The content on this page has been converted from PDF to HTML format using an artificial intelligence (AI) tool as part of our ongoing efforts to improve accessibility and usability of our publications. Note:

- No human verification has been conducted of the converted content.

- While we strive for accuracy errors or omissions may exist.

- This content is provided for informational purposes only and should not be relied upon as a definitive or authoritative source.

- For the official and verified version of the publication, refer to the original PDF document.

If you identify any inaccuracies or have concerns about the content, please contact us at [email protected].

ComRes FRC stakeholder survey results - December 2017

OBJECTIVES & METHODOLOGY

In order to generate robust measures of delivery against KPIs, the Financial Reporting Council (FRC) decided to build on previous reputation audits and to commission fresh research into stakeholder audiences. Identifying the need for current analysis of stakeholder engagement and perceptions, they commissioned ComRes to deliver a mixed-methodology research project.

ComRes supplied lists of directors and non-executive directors (NEDs) to add to the FRC's existing contact lists, and delivered an online survey with agreed segments of stakeholders, followed by qualitative interviews with these audiences. The research was designed to test levels of familiarity with the role and functions of FRC, to explore favourability of the FRC brand among priority audiences, and to measure effectiveness of FRC communications.

ComRes surveyed 297 senior stakeholders online and over the telephone between July and September 2017. 32 interviews with key stakeholders took place between August and October 2017.

Responses were split as follows:

| Role | Stakeholder survey | Stakeholder interviews |

|---|---|---|

| Institutional investors | 42 | 5 |

| Directors | 128 | 7 |

| Non-Executive Directors | 31 | 2 |

| Auditors | 48 | 5 |

| Actuaries | 11 insurance actuaries, 14 pensions actuaries | 4 |

| Professional bodies | 23 | 2 |

| Others | – | 7 |

| Total | 297 | 32 |

Please note, where an asterisk is used in segment charts, this denotes a low base size and findings should be treated as indicative.

A full list of stakeholders who participated in the interviews is available in the Appendix. Those listed as 'Others' include a mix of individuals representing a broad range of interests and experiences, spanning business and government.

COMRES FOREWORD

Since the 2007 financial crisis, trust in business and financial institutions has remained persistently low despite efforts to assure consumers otherwise. Indeed, public research we have undertaken supports this, with many consumers saying they trust those working at their local, high-street bank but with far less trust for large financial institutions, 'fat-cats' and the finance sector as a whole. This has coincided with an increasing demand for, and expectation of, more transparency from organisations whether they be public or private sector. If the research we undertake for a range of clients is anything to go by, how to be truly transparent and open in a meaningful way is an issue that many organisations, and regulators, are currently grappling with.

In what has been the broadest research study the FRC has undertaken with its stakeholders, the findings demonstrate that stakeholders reflect this consensus for a need for increased transparency, wanting more visibility of the FRC's processes and outcomes. Nor was this view exclusive to one particular stakeholder group – rather is was voiced by many from across the spectrum of those we spoke with. The recent press coverage around the FRC further substantiates this, with some critics voicing concerns over the outcomes of recent investigations and conflicts of interests within the FRC. Arguably, there is room for the FRC to be more transparent in its disciplinary investigations and communication about how it manages conflict of interest. As a regulator, the FRC needs to be appropriately stringent in its enforcement activities, but in order to meet the needs of stakeholders, it needs to do so in a way that isn't opaque.

However, transparency is not the only challenge that the FRC faces. Stakeholders also want to see the FRC become more outcome-orientated, and less process-driven. Their desire for resourcing to be deployed more strategically and communications improved are but a few of the key suggestions included in this report. Expanding the stakeholder list in future research, such as including MPs, could provide useful insight into the progress that has been made in these areas and whether there is public interest in promoting the work the FRC does.

One thing that has been clear in conducting this research for the FRC is the difficulty in uniting the attitudes, experiences and recommendations of a varied group of stakeholders. Given the variety of areas that the FRC covers, stakeholders represent a diverse array of professions with a diverse array of interests. Bringing together the views of these individuals – who sometimes only engage with one part of the FRC - appears to be a unique challenge.

That said, the FRC is in a strong position to address some of the key feedback from stakeholders. Overall familiarity is high and stakeholders are more likely to be favourable than not towards the organisation. This suggests that by addressing some of these concerns, the FRC is well-placed to further increase its favourability and trust amongst key audiences in the year ahead.

Meghan Oliver Associate Director

EXECUTIVE SUMMARY

Overall, stakeholders highlighted a number of positives for the FRC, while acknowledging that key improvements need to be made. Key strengths for the regulator include its high level of familiarity, the efficacy of its work in corporate reporting and governance, and a view that improvements have been made in recent years – both in areas of work, as well as ways of working. That said, stakeholders also felt that the FRC could make a number of improvements. Namely, stakeholders expressed concern over the transparency of the FRC's processes and decision making, its speed of enforcement activities, how effectively it prioritises resource and they would like to see the FRC be more outcome-driven.

Stakeholder groups expressed varying levels of positivity towards the FRC. The ‘others' segment were the most vocal in their criticism of the FRC, perhaps as a consequence of having a broader view of the FRC's work and its public perceptions. Company directors and institutional investors were more mixed in their views of the FRC. Although auditors were not universally positive towards the FRC, given their increased understanding of the FRC's work, they were generally more positive than other groups in the survey results and expressed a more balanced opinion in interviews.

- Broadly speaking, stakeholders are familiar with the FRC, but this tends to be only in the specific areas in which stakeholders come into contact with the FRC, as opposed to the full remit of the FRC's work. It is notable that stakeholders who expressed greater familiarity with the FRC were also more favourable, suggesting that there is room for the FRC to increase communication and engagement with key groups – particularly company directors, NEDs and institutional investors.

- Despite recent criticism in the press, stakeholders broadly consider the FRC to be independent of the audit profession. Even removing auditors from those surveyed, the majority of stakeholders consider the FRC to be independent. Institutional investors expressed the most concern about the FRC's independence, related to the hiring of ex-auditors, and would like conflicts of interest to be made more visible.

- Many felt that improvements could be made in transparency within the FRC itself. Given that the FRC holds others accountable, it needs to be seen to be holding itself accountable to these same measures. Several stakeholders felt that the FRC is too opaque in its own processes and outcomes of reviews.

- In line with this, stakeholders would like to see more transparency in disciplinary and enforcement activities. About half of stakeholders feel the stringency of enforcement activities is 'about right' – notably auditors were the most likely to believe the FRC is too stringent, while institutional investors were most likely to believe the FRC is not stringent enough. In addition to this, some stakeholders felt the FRC ‘lacked teeth', and that the slow speed of enforcement activities undermined their outcomes.

- Further to this, stakeholders would like to see the FRC improve its ways of working, both in terms in terms of its focus and its internal processes. Namely, stakeholders would like to see the FRC be more outcome-driven and less process oriented. Although the majority of stakeholders are favourable towards the FRC, there was a sense across the spectrum of stakeholder audiences, that the FRC can undertake regulation for the sake of it. As such, increased communication around the FRC's goals and activities would be welcome. Finally, several stakeholders also raised concerns about resourcing at the FRC; whether resources are deployed effectively or if the quality is at the same level of other regulators. However, several stakeholders felt there have been improvements in recent years in this area.

- Stakeholders were broadly positive about the FRC's work in corporate governance, reporting and audit. In several instances, stakeholders felt that the FRC set global standards in these areas with a few notable improvements. Although the UK Corporate Governance Code was held up by many as a global standard, constant small revisions to the Code was flagged by stakeholders as cumbersome with unclear value. Similarly, although corporate reporting was generally considered to be of high quality, the length of reports with too much ‘boiler-plate' were flagged as issues which need to be addressed.

- Views were more mixed on the FRC's work in actuarial work and investor stewardship. In the case of actuarial work, there was very limited familiarity amongst stakeholders of the work undertaken in this area apart from those who work in this area. Actuaries were broadly positive about the work the FRC undertakes but there is an opportunity to further distinguish between the FRC and the Institute and Faculty of Actuaries (IFOA)'s remit. Investor stewardship had a lower profile than corporate governance, reporting and audit, and stakeholders were less convinced of the efficacy of the FRC's work in this area. Reasons for this include the fact that the Stewardship Code is relatively new (and thus less entrenched) and that it does not apply to shareholders based outside the UK. Although stakeholders feel more could be done in this area, the Stewardship Code is a promising start.

RECOMMENDATIONS

Regulatory approach

- Stakeholders would like to see the FRC be more outcome-orientated, and less driven by processes. With numerous consultations and revisions to Codes, stakeholders require reassurance that changes taken will add value to outcomes, and are not simply additional regulation.

- This also applies to enforcement activities, where stakeholders would like to see that actions look to correct the problem more broadly, and are not simply punitive in nature.

Ways of working

- As a regulator, stakeholders expect to see the FRC be more transparent and open about its internal processes and outcomes of its reviews. This increased transparency would ensure that the FRC is held to high standards.

- Given the broad remit of the FRC and its finite resources, stakeholders would like to see to staffing re-prioritised or increased in order to ensure that all areas of work receive equal attention. In practice, this means ensuring that the right people are undertaking the right tasks and that processes are appropriately streamlined.

The FRC's work

- Nearly all stakeholders would like to see corporate reports shortened in order to make them more relevant and key information easier to find. As annual reports are primarily used to assess the financial performance of a company, there is also the opportunity to address whether non-financial matters covered in reports (e.g. culture and values) should be made available on corporate websites instead.

- Stakeholders are positive about the UK Corporate Governance Code and the Investor Stewardship Code, however felt that both could be improved. There is hope that there will be fewer amendments to the Governance Code in order to ensure consistency and remove change for the sake of change, while stakeholders were keen to see the FRC go further with the Stewardship Code and ensure buy in from institutional investors.

Communications

- Given that stakeholders who are more engaged with the FRC have a greater understanding of internal processes (and constraints), increasing outreach and communication with less engaged stakeholders offers an opportunity to improve favourability and perceptions of transparency. Consistent communication and face-to-face events can help generate engagement.

- There is an opportunity to increase the profile of the FRC's work in key areas namely investor stewardship and actuarial work where familiarity is more limited.

- Additional communication around enforcement activities would also demonstrate that the FRC has 'teeth' and the increased transparency of the FRC's work in this area could help to generate trust.

KEY CONSIDERATIONS

The findings from this research and the conclusions we have drawn present a number of questions that warrant further thought and discussion by the FRC. These questions are worthy of further consideration as the FRC decides what actions it can reasonably take and what its priorities should be based on the feedback gained from its stakeholders. We have listed these out below:

Transparency

- Are clear conflict of interest policies in place to assure stakeholders that the FRC is not captured by the audit profession? Are these clearly communicated and easily available?

- Will the register of interests go far enough in generating increased levels of transparency amongst stakeholders? What else should the FRC be doing to generate this?

Familiarity and engagement

- Given that familiarity with the FRC tends to be in specific areas, does the FRC need to do more to bring together disparate groups of stakeholders?

- What type of public profile should the FRC have? Does the FRC communicate effectively with the broad public?

- Could the FRC engage better with specific groups of stakeholders? Do, and should, all stakeholders within a particular audience receive the same level of outreach?

- Should the FRC look to engage with institutional investors further to explore their attitudes towards audit and views towards the FRC's independence and transparency?

- Do discrepancies in opinion between stakeholder groups present any causes for concern? For example, will the FRC be able to balance the enforcement stringency requested by institutional investors with the desire for less stringency by auditors?

- Is criticism of the FRC amongst a vocal minority? And what can be done to respond to the critics?

Ways of working

- Are internal resources deployed effectively? Are the right resources, with the necessary expertise, in place? Are there specific processes or functions which could be better streamlined?

- Do existing processes improve outcomes or are they more punitive or process-orientated in nature?

The FRC's work

- How effective are corporate reports in terms of length and all that is included within them e.g. environmental sustainability and corporate social responsibility? Can some sections be made available elsewhere e.g. company websites?

- Does the FRC's Governance Code need constant revision or a complete re-assessment?

- Is there a clear enough distinction between the work that the FRC does and the work other bodies that may represent different sectors, such as the Institute and Faculty of Actuaries?

THE FRC AND ITS WORK

FAMILIARITY

| Stakeholder | % |

|---|---|

| Insurance company director* | 71% |

| Company director | 83% |

| NED | 81% |

| Auditor | 98% |

| Insurance Actuary* | 100% |

| Pension Actuary* | 100% |

| Professional body* | 100% |

| Institutional investor | 90% |

Q4. How familiar or unfamiliar would you say that you are with the Financial Reporting Council as an organisation? Base: All respondents (n=297)

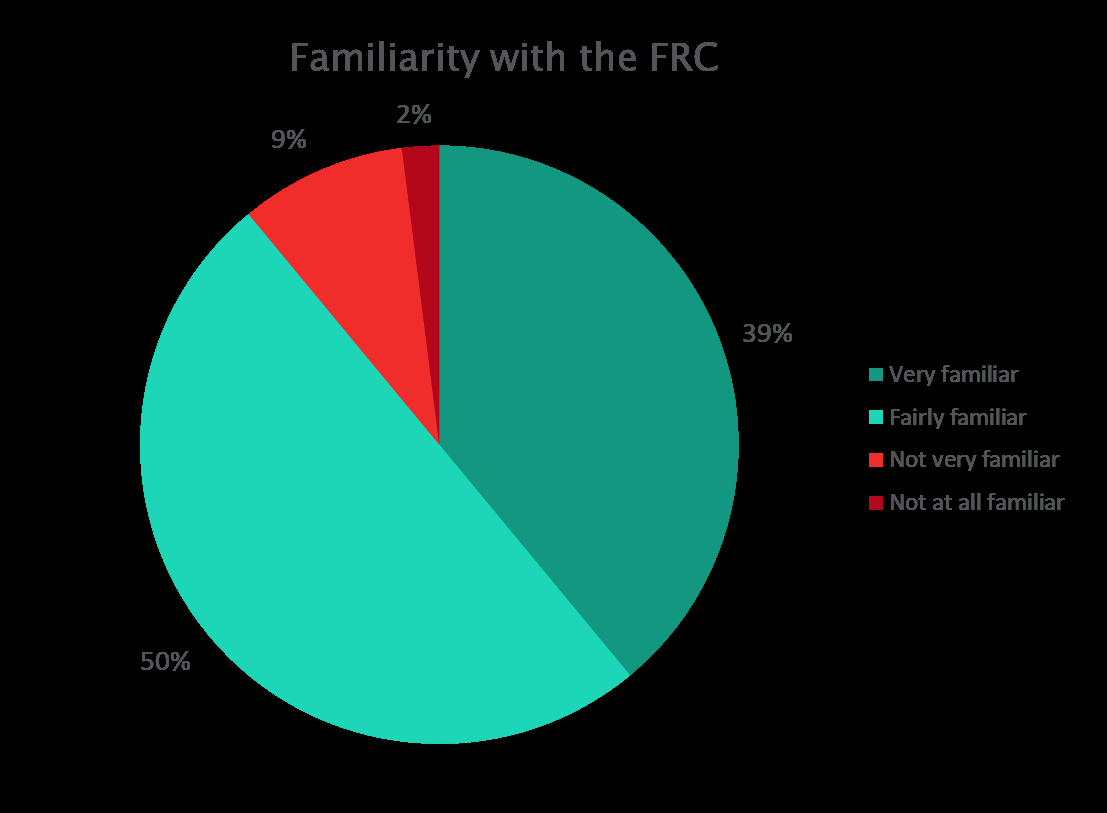

The vast majority of stakeholders (89%) consider themselves familiar with the FRC. Given that the FRC has had less engagement with company directors and NEDs in the past, it is positive that four-fifths of these groups (83% and 81%, respectively) consider themselves familiar with the FRC.

Although most stakeholders feel they are familiar with the FRC, few are familiar with all of the FRC's areas of work or its full remit. Rather, most are only familiar with the areas that they engage with (e.g. audit, corporate reporting) and have little knowledge beyond these areas. Although stakeholders didn't express a desire to know about all areas of the FRC, it may be worth the FRC considering how important it is for different stakeholder groups to have greater awareness of its full remit in order to encourage further understanding of its structure and processes.

In stakeholder interviews, nearly all were aware that the FRC is a public body although this didn't influence their view of it. Where stakeholders expressed a desire for greater familiarity was with FRC strategy and internal processes, in line with a broader desire for increased transparency from the regulator.

I think it would be good to get a good grasp of, you know, who they are, what are they looking to achieve, and then who is involved in what. It feels a bit erratic at times.

Institutional Investor

FAVOURABILITY

| Stakeholder | % |

|---|---|

| Insurance company director* | 67% |

| Company director | 64% |

| NED | 55% |

| Auditor | 63% |

| Insurance Actuary* | 91% |

| Pension Actuary* | 64% |

| Professional body* | 78% |

| Institutional investor | 64% |

Q5. How favourable or unfavourable is your overall impression of the Financial Reporting Council as an organisation? Base: All who are familiar with the FRC (n=291)

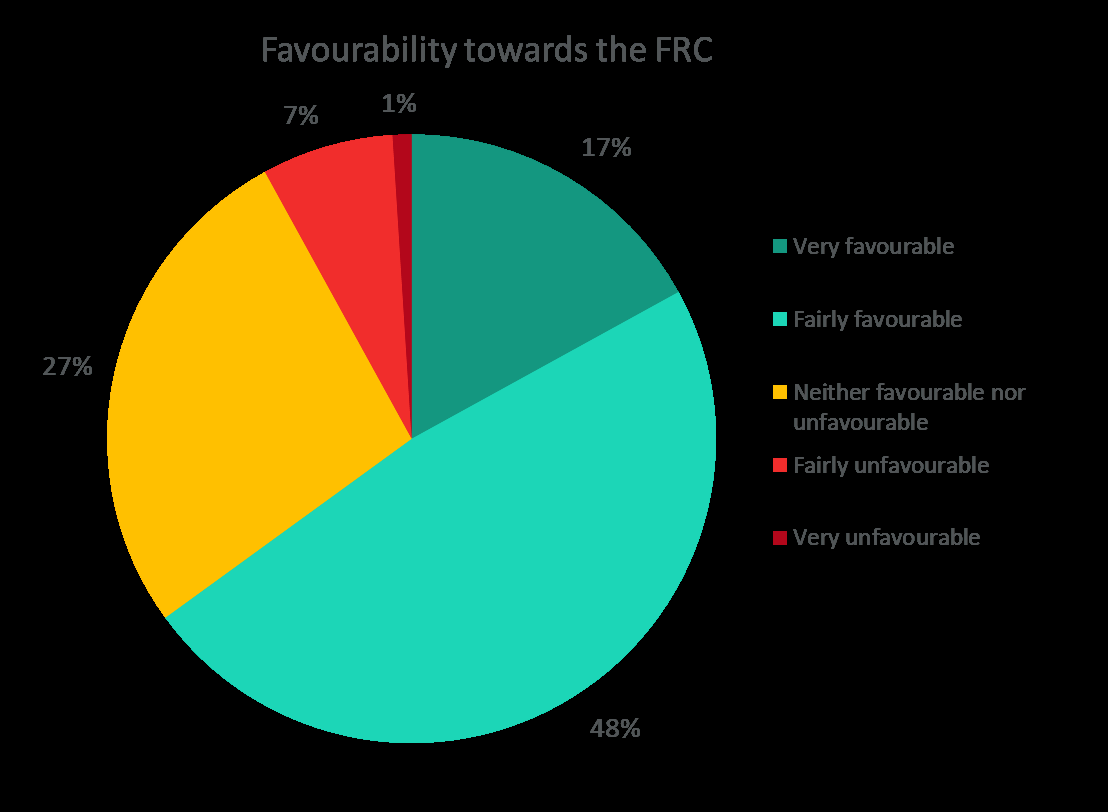

Two-thirds of stakeholders (65%) are favourable towards the FRC, with clear differences between the segments. Insurance actuaries are most favourable (91%, albeit from a low base size), while NEDs expressed the lowest favourability (55%) towards the FRC. Only 8% of stakeholders feel unfavourable towards the FRC, leaving just over one-quarter (27%) being neutral. As such, there is a clear opportunity for the FRC to shift a sizable minority of stakeholders from neutrality towards favourability.

Although a broad group of stakeholders are favourable, stakeholders expressed several areas where the FRC could improve.

Firstly, stakeholders identified the FRC's regulatory approach as requiring improvement, with some concerned that the FRC is too focused on the development of regulation rather than the outcomes or implementation of regulation. There was a sense that, as a regulator, it can be focused on simply generating regulation as opposed to ensuring the outcomes are suited to needs. As such, stakeholders would like to see the FRC be more outcome rather than process focused, and clearly demonstrate how the actions being undertaken will correct or improve outcomes.

I think they could be more efficient if they focussed on the implementation of the regulation rather than the development of regulation through comment letters.

Company Director

[The FRC] could be more worried about outcomes, and less about processes...they need to be thinking, are audits really fulfilling the purpose they were intended for?

Other

Secondly, several stakeholders feel the extensive scope of the work being undertaken at the FRC limits their favourability towards the regulator. In interviews, stakeholders commented that the breadth of the FRC's remit was too broad given its finite staffing resources or that resource is not deployed effectively in order to ensure that all areas of work are equally served. While some feel the quality of work produced by the FRC has improved in recent years, several stakeholders across a range of segments still feel the quality of output could be improved and the FRC would be better served by focusing its efforts as opposed to spreading itself too thin.

They are fine, and perfectly pleasant people but how much they are capable of seeing the big picture and thinking about things from first principles – I'm not hugely confident.

Actuary

Resourcing, staff turnover, and the fact that there isn't actually equal amount of focus put on governance and stewardship, as it is on accounting and actuarial work.

Institutional Investor

It almost has too wide a role, or it sees too wide a role, for its resources.

Other

Finally, for most stakeholders interviewed, there is a clear correlation between the depth of their relationship with the FRC and their favourability towards the regulator. Those who have an active relationship with the FRC (having attended various events, workshops, and/or felt they had a clear point of contact) feel they have a better understanding of the processes and constraints of the regulator and as such, were more favourable to the work being undertaken. Those who feel they have limited contact with the FRC, or were less familiar with the details of the regulator, were generally less favourable towards the FRC as they have less clarity on the work being undertaken. Given this, increasing engagement opportunities and proactive outreach targeting those with whom the FRC has a limited relationship with, could go a long way to increasing favourability towards the FRC.

It always feels like they care more about the regulation and the avoidance of anything bad happening rather than the greater good.

Actuary

EFFECTIVENESS OF COMMUNICATIONS

| Stakeholder | % |

|---|---|

| Insurance company director* | 57% |

| Company director | 60% |

| NED | 65% |

| Auditor | 79% |

| Insurance Actuary* | 100% |

| Pension Actuary* | 64% |

| Professional body* | 78% |

| Institutional investor | 79% |

Q27. Overall, how effectively, if at all, do you think the Financial Reporting Council communicates with its stakeholders? Base: All respondents (n=297)

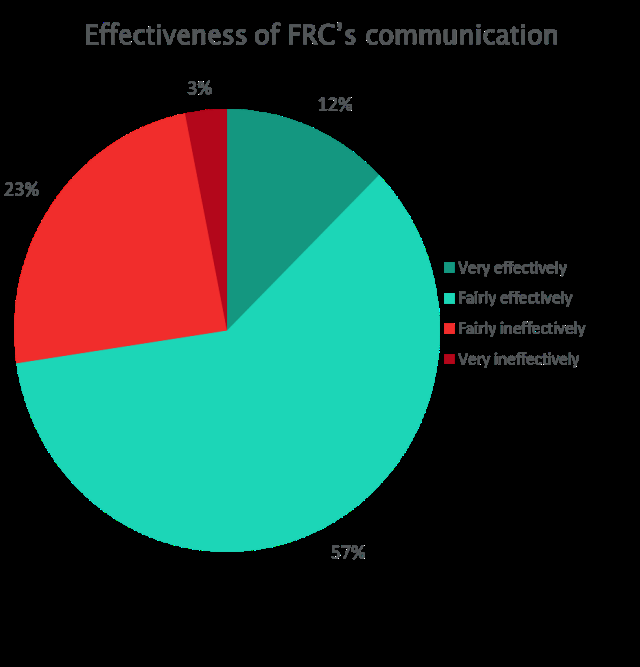

Over two-thirds (69%) of stakeholders say that the FRC is effective in this area. However, a quarter (25%) find the FRC ineffective in its communications, a view supported by many of the stakeholder interviews. Unsurprisingly, company directors and NEDs were the least likely to think the FRC communicates effectively (57%-60% and 65%, respectively), perhaps as a result of the more limited engagement with these audiences.

One issue arising from the interviews was inconsistency in communications. Some stakeholders commented they were in receipt of frequent communications from the FRC ranging from invitations to events to personal contacts, and as such, are pleased with the level of contact they received. Others however felt they received infrequent or inconsistent communications, and would like to see more targeted, regular communications. This view was not exclusive to any specific segment even within segments there could be a mixed experience. For example, around half of institutional investors we spoke with felt that communication was adequate and clear, while others had very limited communication, and expressed a desire for more.

They should do more small, round-tables, with groups of six to eight key industry stakeholders where they get real, valuable, face-to-face input.

Company director

We pay fairly hefty subscription for regulatory oversight and that, I think, has been responded to by the heightened engagement and support that we receive, but it's a tough call for the FRC because they do have a lot of stakeholders to keep happy.

Professional body

Engaging with the FRC face-to-face was frequently mentioned by stakeholders who had attended such events, for example roundtable meetings and the FRC Lab. These were seen as a positive and useful engagement opportunity to hear from both the FRC as well as others in their field. As such, these present an opportunity for the FRC to build and maintain relationships with stakeholders, particularly those who it may have had limited contact with in the past.

In addition, given that many stakeholders have a limited understanding of all the areas of the FRC's work, communications which explain more about the FRC's full remit could bring together different groups of stakeholders and increase transparency of the FRC's ways of working.

Finally, several stakeholders mentioned that the FRC has more limited visibility amongst the general public. This view was frequently mentioned by those in the 'Other' group as being an issue that the FRC needs to address. Although the FRC can be effective at communicating technical information to its stakeholders, it is seen as less good at communicating this with the public, particularly when compared to other regulators such as the FCA.

The quality, tenor, and tone of communications may need to change to reflect the times. Because of the nature of the subjects involved, it is highly technical and complex. So talking professional to professional – the FRC does this well. It is less good at getting out the war stories of success to non-expert and non-technical audiences.

Company director

INDEPENDENCE AND TRANSPARENCY

| Stakeholder | % |

|---|---|

| Insurance company director* | 86% |

| Company director | 79% |

| NED | 77% |

| Auditor | 94% |

| Insurance Actuary* | 100% |

| Pension Actuary* | 93% |

| Professional body* | 91% |

| Institutional investor | 55% |

Q14. How independent, if at all, do you think the Financial Reporting Council is from the audit profession? Base: all respondents (n=297)

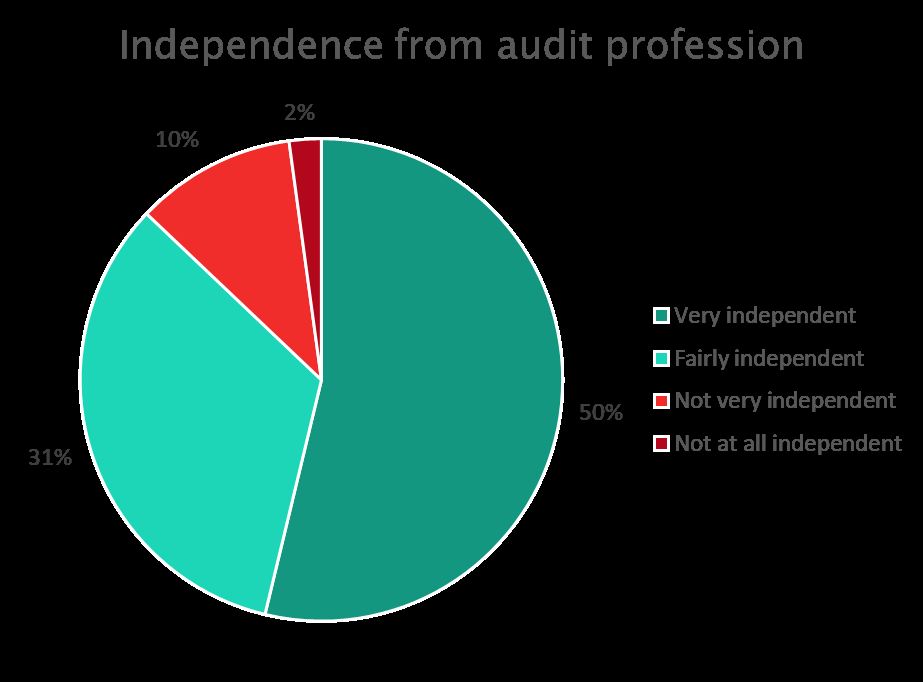

Positively, the majority of stakeholders (80%) consider the FRC to be independent of the audit profession. Nor is this view driven by auditors – excluding them from the sample results in a similar overall proportion (78%) who believe the FRC to be independent of audit.

However, institutional investors are least likely to find the FRC independent over one-quarter (29%) don't believe the FRC is independent of the audit profession. Reasons for this include the fact that the FRC hires many ex-auditors, a funding model which derives funds – in part – from audit firms, and a feeling that the FRC does not always hold auditors as accountable as they should be. In order to provide institutional investors with increased confidence in the FRC's independence, additional transparency around decision making and clear demonstration that conflict of interest policies are adhered to is needed.

Yes, I think they're independent from those that they regulate. I just think that they haven't taken a strong enough position. So, if we take, like I mentioned the audit profession, they introduced a new, sort of, public reports. Some of those reports were quite damning to the auditors but there was no consequence to it.

Institutional investor

I think they should be, but I think it's difficult if you're regulated by somebody who's funding you, and would cause potential conflicts.

Institutional investor

Often the investor view is not always felt to be represented through the governance structures of the FRC, but also that it is not often felt through their working approaches, because a lot of employees are ex-auditors and it's whether there's a sort of balance that needs to be re-struck there.

Institutional investor

I have never doubted, or I have never questioned, their independence.

Institutional investor

Beyond institutional investors, most stakeholders broadly consider the FRC to be independent. Stakeholders acknowledged that, as a regulator, the FRC needs to walk a fine line between engaging with audit enough to be knowledgeable about the industry, while also being independent enough to regulate. Most felt that the FRC achieves this balance, and consistently strives to maintain it. There was also an acknowledgment from several stakeholders that the FRC is under pressure from government to undertake certain actions e.g. the recent review of the UK Corporate Governance Code. If anything, several stakeholders felt the FRC was too focused on being seen as independent, and this should be of a lesser priority.

In my experience those regulators that withstand that criticism and work closely with the industry whilst being independent achieve a lot more than those that perhaps go out of their way to prove that they are not close to those that they're regulating, in order to satisfy another stakeholder.

Auditor

Stakeholders have a slightly more mixed view of the FRC's transparency. Although several acknowledged that improvements had been made in recent years, there was a sense that more could be done in this area. This reflects broader public and business attitudes towards regulators which expect greater transparency. In particular, stakeholders feel that on internal issues or processes, the FRC is less forthcoming, or the outcomes of reviews are not made available. Of note, the 'Other' segment of stakeholders were slightly more critical of the FRC's transparency, with several noting that while the FRC reviewed its own behaviour, it keeps its cards 'close to its chest'. As such, stakeholders across all segments, feel there is an opportunity for the FRC to increase its transparency by publishing clearer information about its processes. The FRC should be seen to hold itself accountable to the same standards which it requires of others. At the same time, there is an opportunity for the FRC to engage with a wider range of groups on initiatives, and be more outward looking in approach.

I think that the thing is, when you're setting standards of governance for other companies and telling companies what they should be doing, then you have to be whiter than white.

Other

Their judgement processes. They tend to be very close to their chest. If there's an issue raised with them about their judgements or their behaviours, they will tell you they have examined it, but they won't display what that examination showed, and what actions they took.

Other

I think they could do more to engage with the whole range of interests...they need to look for active ways of engaging with different views, different interests, different voices.

Other

Once again, where stakeholders are highly engaged with the FRC, there is a sense of understanding of the regulator and its processes. However, where stakeholders are less engaged, there exists less familiarity with internal structure and processes, which inhibits stakeholders' perceptions of transparency. In order to generate an increased sense of transparency, raising the FRC's profile and increasing communication with stakeholders about the FRC's work, strategy and processes would be welcome.

DISCIPLINE AND ENFORCEMENT

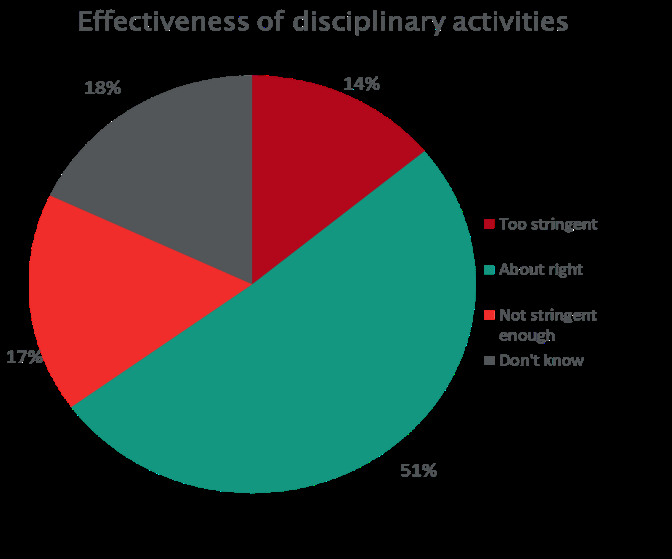

STRINGENCY

| Stakeholder | % |

|---|---|

| Insurance company director* | 29% |

| Company director | 55% |

| NED | 58% |

| Auditor | 42% |

| Insurance Actuary* | 73% |

| Pension Actuary* | 79% |

| Professional body* | 52% |

| Institutional investor | 31% |

Q24. In its enforcement of professional standards, do you think the Financial Reporting Council is... Too stringent/ Not stringent enough/ About right. Base: all respondents (n=297)

Half (51%) of stakeholders think the FRC's enforcement of professional standards are about right, with similar proportions believing the FRC is too stringent (14%) and not stringent enough (17%). Unsurprisingly, auditors were most likely to feel the FRC is too stringent (40%) while institutional investors were most likely to find the FRC not stringent enough (45%). As such, less than half of each of these stakeholder groups think the FRC is 'about right' in its enforcement activities. Given the diversity in stakeholder groups, it will be a challenge for the FRC to shift attitudes on the issue. Increasing transparency within the process may help generate more confidence in processes and outcomes.

However, stakeholders identified a number of improvements which could be made to the process both in terms of approach and outcomes.

I think it's about trying to encourage the right behaviours from the people they're regulating. Given that their job is to improve the quality of audits, they should be trying to make audit a very attractive profession and something which is highly valued. I think many of the things they do, do the opposite of that, they put people off going into audit.

Other

In terms of approach, several stakeholders across different stakeholder groups feel the FRC could first approach enforcement activities through dialogue with those involved, which would both offer the opportunity to resolve the opportunity without the need for full enforcement activities, while also being quicker.

It's the difference between an arbitration type settlement between businesses, and waiting for a full High Court judgement on a major contractual battle. The first one will probably solve the problem, and do it in a matter of months, or even weeks. The second one, it can literally take years, because you've got to gather all the evidence, prove to yourself all the evidence, audit all that evidence, have it ready for the equivalent of presentation in a court case, during which time you aren't discussing with whoever the offending, or potentially offending company is.

Other

In terms of outcomes, several stakeholders feel that the FRC ‘lacks teeth' as it is either unclear what its enforcement capabilities are, or that a large fine is not an appropriate deterrent. Similar to the views expressed around independence, some stakeholders questioned whether auditors are truly held accountable for their actions.

A few stakeholders commented that they feel a more forward-looking approach could be undertaken by the FRC; enforcement activities may punish the perpetrator, but they do not ultimately correct the problem. When disciplinary issues arise, they would like to see the FRC look to understand if the problem is representative of issues within the system itself that need to be rectified, before ultimately undertaking enforcement activities.

When a plane falls out of the sky, the initial focus doesn't really seem to be on, ‘Who can we sue,' or, ‘Who goes to jail?' It's on, ‘How do we stop it happening again?' Just that mind-set is very different to that which seems to currently exist within the enforcement function.

Auditor

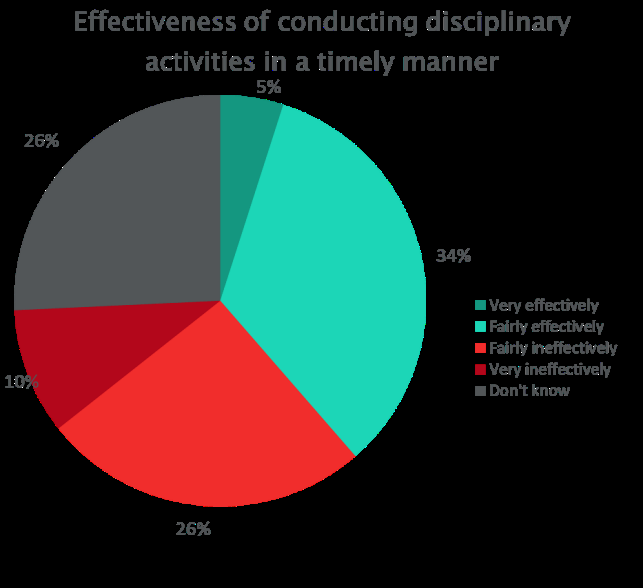

TIMELINESS

| Stakeholder | % |

|---|---|

| Insurance company director* | 29% |

| Company director | 47% |

| NED | 35% |

| Auditor | 21% |

| Insurance Actuary* | 64% |

| Pension Actuary* | 57% |

| Professional body* | 48% |

| Institutional investor | 19% |

Q28. How effective, if at all, would you say the Financial Reporting Council is at conducting its disciplinary and audit enforcement activities in a timely manner? Base: all respondents (n=297)

Although many stakeholders understand that the FRC has specific processes for disciplinary and enforcement activities, and the need for balance in this process, they were relatively evenly split on the effectiveness of the FRC conducting disciplinary and audit enforcement activities in a timely manner, with 38% finding the FRC effective and 36% finding it ineffective. Notably one-quarter (26%) said they 'don't know', perhaps suggesting that, again, more transparency and visibility is needed.

Feedback from stakeholder interviews across all groups erred towards the FRC being ineffective, with many wishing to see the FRC be timelier in its activities. There was a sense that too much time elapses between an incident and reporting of findings, making action more difficult and less relevant. As part of this, some questioned the FRC's efficiency and whether it had the capacity to undertake activities in a more timely manner.

I think one's biggest criticism is possibly it's a slow process...one understands that part of the reason for that is very careful internal quality control review processes, which, of course, in principle, one supports, but, you know, I think that does need to be balanced with due speed, and being up-to-date.

Auditor

I don't know whether the organisation has enough capacity...to maybe increase the speed of those investigations and enforcement activities, I don't know whether that's partly related to the organisation itself or the capacity with the FRC.

Institutional investor

VISIBILITY

In interviews, stakeholders expressed a desire for increased visibility of disciplinary and enforcement activities. While those who were familiar with the processes at the FRC, for example professional bodies, felt it was clear which processes were being undertaken, there was a desire from stakeholders to see more information about enforcement activities. Although a need for discretion or confidentiality was acknowledged, stakeholders felt that improving visibility of both actions and outcomes would demonstrate the FRC's enforcement activities and increase the transparency of the work the FRC is doing in this area. This would be particularly welcome given the recent negative press around the FRC's links to the audit profession and closure of high-profile investigations.

I don't think you can totally remove the conflict of interest, but I think, what you can do, is be transparent about them, and if necessary, disclose specific cases, during the year, where there have been, or could be perceived conflicts of interest and how they dealt with them. I think that's the only way one is going to try and remove that doubt.

Institutional investor

They probably could be more visible as a way of informing the public and engendering confidence in the public... I think if there's more of that media engagement, I think that would help.

Professional body

I think if bad things are happening, then perhaps it needs to be a little bit more public, you know, to set an example, then. Showing that they have teeth.

Company director

I think their visibility has increased in the least year.

Institutional investor

FRC'S AREAS OF WORK

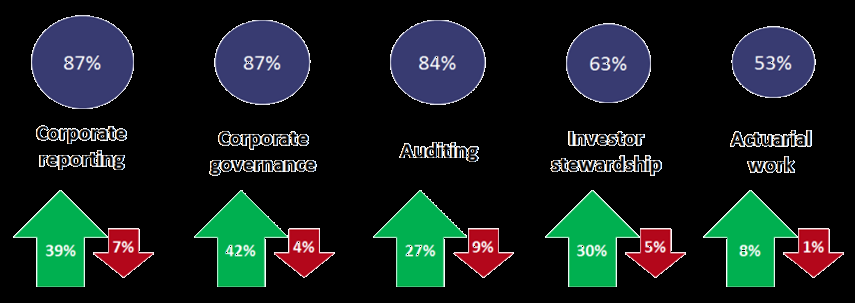

Stakeholder confidence in corporate reporting, governance and audit is broadly high at 87% for reporting and governance, and 84% for audit. Familiarity with, and confidence in, investor stewardship and actuarial work is lower. In particular for actuarial work, where stakeholder confidence is lower, this is more often as a consequence of a lack of familiarity with the area. For example, a majority (53%) report that they are confident in the quality of actuarial work but just 4% say they are unconfident. Instead, similar proportions report that they are neither confident nor not confident (19%) or say they don't know (24%), indicative of a lack of knowledge in this area.

Amongst stakeholder groups, institutional investors are least likely to be confident in most of the areas tested in comparison to NEDs, in particular in corporate reporting (79% vs. 97% respectively), audit (67% vs. 94%) and actuarial work (31% vs. 58%). However, institutional investors are more likely than auditors to be confident in the quality of investor stewardship (71% vs. 46% respectively) and corporate governance (95% vs. 73%).

Confidence in the corporate reporting and governance, and change in confidence over time

Q2. How confident, if at all, would you say you are in the quality of each of the following components of corporate governance and reporting in the UK? Q3. Would you say your confidence in the quality of each of the following has increased, decreased or stayed about the same over the last 2 years in the UK? Base: All respondents (n=297)

Stakeholders are more likely to say that their confidence has increased rather than decreased (42% increased vs. 4% decreased for corporate governance). NEDs are most likely to report that their confidence has increased in corporate governance (58% vs. 33% auditors and institutional investors), corporate reporting (55% vs. 23% auditors) and audit (42% vs. 24% company directors). In contrast, institutional investors are more likely than company directors to say their confidence in investor stewardship has increased (55% vs. 23% company directors).

CORPORATE REPORTING

Stakeholders are broadly positive about the FRC's work in corporate reporting; nine in ten are familiar with the FRC's work in this area (90%) and a slightly lower proportion find that its work is effective (85%). While overall, each stakeholder group is equally likely to say they are familiar with corporate reporting, auditors are significantly more likely than institutional investors to report being very familiar with this area of the FRC's work (60% vs. 29%). Institutional investors are also least likely to say that the FRC's work in this area is very effective (12% vs. 29% company directors).

Familiarity with and effectiveness of the FRC's work in...

| Familiarity with the FRC's work in... | CORPORATE REPORTING | Effectiveness of the FRC's work in... |

|---|---|---|

| 90% | 85% |

Q6. And how familiar or unfamiliar would you say you are with the Financial Reporting Council's work in each of the following areas? Q7. How would you rate the effectiveness of the Financial Reporting Council's work in each of the following areas in the UK? Base: All who are familiar with the FRC (n=291)

Seven in ten stakeholders (70%) use annual reports and accounts as a primary means to find out information and a majority (56%) say that this is most useful to them. Institutional investors are most likely to use annual reports and accounts to find out information, with more than four in five (86%) reporting this compared to half of auditors (54%). Consistent with this, institutional investors find annual reports and accounts most useful compared to auditors (68% vs. 40%). A majority of stakeholders (55%) use annual reports and accounts to a great extent to understand the underlying financial performance and position of a company and find the financial performance, position and cash flows as the most useful information (58%) in annual reports and accounts.

Given the importance of annual reports in finding out key information about a company, stakeholders across all groups felt reports could be improved by decreasing their length and the amount of 'boiler-plate' text. It was felt that companies were being asked to report on an ever increasing number of issues, which could often lead to box-ticking rather than taking the time and care that could help to deliver more effective reporting.

The problem we have is that firms are required to report against an ever-expanding number of issues. Many of which are increasingly social, environmental, based around diversity etc. I think whether they are simply a box-ticking exercise or whether they provide meaningful and comparable information to third parties, investors, is an open question.

Other

The constant stream of pointless changes to the corporate reporting requirements [needs to be changed].

Company Director

I think the big challenge that companies have, is that company reports are getting longer and longer, and unfortunately, the language used, tends to be written in such a generic-type way, that it's not really that useful.

Institutional Investor

CORPORATE GOVERNANCE

I think they do a lot of very good and proactive work in this area and that's probably an area where I've been very happy with my engagement with them... their openness to meet and discuss is in contrast to certain other regulators.

Other

Further to this, over one-third (35%) feel that environmental, social and community matters could be communicated through other means, the option most selected by stakeholders. Some stakeholders suggested that reporting on environmental sustainability and corporate social responsibility could be placed on company websites where real time updates would allow greater accountability than a yearly announcement through the annual report. This would help to slim down annual reports and focus them on the areas that are most used and most effective for stakeholders.

Focusing annual reports and accounts on the financial areas of companies and relocating company values could improve the usefulness of annual reports and ensure they are fit for purpose.

Similar to corporate reporting, stakeholders are broadly confident with the FRC's work in corporate governance. Nearly nine in ten report being familiar with the FRC's work in this area (87%) while four in five perceive it to be effective (80%). While stakeholders are equally likely to be familiar with and find the FRC's work effective in corporate governance, institutional investors are significantly more likely than company directors to say they are very familiar with the FRC's work in corporate governance (60% vs. 33%). This confidence was reflected in interviews, where stakeholders often pointed out that the UK Corporate Governance Code has been mirror globally, and adopted as best practice.

Familiarity with and effectiveness of the FRC's work in...

| Familiarity with the FRC's work in... | CORPORATE GOVERNANCE | Effectiveness of the FRC's work in... |

|---|---|---|

| 87% | 80% |

Q6. And how familiar or unfamiliar would you say you are with the Financial Reporting Council's work in each of the following areas? Q7. How would you rate the effectiveness of the Financial Reporting Council's work in each of the following areas in the UK? Base: All who are familiar with the FRC (n=291)

What we have is recognised globally as the best practice, so lots of other countries adopt a very similar approach to us. Lots of other companies in the UK who are not subject to the code will nevertheless adopt it as best practice.

Other

I'm not really sure that the FRC is necessarily best placed to be leading on corporate governance... because it's not simply a financial issue... There isn't, I guess, the weight of legislation behind corporate governance that leads to that compliance.

Professional Body

At the same time, stakeholders also feel that the Code is updated too frequently, with unclear benefit of revisions. While appreciative of the consultations, stakeholders did not feel it was necessary to constantly adapt things following this process, as it often appears as though the FRC are making changes for the sake of it.

Constant evolution is important, but, the constant adding of requirements, adding of requirements, adding of requirements, takes away the fundamentals of what they were trying to achieve in the first place.

Auditor

I don't think there's an appetite for a complete overhaul. I think if we were to write it from scratch now it would look very different.

Institutional Investor

The one danger that I think the FRC needs to look out for is looking to make change almost for the sake of making change when it does a review, rather than a substantive need.

Auditor

For some, this was perceived to be because of the length of time the Code has been in existence, being drawn up in the 1990s and with only amends being made to it, as opposed to a re-evaluation of the entire process. Stakeholders are aware of the difficulty in maintaining consistency and delivering quality of governance but also ensuring that it is fit for practice, reflecting the world that they work in. A significant challenge for the FRC moving forward is how best they can maintain standards that stakeholders are familiar with, as well as updating the Code where relevant to take into account changing circumstances.

It's a confused system and I think the FRC should give itself some time to reflect on the overall requirements of the governance code, rather than constantly trying to renew and refresh it.

Company Director

AUDIT

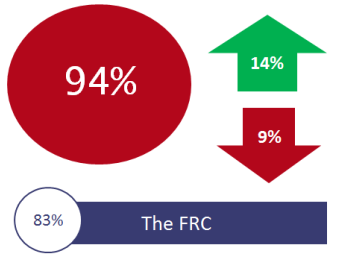

Stakeholder familiarity and perceived effectiveness of the FRC's work in audit is high. Four in five report being familiar with the FRC's work in audit and perceive it to be effective (80% and 81% respectively). Furthermore, more than nine in ten stakeholders say they are confident in the integrity of the UK audit profession (94%); 14% say that their confidence has increased over the last year, though 9% say it has decreased.

Familiarity with and effectiveness of the FRC's work in...

| Familiarity with the FRC's work in... | AUDITING | Effectiveness of the FRC's work in... |

|---|---|---|

| 80% | 81% |

Q6. And how familiar or unfamiliar would you say you are with the Financial Reporting Council's work in each of the following areas? Q7. How would you rate the effectiveness of the Financial Reporting Council's work in each of the following areas in the UK? Base: All who are familiar with the FRC (n=291)

It is worth highlighting that, of all stakeholders, institutional investors are notably more pessimistic about audit than other stakeholders. Although they are least likely to report being familiar with the FRC's work in audit (62% vs. 71–100% of other stakeholders) they were also most likely to say this work is not effective (26% vs. 8-16% of other stakeholders). Although a knowledge gap may account for these views, it may be more reflective of institutional investors broader attitudes towards audit; they had the lowest confidence of all stakeholders in the overall quality of audit in the UK (67% vs. 88-94% of other stakeholders) while also saying that confidence had decreased in the past 2 years (21% vs. 2–11% of other stakeholders). This may also be linked to institutional investor's view that the FRC's enforcement activities could be made more stringent. As such, further efforts by the FRC to address institutional investors' concerns around audit, may help improve confidence.

[Auditors] haven't been able to communicate the findings in an effective way for it to be utilised and resonate with stakeholders whether they be investors or companies.

Institutional Investor

I think [the FRC's] oversight of the audit profession has been, I don't want to say weak but not as effective as it could have been.

Institutional Investor

That acknowledged, stakeholders are happy with the FRC's work in audit, but are likely to suggest that minor tweaks could improve the FRC's work in this area further. In particular, on the issue of standard setting stakeholders pointed out that the FRC follows international standards, causing it to be limited when considering what would be useful for the UK while also maintaining global consistency. Ensuring a balance between global and UK standards should be a priority for the FRC in this area.

Its hands are slightly more tied on audit and accounting, because it follows international standards, largely. You know, you are in a position of always making a trade-off between what might be arguably sensible from a UK context, but then steps out of line in terms of achieving global consistency.

Auditor

Confidence in the integrity of the UK audit professions, change in confidence and responsibility for the quality of audit

Positively for the FRC, stakeholder confidence in the integrity of the audit profession of the UK is high at over nine in ten (94%), with more stakeholders reporting that this confidence has increased (14%) rather than decreased (9%) over the last year. Given the high amount of confidence in the audit profession, it is encouraging that stakeholders associate the FRC with being responsible for the quality of audit in the UK (83%), significantly higher than the two thirds (66%) who say this of audit firms. Perhaps as could be expected, institutional investors are least likely to report being confident in the integrity of the UK audit profession (81%).

Q17. How confident, if at all, are you of the integrity of the UK audit profession? Q18. How has your confidence in the integrity of the UK audit profession changed over the last year? Has it... Q20. Which parties, do you think are responsible for the quality of audit in the UK? Base: All respondents (n=297)

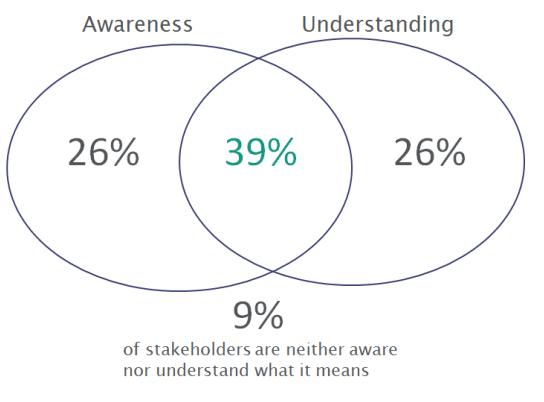

Following the FRC becoming the single competent authority for audit in June 2016, two in five stakeholders report that they are both aware and understand what this means (39%). Similar proportions report being aware but not understanding, or say they understand but are not aware of what this means (26% for both). Just 9% are neither aware nor understand what this means.

Awareness and understanding of the FRC becoming the single competent authority for audit

Q19. In June 2016, the Financial Reporting Council became the single competent authority for audit. Before today, is this something you were aware of? Base: All respondents (n=297)

Company directors are least likely to say this (21%). Instead, company directors are most likely to understand what the change means, but have not been previously aware of it (38%), indicating a need for greater communication with this group. In contrast, more than a third of institutional investors (36%) are aware of the change but don't understand what it means. This suggests that while communications may be high with this group there is room for greater engagement.

Efforts to improve confidence in audit

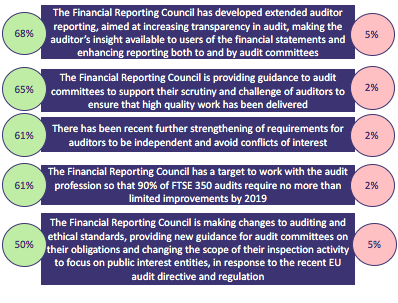

When considering what further actions the FRC could undertake to improve stakeholder confidence in audit, at least half of all stakeholders reported that if they implemented any of the measures tested that their confidence in audit would increase (50% for the FRC making changes to auditing and ethical standards) and between 2-5% report that these actions would decrease their confidence.

Q15. For each of the following, can you tell me whether it increases, decreases, or makes no difference to your confidence in audit? Base: All respondents (n=297)

Institutional investors are most likely to say that the statements tested would improve their confidence in audit, consistent with their already low levels of confidence in this area. Nine in ten institutional investors (90%) say that the FRC's development of extended auditor reporting to increase transparency in audit would increase their confidence, while a further seven in ten (71%) say the recent further strengthening of requirements for auditors to be independent and avoid conflicts of interest would improve their confidence.

INVESTOR STEWARDSHIP

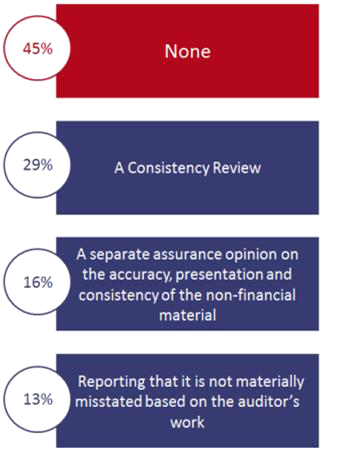

Nearly half of stakeholders (45%) feel that there is no assurance an auditor could provide over non-financial material contained in an annual report. Three in ten feel a consistency review would be useful (29%) and similar proportions want to see a separate assurance opinion and reporting that is not materially misstated based on the auditor's work (16% and 13% respectively). Institutional investors are most likely to want additional assurance; a quarter reported that they would like a separate assurance opinion (26%) compared to just one in nine company directors (11%). One in five institutional investors would like to see reporting that it is not materially misstated based on the auditor's work (19%) whereas just 2% of auditors say the same.

Other means of assurance auditors could provide

Q16. What assurance, if any, should an auditor provide over non-financial material contained in an annual report? Base: All respondents (n=297)

With the exception of concerns from institutional investors, audit is seen to be in a broadly positive position. As evidenced, undertaking any of the actions tested and ensuring positive communication about them to stakeholders will help to increase confidence in the audit profession. Ensuring communications and engagement are consistent among all stakeholders could also help to increase stakeholder awareness and understanding of the FRC's role as the single competent authority for audit. Further reassurances to institutional investors should be a focus for the FRC moving forward in order to improve their confidence in the audit profession.

More than half of stakeholders report that they are familiar with the FRC's work in investor stewardship and perceive it as effective (59% and 52% respectively). This is most marked among institutional investors, with nine in ten (90%) saying they are familiar, compared to half of company directors who say they are familiar (50%, with an equal number saying they are unfamiliar).

Familiarity with and effectiveness of the FRC's work in...

| Familiarity with the FRC's work in... | INVESTOR STEWARDSHIP | Effectiveness of the FRC's work in... |

|---|---|---|

| 59% | 52% |

Q6. And how familiar or unfamiliar would you say you are with the Financial Reporting Council's work in each of the following areas? Q7. How would you rate the effectiveness of the Financial Reporting Council's work in each of the following areas in the UK? Base: All who are familiar with the FRC (n=291)

However, some stakeholders feel that specific areas of the FRC's work, such as the UK Stewardship Code, has not made a significant impact on the work of investors. In particular, stakeholders hoped the FRC would be more forward and international looking. While there was an acceptance that it is difficult to apply something outside of the FRC's remit, there was a desire that the global, interconnected nature of business should have been taken into account more when designing the Code.

Investors will be as interested in stewardship as they want to be. You know, the Stewardship Code is all jolly good, but do I really think it's made any great difference... I rather doubt it.

Auditor

A much greater internationalisation of share ownership, which means that very significant holders of shares in many of our major companies are overseas-based and therefore rather more distant from companies in which they invest and rather less engaged in any active stewardship of their holdings. Those are fundamentals that the FRC and its Code are having to adjust to but it will take bigger forces than the FRC to change some of those very big global trends.

Other

Not all the shareholders in our companies are UK based, who would then be subject to the Stewardship Code and to the FRC. So, where we have difficulties on stewardship type things with engagement in shareholders, it's generally with our overseas shareholders. The FRC didn't have any remit for them.

Company Director

Other stakeholders were more positive, highlighting how the Code is now the global standard and in some respects the FRC has become a source of guidance for future governance and regulation. Stakeholders also commented that the recent tiering of signatories has been useful. At the same time, stakeholders felt that perhaps more could be done by the FRC in this area by bringing investors with them and involving them more in the processes rather than just setting out the Code and expecting investors to follow.

On the Investor Stewardship Code, it was progressive to the point where every market around the world now is using the UK standard as the gold standard that they're copying.

Institutional Investor

I think the question is whether the FRC could have been slightly harder in hauling investors along. I mean, there's no doubt that what it's done has been helpful, I think the question there is, ‘Could they have done more?'

Auditor

While opinion appears somewhat split amongst stakeholders on the specifics, stakeholders overall are positive towards the Code, with a desire amongst some for the FRC to go further in the involvement of institutional investors and ensure that they consider the global outlook as well as the UK context.

Familiarity with and effectiveness of the FRC's work in...

| Familiarity with the FRC's work in... | ACTUARIAL WORK | Effectiveness of the FRC's work in... |

|---|---|---|

| 22% | 32% |

Q6. And how familiar or unfamiliar would you say you are with the Financial Reporting Council's work in each of the following areas? Q7. How would you rate the effectiveness of the Financial Reporting Council's work in each of the following areas in the UK? Base: All who are familiar with the FRC (n=291)

ACTUARIAL WORK

Of the areas of work that the FRC is involved in, stakeholders are least familiar with actuarial work (22% vs. 69% not familiar). This, in turn, impacts on the perceived effectiveness amongst stakeholders (32%); more than half (56%) say they don't know whether the FRC is effective in this area. This is indicative of a lack of stakeholder knowledge of actuaries more broadly; a third (33%) report that they have never come into contact with an actuary. This led to a number of stakeholders perceiving actuarial work as effective from the limited contact they have although they are unable to make a comment beyond this.

Sectors stakeholders have interacted with actuaries in

Q22. In which of the following sectors, if any, have you mainly interacted with actuaries? Base: All non-actuaries who have had contact with actuaries (n=177)

Among stakeholder groups who are not actuaries, auditors are most likely to report being familiar with actuarial work (27% vs. 12% company directors) but all stakeholders are equally likely to report that the FRC's work in this area is effective. However, significant proportions say they don't know; 55% of NEDs and seven in ten (71%) institutional investors say this. As such, there is a great amount of scope for FRC to increase the profile of actuarial work as a whole, and the work it undertakes in this area.

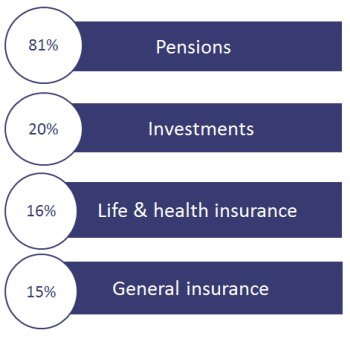

Among those who do come into contact with actuaries, that contact has primarily come through pensions (81%), while just one in five say they have had this contact via investments (20%) and similar proportions say the same of life & health and general insurance (16% and 15% respectively). There is no significant difference amongst stakeholders.

There is a sense amongst stakeholders familiar with actuarial work that it is of lower priority for the FRC compared to other areas, and that the actuarial profession in general has a more limited profile. As mentioned, increasing the internal and external profile on actuarial work could help to redress this balance.

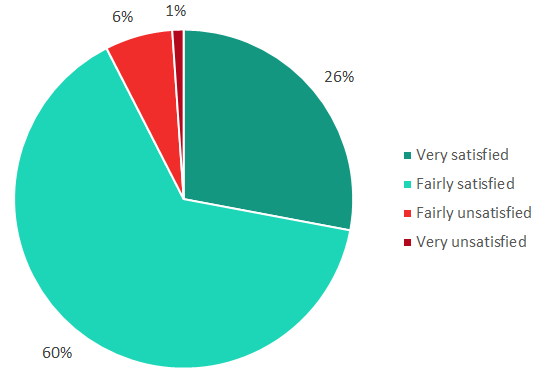

Stakeholders' satisfaction when interacting with actuaries

Q24. When you have interacted with actuaries, how satisfied, if at all, have you been with the quality of their work? Base: All non-actuaries who have had contact with actuaries (n=177)

We're small compared with the rest of the stuff that the FRC has to do. So, we will never be at the top of the agenda when it gets to something big.

Actuary

So if I look at a profile of the work that it does, whether it's stewardship, whether it's governance, whether it's corporate reporting, whether it's audit, all of those seem to have a degree of profile. Actuarial is somewhat lost.

Auditor

Despite this, stakeholders who have had contact with actuaries are satisfied overall with the quality of actuarial work. More than four in five (86%) report being satisfied and a quarter report that they are very satisfied (26%). Furthermore, when considering actuaries' communications, nine in ten stakeholders report that their communications are clear (89%). This is consistent across stakeholder type.

The FRC's laying down certain standards, but the actuarial profession is keeping an eye on that, and also, other aspects of things I have to comply with. I'm very happy with how that structure between the FRC and the actuarial profession operates.

Actuary

Clarity of communications from actuaries and safeguards' importance in ensuring high quality actuarial work

Q25. Thinking about the communication and advice you have received from actuaries, has this been clear enough to enable you to effectively make decisions? Base: All non-actuaries who have had contact with actuaries (n=177) Q26. Please rank the following three safeguards in terms of their importance in ensuring high quality actuarial work? Base: All respondents (n=297)

Stakeholders were also asked which safeguards are most important in ensuring high quality actuarial work. A majority report that maintaining professional standards is most important (53%), around three in ten say the regular monitoring of standards (27%) and a further two in five say the enforcement of standards (20%). However, institutional investors are significantly more likely than any other stakeholder group to report that the enforcement of standards is most important, with nearly half (48%) ranking this as most important, compared to one in ten auditors (10%) who say the same. A third of institutional investors (33%) rank maintaining professional standards as important compared to seven in ten auditors who say the same (69%). This is indicative of the different priorities of each stakeholder group, with investors more likely to be concerned with the enforcement of standards than other groups.

Amongst the actuaries interviewed, there was some blurring between where the responsibilities of the FRC and the Institute and Faculty of Actuaries began and where they ended, in particular around the Institute developing a more active approach to a peer review process, similar to that which the FRC currently does for audits. There was some confusion as to why the Institute was developing this and whether the FRC should be more proactive in improving actuarial work in the future.

Where do the FRCs responsibilities end and where do the Institute start... the question that forms a little bit in your mind is, you know, why is the Institute developing that rather than the FRC.

Actuary

I did particularly find that I thought they did a good job of the roll out of the new technical actuarial standards. The standards themselves were well thought through but then the way they promulgated them was also well done, I thought.

Actuary

I think the only thing I would say that is possibly undermining, is changing things in a very short period of time, because it implies that you rushed the first thing out, and then you went, a year later, ‘Oh, whoops. We did that wrong.' I think that has happened maybe a couple of times on the actuarial standards.

Actuary

Other concerns from actuaries mirrored similar worries from other stakeholders regarding the changing and updating of standards in a short period of time. For some, it caused them to perceive these actions as being rushed, and actuaries were keen to see more consideration taken regarding this in order to avoid confusion and reduce any unnecessary issues.

| LONDON | BRUSSELS | SHANGHAI |

|---|---|---|

| Four Millbank | Rond Point Schuman 6 | 51/F Raffles City |

| London | Box5, 1040 | No.268 Xi Zang Middle Rd |

| SW1P 3JA | Bruxelles | HuangPu District Shanghai |

| T: +44 (0)20 7871 8660 | T: +32 (0)2 234 63 82 | 200001 China |

| F: +44 (0)20 7799 2391 | F: +32 (0)2 234 79 11 | T: +86 (0)21 2312 7674 |

| E: [email protected] | E: [email protected] | E: [email protected] |