The content on this page has been converted from PDF to HTML format using an artificial intelligence (AI) tool as part of our ongoing efforts to improve accessibility and usability of our publications. Note:

- No human verification has been conducted of the converted content.

- While we strive for accuracy errors or omissions may exist.

- This content is provided for informational purposes only and should not be relied upon as a definitive or authoritative source.

- For the official and verified version of the publication, refer to the original PDF document.

If you identify any inaccuracies or have concerns about the content, please contact us at [email protected].

FRC Climate Thematic – Corporate Reporting

- Introduction

- Background

- The challenges of climate change

- How might disclosure respond?

- Reporting requirements in relation to climate change – narrative reporting

- Reporting requirements in relation to climate change – financial statements

- The Financial Reporting Lab report

- The Task Force on Climate-related Financial Disclosures

- Our findings and expectations on reporting

- Narrative reporting

- Impact of climate change on the company

- TCFD disclosure

- FRC view on reporting frameworks

- Risk disclosure

- Physical and transitional risks

- Climate-related risk process

- Lab insight - investor views on risk management

- Opportunities

- Scenario planning

- Materiality

- IMPACT OF THE COMPANY ON CLIMATE CHANGE AND THE EXTERNAL ENVIRONMENT

- Commitment-setting

- Board practice

- Lab findings – investor views on target-setting

- Outcomes of environmental policies and Key Performance Indicators (KPIs)

- Impact of the business on the environment

- Greenhouse Gas Emissions (GHG) disclosures

- Upstream and downstream of Unilever operations (scope 3)

- Section 172 and stakeholder engagement

- Financial statements – headline finding:

- Climate change in the financial statements

- Extent of climate disclosure in the financial statements

- Reporting requirements in relation to climate change

- Consistency between narrative reporting and financial statement disclosures

- UK Corporate Governance Code

- Materiality

- IAS and IFRS requirements - Materiality

- Lab finding - investor views on financial statements implications

- TCFD assessment of possible financial statements implications of climate change

- Impairment reviews

- IAS requirements – Impairment disclosures: cash-generating units (CGUs) containing goodwill or intangible assets with indefinite useful lives (IAS 36.134-135)

- Commodity price assumptions – insights from a specific review

- FRC climate thematic – audit

- Climate scenarios – implications for the financial statements

- Accounting for climate change

- Useful lives of assets

- Judgements and estimates

- Segmental reporting and disaggregated revenue disclosures

- Other forward-looking assumptions

- Appendix – Scope

Introduction

Throughout 2020, the Financial Reporting Council (FRC) has been undertaking a thematic review of climate-related considerations by boards, companies, auditors, investors and professional associations. This report forms part of that review and addresses the question ‘how are companies developing their reporting on climate-related challenges?'.

Other aspects of the FRC's findings can be found at the following links:

- The consolidated findings across corporate reporting and audit can be found here.

- The detailed findings on governance can be found here.

- The detailed findings on audit can be found here.

- The detailed findings on professional oversight can be found here.

- The detailed findings on investor reporting and better practice reporting under the Task Force on Climate-related Financial Disclosures can be found here.

KEY TO SYMBOLS

We use the following key to identify specific elements of reporting, to identify requirements or recommendations, and to identify better practice disclosure. 'Mandatory requirements' relate to the Companies Act or IFRS, for instance. 'TCFD and other guidance' includes publications and guidance which is not required, but may be better practice or reflect investor expectations.

Represents good practice

Represents an omission of required disclosure or other issue

Represents an opportunity for enhancing disclosures

Mandatory requirements

TCFD and other guidance

Examples of better disclosure

Highlighting aspects of reporting by a particular company should not be considered an evaluation of that company's reporting as a whole. Nor does it provide any assurances of the viability or going concern of that company and should therefore not be relied upon as such. Investors have contributed to this project at a conceptual level. The examples used illustrate the principles and should not be taken as confirmation of acceptance of the company's reporting more generally.

The diagram illustrates the interconnected elements of Corporate Reporting. It shows Corporate Reporting at the center, influenced by:

- Audit

- Professional Oversight

- Company approach and disclosure (leading to Corporate Reporting)

- Investors

- Governance

We asked: How are companies developing their reporting on climate-related challenges?

Why is this important?

As climate change has the potential to impact societies and companies around the world, companies are, and will need to, respond to its far-reaching impacts.

Corporate reporting provides a link between a company and its investors. Reporting about how a company is considering climate-related impacts on its business model, its risks and opportunities, the impact the company has on the environment and the financial statements impacts of climate-related considerations now and in the future provides a key insight for investors. It helps them understand the future the company faces, and the future it intends to help bring about.

What did we do?

We assessed a sample of 24 companies' annual reports and accounts to see whether they complied with the requirements of the Companies Act 2006, including reporting in accordance with International Financial Reporting Standards. The sample, which was based primarily on December 2019 annual reports, was weighted towards sectors and industries which are perceived to face greater risks concerning climate change.

We assessed a sample of 60 premium-listed companies' governance structures and references to climate-related considerations in the context of the UK Corporate Governance Code.

We spoke to investors to re-test their views to see if, and how, they had developed since the publication of the FRC Lab's 2019 report on climate-related corporate reporting.

What did we find?

An increasing number of companies are providing narrative reporting on climate-related issues. While minimum legal requirements are often being met, users are calling for additional disclosure to inform their decision making. Some companies have set strategic goals such as ‘net zero', but it is unclear from their reporting how progress towards these goals will be achieved, monitored or assured.

Consideration and disclosure of climate change in the financial statements lags behind narrative reporting. We identified areas of potential non-compliance with the requirements of International Financial Reporting Standards (IFRS).

Background

The challenges of climate change

The Paris Agreement aims to strengthen the response to climate change by: "Holding the increase in the global average temperature to well below 2°C above pre-industrial levels and pursuing efforts to limit the temperature increase to 1.5°C above pre-industrial levels, recognising that this would significantly reduce the risks and impacts of climate change", amongst other aims.

A serious reallocation of resources would be required to meet these goals, and therefore companies can be exposed to a wide range of risks and opportunities. Below is a high-level overview of some of the physical and transitional risks and opportunities companies will face. Climate change considerations are obviously relevant for entities across many industries and will therefore be relevant for their reporting and their financial statements.

| Physical risks | Transition risks | Opportunities |

|---|---|---|

| Long-term changes to weather and climate at a regional and international level | Impact of changing policy and regulation | Resource efficiency |

| Risks of acute events such as floods, droughts and storms | Reputational damage | Energy source |

| Changing consumer preferences and concerns | Products and services | |

| Changes in technology to respond to climate concerns | Markets | |

| Resilience |

Figure 1: Possible physical risks, transitional risks and opportunities companies may face, as identified by the Task Force on Climate-related Financial Disclosures.

How might disclosure respond?

While 'climate change' is not specifically mentioned as a required topic for reporting, there are a number of ways in which climate-related issues may still need to be disclosed.

Reporting requirements in relation to climate change – narrative reporting

Narrative reporting requirements and expectations relate to both the company's impact on the environment, where climate change may be relevant for some companies, and the impact climate change may have on the future of the business.

There are a number of Companies Act requirements for companies to report on environmental-related matters, or areas where climate-related considerations may be material, for example their company's strategy.

The UK Corporate Governance Code 2018 also includes some reporting expectations for which climate-related considerations may be relevant.

How we considered these narrative reporting requirements and associated expectations in our thematic review is outlined on page 6.

Reporting requirements in relation to climate change – financial statements

Companies may also need to report on the financial implications of climate-related challenges they face. The range of physical and transitional risks, and opportunities, highlights the wide consideration that needs to be given to the possible financial impacts of climate change.

There is no standalone IFRS which addresses climate change specifically. However, the requirements of IFRS standards provide a clear framework for incorporating the risks of climate change into companies' financial reporting. These apply, for example, to measurement uncertainty associated with forward-looking assumptions and estimates, and the related disclosures.

In November 2019, a member of the International Accounting Standards Board (IASB) provided an overview of existing IFRS requirements and guidance on the application of materiality in the article 'IFRS Standards and climate-related disclosures' (IASB article). The article does not have the status of a standard and does not provide a complete 'checklist' of relevant requirements but does provide helpful insight into how climate change should be considered when addressing certain requirements. The article also emphasises the existing materiality requirements and guidance.

The Financial Reporting Lab report

The Financial Reporting Lab's 2019 report on climate-related disclosure outlined investors' views on the integration of climate-related considerations into company activity and reporting. This report found that investors were very interested in climate-related reporting, and the investors we spoke to were very supportive of the Task Force on Climate-related Financial Disclosures (TCFD) frameworks of 11 recommended disclosures across four core areas as a framework for companies to think through, and report on, their climate-related activities.

Climate change can be a new consideration, so in order to help companies consider what they might report in the context of the TCFD recommendations, the Lab's report outlines a series of questions investors encourage companies to ask themselves in relation to governance, strategy risk management and metrics and targets.

The report highlighted examples of the developing area of reporting, and whilst those developments were welcomed, investors noted that reporting needed to continue to develop to better meet their needs. We spoke to a range of investors as part of the 2020 thematic and the views remain very similar.

The Task Force on Climate-related Financial Disclosures

The TCFD, established in December 2015 by the Financial Stability Board, was tasked with reviewing how the financial sector could take account of climate-related issues. In 2017, the TCFD published a report which set out four core elements of recommended climate-related financial disclosures that apply to organisations across sectors and jurisdictions:

- Governance: The organisation's governance around climate-related risks and opportunities.

- Strategy: The actual and potential impacts of climate-related risks and opportunities on the organisation's businesses, strategy, and financial planning.

- Risk Management: The processes used by the organisation to identify, assess, and manage climate-related risks.

- Metrics and Targets: The metrics and targets used to assess and manage relevant climate-related risks and opportunities.

While reporting using the TCFD is not currently mandatory, as outlined through this report, a number of companies have begun to use this as a disclosure framework, and this additional disclosure is well supported by investors.

The TCFD also recently published its 2020 Status Report providing an overview of current disclosure practices in terms of their alignment with the TCFD's recommendations. The report found that “Disclosure of TCFD-aligned information increased by six percentage points, on average, between 2017 and 2019; and the Task Force applauds the improvements made – both in terms of the number of companies reporting and the quality of such reporting. However, companies' disclosure of the potential financial impact of climate change on their businesses and strategies remains low."

| Governance | Strategy | Risk Management | Metrics and Targets |

|---|---|---|---|

| Disclose the organization's governance around climate-related risks and opportunities. | Disclose the actual and potential impacts of climate-related risks and opportunities on the organization's businesses, strategy, and financial planning where such information is material. | Disclose how the organization identifies, assesses, and manages climate-related risks. | Disclose the metrics and targets used to assess and manage relevant climate-related risks and opportunities where such information is material. |

| Recommended Disclosures | Recommended Disclosures | Recommended Disclosures | Recommended Disclosures |

|

|

|

|

|

|

|

|

|

|

|

Figure 2: TCFD recommended disclosures

Our findings and expectations on reporting

Our assessment of reporting – what is covered

The areas our assessment, or consideration, of corporate reporting addressed are outlined in the schematic below.

- The Corporate Reporting Review (CRR) team, as the regulator of UK corporate reporting, has assessed a sample of 24 annual reports and accounts against the requirements of the Companies Act 2006 and International Financial Reporting Standards.

- The Corporate Governance and Stewardship (CG&S) team sampled 60 premium-listed companies to monitor how companies have taken account of climate-related considerations in reporting against the UK Corporate Governance Code 2018. Such areas include the consideration of emerging risks, or how climate-related considerations have been incorporated into considerations of the long-term success of the company.

- The Financial Reporting Lab (the Lab) spoke to investors to get their views on company reporting, and whether it meets their needs.

This report brings together the key findings from the work of all the FRC teams above. Our observations reflect compliance with regulatory requirements, expectations of good governance and investor expectations. Companies should reflect on all of these matters. The FRC's expectations of how relevant reporting requirements should be addressed are set out on page 9 for narrative reporting and page 10 for financial statements.

The diagram illustrates two main categories of narrative reporting and financial statements, with an overarching theme of "Consistency".

Narrative reporting - impact of climate change on the company * Business model and strategy * Risks, uncertainties and opportunities * Disclosure under the TCFD * Reporting on scenarios and viability

Narrative reporting - impact of the company on the environment * Non-financial information * Targets, commitments and key performance indicators * Greenhouse Gas (GHG) Emissions * Board consideration and stakeholder engagement

Financial Statements * Financial statement assumptions * Materiality * Asset impairment and useful lives * Judgements and Estimates * Segmental reporting

What did we find?

This review has resulted in a range of detailed findings included over the next two pages, but our headline findings are as follows:

An increasing number of companies are providing narrative reporting on climate-related issues. While minimum legal requirements are often being met, users are calling for additional disclosure to inform their decision making. Some companies have set strategic goals such as 'net zero', but it is unclear from their reporting how progress towards these goals will be achieved, monitored or assured.

Consideration and disclosure of climate change in the financial statements lags behind narrative reporting. We identified areas of potential non-compliance with the requirements of International Financial Reporting Standards (IFRS).

FRC Statement – Green Finance Strategy

In 2019 the FRC joined the Financial Conduct Authority (FCA), the Prudential Regulation Authority (PRA) and The Pensions Regulator (TPR) in stating its view that the challenges associated with climate change, including both physical factors, such as extreme weather events, and transition risks that can arise for the process of adjustment to a carbon neutral economy, would challenge and change our society and the wider market. At the time, the FRC stated that:

The Boards of UK companies have a responsibility to consider their impact on the environment and the likely consequences of any business decisions in the long-term. They should therefore address, and where relevant report on, the effects of climate change (both direct and indirect). Reporting should set out how the company has taken into account the resilience of the company's business model and its risks, uncertainties and viability in both the immediate and longer-term in light of climate change. Companies should also reflect the current or future impacts of climate change on their financial position, for example in the valuation of their assets, assumptions used in impairment testing, depreciation rates, decommissioning, restoration and other similar liabilities and financial risk disclosures.

This expectation in part led us to undertake the FRC's thematic review of corporate reporting and audit. In some instances, our review has identified potential non-compliance with the reporting requirements, both in relation to narrative and financial statements disclosures. Climate-related issues will be an ongoing area of focus for the FRC. We will continue to consider climate-related issues in our Code monitoring. Financial reporting in respect of climate change will be an area of focus for the FRC in our regulatory reviews of companies' annual reports and accounts. The FRC's expectations of how relevant reporting requirements should be addressed are set out on pages 9 and

- We will make enquiries with companies where it is apparent that the relevant reporting requirements have not been met.

Our findings – narrative reporting

An increasing number of companies are providing narrative reporting on climate-related issues. While minimum legal requirements are often being met, users are calling for additional disclosure to inform their decision making. Some companies have set strategic goals such as 'net zero', but it is unclear from their reporting how progress towards these goals will be achieved, monitored or assured.

Whilst many of the requirements are being met, a view of the impacts of climate change on the business model is often lacking the detail that users are calling for.

More companies are referencing TCFD in their disclosures, with more fulsome reporting at the larger end of the listed market. This reporting is developing, but does not yet meet investors' needs, particularly regarding strategy and metrics and targets.

Consideration of climate change as a risk is increasing, but disclosures are often lacking in substance, unclear and non-specific. Most companies discussed the risks they faced from climate change. Where users might have a reasonable expectation that climate change is an issue, but management considers that it does not give rise to any significant risk, it may be helpful to explain why.

Opportunities were identified by the majority of companies, but these disclosures were often non-specific. Better disclosures explained the changes needed to their strategy to capitalise on these opportunities.

The discussion of risks and opportunities should be balanced. Where a company believes that it has significant opportunities from the response to climate change but also potential risks, it should pay equal attention to describing areas of the business at risk.

Reporting on scenarios remains a key area of investor interest, and an area of weaker disclosure. Some companies disclose climate change scenarios that may affect viability, but detail is scarce.

Disclosures of the impact of the company on the environment were less developed. There is scope to improve non-financial reporting statements in relation to specific policies pursued, and details of the specific business relationships, products and services which are likely to cause adverse environmental impacts.

A number of companies are reporting climate change commitments, for example pledges to reach ‘net zero', and disclosing indicators around climate change, but these are often ill-defined, difficult to understand and compare, and have the potential to be misleading. Companies should clearly distinguish ‘aims' and 'ambitions' from policies which are actively being pursued and are included in business plans and budgets.

Companies should avoid providing disproportionate focus on ‘good news stories' representing a small part of the business, and clearly report the most significant outcomes for the business as a whole, including performance against any previously announced targets.

Information outlining the impact of the company on the environment is less developed and informative than the challenge climate change poses to the company.

Required greenhouse gas emissions (GHG) disclosures were provided by almost all companies, but the scope of the emissions included and the basis on which the emissions are calculated is often unclear. This is particularly important where this forms the basis of a ‘net zero' commitment or strategy.

Stakeholder engagement and section 172 disclosures were often combined, sometimes leading to the omission of certain aspects of the required disclosures, particularly those not directly related to stakeholder engagement.

Our findings – financial statements

Consideration and disclosure of climate change in the financial statements lags behind narrative reporting. We identified areas of potential non-compliance with the requirements of International Financial Reporting Standards (IFRS).

There was limited reference to climate change in the financial statements and it was generally unclear how the forward-looking assumptions and judgements applied in preparation of the financial statements were consistent with narrative discussion of climate change in the strategic report.

Companies should consider whether the annual report and accounts, taken as a whole, presents a consistent message on the most significant risks presented by climate change, and includes all information that may be material for decision making.

Climate change was not generally addressed in disclosures of management's approach to determining key assumptions in impairment assessments, and it was unclear whether all disclosure requirements had been met. Given the wide range of outcomes and the potentially significant impacts on the financial statements, it is important that users can understand the basis applied by management in arriving at assumptions related to impairments.

There are no requirements to link financial statement assumptions to a particular climate scenario, although users have highlighted the importance of being able to understand this linkage.

It was unclear whether climate change uncertainties had been taken into account when determining useful economic lives of assets which appear to be exposed to these risks.

Climate change was not generally addressed in disclosures of significant judgements, or about sources of estimation uncertainty which have a significant risk of resulting in a material adjustment within the next financial year. While uncertainties associated with climate change are often resolved over a timeframe greater than 12 months, this is not always the case.

Segmental and disaggregated revenue disclosures did not typically provide insight into the differing impact of climate change across separate parts of the business.

Uncertainties associated with climate change may impact a broad range of financial statement estimates. We identified company-specific issues in relation to fair values, commodity hedging, expected credit losses and other provisions.

Our expectations – narrative reporting

Climate change and related disclosures will be an area of focus for CRR in its ongoing reviews. In relation to narrative reporting, we expect companies to:

Include a separately identifiable non-financial information statement in their strategic report which addresses environmental matters such as climate change 'to the extent necessary for an understanding of the company's development, performance and position and the impact of its activity' (CA2006 414CB(1)(a)). In particular companies should:

- provide a description of significant 'policies pursued' with respect to climate change, rather than simply naming them, or explain the reason if no such policies are pursued;

- provide clear explanations which help users to understand and compare major commitments such as 'net zero emissions' targets or 'Paris-aligned' strategies, including which activities and emissions are included in the scope of these commitments. It should be clear whether these are aspirational, or currently pursued and factored into budgets and business plans used when preparing the financial statements;

- describe the most significant outcomes of those policies for the business as a whole, without disproportionate focus on immaterial activities or 'good news stories';

- where climate-related targets have previously been announced, describe the company's performance against those targets;

- explain any changes in targets or KPIs from the previous year, including the reason for the change;

- describe the impact of the company's business on the environment, as well as the risks that climate change gives rise to for the company;

- ensure impacts within the company's supply chain and from use of products are addressed in the disclosures, particularly where these are significant relative to those arising from the company's direct activities;

- ensure that any cross-referencing to information included elsewhere in the annual report is sufficiently specific to enable readers to locate and identify the particular information in question.

Describe the principal risks and uncertainties facing the company which relate to climate change, and any significant impacts on the business model. Better disclosures provide users with information which is specific to the company's circumstances, and are clear on the magnitude of the risk.

Consider explaining the rationale if management has concluded that climate change does not give rise to any significant risks for the company.

Describe the methodologies used to calculate emissions metrics and the extent of any due diligence or assurance over these. There is significant scope for judgements in determining boundaries and which emissions are included so companies should explain these decisions clearly. This information is expected to be more material where these metrics underpin a major policy or strategy.

Ensure that section 172(1) statements describe the actions of the board of directors, rather than other parties, and address all the regulatory requirements, not just those associated with stakeholder engagement, particularly where those statements are combined.

Ensure that stakeholder engagement reports reflect all significant environmental matters discussed with stakeholders during the year.

Our expectations – financial statements

Climate change and related disclosures will be an area of focus for CRR in its ongoing reviews. In relation to financial statements, we expect companies to:

Ensure that material climate change risks and uncertainties discussed in narrative reporting have been appropriately considered in the financial statements. Narrative reporting should not be inconsistent with the financial statements. Better disclosures present a coherent linkage between narrative reporting and accounting judgements and estimates and may explain why apparently significant risks have not had a material impact on the financial statements where investors may expect them to do so.

Reflect on the information about climate change which is material to users for both narrative reporting and financial statement disclosure. We do not encourage a checklist approach as this may lead to both clutter and omission of key information. Information may be required by IAS 1 where it is relevant to an understanding of the financial statements, even where it is not specified in a standard. We note that expectations from investors in this area are high.

Ensure that disclosures of impairment assumptions and sensitivities meet the requirements of IAS 36 with additional requirements for cash generating units (CGUs) containing goodwill or indefinite lived intangibles. In particular:

- Impairment should be assessed on an asset by asset basis, as well as by cash generating unit ('CGU'); where investors may reasonably expect climate change to have a significant impact on future expected cash flows for a particular asset or CGU, ensure that this is addressed in the description of management's approach to determining the risk of impairment and any key assumptions;

- Where a reasonably possible change in a key assumption would lead to an impairment under IAS 36, companies should disclose the value of the assumption, headroom and amount by which that assumption would need to change to drive an impairment. IAS 36 does not include a timescale for this assessment; and

- Sensitivities should address all reasonably possible changes in the relevant timescale. Better disclosure helps users understand how assumptions and sensitivities correspond to scenarios discussed in narrative reporting.

Include sensitivity analysis or the range of reasonably possible outcomes where an estimate meets the IAS 1 paragraph 125 criteria, with a significant risk of material adjustment within one year. This may arise if an uncertainty is expected to be resolved, or if longer-term assumptions around climate change are at risk of significant revision within the next year. It may be helpful to disclose other uncertainties associated with climate change which are not expected to result in an adjustment in one year, but these should be clearly distinguished.

Provide all required segmental and disaggregated revenue disclosures to enable users of financial statements to understand the relative sizes of operations for which climate change presents substantially different risks and opportunities, particularly where this is discussed in narrative reporting.

Consider the matters highlighted in the IASB article 'IFRS Standards and climate-related disclosures' in their financial reporting. The article does not have the status of a standard and does not provide a complete ‘checklist' of relevant requirements but does provide helpful insight into how climate change should be considered when addressing existing IFRS requirements.

Consider explaining how climate change has been taken into account where investors may reasonably expect a significant impact on the expected life or fair value of an asset or liability.

Narrative reporting

Narrative reporting – headline finding:

An increasing number of companies are providing narrative reporting on climate-related issues. While minimum legal requirements are often being met, users are calling for additional disclosure to inform their decision making. Some companies have set strategic goals such as 'net zero', but it is unclear from their reporting how progress towards these goals will be achieved, monitored or assured.

Impact of climate change on the company

Climate-related narrative reporting requirements and expectations cover both the potential impact on the future of a business and the company's impact on the environment. This section outlines how company disclosures address the challenges posed to the business model. It discusses strategy, risks, uncertainties and opportunities, TCFD disclosures and reporting on scenarios and viability.

Companies Act requirement - Impact of climate change on the business model

Section 414CB of the Companies Act 2006 requires public interest entities to include a non-financial information statement as part of their strategic report. Amongst other matters, this must include information regarding the impact of environmental matters on the company's business, to the extent necessary for an understanding of the company's development, performance and position and the impact of its activity. We would expect this to include climate change where material to the company.

Business model reporting

KEY FINDING: Whilst many of the requirements are being met, a view of the impacts of climate change on the business model is often lacking the detail that users are calling for.

20 companies in the sample of 24 disclosed that their business model was affected by climate change, as would be expected given the sample bias towards industries expected to be affected (further detail on the scope of our review can be found in Appendix - Scope).

Topics discussed included exposure to fossil fuels, future investments, renewable energy, sustainable growth and customer expectations.

Disclosures in this area, however, could be improved.

Omission/Issue: Generic comments such as to be 'flexible and adapt' are not helpful to users of financial statements.

Opportunity: Several companies had discussed strategies that were aligned with the goals of the Paris climate agreement or an intention to 'be carbon negative' or reach 'net zero emissions' by a particular date. This did not always address what this meant in practice for the business. We have highlighted our expectations on these matters on page 32.

Good practice: We observed that the most helpful disclosures:

- Included climate change within the business model section itself.

- Gave specific detail about product lines, services and investments.

- Linked climate-related risks and opportunities to these business areas.

- Specifically addressed sustainability.

Lab finding - business model and strategy

As the demand for climate-related disclosure by investors and wider stakeholders increases, many companies are developing their climate governance in line with reporting frameworks, principally TCFD. The Lab's 2019 report on climate-related disclosures found investors to be very supportive of the TCFD framework for company consideration, and disclosure, of climate-related issues. The investors we spoke to as part of this thematic remained enthusiastic about TCFD reporting.

The Lab's report identified that investors wanted to understand the challenges a company faces in relation to climate change, and the strategy for addressing these issues. A key question investors ask relates to the resilience and sustainability of the business model. Unfortunately, many companies are failing to articulate their conclusions in this area.

Investors echo our insights, including the finding that generic comments and lack of specificity as to actual business plans is unhelpful.

Business model and strategy questions

- What does the company look like in the future and how will it continue to generate value? What strategy does the company have for responding to the challenges?

- How was the decision about the materiality of climate-related issues made?

- What opportunities and risks concerning climate-related issues are most relevant to the company's business model and strategy? Which, if any, of these are financially material? What process has been followed in order to assess the impact of climate-related issues?

- Where do the biggest risks and opportunities sit?

- Has the company considered the impact of low-carbon transition as well as physical risk?

- What are the relevant short, medium and long-term horizons? How do these different horizons affect key divisions, markets, products and/or revenue/profit drivers?

- How resilient is the business model to climate change? How does the company respond to a 1.5 degree, 2 degree or more world?

- What strategy has been put in place to reach that aim, and what operational or capital expenditures are needed to address any necessary business model changes? How are long-term projects structured to ensure flexibility, including options for deemphasising and emphasising if circumstances should dictate?

- What are the possible effects on the company's revenues, expenditures, assets, liabilities, products, customers, suppliers etc of different climate scenarios?

- How does the information gathered factor into strategic planning? What triggers would require a change of direction?

- Are there opportunities better to explain exposure to particular product lines or 'green' revenues?

- How are the risks and opportunities reflected in the financial statements, for example the effect of assumptions used in impairment testing, depreciation rates, decommissioning, restoration and other similar liabilities and financial risk disclosures?

"On Paris-agreement goals, I want not only an assessment of where the risks are, I want to know what the company is doing. How is it adjusting its business model and strategy to thrive in a changed world where we have transitioned to low carbon, or there is some degree of increased climate risk?" - Investor

“At the end of the day this is the beginning [of reporting]. More of an art than a science and I'm not looking for precision. I want the company to be doing the exercise, having high-level decision makers involved, some kind of strategic implementation and consideration – that's the important part" - Investor

TCFD disclosure

KEY FINDING: More companies are referencing TCFD in their disclosures, with more fulsome reporting at the larger end of the listed market. This reporting is developing, but does not yet meet investors' needs, particularly regarding strategy and metrics and targets.

The TCFD is a framework under which many companies are choosing to report the narrative aspects of their climate-related considerations. This framework covers reporting in four core areas – governance, strategy, risk management and metrics and targets.

Our review identified many companies using, or stating that they will use, the TCFD framework for their reporting. This was welcomed by the investors we spoke to, but they noted that a greater degree of granularity, particularly with regard to specific plans and targets, and metrics used to assess climate-related factors was important for their investment decision making.

Extent of TCFD reporting

Many of the FTSE 100 companies reviewed had started to implement TCFD recommendations, some with full effect. In our sample of 24, five FTSE 100 companies had fully adopted the TCFD requirements; with four choosing to include a separately identifiable section in their strategic report.

Whilst a separate TCFD section is not necessarily needed, it can be an effective method to present the information. However, it is important to ensure that the information presented does not appear to be an 'add-on' containing boilerplate messages. Reporting under the TCFD recommendations was improved where it was better integrated with the company's strategy with the use of cross-referencing.

Other company reports we assessed stated the company's intention to implement the framework in the next two years. For example, in our sample of 24, nine companies either partly complied with TCFD or disclosed that they had the intention to adopt.

We found some encouraging reporting practice within the FTSE250, where companies disclosed a clear and comprehensive roadmap towards full TCFD disclosure as well as their progress thus far, including any relevant milestones. This was more common in more carbon-intense industries such as Materials, Buildings and Construction.

Lab finding - investor views on TCFD

Investors reported an increase in disclosure on TCFD. Whether this is in response to investor pressure, or governmental and regulatory pressures, this development was welcomed.

Investor support for the TCFD as a framework for companies to consider and report on their climate-related issues appears only to grow. This view is increasingly supported by regulatory changes. In fact, many investors were supportive of the increasing international momentum to include, or consider including, TCFD within the regulatory disclosure framework, including within FCA rules as proposed in the recent consultation (see next page).

However, investors noted that disclosure needed to continue to develop to meet their needs. As outlined above, issues around the strategy and business model remain key. This also links to the expectations of scenario analysis and disclosures, and through to assessments of the sustainability and resilience of the business model.

Metrics and targets remain another area of concern for investors, with many investors reporting that targets are non-specific and lack substance, particularly relating to interim milestones. More specific views are provided in the section on target-setting.

FRC view on reporting frameworks

The FRC supports the establishment and adoption of global non-financial reporting standards and we look forward to engaging with the IFRS Foundation Trustees and other organisations working to achieve that goal. However, in the shorter term we think there is a need for the market to move more quickly to improve disclosures in this area. In order to help investors and other capital providers to get more of the information they seek, the FRC encourages UK public interest entities to report against the TCFD 11 recommended disclosures and, with reference to their sector, to use the Sustainability Accounting Standards Board (SASB) metrics.

Encouraging reporting under TCFD and SASB is a step towards a better system of reporting. The FRC's full statement on non-financial reporting can be found here.

FCA consultation on TCFD reporting

On 6 March 2020, the FCA launched a consultation on the introduction of TCFD disclosures, on a comply or explain basis, for commercial companies with a premium-listing (CP20/3: Proposals to enhance climate-related disclosures by listed issuers and clarification of existing disclosure obligations). We support the FCA's encouragement of greater transparency over the climate-related risks and opportunities premium-listed companies face and the FCA's role in encouraging and supporting a greater range of companies to meet these expectations.

Investor views on TCFD from FRC review of the UK Stewardship Code 2020

The scope of our review of UK Stewardship Code disclosures is outlined in the connected report on investor reporting, available here. However, the vast majority of the investor reports reviewed noted that they were supporters of TCFD. Many of the organisations explained that they use the TCFD core areas as a lens to consider climate-related issues for the companies in which they invest. A number of reports reviewed, particularly those by larger asset managers, indicated that they are already, or intend to, produce their own TCFD reporting, though these disclosures are largely still at a preliminary stage.

“TCFD disclosure is obviously very helpful and useful regarding a focus on strategy and not just risk, but it's possible to create TCFD reports that are as good as meaningless, [with companies] hiding behind the high-level disclosure that things are fine" - Investor

Risk disclosure

KEY FINDING: Consideration of climate change as a risk is increasing, but disclosures are often lacking in substance, unclear and non-specific. Most companies discussed the risks they faced from climate change. Where users might have a reasonable expectation that climate change is an issue, but management considers that it does not give rise to any significant risk, it may be helpful to explain why.

Companies Act requirement – principal risks

Section 414CB of the Companies Act 2006 requires a description of the principal risks relating to environmental matters, including a description of how it manages the principal risks.

Extent of climate-related risk disclosure

As outlined above, the Companies Act requires disclosure regarding principal risks related to environmental matters, and the Code now also encourages the consideration of emerging risks. Our review identified many companies reporting climate change as either a principal or emerging risk. However, in the small cap sample, only a small minority of companies mentioned climate change as a risk.

About half (13 of 24 companies reviewed) disclosed a principal risk relating to climate change, of which one was disclosed under non-financial reporting specific risks and the remainder were included within general risks. A further four companies disclosed climate-related matters as emerging risks. The number of climate-related principal risks disclosed for any one company ranged from one to six.

It was expected that companies within the oil and gas and mining sectors would disclose at least one climate-related principal risk, which proved to be the case within our sample, with the impacts of climate change linked to specific areas of the business and strategy. These included regulatory developments, carbon pricing, disruption of operations, business reputation and energy costs. Only one company within the mining sector disclosed climate change as an emerging risk rather than a principal risk. This company had less exposure to commodity price risk due to the nature of its products. Some companies chose to disclose climate change as one main principal risk, discussing several issues under one heading, whilst others chose to present separate climate-related risks.

Some companies in other sectors, including financial services, aviation, packaging and consumer goods, had disclosed at least one climate-related principal risk. Those that had not, tended to operate in sectors in which climate change is considered to have a predominantly medium or long-term impact.

Better practice reporting:

- Disclosed both the likelihood and impact of the climate-related principal risk(s). Whilst a matrix presentation is not required, we encourage companies to indicate the significance of climate-related risks relative to other risks.

- Discussed how they had determined which risks were material to disclose.

Of the companies that did not disclose any climate-related principal risks, four disclosed climate change as an emerging risk. Disclosure is considered helpful in circumstances where users would have a reasonable expectation that climate change would give rise to a risk. If management considers that climate change does not give rise to any significant risk, we encourage companies to articulate why in sufficient detail to enable users to assess management's considerations and conclusions in this area.

Physical and transitional risks

We also found that a number of companies distinguished between physical and transitional risks; for example, in our sample, 13 of the 24 companies did so.

The most helpful disclosures:

- Further divided physical risks between acute and chronic.

- Further divided transitional risks between policy and legal, technology, market and reputation.

- Linked each risk to a specific business area.

The physical and transitional risks identified by companies included government intervention on climate change and environmental issues (e.g. Greenhouse Gas emissions, packaging, waste); extreme weather events which may impact business operations; the impact of use of products by customers; supply chain risk; large fluctuations in energy costs; and sustainability performance failing to keep pace with demands.

| Global Risk Report | |||

|---|---|---|---|

| 2017 | 2018 | 2019 | 2020 |

| Extreme weather | Extreme weather | Extreme weather | Extreme weather |

| Involuntary migration | Natural disasters | Climate action failure | Climate action failure |

| Natural disasters | Cyberattacks | Natural disasters | Natural disasters |

| Terrorist attacks | Data fraud or theft | Data fraud or theft | Biodiversity loss |

| Data fraud or theft | Climate action failure | Cyberattacks | Human-made environmental disasters |

World Economic Forum, The Global Risks Report 2020, Insight Report 15th Edition In partnership with Marsh & McLennan and Zurich Insurance Group.

The World Economic Forum Global Risk Report 2020 identified environmental risks as the five greatest risks in terms of likelihood. The five risks identified were extreme weather; climate action failure; natural disasters; biodiversity loss; and human-made environmental disasters. The environmental risks of climate action failure; biodiversity loss; and extreme weather were also identified as three of the top five risks in terms of impact.

Examples of better disclosure

"vi) The impact of climate change on the Group's business

The risks associated with climate change are subject to rapidly increasing societal, regulatory and political focus, both in the UK and internationally. Embedding climate risk into the Group's risk framework in line with regulatory expectations, and adapting the Group's operations and business strategy to address both the financial risks resulting from: (i) the physical risk of climate change; and (ii) the risk from the transition to a low-carbon economy, could have a significant impact on the Group's business.

Physical risks from climate change arise from a number of factors and relate to specific weather events and longer-term shifts in the climate. The nature and timing of extreme weather events are uncertain but they are increasing in frequency and their impact on the economy is predicted to be more acute in the future. The potential impact on the economy includes, but is not limited to, lower GDP growth, higher unemployment and significant changes in asset prices and profitability of industries. Damage to the properties and operations of borrowers could impair asset values and the creditworthiness of customers leading to increased default rates, delinquencies, write-offs and impairment charges in the Group's portfolios. In addition, the Group's premises and resilience may also suffer physical damage due to weather events leading to increased costs for the Group.

As the economy transitions to a low-carbon economy, financial institutions such as the Group may face significant and rapid developments in stakeholder expectations, policy, law and regulation which could impact the lending activities the Group undertakes, as well as the risks associated with its lending portfolios, and the value of the Group's financial assets. As sentiment towards climate change shifts and societal preferences change, the Group may face greater scrutiny of the type of business it conducts, adverse media coverage and reputational damage, which may in turn impact customer demand for the Group's products, returns on certain business activities and the value of certain assets and trading positions resulting in impairment charges. In addition, the impacts of physical and transition climate risks can lead to second order connected risks, which have the potential to affect the Group's retail and wholesale portfolios. The impacts of climate change may increase losses for those sectors sensitive to the effects of physical and transition risks. Any subsequent increase in defaults and rising unemployment could create recessionary pressures, which may lead to wider deterioration in the creditworthiness of the Group's clients, higher ECLs, and increased charge

- offs and defaults among retail customers.

If the Group does not adequately embed risks associated with climate change into its risk framework to appropriately measure, manage and disclose the various financial and operational risks it faces as a result of climate change, or fails to adapt its strategy and business model to the changing regulatory requirements and market expectations on a timely basis, it may have a material and adverse impact on the Group's level of business growth, competitiveness, profitability, capital requirements, cost of funding, and financial condition.”

Barclays plc, Annual Report 2019, page 131

Discussion of physical and transition risks.

Clear articulation of the potential impact of transition to a low-carbon economy on the business.

Discussion of second order risks.

Climate-related risk process

The TCFD framework suggests that companies disclose the process for identifying and assessing climate-related risks. Many of the company reports we reviewed identified the process for the identification, monitoring and management of climate-related risks. A number of companies had also initiated risks projects and environmental initiatives to gain greater understanding of current and potential future risks arising from climate change.

Risk identification processes included top-down, bottom-up risk assessments, the establishment of a Climate Change Working Group and regular management updates on non-financial risk areas presented to the Audit Committee. It was encouraging that companies not currently compliant with TCFD also mentioned steps being taken to identify and assess climate-related risks such as increased data collection and the inclusion of climate change on risk registers.

The management of climate-related risks should discuss decisions on mitigating, transferring, accepting or controlling those risks.

- Weaker disclosures discussed climate-related risks, internal controls, mitigation and monitoring in general.

- The most helpful disclosures discussed the management of each risk in turn.

12 of the 13 companies in our sample of 24 that identified at least one climate-related principal risk disclosed how these were managed. Examples of mitigation activities included:

- employing specialist technical advisors to assist in understanding climate-related risk;

- action to influence policy and regulation;

- optimising use of fossil fuels and increasing efficiency; and

- diversification of supply chain.

Risk management disclosure should cover both risks to the company and risks to the environment. There is further discussion of the disclosure of risks posed by the company to the environment on page 29.

WE EXPECT COMPANIES TO: Describe the principal risks and uncertainties facing the company which relate to climate change, and any significant impacts on the business model. Better disclosures provide users with information which is specific to the company's circumstances, and are clear on the magnitude of the risk.

Consider explaining the rationale if management has concluded that climate change does not give rise to any significant risks for the company.

Lack of specificity

Our sample identified examples of good disclosure with impacts of climate change linked to specific areas of the business and strategy. However, this finding may reflect the fact that these companies were selected from sectors most likely to be affected by climate change.

Our wider sample of reporting by premium-listed companies found that disclosure on climate-related risks often lacked substance. For example, many companies provided vague or generic explanation of climate-related risks (e.g. extreme weather events, flooding that may impact sites negatively), but did not report on the specific location of their operations or assets at risk. There was also a lack of detail as to how some of the risks connected to the company's specific business model and strategy. These are key focus areas for investors.

We found that reporting was more effective where it identified the climate-related risk (e.g. financial impact of extreme weather events), described the specific mechanism used to mitigate or help identify that risk (e.g. flood mapping analytics) and the specific outcome of such risk mitigation (e.g. building flood defences at site X).

In a similar vein, when reporting on climate-related risk mitigation, some companies pointed to actions taken to mitigate climate-related risk; for example, a diversified geographical and technological portfolio of assets. However, they did not make it clear whether certain locations have the capacity to recoup any losses incurred by damage to business operations at another location.

Examples of better disclosure

Risk management – policy

In 2019, the Group published a 'Climate Change Financial Risk and Operational Risk Policy'. This introduced climate change as an overarching risk impacting certain principal risks: credit risk, market risk, treasury & capital risk and operational risk. The policy is jointly owned by the relevant Principal Risk Leads with oversight by the BRC.

Each relevant Principal Risk Lead has developed a methodology and implementation plan for quantifying climate change risk.

| Risk | Measurement approach |

|---|---|

| Credit risk | A Credit Risk Materiality Matrix (Climate Lens) assesses the climate change risk of a counterparty to which the Group is exposed. The Climate Lens considers transition factors such as a counterparty's reliance on fossil fuels, sensitivity to policy changes and ability to diversify, as well as exposure to physical risks. Where an obligor is rated as Medium or High, the details are referred to the Environmental Risk Management team, who conduct enhanced due diligence. |

| Market risk | Stress tests are used to assess and aggregate exposures arising from climate related risks. Stress test scenarios are applied to a range of assets, reflecting the impact of climate change across sectors, countries and regions. |

| Treasury and capital risk | Stress tests are used to assess and aggregate exposures arising from climate related risks. They are measured as part of existing stress testing, ICAAP and capital planning. |

| Operational risk | The risks associated with Climate Change are relevant to the following Operational Risk Categories/Themes, which are managed through the Operational Risk Framework: Premises Risk, Supplier Risk and Resilience. Climate Change has been included in the Strategic Risk Assessment to understand exposure on a forward looking basis across the five-year business planning cycle. |

Climate change specifically addressed within risk management policy.

Gives a clear horizon over which risk assessment has been carried out.

Barclays plc, Annual Report 2019, page 138

Lab insight - investor views on risk management

Investors report that risks and opportunities are often not clearly described. The Lab's recent projects on risk and viability have consistently found that investors do not consider risks and opportunities to be sufficiently related to the strategy and business model of the company.

Investors are looking to understand the risks and opportunities presented by climate change including the prioritisation, likelihood and impact, what scenarios might affect the company's sustainability and viability, and how the company is responding.

The increasing consideration of climate change within principal or emerging risk disclosure was welcomed by investors, but the lack of specificity made a true assessment of the risks and opportunities the entity faces difficult to appreciate. Investors seek to understand over which timeframes risks and opportunities might crystallise.

Investors report that it is still difficult to understand how the company intends to respond to the climate-related risks and opportunities it faces. Disclosure can be very generic, and the lack of clarity, particularly in the context of targets such as 'net zero', is a key concern.

In order to help companies respond, the Lab's 2019 report posed a series of suggested questions. Investors noted that these remain highly relevant and useful, so the risk management questions have been included to the right.

“So when, for example I'm looking at capital expenditure for opportunities, it's difficult for investors to consider it material when making investment decisions if it's not linked through. This gap is not being met" - Investor

Risk management questions

- What oversight does the board have of climate-related opportunities and risks?

- What systems and processes are in place for identifying, assessing and managing climate-related risks? To what extent can current processes be developed to assist?

- How will transitional and physical risks affect the company?

- How is a consideration of climate-related issues integrated into the risk management process and connected to other related risks?

- Over what horizons have the risks been considered and risk assessments carried out?

- How are the risks from climate change being monitored, including decisions around mitigation, transfer, acceptance and control?

- How is the assessment of the company's viability over the longer-term taking into account climate-related issues?

- Is the company's business and business model viable? What signals or leading indicators might encourage a reconsideration of this assessment and the related strategy, or an understanding of whether the risk mitigation activities are being achieved?

- If the company is undertaking scenario analysis, how did the company decide on which scenarios to use and what assumptions have been made? How do these relate to the outcomes advocated in the Paris Agreement?

- Are the scenarios sufficiently diverse and challenging?

- How did the company translate scenarios to operational/financial models?

- How is the scenario analysis used in strategic planning?

Opportunities

KEY FINDING: Opportunities were identified by the majority of companies, but these disclosures were often non-specific. Better disclosures explained the changes needed to their strategy to capitalise on these opportunities.

15 companies gave some indication of the changes needed to strategy to capitalise on climate-related opportunities. We observed that the most helpful disclosures:

- Clearly showed a change in strategy either by including climate change in the strategy section itself or by specifically referring to strategy in the narrative.

- Discussed changes in operations.

- Disclosed any investments such as in research and development.

- Discussed specific growth strategies e.g. organic, M&A.

Extent of disclosure of opportunities

CRR's review, with a sample biased towards those most affected by climate change, identified several examples of good disclosure. However, the wider review of premium listed companies by CG&S identified that disclosures of opportunities related to climate change were often boilerplate. Where companies had identified risks and opportunities these were often not identified according to specific horizons, and the horizons themselves were not identified.

Although not required by legislation, 18 companies in the CRR sample disclosed climate-related opportunities. Examples included the development of products to help customers comply with sustainability requirements, demand for raw materials used in environmentally friendly products and sales of byproducts from generating green energy. However, six of these companies provided more boilerplate comments, such as being well-placed to address the need for low and zero emission technology or referencing opportunities in new markets but without further detail.

Weaker disclosures:

- Mentioned actions or decisions concerning climate change opportunities within the annual report but did not specifically discuss strategy.

- Made general comments such as needing to respond to customer expectations.

Risks and opportunities horizons

Across all of our reporting reviews, we found that disclosures of risks and opportunities over the short, medium and long term varied in how clearly they were presented. Some companies referred to time frames within their narrative, often discussing climate-related risks in general rather than separate risks, for example stating that climate-related risks were viewed as having only medium or long-term impacts.

- Better disclosures provide sufficiently detailed information about products and services, supply chain and/or value chain, adaptation and mitigation activities, investment in research and development and operations.

On a sector-by-sector basis across the premium-listed sample, reporting on specific horizons was most developed in the Materials, Buildings and Construction industry and least developed in Consumer Products & Manufacturing. Where companies did report on these issues, comparability was enhanced where the company used informative graphics and/or tables to explain, in a concise yet complete manner, the short, medium and long-term risks and opportunities engendered by climate change.

Examples of better disclosure

Describe the climate-related risks and opportunities the organisation has identified over the short, medium and long-term

- Short-term (0-5 years): customer carbon emission targets and increasing availability of green electricity could encourage a move towards electric heating solutions that have zero emissions at point of use. While an opportunity for the Electric Thermal Solutions business, some sales could be at risk in the Steam Specialties business for applications where steam or electric heating solutions are equally viable.

- Medium-term (5-10 years): growth in electric vehicles could cause a decline in the oil and gas industry, particularly refinery demand.

- Long-term (10+ years): large oil, coal and gas fired boilers could be replaced by banks of small electric generators reducing demand for boiler controls and boiler-house products.

- Increasing frequency of climate related extreme weather events.

Spriax-Sarco Engineering plc, Annual Report 2019, page 69

Risks and opportunities are divided into clear time bands

Examples of better disclosure

"Managing climate-related risks and opportunities

We identify and assess climate-related risks using our group-wide risk management framework. It includes pre-determined risk tolerance limits, established by the Board, based on the likelihood and severity of risk factors. Climate change has the potential to affect our business in various ways. While these may not be severe in the short term, we believe climate-related risks are likely to have a medium and long-term impact on our business. We have identified both transition and physical risks. Governments and regulators are likely to take action to curb carbon emissions that may impact our business, such as the introduction of carbon taxes. Changes in precipitation patterns and extreme weather conditions such as floods, storms, droughts and fires may impact our plantations and the forests we source wood from and could result in fibre supply chain interruptions and higher fibre costs. Higher temperatures may also increase the vulnerability of forests to pests and disease. Increased severity of extreme weather events may also interrupt our operations. In water-scarce countries, we may see an impact on our production process as a result of limited water availability. [...] Our climate-related opportunities include reduced operating costs through greater energy and water efficiency and generating income by selling low-carbon, biomass based chemical by-products from our pulp process (such as turpentines) as well secondary raw materials."

Mondi Group, Integrated report and financial statements 2019, page 43

Timeframes for the impact of climate change on the company.

Discusses transition and physical risks.

Links to specific areas of the business (plantations/forests). These are discussed in greater detail in the sustainability performance section of the annual report.

Income generated from the sale of green energy and CO2e credits is recorded within other net operating expenses in the income statement.

All five companies in our sample that had adopted TCFD explained how the risks and opportunities that had been identified were factored into their considerations of strategy and financial planning.

- The best disclosures clearly articulated how climate change considerations were embedded into strategic plans and budgets.

- We expect to see discussion of the impact of financial planning on operating costs and revenues, capital expenditures and capital allocation, acquisitions or divestments, and access to capital.

KEY FINDING: The discussion of risks and opportunities should be balanced. Where a company believes that it has significant opportunities from the response to climate change but also potential risks, it should pay equal attention to describing areas of the business at risk.

Scenario planning

KEY FINDING: Reporting on scenarios remains a key area of investor interest, and an area of weaker disclosure. Some companies disclose climate change scenarios that may affect viability, but detail is scarce.

There is no single view of the future we face in relation to climate change. Equally, where a specific temperature outcome is being used for scenario purposes there will be a range of possible pathways that could be followed to reach that outcome. Considering the wide range of ways climate change could impact businesses and the difficulty in planning for uncertain climate-related events, boards should be considering the possible impacts of climate change on their company. This approach can help organisations plan for a number of eventualities and demonstrate to investors the resilience of the business model.

Extent of disclosure on scenarios

It was encouraging to find that companies are beginning to develop models and tools to evaluate the potential impact on the business of different climate scenarios, typically the four scenarios identified by the Intergovernmental Panel on Climate Change (IPCC). Reporting on climate scenario analyses was more common by companies that had endorsed the TCFD.

The TCFD provides that companies should develop and apply scenario analysis to the impact of climate change. These disclosures should document:

- Detailed key inputs, assumptions, analytical methods and outputs

- Sensitivities to key assumptions

- Management's assessment of the resilience of its strategic plans to climate change

11 companies of the 24 assessed disclosed at least one scenario that might affect the company's sustainability and viability. In addition to scenarios based on global temperature rises, scenarios included weather pattern disruption, water stress and the reduction of CO2 allowances.

Detail of the scenarios

There were large variations in the level of detail provided for the outcomes a business may be exposed to under each scenario. Most companies described assessing their business model and strategy against certain scenarios and stress tests but these gave little detail on key inputs, and provided only vague detail concerning the specific risks considered, the assumptions made and the outcomes.

Disclosure of climate scenarios could be improved by:

- Providing sufficient detail of the scenarios and stress tests used for readers to understand their key features.

- Discussing clear outcomes of the scenario analysis in terms of how these outcomes influenced strategic planning and the actions taken as a result.

- Describing how the outcomes of the scenarios relate to the outcomes advocated in the Paris Agreement, where relevant.

- Ensuring that narrative discussion of climate scenarios is consistent with the assumptions and disclosures in the financial statements. Users may find additional explanation helpful. This includes how both financial statement assumptions, and sensitivities considered, correspond to narrative disclosures of climate change (see further discussion in Climate change in the financial statements – Climate scenarios).

It is also worth noting that none of the companies in our sample for whom climate change presents an immediate significant risk included all the disclosures recommended by the TCFD.

- Three of the five companies adopting TCFD discussed using climate-related scenarios but gave no further details. Another company explained that it was still reviewing its resilience in the context of a 2°C scenario.

- Given the level of investor interest in this area, we encourage companies to expand their disclosures giving the key outcomes of each modelled scenario and the changes to business areas, strategy and financial planning that would be needed as a result in order to ensure the company's sustainability and viability.

- As practice develops, scenarios should develop from qualitative to quantitative models and, where applicable, provide disclosure of key inputs, assumptions, analytical methods, outputs and sensitivities.

- None of the companies in our sample linked their scenarios clearly to an assessment of the resilience of their climate-related strategic plans.

Lab finding - investor views on scenarios

The analysis of scenarios as a key input into strategic planning remained an area of great interest to investors when we asked them about their views on climate-related disclosure this year. Mirroring many of the FRC's findings above, investors noted that they find reporting in this area to be vague and lacking in specifics related both to the scenario and to the company.

Investors want to understand the resilience of business models under a range of scenarios. Investors find especially important the disclosure of assumptions around the scenarios being tested, as there are many different pathways to one temperature outcome. Most investors expect a range of scenarios to be modelled, but want a 'below 2 degrees' scenario to be tested as one of the key possible scenarios.

The more detail a company provides on the ways in which the business model may be affected, and how it could capitalise on opportunities or mitigate risks, the more helpful it is for investors and other stakeholders to make an informed decision. And that is, ultimately, also why investors want companies to be considering scenario analyses

- so they are in the best position to make the most informed decisions about the future of the company, and to be able to respond to different inflection points and pathways. Scenario analysis is not intended to be a process in and of itself, but instead to feed into the strategic decision making undertaken by the board and management.

"Scenario analysis is clearly challenging – there are hundreds of scenarios that involve lots of assumptions, so we need to understand those assumptions in a bit of detail to know what it actually means" - Investor

"There should be consideration of an ambitious scenario (less than 2), and an understanding of a 'current policy' scenario – so what if there's no political will and we continue on the same trajectory given current policies. Rather than aligning with X – tell me what the range of outcomes might be in different scenarios" - Investor

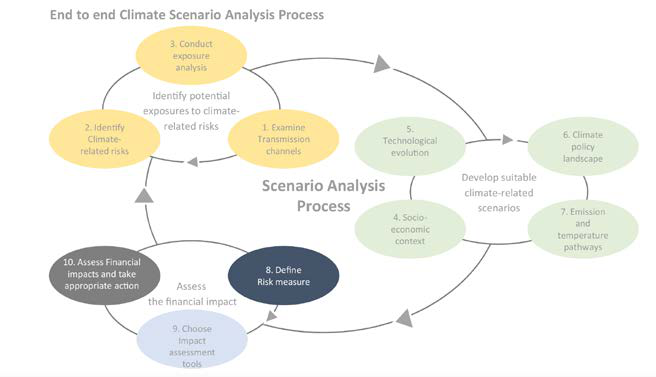

End to end Climate Scenario Analysis Process

This diagram illustrates a 10-step cyclical process for climate scenario analysis:

- Examine Transmission channels

- Identify Climate-related risks

- Conduct exposure analysis

- (Sub-step: Identify potential exposures to climate-related risks)

- Socio-economic context

- Technological evolution

- (Sub-step: Develop suitable climate-related scenarios)

- Climate policy landscape

- Emission and temperature pathways

- Define Risk measure

- Choose Impact assessment tools

- Assess Financial impacts and take appropriate action

- (Sub-step: Assess the financial impact)

“I have seen an uptick on disclosures on scenarios. I'm not prescribing [scenarios]. I want evidence it has been done and then different underlying scenarios, but at least one on 1.5 degrees" - Investor

"I'm sceptical of everything on scenario planning. Where companies say they're fine in all scenarios, that's clearly not the case" - Investor

Climate Financial Risk Forum