The content on this page has been converted from PDF to HTML format using an artificial intelligence (AI) tool as part of our ongoing efforts to improve accessibility and usability of our publications. Note:

- No human verification has been conducted of the converted content.

- While we strive for accuracy errors or omissions may exist.

- This content is provided for informational purposes only and should not be relied upon as a definitive or authoritative source.

- For the official and verified version of the publication, refer to the original PDF document.

If you identify any inaccuracies or have concerns about the content, please contact us at [email protected].

The influence of proxy advisors and ESG rating agencies on the actions and reporting of FTSE 350 com

Copyright © The Financial Reporting Council Limited 2023 The Financial Reporting Council Limited is a company limited by guarantee. Registered in England number 2486368. Registered Office: 8th Floor, 125 London Wall, London EC2Y 5AS

Liability No party accepts any liability for any loss damage or costs howsoever arising, whether directly or indirectly, whether in contract, tort or otherwise from any action or decision taken (or not taken) as a result of any person relying on or otherwise using this publication or arising from any omission from it.

- I. INTRODUCTION

- II. EXECUTIVE SUMMARY

- III. PROXY VOTING RESEARCH

- Footnotes

- INVESTORS' USE OF VOTING POLICIES

- IMPACT ON COMPANIES' BEHAVIOUR

- HOW PROXY ADVISORS DEVELOP VOTING POLICIES

- COMPANY VIEWS AND BEHAVIOURS

- HOW PROXY ADVISORS DEVELOP AND APPLY POLICIES

- HOW INVESTORS USE VOTING RESEARCH

- OTHER INPUTS TO INVESTOR VOTING POLICIES AND DECISIONS

- INVESTORS' DECISION-MAKING PROCESSES

- VOTING ANALYSIS

- ANALYSIS OF VOTING OUTCOMES

- ENGAGEMENT DURING THE AGM SEASON

- INTRODUCTION

- CONTEXT

- THE ABILITY TO REVIEW DRAFT RESEARCH REPORTS

- TIME AVAILABLE FOR COMMENT

- THE ACCURACY AND BALANCE OF RESEARCH REPORTS

- FACTUAL ERRORS IN RESEARCH REPORTS

- BALANCE ON RESEARCH REPORTS

- ENGAGEMENT ON DRAFT RESEARCH REPORTS

- DIRECT ENGAGEMENT BETWEEN COMPANIES AND PROXY ADVISORS

- DIRECT ENGAGEMENT BETWEEN COMPANIES AND PROXY ADVISORS

- ENGAGEMENT BETWEEN COMPANIES AND INVESTORS

- NOTIFICATION OF VOTING INTENTION

- ENGAGEMENT OUTSIDE THE AGM SEASON

- OTHER ISSUES

- IV. ESG RESEARCH AND RATINGS

- IMPACT ON COMPANIES OF ESG RESEARCH AND RATING AGENCIES

- HOW INVESTORS USE ESG RESEARCH TO SUPPORT STEWARDSHIP

- CONCERNS RAISED BY COMPANIES AND INVESTORS

- OVERALL VIEWS ON QUALITY OF ESG RATING AGENCIES' RESEARCH

- TRANSPARENCY OF METHODOLOGIES

- HOW TRANSPARENCY COULD BE IMPROVED

- USE AND RELEVANCE OF ESG METRICS AND DATA POINTS

- DATA GATHERING ISSUES - COMPANY DISCLOSURES

- DATA GATHERING ISSUES - CONTROVERSY REPORTS

- RESPONSIVENESS OF ESG RATING AGENCIES

- TIMELINESS

- OTHER ISSUES

- APPENDIX A: METHODOLOGY

- ETHICAL CONSIDERATIONS

- APPENDIX B: LIST OF SOURCES

I. INTRODUCTION

1In August 2022 the Financial Reporting Council (FRC) commissioned independent research to better understand the influence and impact of proxy voting advisors and ESG rating agencies on actions and reporting by FTSE 350 companies and on investors (asset managers and asset owners). This report presents the findings of the project carried out for the FRC by a team of researchers from Morrow Sodali (including its subsidiary Nestor Advisors) and Durham University Business School.

2When commissioning the research, the FRC asked these questions:

2.1What are the impacts of recommendations/ratings given by proxy voting/ESG rating agencies on FTSE 350 companies' behaviour and reporting, and investor voting decisions? This should include the impact on governance policies and practices, and on so-called ‘tick box' behaviour.

2.2What have been the processes and outcomes of engagement over the last two years among FTSE 350 companies, investors, and proxy voting/ESG rating agencies? We are interested in three types of bilateral engagement:

2.2.1Between FTSE 350 companies and proxy voting/ESG rating agencies on recommendations/ratings given by the latter;

2.2.2Between investors and proxy voting/ESG rating agencies on recommendations/ratings given by the latter; and

2.2.3Between investors and FTSE 350 companies on recommendations/rating given by proxy voting/ESG rating agencies.

3Answering these questions is not a straightforward task. There are many different factors that influence the behaviour of companies and investors and the decisions that they take – not least resource constraints and the deadlines to which they have to work during the AGM season – and there is considerable variety in the policies that they apply and their working practices.

4Recommendations and ratings given by proxy advisors and ESG rating agencies undoubtedly have some influence on behaviour and voting decisions. However, our analysis of voting patterns and interviews with investors suggests that the nature and extent of this influence may be more nuanced and less clearcut than is believed to be the case by many companies, stakeholders and other commentators.

5For many companies, their perceptions of the influence that proxy advisors and ESG rating agencies have over investors in turn influences their own behaviour and affects the nature and tenor of engagement between the different parties. With this in mind, this Report aims to reflect the full range of perspectives that we heard from companies, investors, proxy advisors and ESG rating agencies during the course of our research.

6In order to answer the FRC’s questions, between October 2022 and March 2023 the research team: 1

6.1Obtained and analysed survey responses received from 48 companies, 32 investors and eight proxy advisors and ESG rating agencies;

6.2Conducted in-depth interviews with 13 companies, 14 investors, and five proxy advisors and three ESG rating agencies;

6.3Held three roundtable discussions with 55 representatives of companies and investors;

6.4Examined resolutions on board appointments and remuneration from 2022 FTSE 350 AGMs on which either or both Institutional Shareholder Services (ISS) and Glass Lewis – as the two proxy advisors with the largest client bases – recommended voting against, reviewing the voting outcomes and how a representative sample of 38 investors voted in those resolutions.

7Morrow Sodali and Durham University Business School are grateful to everyone who participated in the surveys, interviews, and roundtables. We would also like to thank the Chartered Governance Institute and GC100 for facilitating the company survey, the GC100 again for helping to organise one of the roundtables, and Minerva Analytics for providing some of the data used in the voting analysis.

Acknowledgements

Dr. Anna Tilba, Associate Professor in Strategy and Governance Durham University Business School

Chris Hodge, Senior Advisor Morrow Sodali Patrick McNamara, Manager

- Governance Morrow Sodali

Julian Green, Analyst – Governance Morrow Sodali

II. EXECUTIVE SUMMARY

During the course of the research some themes emerged that were common to both proxy advisors and ESG rating agencies, for example, the quality and timeliness of their research and the extent to which they were willing or able to take account of each company's specific circumstances.

However, there are also notable differences in the use made of the research by investors, the nature of the agencies' relationships with their investor clients and companies, and the structure of the markets for proxy voting and ESG research. For these reasons, this Report assesses the influence of proxy advisors separately from that of ESG rating agencies.

THE INFLUENCE OF PROXY ADVISORS

Voting decisions and outcomes

The first section of the Report looks at how investors use proxy voting research to inform their voting decisions and at voting outcomes where proxy advisors recommend a vote against, focusing on board appointments and remuneration. The aim was to test the validity of the accusation that many investors will automatically follow the voting recommendations of their chosen proxy advisor.

While almost all investors use the services of proxy advisors, an increasing number of them ask for voting research to be based on the investor's own in-house voting policies (known as customised policies) rather than the advisor's standard policies (known as benchmark policies) – 75% of those investors that responded to the survey stated that they do so.

Due to limited resources, most investors will issue voting instructions based on recommendations from proxy advisors without manual intervention where the resolution is uncontroversial. All investor interviewees said that they always review recommendations to vote against management and other resolutions that met certain criteria. For example, all companies above a certain size or in which they own more than a certain percentage of the shares, or with which they have previously engaged about governance concerns.

While there is some evidence of correlation between negative voting recommendations and voting outcomes in FTSE 350 companies, it appears to be less extensive than is sometimes asserted. A vote of 20% or more against a resolution relating to director elections or remuneration occurred in only half of the cases where one or both of ISS or Glass Lewis had made such a recommendation in 2022, although this increased to 77% of cases when both did so.

There do not appear to be many notable differences in voting behaviour based on the size of the investor or the choice of proxy advisor. However, comparing investors with UK-based teams to those without UK-based teams, a much higher proportion of the latter voted in line with their proxy advisor on more than 50% of resolutions. There is a similar pattern when comparing asset owners and asset managers.

With the notable exception of remuneration, recommendations by the largest proxy advisors to vote against resolutions are relatively rare on most topics. For example, only 1.2% of all board appointment resolutions in FTSE 350 companies in 2022 attracted a vote against recommendation from one or both of ISS or Glass Lewis. By contrast, 14.6% of remuneration resolutions attracted a vote against recommendation.

Engagement during the AGM season

There can be considerable variation in the position taken by ISS and Glass Lewis on remuneration and director appointments. In two-thirds of cases where one recommended a vote against in 2022, the other took the opposite position.

Many company interviewees considered that proxy advisor methodologies should be aligned to the UK Corporate Governance Code (the Code) to increase consistency. All proxy advisor interviewees stated that the Code is one of the main sources for their UK benchmark policy. However, there are a few topics on which benchmark policies are more specific than the Code and other UK regulatory requirements and standards.

This section of the Report also looks at how companies' perceptions of the extent of proxy advisors' influence on the likely voting outcomes affects their own behaviour. Some company interviewees stated that they had changed proposals purely in order to avoid receiving a recommendation to vote against from proxy advisors on at least one occasion, but only in relation to what they considered to be non-strategic issues.

During the AGM season, companies, investors and proxy advisors are all working under pressure, with time and resources at a premium. There can be as few as 14 calendar days between AGM papers being sent by companies to shareholders and the shareholders having to submit their voting instructions; and a large number of AGMs take place in a short period of time, increasing the pressure on investors and proxy advisors.

Perhaps inevitably, these conditions contribute to frustrations on all sides about the effectiveness of the process, the behaviour of the other parties and, on companies' part, to concerns that their AGM resolutions may not get the level of attention from proxy advisors and investors that they deserve.

Companies value the opportunity to comment on draft research reports produced by proxy advisors for their investor clients to ensure they are balanced and factually accurate. Proxy advisors have adopted different policies – some provide an opportunity to comment in all cases, others only in certain circumstances, and others not all. All companies considered that they should have a mandatory right to comment on draft research reports. Only 56% of investor respondents thought that companies should have this right.

The majority of proxy advisors will not usually engage face-to-face with companies during the AGM season, with most citing time and resource constraints as the main reason. Many investors take the same position for the same reasons. In addition, the majority of investors do not notify companies of their intention to vote against a resolution in advance of doing so.

There was no consensus between companies and investors on the quality of the research reports prepared by proxy advisors. Nearly half of companies that responded to the survey said that they were dissatisfied, compared to only 6% of investors.

Engagement outside the AGM season

Many companies will seek to engage with proxy advisors and major shareholders when considering changes to their governance policies and structures. Because of the constraints described above, this engagement typically takes place in advance of the AGM season.

Just over 60% of companies that responded to the survey had attempted to engage with one or more proxy advisor in advance of the AGM season in the previous two years. Of these companies, 96% had engaged on remuneration, compared to 23% on both board composition and ESG issues.

There was a notable difference in the percentage of FTSE 100 companies that had attempted to engage with proxy advisors (68%) compared to FTSE 250 companies (50%). The reason for this difference is not clear.

Companies and proxy advisors had different views on the purpose of engagement in advance of the AGM season. Many companies sought to obtain an indication of whether or not the proxy advisor would recommend voting in favour of the company's proposals, whereas proxy advisors viewed it purely as an opportunity to exchange information.

Interviews with company and investor representatives suggest that there can often be a mismatch between a company's desire to engage with its major shareholders and those shareholders' willingness or ability to do so. Some company interviewees suggested that when investors were unwilling or unable to engage, this contributed to the perception on the part of companies, that those investors were not active stewards and may have delegated their voting decisions to proxy advisors.

Evidence suggests that the ability of companies to engage with their major shareholders may be related to the size of the company and the composition of its share register. Investor interviewees stated that their decision on which companies to engage with were primarily driven by their own priorities rather than in response to requests from companies.

THE INFLUENCE OF ESG RATING AGENCIES

Most companies stated that the fear of receiving an adverse ESG rating was not a significant consideration when the company was setting the strategy and developing action plans to address ESG-related issues.

However, they were concerned that investors may place reliance on the headline ratings when making voting decisions, and that the potential existed for the company to be penalised on the basis of a rating that, in their opinion, did not fairly reflect the company's actions or performance. For this reason, the majority of company interviewees concluded that they needed to 'play the game' by providing the information used by ESG rating agencies in their methodologies, in the hope that they would receive a positive rating.

Most investors stated that they primarily used ESG rating agencies as a source of data rather than relying on the rating itself to inform voting decisions; and some have developed their own proprietary rating systems. However, some investors acknowledged that their clients may place more weight on the headline ratings from the rating agencies than they do themselves.

There are many ESG data providers and rating agencies operating in the UK market. This means there are considerable differences in terms of the reliability of the research and the approach taken to collecting and interpreting data, as well as the particular data points that are used. This can have a significant impact on the volume of data that companies measure and publish and the associated resources.

Both companies and investors would welcome greater transparency on the methodologies used by ESG rating agencies including, for example, more information on the specific ESG factors covered and how they are weighted, the extent to which the model takes account of national and sectoral differences, and the quality assurance process. The code of conduct being developed by the FCA and an industry working group may address some of these issues.

Companies identified a number of concerns about the data-gathering techniques used by some ESG rating agencies and data providers, in particular the use of 'data scraping' and controversy reports (reports on ESG-related incidents involving the company).

In addition, both companies and some investors raised concerns about the timeliness and timing of ESG rating agencies' updates to their ratings and research reports. These do not always align with reporting and voting cycles, meaning that the information on which investors draw when making decisions may be out-of-date.

III. PROXY VOTING RESEARCH

8This chapter of the Report dealing with proxy voting research has been divided into four sections. The first section provides an overview of the market for voting research and the regulatory framework within which proxy advisors operate.

9The second section assesses the impact of this research on voting outcomes. It covers how proxy advisors develop their voting policies and recommendations, how those are used by investors, and the perceptions and behaviour of FTSE 350 companies. This section concludes with an analysis of voting activity in the 2022 AGM season to assess the extent to which there is a correlation between proxy advisors' recommendations and voting outcomes.

10The third section addresses engagement between companies, investors, and proxy advisors in the period between companies issuing their AGM papers and the voting deadline, with a particular focus on the content of the research reports issued by proxy advisors and companies' ability to comment on them. The final section elaborates on the extent and nature of engagement between the different parties outside the AGM season, the period during which companies will be developing the policies and proposals on which they will ultimately seek shareholder approval.

11Key research insights on each of these topics can be found at the beginning of the second, third and fourth sections.

MARKET OVERVIEW

CONTEXT

12Proxy advisors provide research and advice to shareholders and their intermediaries, including recommendations on how to vote in the general meetings of listed companies. The services offered by proxy advisors are increasingly used by investors as a source to inform and implement voting decisions. According to the research commissioned by the FRC, 47% of asset managers outsource proxy vote management and administration – the most frequently outsourced stewardship activity – and 27% outsource all proxy governance research. 2 As a result, proxy advisors have come under increasing scrutiny and criticism, in particular from companies, for their perceived influence over voting outcomes.

13Proxy advisors offer a variety of research and voting services. The main services include voting research, voting platforms for clients to manage votes, vote processing, and in some cases ESG data research. Most proxy advisors operating in the UK, but not all of them, have a standard voting policy (known as a benchmark policy) which they will use when assessing a company's governance and when making voting recommendation to their clients. Some proxy advisors also offer 'specialty' research and voting policies which vary from the benchmark policy in certain respects, usually in relation to one or more aspects of ESG. In addition, almost all proxy advisors will provide customised research and recommendations using the client's own policy.

SUMMARY OF PROVIDERS

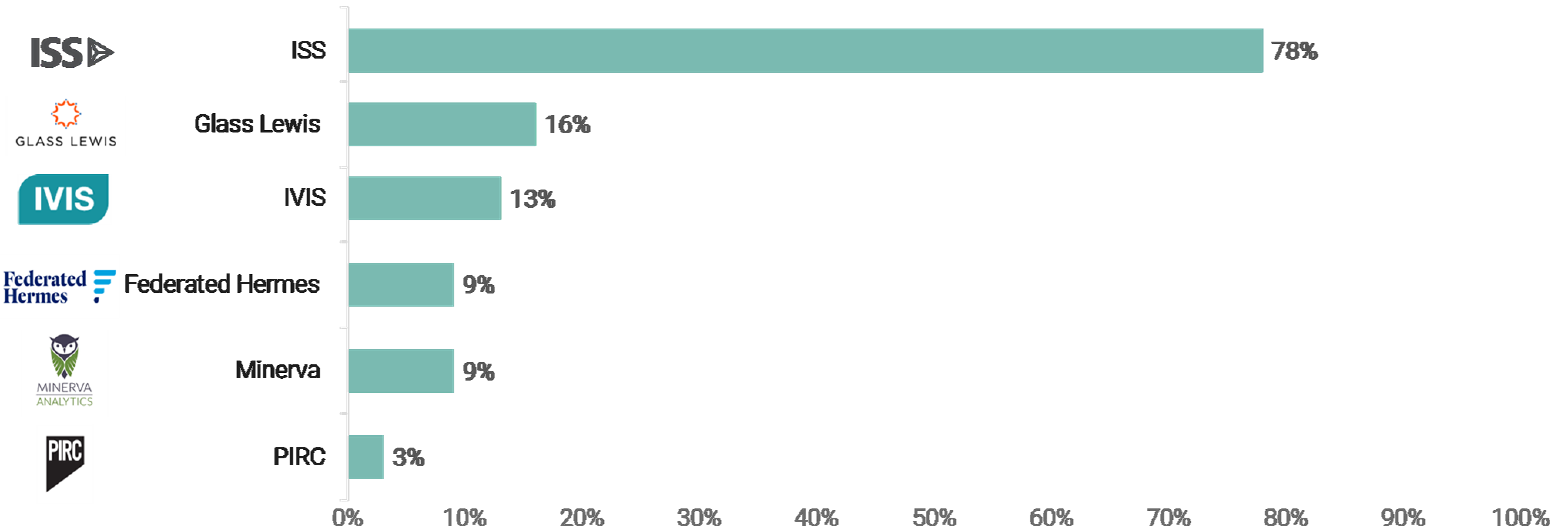

14In the UK, there are six proxy advisors: 3 Glass Lewis, Institutional Shareholder Services (ISS), Minerva Analytics, Pensions & Investment Research Consultants (PIRC), Institutional Voting Information Service (IVIS), and Federated Hermes EOS. Proxy research is the primary service provided by the first five, although some offer other services to investors and in some cases companies as well (see paragraph 227), including voting platforms for clients to manage votes, vote processing, and ESG data research. Federated Hermes EOS offers proxy services as part of its broader engagement overlay service, and neither it nor IVIS provide a voting platform for clients. In addition, Sustainalytics offers a limited proxy advisory service on ESG resolutions only.

15ISS has the largest market presence. As shown in Exhibit 1, three-quarters of the investors that responded to the survey stated that they used ISS for voting research, but not exclusively in all cases. In total, 31% of investor survey participants indicated they use more than one proxy advisor.

|

16Proxy advisors can be differentiated to a degree according to their client base in terms of their location and type of investor. For example, approximately 76% of Glass Lewis' clients are based in the Americas 4 while ISS maintains a significant presence both globally and in the UK. In comparison 52% of IVIS' subscribers are Investment Association members, who are predominantly UK-based global asset managers. 5 The majority of ISS and Glass Lewis' proxy research clients are asset managers (65% in the case of Glass Lewis), while a significant proportion of Federated Hermes EOS' clients are asset owners. 6 Similarly, PIRC's client base leans towards asset owners, predominantly pension funds.

17Investors are the primary customers for proxy advisors. However, some proxy advisors also provide consulting services to companies.

REGULATORY FRAMEWORK

18In the UK, proxy advisors are regulated under The Proxy Advisors (Shareholders' Rights) Regulations 2019. 7 The regulations require proxy advisors to state whether they adhere to an identified code of conduct and to disclose certain prescribed information, for example, on their methodologies and voting policies, the sources of information they use, their quality assurance procedures, and how they manage conflicts of interest. The regulations are overseen by the Financial Conduct Authority (FCA).

19In addition to the regulations, the FRC's UK Stewardship Code (2020) 8 contains a set of 'apply and explain' Principles for service providers (including proxy advisors) covering their purpose, governance, conflicts of interest, the promotion of well-functioning financial markets, how they support their clients' stewardship and how they review and assure their internal policies and processes.

20Compliance with the UK Stewardship Code is not mandatory, but signatories are required to disclose on an annual basis how they have applied the principles. The majority of proxy advisors operating in the UK are currently signatories. [^9]

21In the final quarter of 2023, the FRC – working with the FCA, Department for Work and Pensions (DWP) and The Pensions Regulator – will review the regulatory framework for effective stewardship, including the operation of the Stewardship Code. The review will assess whether the Stewardship Code is creating a market for effective stewardship and the need for any further regulation in this area.

22The majority of proxy advisors are also signatories to the Best Practice Principles for Shareholder Voting Research (BPP). The BPP Group [^10] (BPPG) was formed in February 2013 by a collective of industry members to develop an industry code of conduct, and the principles were most recently revised in 2019. These three principles cover service quality, conflict of interest avoidance or management, and communications policy with signatories' compliance reviewed based on an apply-and-explain framework.

23In 2020, the Group established an independent Oversight Committee to provide an annual review of the BPP and the public compliance statements of each BPP Signatory and to provide oversight of the BPPG's complaints management procedure, including monitoring of outcomes of those procedures.

THE USE MADE OF PROXY VOTING RESEARCH

INTRODUCTION

24The FRC's first objective when commissioning this research project was to gain a better understanding of the impacts of recommendations given by proxy advisors on the behaviour of FTSE 350 companies and on investor voting decisions.

25This section starts by looking at how companies believe investors make use of the research and recommendations they receive from proxy advisors. It also considers the extent and manner in which companies take account of the perceived influence of proxy advisors when designing their own governance arrangements and policies. It then compares the views of companies with evidence received from investors and proxy advisors, including on the selection of the voting policy against which the proxy advisor provides recommendations, other inputs used by investors, and processes followed by investors when making voting decisions, and the use made by investors of proxy advisors' voting platforms.

26The section concludes with an analysis of voting behaviour in 2022 FTSE 350 AGMs, focusing primarily on a sample of resolutions on which one or both of ISS and Glass Lewis recommended voting against the resolution, in an attempt to identify whether there is an apparent correlation between those recommendations and the voting outcomes.

KEY INSIGHTS

INFLUENCE ON VOTING OUTCOMES An analysis was undertaken of the voting recommendations made by ISS and Glass Lewis – as the proxy advisors with the largest client base – on resolutions on board appointments and remuneration in FTSE 350 companies in

- These recommendations were compared with the actual voting outcomes and the voting activity of selected investors.

While there is some evidence of correlation between negative voting recommendations and voting outcomes in FTSE 350 companies, it appears to be less extensive than is sometimes asserted. A vote of 20% or more against a resolution relating to director elections or remuneration occurred in only half of the cases where one or both of ISS or Glass Lewis had made such a recommendation in 2022, although this increased to 77% of cases when both did so.

Only one of the 38 investors in our sample voted against resolutions in more than 75% of cases when their proxy advisor recommended doing so, while 45% of investors voted against in fewer than half such cases. Higher levels of correlation might be expected if proxy advisors' recommendations were the primary influence on voting decisions.

There do not appear to be many notable differences in voting behaviour based on the size of the investor or the choice of proxy advisor. However, comparing investors with UK-based teams to those without UK-based teams, a much higher proportion of the latter voted in line with their proxy advisor on more than 50% of resolutions. There is a similar pattern when comparing asset owners and asset managers.

Recommendations by the largest proxy advisors to vote against resolutions are relatively rare on most topics, for example, only 1.2% of board appointment resolutions in 2022 attracted a vote against recommendation from one or both of ISS or Glass Lewis. A notable exception is resolutions relating to remuneration, of which 14.6% attracted a vote against recommendation.

INVESTORS' USE OF VOTING POLICIES

An increasing number of investors are asking proxy advisors to provide voting research based on the investor's own customised voting policies (policies developed by the investor rather than the proxy advisor) – 75% of those investors that responded to the survey did so, and all proxy advisor interviewees reported an increase in the demand for customised policies from clients.

There is some evidence of investors taking a harder line than proxy advisors on some issues, for example, overboarding (directors holding multiple board positions). In 40% of the cases where a director's election attracted a vote against of more than 20% in 2022, both ISS and Glass Lewis had recommended a vote in favour.

As well as research reports from proxy advisors, the other main sources used by investors that responded to the survey when taking voting decisions are: their own in-house analysis, the company's disclosures, and ESG research obtained from other service providers.

Due to limited resources, most investors will issue voting instructions based on recommendations from proxy advisors without manual intervention where the resolution is uncontroversial. All investor interviewees said that they always review recommendations to vote against management and resolutions that met certain criteria, for example, all companies above a certain size or in which they own more than a certain percentage of the shares, or with which they have engaged about governance concerns.

IMPACT ON COMPANIES' BEHAVIOUR

All company interviewees said that they attempted to anticipate the likely position of some or all proxy advisors and ensure that the board or relevant committee had this information available. Many had analysed their share register to identify which proxy advisors were most likely to have a potential impact on voting outcomes.

A few company interviewees stated that their company had changed proposed resolutions or their existing governance arrangements purely in order to avoid receiving a recommendation to vote against from proxy advisors on at least one occasion, but only in relation to what they considered to be non-strategic issues.

HOW PROXY ADVISORS DEVELOP VOTING POLICIES

There can be considerable variation in the position taken by ISS and Glass Lewis on remuneration and director appointments. In two-thirds of cases where one of these proxy advisors recommended a vote against in 2022, the other took the opposite position.

Footnotes

| Financial Reporting Council (frc.org.uk) [^10]: More information available at: Home

| Best Practice Principles for Shareholder Voting Research (bppgrp.info)

INVESTORS' USE OF VOTING POLICIES

An increasing number of investors are asking proxy advisors to provide voting research based on the investor's own customised voting policies (policies developed by the investor rather than the proxy advisor) – 75% of those investors that responded to the survey did so, and all proxy advisor interviewees reported an increase in the demand for customised policies from clients.

There is some evidence of investors taking a harder line than proxy advisors on some issues, for example, overboarding (directors holding multiple board positions). In 40% of the cases where a director’s election attracted a vote against of more than 20% in 2022, both ISS and Glass Lewis had recommended a vote in favour.

As well as research reports from proxy advisors, the other main sources used by investors that responded to the survey when taking voting decisions are: their own in-house analysis, the company's disclosures, and ESG research obtained from other service providers.

Due to limited resources, most investors will issue voting instructions based on recommendations from proxy advisors without manual intervention where the resolution is uncontroversial. All investor interviewees said that they always review recommendations to vote against management and resolutions that met certain criteria, for example, all companies above a certain size or in which they own more than a certain percentage of the shares, or with which they have engaged about governance concerns.

IMPACT ON COMPANIES' BEHAVIOUR

All company interviewees said that they attempted to anticipate the likely position of some or all proxy advisors and ensure that the board or relevant committee had this information available. Many had analysed their share register to identify which proxy advisors were most likely to have a potential impact on voting outcomes.

A few company interviewees stated that their company had changed proposed resolutions or their existing governance arrangements purely in order to avoid receiving a recommendation to vote against from proxy advisors on at least one occasion, but only in relation to what they considered to be non-strategic issues.

HOW PROXY ADVISORS DEVELOP VOTING POLICIES

There can be considerable variation in the position taken by ISS and Glass Lewis on remuneration and director appointments. In two-thirds of cases where one of these proxy advisors recommended a vote against in 2022, the other took the opposite position.

All proxy advisor interviewees stated that the UK Corporate Governance Code is one of the main sources for their UK benchmark policy. On some issues the UK benchmark policies set more onerous standards than the same proxy advisors' voting guidelines for other markets, which may reflect higher expectations on the part of their UK clients as well as national requirements.

There are a few topics on which benchmark policies are more specific than the Code and other UK regulatory requirements and standards. One such example is the total number of board appointments that can be held by a director. Company interviewees consider that proxy advisor methodologies should be aligned to the Code to increase consistency, or that proxy advisors should at least be required to state explicitly how their policies deviated from the Code to increase transparency.

A relatively recent development has been the introduction by some proxy advisors of what are referred to as 'specialty' policies which vary from the benchmark policy, usually in relation to one or more aspects of ESG. The use of these products is likely to increase the variation in proxy advisors' voting recommendations noted by companies.

COMPANY VIEWS AND BEHAVIOURS

COMPANY VIEWS ON PROXY ADVISORS' IMPACT ON VOTING OUTCOMES

27The majority of company representatives that were interviewed or who took part in the roundtable meetings believed that at least some investors have in effect outsourced many or all of their voting decisions to proxy advisors, with the result that the advisors exercise considerable influence over voting outcomes. Interviewees’ views on how and why voting outcomes are influenced are set out below; the voting analysis in paragraph 91 onwards assesses to what extent the evidence appears to support these views.

28This was a particular concern because proxy advisors were perceived as taking a 'box-ticking' approach which failed to take into account individual companies’ specific circumstances and was inconsistent with the 'comply or explain' approach advocated in the UK Corporate Governance Code and because, in the words of one company interviewee, 'you have people without skin in the game.'

29These views were consistent with those of previous commentators working for or with listed companies, such as the FTSE chairs quoted in the report by Tulchan Communications published in November 2022.[^11]

30While almost all company interviewees believed that some investors vote in line with proxy advisors' recommendations without any further scrutiny, there were differences of view about the extent to which this happened. Some considered that it was widespread, while others felt it was more likely to be confined to certain circumstances.

31Several interviewees suggested that investors were more likely to vote in line with voting recommendations where they lacked resources or were looking to reduce costs. Among other impacts, this meant that these investors were often unable or unwilling to engage with companies to obtain a more informed view of their position and the rationale for the company's proposals.

32Other factors mentioned by interviewees as potentially influencing investors to vote in line with proxy advisors' recommendations included:

32.1The investor's investment approach. In particular, it was suggested by a few interviewees that index funds and investors adopting a passive approach would be more likely to follow recommendations.

‘I think passive investment funds may treat it as a tick box exercise because they’re not proactively choosing what companies to invest in.’

Company Secretary

32.2Foreign investors that did not have a UK presence. It was suggested by some interviewees that these investors may be less familiar with the UK companies in which they invest, and/or that these companies may be viewed as less significant in terms of their overall portfolio.

‘There is a difference between the US and UK in terms of how they vote. US shareholders will automatically vote against resolutions in our notice.’

Company Secretary

33Many company respondents believed that where voting decisions were taken by the investor’s stewardship or responsible investment teams, they often lacked the necessary understanding of the company or its business model and would therefore be more inclined to rely on the proxy advisor. It was implied that the same investor’s fund managers might reach a different conclusion.

34One company interviewee also considered that investors' internal processes to sign off on voting decisions might create a disincentive to vote in a way contrary to the recommendation received from the proxy advisor, as it would require them to escalate the issue in order to do so.

‘When you look at voting patterns, a lot of institutional investors won’t vote until the ISS report comes out. If they want to disagree with ISS, they have to go to their investment committees. So as long as they’re aligned with ISS, they can vote.’

Company Secretary

EVIDENCE OF INVESTOR-LED VOTING OUTCOMES

35There were different views on how widespread the reliance on proxy advisors was, with several interviewees sharing examples of where at least some investors had voted contrary to the recommendation made by their proxy advisor, both for and against the company. In their experience, it tended to be larger shareholders (in terms of their shareholding in the company and/or their overall assets under management) that did so. This might perhaps suggest that those shareholders voted in accordance with their own customised policy rather than the proxy advisors’ benchmark policy.

36Several company interviewees perceived that some UK investors were more ‘hard line’ than most of the proxy advisors’ benchmark policies on some corporate governance issues. The most frequently cited issue was overboarding (directors holding multiple board positions). One interviewee said that one of their directors had attracted a significant vote against at the previous AGM even though all the proxy advisors had recommended a vote in favour in their benchmark policies.

‘None of the proxy advisors recommended voting against the reappointment. The vote against was led by major shareholders using their own internal governance policies on overboarding. In this case it was four of the top 50 shareholders voting against. Before and after the vote we engaged with them, to hear what their concerns were and to avoid a similar case in the future. Their policy was stricter than the UK Corporate Governance Code, but they stood by it.’

Company Secretary

THE IMPACT OF PROXY ADVISORS ON COMPANIES' OWN PRACTICES

37All company interviewees were asked how they took account of the perceived influence of proxy advisors when designing their own governance arrangements and policies and explaining them to shareholders in their AGM papers and annual reports.

38The majority of the interviewees stated that they attempted to engage with proxy advisors before and during the AGM season with the aim of ensuring that they understood the company’s proposal, and that the research reports produced by proxy advisors for their investor clients were factually accurate. These issues are addressed in more detail in the Engagement During the AGM Season and Engagement Outside the AGM Season sections of this report.

Understanding proxy advisors' likely views

39In addition to engagement, most company interviewees said they attempted to anticipate the likely position of some or all proxy advisors and ensure that the board or relevant committee had this information available.

40This was considered particularly important when the company was developing governance policies, such as the remuneration policy, or considering significant changes to their governance structures, such as those affecting senior board positions.

41Most interviewees said that they scrutinised the proxy advisors' benchmark voting policies in an attempt to anticipate what their view was likely to be toward the company’s proposals, but noted that this can be very time-consuming for the company secretariat.

‘It would be easily two to three days’ work for somebody in the team to go through each report and build a matrix of what the voting recommendation looks like, including the main agencies and the large institutional investors that write to you on their key focus areas for the year. So, a lot of work goes into this.’

Company Secretary

42The majority of company interviewees said that they either analysed their share register to identify which shareholders were clients of which proxy advisors or engaged a third party to do so. This enabled them to identify which of the advisors might potentially have an impact on voting outcomes, helping them to target their engagement and reduce the level of resource required.

‘We focus a lot on the top 30 shareholders who make up about 70% of our register. In that group, we think ISS is the biggest swing factor for us.’

Company Secretary

How proxy advisors' views inform a company's decisions

43Once the analysis of proxy advisors’ policies has been undertaken it will typically be shared with the board or relevant committee so that they can factor it into their decision-making process.

‘Whenever we are doing something that we are aware will cross a line for a proxy voting advisor, we do highlight that and then the board makes the decision.’

Company Secretary

44The extent to which the views of proxy advisors informed the development of the company’s proposals, as opposed to being viewed as a ‘health check’ before the proposals were approved, varied between interviewees. Some described examples of where the views of proxy advisors were integral to the process.

‘We are very mindful when producing policy about what the proxy guidelines are. That is a big part of how we structure our internal policies.’

Head of Secretariat

45Interviewees were asked whether their company had ever changed proposals or their existing governance arrangements purely to avoid receiving a recommendation to vote against from one or more proxy advisor. A few interviewees said that there had been instances where this had been the case, but only in relation to what they described as ‘non-strategic’ issues. On matters of strategic importance, for example, board composition and the company’s climate action plan, all interviewees believed that their board would do what it considered to be in the best interests of the company and accept the potential consequences.

‘If there’s an easier path to take and it’s actually not going to fundamentally affect us from a strategic perspective, then we would probably go down the path of least resistance.’

Company Secretary and General Counsel

‘We try to do what’s right for the business and then just live with the consequences with the proxy advisors. If our approach is not what they support, so be it.’

Company Secretary

Conflicting proxy advisor recommendations

46One aspect of proxy advisors’ influence that was raised by several company interviewees was the perception that proxy advisors would often take different positions on specific resolutions or certain governance topics. This complicated the assessment process, as it could put the company in the position where it would fall foul of at least one proxy advisor whatever action it chose to take. It also made it more difficult to anticipate the likely voting outcome.

47Many company interviewees found this very frustrating and expressed the view that proxy advisor methodologies should be more closely aligned to the UK Corporate Governance Code and other national standards to ensure more consistency, or that proxy advisors should at least be required to state explicitly how their policies deviated from the Code to increase transparency. Several interviewees took the view that as there were clearly diverging views among investors on certain governance topics it was only to be expected that this would be reflected in proxy advisors’ voting policies. While some shared the frustration of the other interviewees, they accepted this was unlikely to change and was something that companies needed to learn to manage.

‘You’ve got people with different views; you’ve got to accept that you’ve got to try and strike a balance… When you get to things like remuneration where the views can be so polar or so diverse, you are going to have to accept that you’re not going to please everyone. But that’s a challenge for us.’

Company Secretary

‘Take the issue of director overboarding. There is quite a disparity of opinion, so we take the sort of lowest common denominator across all of them to make sure that any particular group that has influence isn’t unduly annoyed when we make an appointment.’

Company Secretary

48A few interviewees commented on the introduction of specialty voting policies by ISS and Glass Lewis (see paragraph 58), which can sometimes make different voting recommendations to the same proxy advisors’ benchmark policies. This added to the complexity of assessing proxy advisors’ views and predicting voting outcomes. Specifically, it may result in a single proxy advisor making different recommendations on the same resolution depending on which policy is being applied. Some company interviewees gave examples of where this had happened in relation to one of their resolutions.

49The level of awareness of these policies among company interviewees was low, and respondents felt that there was a need for greater transparency on the part of proxy advisors.

HOW PROXY ADVISORS DEVELOP AND APPLY POLICIES

BENCHMARK POLICIES

50The majority of the proxy advisors operating in the UK have a standard voting policy which they will use when assessing a company's governance and making a recommendation to their clients on whether to vote for or against a resolution (or in the case of IVIS, whether to colour code their report as 'red' or 'amber' to indicate to clients that there are potential concerns). The exception is Minerva Analytics, which produces a tailored research report for each client based on their preferences.

51These standard policies are normally referred to as benchmark policies (or 'house policies'). All the proxy advisors that use them have developed a UK-specific benchmark policy, which may be derived from a global policy in the case of those advisors who offer voting research services in multiple markets.

52All proxy advisor interviewees stated that the UK Corporate Governance Code is one of the main sources for their respective UK benchmark policies. Other sources cited by all proxy advisors include UK laws and regulations, for example, the UK Listing Rules requirements on gender and ethnic diversity at board level,[^12] and the views of investor clients and other UK stakeholders. Multiple other sources were mentioned by one or more proxy advisor.

53The proxy advisors' latest UK benchmark policies were reviewed as part of the research. In most respects they are consistent with the Code and other UK requirements and we found no evidence of different standards being 'imported' from elsewhere (a claim that is sometimes made by companies). On some issues, the UK benchmark policies set more onerous standards than the same proxy advisors' voting guidelines for other markets, which may reflect higher expectations on the part of their UK clients as well as national requirements. For example, both ISS and Glass Lewis address the issue of pensions alignment in their 2023 UK voting guidelines, but not in their guidelines for other markets.

54However, there are a few topics on which benchmark policies are less flexible than the Code or other UK regulatory requirements and standards. These tend to be topics on which the Code does not specify a minimum requirement. One such example is the total number of board appointments that can be held by a director. With the exception of executive directors the Code does not currently specify what the FRC considers to be an acceptable number of board positions, whereas the UK benchmark policies of both ISS and Glass Lewis specify a maximum of five board positions (with some exceptions and with specific circumstances taken into consideration).[^13]

55Typically, proxy advisors have an established process which they use to review the benchmark policy and update it where necessary. All proxy advisor interviewees stated that their benchmark policies are reviewed annually to take account of any regulatory changes and other market developments. Though the details of the formal process varied, the majority of interviewees mentioned that client feedback and consultation contributed to any potential revisions. For example:

55.1PIRC consults with clients annually on each new edition of its UK Shareholder Voting Guidelines. Once finalised, the guidelines are sent to all companies on the FTSE All Share Index and presented at client seminars and webinars.

55.2Glass Lewis’ review of their UK guidelines includes engagement with the Investment Association and the Association of Investment Companies among others. Glass Lewis also arranges roundtables to give investor clients an opportunity to comment directly.

56While proxy advisors use many of the same inputs to develop their benchmark policies, their voting recommendations may differ. In some cases this may result from differences between their policies on specific governance practices, in others from differences in the detailed methodology used to assess whether the company in question complied with the policy. As noted in paragraph 46, this was a source of frustration for some company interviewees.

57The analysis of voting in FTSE 350 AGMs in 2022 undertaken for this research confirms that there is considerable variation between the voting recommendations made by different proxy advisors (see paragraph 98). While the number of instances where either ISS or Glass Lewis recommended a vote against either a director election or a remuneration resolution was relatively small in terms of the overall number of resolutions, they only made the same recommendation in one-third of those cases when applying their benchmark policies.

SPECIALTY POLICIES AND RESEARCH

58A relatively recent development in the market has been the introduction by some proxy advisors, led by ISS and Glass Lewis, of what are sometimes referred to as 'specialty' research and voting policies which vary from the benchmark policy in certain respects, and which usually relate to one or more aspects of ESG.

59In some cases, these are 'off-the-shelf' policies available to all clients, as opposed to customised research tailored to the specific needs of an individual client.

Specialty policies offered by ISS include, for example:

- Climate Voting Policy

- Public Fund Voting Policy

- Socially Responsible Voting Policy

- Sustainability Voting Policy

60In other cases, proxy advisors will offer supplementary research which is intended to help inform the client's voting decisions. For example, Glass Lewis offers an ESG Profile which includes a series of data points as well as a scoring methodology it has developed (see paragraph 261 onwards for a more detailed analysis of the use of ESG data and methodologies).

61The use of these products is likely to increase the variation in proxy advisors' voting recommendations noted by companies. Specifically, it may result in a single proxy advisor making different recommendations on the same resolution depending on which policy is being applied.

62As noted in paragraph 48, it was clear from the interviews with company representatives that there has to date been little awareness of the existence of these specialty products, and it was confirmed by the proxy advisor interviewees that companies are not given an opportunity to comment on the content of these research reports in the same way as some consult companies on their benchmark research reports.

‘Specialty policies are transparent and on our website. We can’t provide every single custom voting policy to issuers, so they’ll receive a benchmark report. I think that was the issue: companies have visibility of the benchmark report but then hear there’s a different stance on the voting resolution. It looks similar but it’s an educational issue. It’s something we need to address and communicate with issuers.’

Director, Regulatory Affairs and Public Policy (Proxy Advisor)

CUSTOMISED VOTING RESEARCH AND RECOMMENDATIONS

63All proxy advisors apart from IVIS also offer customised research and/or voting recommendations to individual clients, based on that client's own in-house voting policy. This enables that investor to tailor the research and recommendations to reflect its own position, which on some issues may be more stringent than the proxy advisors' benchmark policy.

64All the proxy advisor interviewees confirmed that the number of clients that request customised voting research or recommendations has increased in recent years. Their estimates of the number of clients currently receiving customised research ranged between 25% and 75%. Interviewees stated that the majority tended to be larger or niche investors with in-house stewardship resources. This appears to be borne out by the evidence gathered from the investor survey and interviews described in paragraph 67. However, one proxy advisor interviewee noted that an increasing number of their smaller clients were also adopting customised policies.

65Proxy advisors maintain different processes for helping clients update and implement custom policies. For example:

65.1If requested, ISS’ custom research analysts may offer guidance to clients on how to create and apply their own voting policies, including back-testing policies by market to ensure consistency of application. ISS also offers regular review of clients’ custom policies to ensure new or emerging issues that have garnered increased interest in the investment community are identified.[^14] The interviewee from ISS estimated that they implemented voting recommendations for more than 500 custom client policies in 2022.

65.2Minerva Analytics has a voting policy workbook which covers all topics that clients may wish to cover in their voting policy. Their analysts go through the workbook with the client to establish what their voting preferences are, and these preferences are then used to develop a bespoke voting template. Additionally, Minerva produces background briefings on voteable issues.

HOW INVESTORS USE VOTING RESEARCH

66The evidence from the survey and investor interviews suggests that the nature of the research that investors receive from proxy advisors, and the use to which they put it, varies considerably between investors.

USE OF CUSTOMISED POLICIES

67In total, 75% of the investors who responded to the survey said that they instruct proxy advisors to apply the investors own customised policy as well as or instead of the benchmark policy when undertaking research.

68It is recognised that the respondents may not necessarily be representative of investors as a whole; for example, they have all demonstrated a commitment to stewardship by being signatories to the Stewardship Code. However, these findings are consistent with previous research commissioned by the FRC.[^15]

69An analysis of the respondents found no significant difference between asset managers and asset owners or between UK and foreign-based investors in the use of customised policies. However, there does appear to be some correlation between the size of the investor’s portfolio or assets under management and their use of customised policies, with only 60% of small asset managers using them compared to 90% of large managers.[^16] This is consistent with the evidence from proxy advisors referred to in paragraph 63.

EXHIBIT 2: USE OF CUSTOMISED POLICIES [INVESTOR SURVEY]

70There are not necessarily a significant number of differences between the benchmark policy and the customised policies of individual investor clients. Interviewees highlighted that in-house and benchmark policies will often overlap to a large extent, in part because the investor and proxy advisor both use many of the same sources, such as the UK Corporate Governance Code. In addition, in some cases investors are able to influence the content of the benchmark policy by participating in the proxy advisors' annual review process.

71Examples from interviewees of issues on which their own customised policies often took a harder line than proxy advisors' benchmark policy, included overboarding of directors, diversity and (in the case of some UK-based investors) the alignment of directors' pension arrangements with those of the workforce. One investor interviewee stated that they have a harder line than their proxy advisor on long-term incentives retention periods, and unlike some proxy advisors did not apply lower standards on independence and diversity to smaller companies.

‘They sometimes take too strong a stance and that’s why we do not blanket follow. We look at their recommendations on a case-by-case basis and if there is a difference would much rather go with our own voting policy.’

ESG and Stewardship Analyst

‘Sometimes we differ from our proxy advisor for two reasons. One is because we just have a different view and we’re coming at it from a different starting point. The second is that quite often they don’t do the depth of analysis on emerging ESG issues that we think they should do, for example on workforce analysis.’

Head of Stewardship

USE OF MULTIPLE POLICIES

72Even where an investor is receiving customised research or applying their own in-house voting policy, they may also obtain research that uses a benchmark or specialty policy from the same or a different proxy advisor. As noted in paragraph 15, 31% of investors that responded to the survey use the services of more than one proxy advisor.

73Investor interviewees identified a number of reasons for doing so, including to identify issues on which the customised and benchmark policies and/or the various proxy advisors reached different conclusions – which might prompt them to look at the issue in more detail – and to provide additional insights or fill in gaps in the research.

‘We’re always guided by our own voting policy, but it’s very useful to have that additional research. We get a custom policy report through from the proxy advisor, as well as their benchmark policy, and a sustainability voting template, to give an ESG overlay to our voting.’

ESG and Stewardship Analyst

‘We subscribe to both ISS and Glass Lewis research globally, and we actively look for differences of opinion or discrepancies between the two providers so we can compare and contrast opinions.’

Investment Stewardship Director

OTHER INPUTS TO INVESTOR VOTING POLICIES AND DECISIONS

74All investor interviewees stated that they made use of other inputs when developing their in-house policies and taking voting decisions. As one of them put it, the proxy research report was just 'one piece of the jigsaw.'

75This was consistent with responses to the survey. All investors that responded, including those that use the proxy advisors' benchmark policy rather than a customised policy, identified at least one other source of information that they used. As already noted, interviewees and respondents may not necessarily be representative of all investors.

EXHIBIT 3: WHAT OTHER RESOURCES DO YOU USE TO INFORM YOUR VOTING DECISIONS? [INVESTOR SURVEY]

Bar chart showing the percentage of investors using various resources to inform voting decisions: In-House Analysis 100%, Investee Company Disclosures 91%, ESG Research or Ratings 72%, Other Sources 41%, and None 0%.

76The other sources identified by survey respondents included engagement with the company (either one-to-one engagement or as part of broader collaborative engagement), media reports and guidance, and briefings from third parties, for example, the Pensions and Lifetime Savings Association (PLSA) and Climate Action 100+.

INVESTORS' DECISION-MAKING PROCESSES

THE ROLE OF VOTING PLATFORMS

77Four of the proxy advisors currently providing voting research in the UK – Glass Lewis, ISS, Minerva and PIRC – also provide a voting platform that investors can use to manage their voting activity.

78The scope and functionality of these platforms varies but most share a number of common features. These typically include: access to shareholder meeting agendas, papers and research reports, alerts to notify the investor of impending deadlines (including voting deadlines), and filters that enable investors to identify specific resolutions that they wish to review.

79Most platforms will also include a vote execution function which enables the shareholder to send voting instructions to a custodian or their agent for onward transmission through the voting chain and ultimately to the company (more details of how the voting chain works can be found in the Voting Chain Deadlines section of this report). In the case of Minerva Analytics, instructions are sent directly to vote tabulators rather than to custodians.

80Typically, the voting instructions form for each meeting will be filled in by the proxy advisor using as a default the voting recommendations derived from whichever policy and parameters the investor has asked them to apply. Investors have the ability to change these settings if they wish to vote differently to their chosen policy’s recommendations, or wish not to vote at all.

81Investors can choose to submit their voting instructions in advance of the voting deadline for a specific meeting. If they choose not to do so, then the instructions will be sent automatically by the custodian or intermediary’s deadline, or the deadline agreed with the voting platform if different, regardless of whether or not they have been confirmed by the investor.

USE OF DEFAULT VOTING RECOMMENDATIONS

82The way that the platforms typically work means that it is possible for all of an investor’s votes to be executed without any direct involvement from the investor themselves other than agreeing with the proxy advisor which voting policy was to be applied.

83This contributes to the perception many companies have that some investors effectively delegate their voting decisions to proxy advisors, especially in cases where the same proxy advisors provide both the platform and the voting research (as was the case for 87% of investors that responded to the survey). In interviews with the proxy advisors, some acknowledged that this approach had been adopted by a number of their clients, although the interviewees stated that clients were encouraged to review voting instructions before the relevant deadline.

84Most investor interviewees confirmed that many voting recommendations – in some cases the majority - were executed without having been manually confirmed by the investor. However, they emphasised that this only applied to resolutions that they considered uncontroversial and where the recommendation was to vote with management.

85The main reason given for taking this approach was limited resources. Most interviewees invest in a large number of companies, many of whose AGMs are held close together. Filtering out uncontroversial votes in favour of management enables allows the investor to focus on those AGMs and resolutions that they consider to be priorities.

86All investor interviewees said that they will always review any recommendation to vote against management. Each interviewee also identified other criteria that were used to identify priority resolutions. Examples included:

- All holdings above a certain value;

- All companies in which they own more than a certain percentage of the shares;

- All companies above a certain size;

- All companies about which the investor has previously had concerns or with which they have engaged about governance concerns; and

- All resolutions on certain topics, for example remuneration or climate.

‘All our sizeable positions in the big markets in Western Europe where we have holdings are voted in-house. What gets voted through via the platform using our custom policy is a long tail of very small positions.’

Managing Director, EMEA Investment Stewardship

‘For instance, we have a workforce watchlist because one of our priority themes is the workforce. Every time our intelligence gathering picks up a company where there have been issues we put that on the watchlist. Then we know to pay particular attention to that company when the vote comes up.’

Head of Stewardship

VOTING DECISIONS ON CONTROVERSIAL RESOLUTIONS

87Investor interviewees all stated that they had policies and delegations that applied when considering a vote against a resolution or against their own customised policy (and in some cases also against the recommendation of their proxy advisor).

88The majority of investors stated that the policies required consultation with other teams in these circumstances, for example, with the portfolio manager when the stewardship team had the overall lead responsibility and vice versa. This could sometimes lead to differing views about how to vote. In addition, some investors allow their portfolio managers to vote in different ways, while others require internal alignment.

89Some policies required escalation to a more senior level when voting against a resolution or the usual policy and in cases where there is a difference of opinion, while others allowed some discretion.

‘Each meeting goes to the analyst who is responsible for the stock. They also have responsibility to vote, apart from where it’s deemed a significant vote, a shareholder resolution or it’s something controversial. In those cases it gets elevated up to the senior portfolio manager.’

Responsible Investment Manager

‘If there are areas that we can engage with the companies on, my team has the discretion to go against the proxy advisor recommendation. In addition, any analyst can actually go against a policy recommendation, be it our own custom policy or that of the proxy advisor. However, they have to provide us with a written rationale explaining why they have chosen to do so.’

Head of Governance and Stewardship

| EXHIBIT 4: INVESTOR APPROACHES TO CONTROVERSIAL VOTING DECISIONS | |

|---|---|

| INVESTOR 1 | |

| • | Investor 1 has a dedicated sustainable investing team, which works with the investment teams and is responsible for consolidating the firm’s approach to stewardship, engagement, ESG integration, and exercising votes at general meetings. |

| • | For voting activity, the relevant portfolio managers and analysts will generally be consulted before the vote is cast on certain matters. This includes voting resolutions related to M&A and capital raisings, debt issuances, material changes to the articles and votes against management where the investors shareholding is material. |

| • | In cases where individual portfolio managers have opposing views on a particular resolution, or where views differ between the portfolio managers and the sustainable investing team, the investor has an escalation process. |

| • | Final decision-making authority resides with the Sustainable Investing Oversight Committee (SIOC). Votes that are particularly significant for the organisation as a whole, for example, for reputational reasons, may also be escalated to the SIOC for review and approval. |

| INVESTOR 2 | |

| • | Investor 2 has a voting process which is managed by its Sustainable Investment Research and Stewardship team, who work closely with the fundamental investment teams to decide how to exercise voting rights based on voting principles, any engagement that has been undertaken, and internal knowledge of the investee company. |

| • | In cases where Investor 2 plans to deviate from its initial policy view, the Stewardship Committee reviews the reason and considers the case for/against changing the initial recommendation. |

| • | A majority of committee members should approve the intended vote. Reasons for the final decisions are recorded, tracked and used to inform future policy reviews. |

| • | If an individual portfolio manager is managing a strategy which is seen to be completely different to anything else within the firm, then they have the right to vote in line with the best interest of that particular investment approach. Ideally, however, the investor seeks to arrive at a single decision. |

90While their internal procedures differed, most investor interviewees were able to give examples of where their voting decision differed from the proxy advisor’s recommendations. One head of ESG estimated that this happened on as many as 20% of the resolutions that they classified as priorities, particularly those relating to remuneration and director appointments.

VOTING ANALYSIS

91In an attempt to establish whether there is evidence to support the view held by companies that many investors will routinely vote in line with proxy advisors’ recommendations to vote against resolutions, an analysis was undertaken of selected resolutions from FTSE 350 AGMs in 2022.

92The analysis reviewed the recommendations made by ISS and Glass Lewis on resolutions on board appointments and remuneration (including both binding votes on remuneration policies and advisory votes on remuneration reports) and compared them with the actual voting outcome and the voting activity of selected investors.

93While there are some limitations to the analysis, as explained below, it has produced some interesting findings on the extent of the correlation between voting recommendations of proxy advisors and the voting decisions of investors.

94However, it is important to emphasise that the analysis does not demonstrate any causation between the two activities. As investors and proxy advisors pointed out in the interviews, if an investor has selected a voting policy that closely reflects their views then it is to be expected that their voting decisions would be in line with that policy in most instances, especially where it is their own customised policy.

SAMPLE OF RESOLUTIONS

95The sample included all resolutions on remuneration and board appointments proposed by FTSE 350 companies that held their AGMs before 30 October 2022 – a total of 322 AGMs. An analysis of these resolutions identified 93 cases where one or both of ISS and Glass Lewis recommended a vote against a resolution, 60 on remuneration and 33 on board appointments. Where a proxy advisor recommended against the election of more than one director this has been counted as a single case.

96For context, the total number of remuneration-related resolutions proposed by the 322 companies in the sample was 411, while the total number of directors put forward for election was 2,667.9

97This means that recommendations to vote against were made by either or both ISS and Glass Lewis in respect of 14.6% of all remuneration-related resolutions and 1.2% of director elections.10

98The analysis appears to support the contention of some company interviewees that the recommendations made by different proxy advisors will often differ. In only one-third of the 93 cases in the sample did both ISS and Glass Lewis recommend a vote against in their benchmark policies.

EXHIBIT 5: COMPARISON OF VOTE AGAINST RECOMMENDATIONS BY PROXY ADVISOR

| Category | Both | ISS | Glass Lewis | Total | Overlap |

|---|---|---|---|---|---|

| Total | 30 | 29 | 34 | 93 | 32% |

ANALYSIS OF VOTING OUTCOMES

99The first part of the analysis looked at the percentage total votes for and against each of the resolutions in the sample, using data published by the companies concerned following their AGM. The analysis aimed to identify:

- How many resolutions received a significant level of votes against (defined as 20% or more in the UK Corporate Governance Code and the Investment Association’s Public Register);11

- Whether there was a consistent pattern in the levels of voting dissent across all resolutions in the sample (which might be an indicator of a correlation between voting recommendations and outcomes);

- Whether there was a difference in the levels of dissent where both ISS and Glass Lewis recommended a vote against as opposed to only one of them; and

- Whether there was a difference in the levels of dissent depending on the topic (some company interviewees believed that votes on remuneration will tend to attract higher levels of dissent) or the size of the company (some company interviewees believed that smaller companies might be more exposed to 'automatic voting' as they may be considered lower priority by investors when allocating their stewardship resources).

100There are some limitations to this analysis, the most obvious being that the analysis only covers voting recommendations made by ISS and Glass Lewis rather than all the proxy advisors. The decision only to review the recommendations of the two proxy advisors with the largest client base was primarily taken because of resource and data constraints but it means the potential impact of other advisors has not been researched.

101In addition, it was only possible to analyse the recommendations in ISS’ and Glass Lewis’ benchmark policies; the recommendations made when applying their specialty policies or client’s customised policies may differ. Finally, data was not available on the percentage of each company’s share register that consists of ISS and Glass Lewis clients, which clearly affects the potential impact of their recommendations.

TOTAL VOTES AGAINST

102The analysis found that just over 50% of the resolutions in the sample received a vote against of 20% or more (48 of 93 resolutions), with an average vote against for all resolutions in the sample of 22.3% (see Exhibit 6). Only three resolutions were not approved by shareholders, one in the FTSE 100 and two in the FTSE 250. All three were remuneration-related resolutions.

103There was considerable variation in the levels of dissent across the sample. The lowest percentage of votes against a resolution was 2.2% and the highest was 71.3%. While allowance needs to be made for differences in the composition of company share registers, there appears to be no consistent pattern in the level of dissent where proxy advisors recommend a vote against.

EXHIBIT 6: AVERAGE AND RANGE OF VOTES AGAINST FOR RESOLUTIONS WHERE ONE OR BOTH OF GLASS LEWIS AND ISS RECOMMENDED VOTING AGAINST

| Category | Resolutions | >20% votes against | % >20% votes against | Average vote against | Range of votes against |

|---|---|---|---|---|---|

| ALL | 93 | 48 | 52% | 22.3% | 2.2% 71.3% |

COMPARISON OF VOTING RECOMMENDATIONS BY PROXY ADVISORS

104The analysis found there was a significantly higher likelihood of votes against exceeding 20% when both ISS and Glass Lewis recommended a vote against than when only one did so (see Exhibit 7). The difference between ISS and Glass Lewis might perhaps be expected given their respective UK market shares.

EXHIBIT 7: SIGNIFICANT VOTES AGAINST WHEN RECOMMENDED BY INDIVIDUAL PROXY ADVISORS

Bar chart comparing significant votes against recommendations by individual proxy advisors.

- Both against: 77%

- ISS only against: 59%

- GL only against: 21%

VOTING BY TOPIC AND COMPANY SIZE

105The analysis found that a higher proportion of remuneration-related resolutions received a vote against that exceeded 20% of votes cast than resolutions relating to board appointments (55% compared to 45%), and that the average vote against was higher for these resolutions. However, it was also the case that there was a wider distribution in terms of the highest and lowest levels of dissent.

EXHIBIT 8: BREAKDOWN OF VOTES BY TOPIC

| Category | Resolutions | >20% votes against | % >20% votes against | Average vote against | Range of votes against |

|---|---|---|---|---|---|

| Board appointments | 33 | 15 | 45% | 18.2% | 2.2% 38.8% |

| Remuneration | 60 | 33 | 55% | 24.4% | 5% 71.3% |

106By contrast, there was no significant difference between companies of different sizes. Resolutions proposed by FTSE 100 companies were marginally more likely to receive 20% or more votes against (54% of the total compared to 50% for FTSE 250 companies), but the average vote against was virtually identical.

EXHIBIT 9: BREAKDOWN OF VOTES BETWEEN FTSE 100 AND FTSE 250

| Category | Resolutions | >20% votes against | % >20% votes against | Average vote against | Range of votes against |

|---|---|---|---|---|---|

| FTSE 100 | 39 | 21 | 54% | 22.5% | 3.8% 71.3% |

| FTSE 250 | 54 | 27 | 50% | 22.1% | 2.2% 55.4% |

OTHER SIGNIFICANT VOTES AGAINST