9 |

Table 17

- Please note many members do not apply for the audit qualification until they wish to be able to sign audit reports. In addition, due to the rise in the audit threshold and the reduction in the availability of audit work, fewer students are able to meet the practical training requirements to be awarded this qualification.

Section Six – Audit Firms

Introductory Note: Major Audit Firms

This information has been provided on a voluntary basis and we would like to thank all the firms who responded to our requests. Some of this information is otherwise publicly available – for example those firms which are LLPs must file accounts at Companies Act 2006 which meet the statutory requirements. Table 18 shows the fee income for audit and non-audit services for 36 of the largest registered audit firms for the year ended

- Most of these have clients who are UK public interest entities. Firms are listed in order of fee income from audit, rather than total fee income. For the first time this year we include information on the percentage of principals who are female.

Table 18 also indicates those firms with audit clients whose securities are traded on a UK regulated market17 and must therefore publish a transparency report each year, in accordance with the requirements of the Statutory Auditors (Transparency) Instrument. The 21 audit firms in the table required to publish18 such as report have all done so in respect of their 2012 year ends.

Table 18 should not be seen as a league table. Not all the firms we approached were willing to disclose information on fee income or considered that they could provide sufficiently reliable information in the desired form. It is likely therefore that there are firms not included in the tables that have a higher audit fee income than some of those that are shown. Also, we have not included accountancy firms that are not registered as statutory auditors. Care is needed to make detailed comparisons between firms using the information in Table

- Some firms do not analyse their fee income in this manner and have made an informed estimate of the figures. In addition, firms may classify their audit and non-audit income in slightly different ways.

Charts 16 and 17 analyse the detailed fee income from Table 18 for the Big Four firms and for many of the larger firms outside of the Big Four respectively19.

- The percentage of fee income derived from non-audit clients has been rising steadily over the past five years for both the Big Four and for many of the larger firms outside of the Big Four. This is mirrored by a slow decrease in the proportion of fee income from non-audit work for audit clients.

- The percentage of total fee income derived from audit work has remained fairly steady.

UK FEE INCOME OF MANY OF THE LARGER REGISTERED AUDIT FIRMS - YEAR ENDED 2012 (By fee income from audit)

| UK Firm Name | UK Structure | Year End | No of Principals20 | % of Female Principals | No of Audit Principals | No of Responsible Individuals21 | Fee Income: Audit22 (£m) | Fee Income: Non-Audit Work23 to Audit Clients (£m) | Fee Income: Non-Audit Clients (£m) | Total Fee Income (£m) |

|---|---|---|---|---|---|---|---|---|---|---|

| PricewaterhouseCoopers | LLP | 30-Jun-12 | 872 | 14% | 212 | 366 | 570 | 348 | 1,493 | 2,411 |

| Deloitte24 | LLP | 31-May-12 | 715 | 15% | 180 | 210 | 466 | 173 | 1,479 | 2,118 |

| KPMG25 | LLP | 30-Sep-12 | 602 | 14% | 154 | 256 | 431 | 316 | 1,027 | 1,774 |

| Ernst & Young | LLP | 30-Jun-12 | 549 | 16% | 107 | 169 | 318 | 218 | 1,095 | 1,631 |

| Grant Thornton | LLP | 30-Jun-12 | 209 | 12% | 70 | 160 | 102 | 47 | 268 | 417 |

| BDO26 | LLP | 30-Jun-12 | 193 | 10% | 64 | 84 | 91 | 43 | 137 | 271 |

| Baker Tilly27 | LLP | 31-Mar-12 | 240 | 15% | 98 | 108 | 51 | 27 | 91 | 169 |

| Mazars | LLP | 31-Aug-12 | 116 | 11% | 50 | 53 | 41 | 16 | 58 | 115 |

| PKF (UK) | LLP | 31-Mar-12 | 70 | 8% | 33 | 47 | 33 | 13 | 57 | 103 |

| RSM Tenon Audit | Company | 30-Jun-12 | 5 | 19% | 5 | 70 | 28 | 0 | 0 | 28 |

| Crowe Clark Whitehill | LLP | 31-Mar-12 | 74 | 19% | 46 | 47 | 23 | 8 | 22 | 53 |

| Kingston Smith | LLP | 30-Apr-12 | 54 | 20% | 47 | 47 | 13 | 8 | 12 | 33 |

| Nexia Smith & Williamson Audit | Company | 30-Apr-12 | 36 | 11% | 27 | 26 | 13 | N/A28 | 46 | 59 |

| Moore Stephens | LLP | 30-Apr-12 | 61 | 15% | 29 | 29 | 12 | 4 | 47 | 63 |

| UHY Hacker Young | Group of Partnerships | 30-Apr-12 | 103 | 11% | 59 | 62 | 11 | 5 | 33 | 49 |

| MHA MacIntyre Hudson | LLP | 31-Mar-12 | 42 | --%29 | 20 | 39 | 11 | N/A | N/A | 35 |

| Haysmacintyre | Partnership | 31-Mar-12 | 25 | 24% | 20 | 20 | 9 | 4 | 4 | 17 |

| Saffery Champness | Partnership | 31-Mar-12 | 52 | 21% | 32 | 33 | 9 | 6 | 24 | 39 |

| Haines Watts Group | Group of Partnerships30 | 31-Mar-12 | 165 | 10% | 86 | 88 | 9 | 7 | 46 | 62 |

| Buzzacott | LLP | 30-Sept-12 | 29 | 14% | 12 | 12 | 8 | 2 | 15 | 25 |

| Chantrey Vellacott DFK | LLP | 30-Jun-12 | 44 | 6% | 19 | 19 | 8 | 2 | 17 | 27 |

| Littlejohn | LLP | 31-May-12 | 31 | 16% | 21 | 21 | 6 | 3 | 7 | 16 |

| Menzies | LLP | 31-Mar-12 | 35 | 6% | 20 | 20 | 6 | 6 | 14 | 26 |

| Scott Moncrieff | Partnership | 30-Apr-12 | 16 | 13% | 7 | 8 | 5 | 2 | 6 | 13 |

| Anderson Anderson & Brown | LLP | 31-Mar-12 | 12 | 25% | 5 | 5 | 4 | 3 | 7 | 14 |

| Reeves & Co | LLP | 31-May-12 | 40 | 13% | 16 | 16 | 4 | 2 | 14 | 20 |

| Johnston Carmichael | LLP | 31-May-12 | 47 | 6% | 11 | 18 | 4 | N/A | N/A | 27 |

| Cooper Parry | LLP | 30-Apr-12 | 23 | 4% | 10 | 12 | 4 | 5 | 6 | 15 |

| James Cowper | LLP | 30-Apr-12 | 13 | 23% | 7 | 8 | 3 | 2 | 6 | 11 |

Table 18

| UK Firm Name | UK Structure | Year End | No of Principals32 | % of Female Principals | No of Audit Principals | No of Responsible Individuals33 | Fee Income: Audit34 (£m) | Fee Income: Non-Audit Work34 to Audit Clients (£m) | Fee Income: Non-Audit Clients (£m) | Total Fee Income (£m) |

|---|---|---|---|---|---|---|---|---|---|---|

| Francis Clark | LLP | 31-Mar-12 | 46 | 5% | 23 | 24 | 3 | N/A | N/A | 21 |

| Bishop Fleming | Partnership | 31-May-12 | 25 | 3% | 15 | 16 | 3 | 1 | 9 | 13 |

| Montpelier Audit Ltd35 | Limited Company | 31-Dec-12 | 18 | 27% | 7 | 10 | 2 | N/A | N/A | 10 |

| Mercer & Hole | Partnership | 30-Sep-12 | 19 | 21% | 9 | 9 | 2 | N/A | 8 | 10 |

| Armstrong Watson | Partnership | 31-Mar-12 | 30 | 14% | 6 | 6 | 1 | 1 | 14 | 16 |

| Lovewell Blake | LLP | 30-Sep-12 | 26 | 8% | 10 | 10 | 1 | 1 | 12 | 14 |

| Chiene & Tait | Scottish Partnership | 30-Sep-12 | 8 | 13% | 3 | 3 | 1 | 0 | 5 | 6 |

Table 18

Analysis of Big Four Fee Income (2008 - 2012)

Bar chart showing percentages for Audit Fee Income, Fee Income from Non-Audit work to Audit Clients, and Fee income from Non-Audit Clients from 2008 to 2012.

- 2008: Audit Fee Income 24%, Fee Income from Non-Audit work to Audit Clients 17%, Fee income from Non-Audit Clients 59%

- 2009: Audit Fee Income 24%, Fee Income from Non-Audit work to Audit Clients 16%, Fee income from Non-Audit Clients 60%

- 2010: Audit Fee Income 24%, Fee Income from Non-Audit work to Audit Clients 15%, Fee income from Non-Audit Clients 61%

- 2011: Audit Fee Income 23%, Fee Income from Non-Audit work to Audit Clients 14%, Fee income from Non-Audit Clients 63%

- 2012: Audit Fee Income 23%, Fee Income from Non-Audit work to Audit Clients 13%, Fee income from Non-Audit Clients 64%

Chart 16

Analysis of the Fee Income (2008-2012) of many of the larger registered audit firms outside of the Big Four

Bar chart showing percentages for Audit Fee Income, Fee Income from Non-Audit work to Audit Clients, and Fee income from Non-Audit Clients from 2008 to 2012.

- 2008: Audit Fee Income 31%, Fee Income from Non-Audit work to Audit Clients 16%, Fee income from Non-Audit Clients 54%

- 2009: Audit Fee Income 33%, Fee Income from Non-Audit work to Audit Clients 15%, Fee income from Non-Audit Clients 53%

- 2010: Audit Fee Income 33%, Fee Income from Non-Audit work to Audit Clients 14%, Fee income from Non-Audit Clients 53%

- 2011: Audit Fee Income 31%, Fee Income from Non-Audit work to Audit Clients 14%, Fee income from Non-Audit Clients 51%

- 2012: Audit Fee Income 30%, Fee Income from Non-Audit work to Audit Clients 13%, Fee income from Non-Audit Clients 57%

Chart 17

1The figures for 2011 have been restated and are different from those shown in the tenth edition of Key Facts and Trends.

Growth of Fee Income

Table 1936 shows the percentage growth rate of fee income for each of the years from 2007/08 to 2011/12 for many of the largest registered audit firms, split between the Big Four audit firms, the larger firms outside of the Big Four and between audit and non-audit income.

To ensure consistency in the table below, we have only included income figures for firms that have submitted data for all five years for both audit and non-audit income37.

| Growth Rate % | 2011-12 | 2010-11 | 2009-10 | 2008-9 | 2007-8 |

|---|---|---|---|---|---|

| Big Four Firms | 7.7 | 5.7 | -1.3 | 0.4 | 4.4 |

| Total fee income | |||||

| Non Big Four Firms | 0.6 | -0.5 | -7.0 | -1.9 | 7.6 |

| Big Four Firms | 4.9 | 0.9 | -2.2 | 1.2 | 0.9 |

| Audit fee income | |||||

| Non Big Four Firms | -5.0 | -2.2 | -6.9 | 0.5 | 8.1 |

| Non-audit work to Audit Clients Fee Income | Big Four Firms | 1.9 | -1.8 | -5.7 | -6.2 |

| Non Big Four Firms | -7.5 | -0.5 | -11.7 | -7.2 | 6.3 |

| Non-audit work to Non-Audit Clients fee income | Big Four Firms | 10.0 | 9.4 | 0.2 | 1.9 |

| Non Big Four Firms | 5.9 | 0.6 | -5.6 | -1.8 | 9.4 |

Table 19

- Whilst the percentage of total fee income for the Big Four has increased by 7.7% this year also shows an average increase of 0.6% for the larger registered firms outside of the Big Four in 2011-12.

- This is the first year for some time that there has been a marked increase in audit fee income for the Big Four firms, although audit fee income from for many of the larger registered firms outside of the Big Four firms continues to decline.

- There has been a small increase in non-audit fee income to audit clients generated by the Big Four firms.

Audit Fee Income per Responsible Individual

Table 2038 illustrates audit fee generated per Responsible Individual (RI)39 for 2008 to 2012 (inclusive). This information is split further between the Big Four firms and the largest firms outside of the Big Four.

| Audit Fee Income Per RI (£m) | 2012 | 2011 | 2010 | 2009 | 2008 |

|---|---|---|---|---|---|

| Largest registered audit firms | 1.11 | 1.07 | 1.06 | 1.05 | 0.99 |

| Big Four Firms | 1.78 | 1.67 | 1.65 | 1.60 | 1.54 |

| Non Big Four Firms | 0.48 | 0.50 | 0.50 | 0.51 | 0.48 |

Table 20

- The total fee income from audit per RI has seen an upward trend with 7% growth for the Big Four Firms and a small decrease for many of the larger registered firms outside of the Big Four in 2012.

- Audit fee income for many of the larger registered audit firms outside of the Big Four has remained largely static over the past 5 years.

CONCENTRATION OF LISTED COMPANIES' AUDITS - YEAR ENDED 2012

(By Number of Listed Clients – FTSE 100, FTSE 250, UK Equity Listed on Regulated Markets and AIM)

| UK Firm Name | UK Structure | Year End | No of FTSE 100 Audit Clients40 | No of FTSE 250 Audit Clients40 | Total No of Other Clients listed on Regulated Markets40 | No of AIM Audit Clients40 |

|---|---|---|---|---|---|---|

| PricewaterhouseCoopers | LLP | 30-Jun-12 | 40 | 62 | 210 | 108 |

| KPMG41 | LLP | 30-Sep-12 | 23 | 51 | 120 | 62 |

| Deloitte | LLP | 31-May-12 | 21 | 68 | 73 | 70 |

| Ernst & Young | LLP | 30-Jun-12 | 15 | 44 | 139 | 44 |

| BDO42 | LLP | 30-Jun-12 | 1 | 7 | 28 | 110 |

| Grant Thornton | LLP | 30-Jun-12 | 0 | 6 | 76 | 149 |

| PKF (UK)42 | LLP | 31-Mar-12 | 0 | 0 | 45 | 31 |

| Baker Tilly43 | LLP | 31-Mar-12 | 0 | 0 | 12 | 50 |

| James Cowper | LLP | 30-Apr-12 | 0 | 0 | 7 | 0 |

| Nexia Smith & Williamson Audit | Company | 30-Apr-12 | 0 | 0 | 4 | 29 |

| UHY Hacker Young | Group of Partnerships | 30-Apr-12 | 0 | 0 | 3 | 24 |

| Scott Moncrieff | Partnership | 30-Apr-12 | 0 | 0 | 3 | 3 |

| Chiene & Tait | Scottish Partnership | 30-Sep-12 | 0 | 0 | 3 | 0 |

| Chantrey Vellacott DFK | LLP | 30-Jun-12 | 0 | 0 | 3 | 12 |

| Moore Stephens | LLP | 30-Apr-12 | 0 | 0 | 3 | 6 |

| Mazars | LLP | 31-Aug-12 | 0 | 0 | 2 | 14 |

| Haysmacintyre | Partnership | 31-Mar-12 | 0 | 0 | 2 | 8 |

| Kingston Smith | LLP | 30-Apr-12 | 0 | 0 | 1 | 8 |

| Buzzacott | LLP | 30-Sept-12 | 0 | 0 | 1 | 0 |

| Saffery Champness | Partnership | 31-Mar-12 | 0 | 0 | 1 | 7 |

| Crowe Clark Whitehill | LLP | 31-Mar-12 | 0 | 0 | 1 | 29 |

| Armstrong Watson | Partnership | 31-Mar-12 | 0 | 0 | 1 | 0 |

| Menzies | LLP | 31-Mar-12 | 0 | 0 | 0 | 2 |

| Littlejohn | LLP | 31-May-12 | 0 | 0 | 0 | 14 |

| RSM Tenon Audit | Limited Company | 30-Jun-12 | 0 | 0 | 0 | 18 |

| Haines Watts Group | Group of Partnerships44 | 31-Mar-12 | 0 | 0 | 0 | 3 |

| MHA MacIntyre Hudson | LLP | 31-Mar-12 | 0 | 0 | 0 | 2 |

| Francis Clark | LLP | 31-Mar-12 | 0 | 0 | 0 | 2 |

| Reeves & Co | LLP | 31-May-12 | 0 | 0 | 0 | 3 |

Table 21

Concentration of listed Companies' Audits45

Table 22 illustrates the percentage of the number of audits undertaken by the Big Four firms46, the next six firms47 (based on the number of listed audit clients) and other audit firms, with UK equity listed companies as audit clients.

For the purposes of Table 22, where a listed company is audited by a firm from the Crown Dependencies it has been given the same classification as its UK counterparts.

| Big Four Firms (%)46 | Next Six Firms (%)47 | Other Firms (%) | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 31/12/12 | 31/12/11 | 31/12/10 | 31/12/09 | 31/12/12 | 31/12/11 | 31/12/10 | 31/12/09 | 31/12/12 | 31/12/11 | 31/12/10 | 31/12/09 | |

| FTSE 10045 | 99.0 | 99.0 | 99.0 | 99.0 | 1.0 | 1.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| FTSE 25045 | 94.4 | 95.2 | 95.6 | 94.8 | 5.6 | 4.8 | 4.4 | 4.4 | 0.0 | 0.0 | 0.0 | 0.8 |

| Other UK Main Market | 66.3 | 68.7 | 66.6 | 67.6 | 24.8 | 23.9 | 25.1 | 23.9 | 8.9 | 7.4 | 8.3 | 8.5 |

| All Main Market | 78.3 | 78.4 | 78.5 | 77.3 | 16.5 | 16.8 | 16.5 | 16.9 | 5.2 | 4.8 | 5.0 | 5.8 |

Table 22

Source: Audit Quality Review team

- There has been little change in the proportion of listed companies audited by many of the larger registered firms outside of the Big Four firms in recent years.

Audit Firms

Table 23 analyses fee income of audit firms by size using information either supplied to us by firms48 or from their annual returns for ICAEW registered firms (Please note that in some cases this date is different from the firm's year-end).

| Firms ranked by size | Average Total Fee Income (£'000) |

|---|---|

| 1 to 4 | 1,983,500 |

| 5 to 9 | 215,000 |

| 10 to 30 | 25,939 |

| 31 to 100 | 7,853 |

| 101 to 500 | 2,383 |

| 501 to 1000 | 1,014 |

| 1001 to 2000 | 490 |

| 2001 to 3000 | 186 |

| 3001 to 3886 | 28 |

Table 23

- Approximately 69% of the total fee income of audit firms is attributable to the Big Four. The information in Table 24 is only directly comparable with the figures shown in Table 18 for the largest 9 firms, which consolidate the income of all the entities through which the firm operates i.e. both audit registered entities and other entities.

Financial Reporting Council 5th Floor, Aldwych House 71-91 Aldwych London WC2B 4HN +44 (0)20 7492 2300 www.frc.org.uk

-

Association of Authorised Public Accountants (AAPA) (subsidiary of the ACCA) Association of Chartered Certified Accountants (ACCA) Institute of Chartered Accountants in England & Wales (ICAEW) Chartered Accountants Ireland (CAI) Institute of Chartered Accountants of Scotland (ICAS) ↩↩

-

This information has been derived from previous editions of Key Facts and Trends in the Accountancy Profession. ↩↩

-

See 'Statistical Tables on Companies Registration Activities 2011-12' which can be found on the Companies House website. ↩↩↩↩↩↩

-

Includes the figures for the AAPA, a subsidiary of the ACCA. The ACCA 2012 figures include 225 firms with no audits, monitored in most cases using a desktop questionnaire. ↩↩↩↩

-

Cases passed to the committee relate to: A) the Disciplinary Committee for the ACCA; B) Cases considered by the Investigations Committee and referred to the Disciplinary Committee for the ICAEW; C) the Complaints Committee, Disciplinary Committee and Appeal Committee for the CAI; and D) the Investigation Committee at ICAS. ↩↩

-

The Chartered Accountants Regulatory Board (CARB) is responsible for handling complaints about all members of the CAI, including audit-related complaints, in accordance with the CAI Bye-laws. ↩↩

-

Additional cases (5 in 2010, 1 in 2011 & 2 in 2012) have been passed to the Professional Discipline team (PD) after consultation between PD and the ICAEW. ↩↩↩

-

Association of Chartered Certified Accountants (ACCA) Association of International Accountants (AIA) Chartered Institute of Public Finance and Accountancy (CIPFA) Institute of Chartered Accountants in England and Wales (ICAEW) Chartered Accountants Ireland (CAI) Institute of Chartered Accountants of Scotland (ICAS) ↩

-

Audit Quality Review (AQR), is a part of the Financial Reporting Council. ↩

-

The bodies visit firms with public interest entities which are outside of the scope of the AQR. ↩

-

Audit related complaints only ↩

-

Audit related cases only ↩

-

Due to CIPFA's RQB status being in abeyance they have not provided the figures for Table 17 and we have therefore removed them from this table going forward. ↩

-

25,011 of those awarded in 2011 were awarded the audit qualification automatically, of which 626 were subsequently withdrawn in 2012. The figure for 2011 shows all those awarded, including those that were withdrawn. ↩

-

Where N/A is stated the information is not collected by the body. ↩

-

In most cases the LSE Main Market ↩

-

Available on each firm's website ↩

-

Information on fee income by audit for earlier years can be found in previous editions of Key Facts and Trends in the Accountancy Profession, available at www.frc.org.uk - Key Facts and Trends ↩

-

Principals are partners or members of an LLP ↩

-

RIs are those individuals who are able to sign audit reports and includes Audit Principals and Employees ↩

-

The definition used of 'audit-services' and 'non-audit services' is set out in paragraphs 6, 9 and 12 of the Auditing Practices Board's 'Ethical Standard 5' - updated in December 2011 ↩

-

The definition used of 'audit-services' and 'non-audit services' is set out in paragraphs 6, 9 and 12 of the Auditing Practices Board's 'Ethical Standard 5' - updated in December 2011 ↩

-

Deloitte LLP figures for 2012 relate to practising activities in the UK, Channel Islands and Isle of Man only. ↩

-

Includes both KPMG LLP and KPMG Audit Plc ↩

-

PKF merged with BDO on 31 March 2013. The figures above relate to the period before the merger. ↩

-

Includes both Baker Tilly and Baker Tilly UK Holdings Ltd ↩

-

Where N/A is stated we are told that the information is not available. ↩

-

MHA Macintyre Hudson declined to provide us with this information. ↩

-

Haines Watts Group changed from a Partnership to a Group of Partnerships. ↩

-

The figures stated for Montpelier Audit Ltd are the unaudited figures. ↩

-

Refers to "No of Principals". ↩

-

Refers to "No of Responsible Individuals". ↩

-

Refers to "Fee Income: Audit" and "Fee Income: Non-Audit Work". ↩↩

-

The figures stated for Montpelier Audit Ltd are the unaudited figures. ↩

-

This information is based on the information provided to the FRC and which is shown in the detailed tables on fee income of major audit firms. ↩

-

The data will be different in some cases from that published in earlier versions of Key Facts and Trends in the Accountancy Profession, due to figures being restated for previous years by the firms. ↩

-

The historic information in this table has been updated as a result of changes in a number of submissions made by some of the larger registered audit firms outside of the Big Four. ↩

-

RIs have been awarded the recognised professional qualification in audit and hold a practising certificate. An RI can sign an audit report on behalf of his/her firm. ↩

-

The number of clients reported relates to entities whether incorporated in the UK or elsewhere that are audit clients of the UK firm. The figures for 'Other clients listed on Regulated Markets' include clients which have equity listed on one or more regulated markets. ↩↩↩↩

-

Includes both KPMG LLP and KPMG Audit Plc ↩

-

PKF merged with BDO on 31 March 2013. The figures above relate to the period before the merger. ↩↩

-

Includes both Baker Tilly and Baker Tilly UK Holdings Ltd ↩

-

Haines Watts Group changed from a Partnership to a Group of Partnerships. ↩

-

Includes Big Four network firm offices in the Crown Dependencies of the Isle of Man and the Channel Islands. ↩↩

-

The data for 2011 and 2012 is for the next six firms instead of the next five. The data for previous years in this section has not been restated so is not entirely comparable. ↩↩

-

Information for the largest 9 firms is drawn from information supplied to us by the firms. The remaining information relates only to those firms registered with the ICAEW. ↩