The content on this page has been converted from PDF to HTML format using an artificial intelligence (AI) tool as part of our ongoing efforts to improve accessibility and usability of our publications. Note:

- No human verification has been conducted of the converted content.

- While we strive for accuracy errors or omissions may exist.

- This content is provided for informational purposes only and should not be relied upon as a definitive or authoritative source.

- For the official and verified version of the publication, refer to the original PDF document.

If you identify any inaccuracies or have concerns about the content, please contact us at [email protected].

SGN 02/2018 - Group Guidance

STAFF GUIDANCE NOTE 02/2018

GROUP AUDITS: DETERMINING WHETHER COMPONENTS ARE SIGNIFICANT AND/OR MATERIAL, AND WHAT THAT MEANS FOR KEY AUDIT PARTNERS AND ENGAGEMENT QUALITY CONTROL REVIEWERS

1ISA (UK) 6001 incorporates requirements introduced by the Audit Directive and Regulation. This guidance helps auditors to understand the application of the new requirements and determine whether a component is significant and/or material and what that means for the group engagement team ('GET') and the engagement quality control reviewer ('EQCR'). It builds on the material already in the Rolling Record of Matters discussed by TAG.

Significant and/or material?

2ISA (UK) 600 differentiates work effort between those components that are significant and those that are not. A significant component is defined as: "A component identified by the group engagement team (i) that is of individual financial significance to the group, or (ii) that, due to its specific nature or circumstances, is likely to include significant risks of material misstatement of the group financial statements."2

3The Audit Directive introduced a new term 'material subsidiaries' by reference to the definition of a Key Audit Partner ('KAP'). 'Material subsidiaries' is not defined by the Audit Directive; however, the FRC is of the view that 'a material subsidiary' operates at a lower threshold than a 'significant component'.3 A component could be 'Not Significant' under ISA (UK) 600, but still be 'Material'. The FRC issued guidance4 that when considering which subsidiaries are material in the context of a group engagement, the firm should use the same concept of materiality that is applied by the auditor both in planning and performing the audit, and in evaluating the effect of identified misstatements on the audit and of uncorrected misstatements, if any, on the financial statements.5

4Components will therefore fall into one of three categories:

- Significant and Material

- Material but Not Significant

- Not Significant and Not Material

Key audit partners

5In a group audit, the Audit Directive requires the audit firm to designate a KAP at the group engagement level and at the level of material subsidiaries.6 A KAP is always designated at the level of the group engagement. The designation of a KAP at the component level is subject to the following assessment:

- Components which fall into Category 1 will require a KAP to be designated.

- Components which fall into Category 3 will not require a KAP to be designated.

- Components which fall into Category 2 will depend on the auditor's professional judgment as to whether Sufficient Appropriate Audit Evidence (SAAE) will be obtained on which to base the group audit opinion. Where the GET determines that work is required to be performed on the component in order to obtain SAAE7, a KAP should be designated.

6This guidance can be summarised in a flowchart as follows:

Flowchart: Decision Process for Designating a Key Audit Partner

The flowchart illustrates the process for determining if a Key Audit Partner (KAP) is required for a component.

- Start: "Is work required to be undertaken on the component in order to obtain SAAE on which to base the group audit opinion?"

- If Yes (Y), proceed to the next step.

- If No (N), proceed to the step "Is the component a material* subsidiary?".

- Next step (from Yes path): "Is the component a material* subsidiary?"

- If Yes (Y), result is "Designate KAP".

- If No (N), result is "No KAP required".

- Next step (from No path of first question): "Is the component a material* subsidiary?"

- If Yes (Y), result is "Designate KAP".

- If No (N), result is "No KAP required".

* A note below the flowchart clarifies: "Whether the component is significant or not, is irrelevant for the purposes of designating a KAP".

Group engagement team review

7Paragraph 42D-1 of ISA (UK) 600 requires the GET to evaluate and review the work performed by component auditors where that work is used for the purpose of the group audit. Whilst the Audit Directive does not define 'evaluate' or 'review', the inclusion of both terms in the requirement clearly suggests that it is an additive requirement to those requirements already in ISA (UK) 600. As there has been uncertainty about what this means in practice, the auditor should use the well-established definitions included in the Glossary of Terms:

- Evaluate - Identify and analyse the relevant issues, including performing further procedures as necessary, to come to a specific conclusion on a matter.

- Review - Appraising the quality of the work performed and conclusions reached by others.

8This additional requirement, introduced by the Directive goes further, therefore, than the existing requirement, in paragraph 42(b) which allows the auditor to "determine whether it is necessary to review other relevant parts of the component auditor's audit documentation". The Audit Directive effectively mandates a review of the component auditor's work. This goes beyond the extant requirement to evaluate the component auditor's communication as set out in paragraph 41 of ISA (UK) 600.

9Where the GET determines that work is required to be performed on a component's financial information, and that work is performed by a component auditor, the GET is required to evaluate and review that work.

10Neither the Audit Directive nor ISA (UK) 600 prescribe the nature and extent of the review of the component auditor's work – this is a matter of judgment. This judgement should reflect: the extent to which the GET has been able to evaluate and review the work performed by the CET and the results obtained; the GET's experience of review of the CET in prior periods; the relative significance of the component; and the nature of risks relevant to that component. The review of the component auditor's work will also contribute to meeting the requirement to obtain SAAE on which to base the group audit opinion.

- Where a component is financially significant8, the GET is more likely to determine it necessary to review relatively more of the component auditor's working papers.

- Where a component is significant due to certain account balances, classes of transactions or disclosures relating to significant risks of material misstatement of the group financial statements9, the GET would likely focus their review on audit documentation for these areas.

- Where a component is Material but Not Significant, the GET would likely limit their review to audit documentation that is relevant to the significant risks of material misstatement of the group financial statements.

EQCR review

11For public interest entities, the ISAs (UK) also require an engagement quality control review to be performed to assess whether the KAP(s) could reasonably have come to the opinion and conclusions expressed in the draft of the group auditor's report and the additional report to the audit committee.10

12As part of that review, the EQCR is required to consider certain elements of the group audit, including the significant risks relevant to the audit identified by the KAPs, the measures taken to adequately manage those risks and the reasoning of the KAPs with regard to those significant risks.11 The EQCR is also required to discuss the results of their review with the KAPS.12

13Accordingly, when perform an engagement quality control review for the group audit, the EQCR should also consider these elements for those components where a KAP was designated at the material subsidiary level (see Key audit partners section) and discuss the results of their review with each of those KAPs. Where there are no matters to discuss, rather than requiring the EQCR to dilute the focus of their review, by holding a series of discussions for compliance purposes only, they might instead conclude that in certain circumstances a discussion is not required. Where that is the case, this should be explained and documented on the audit file.

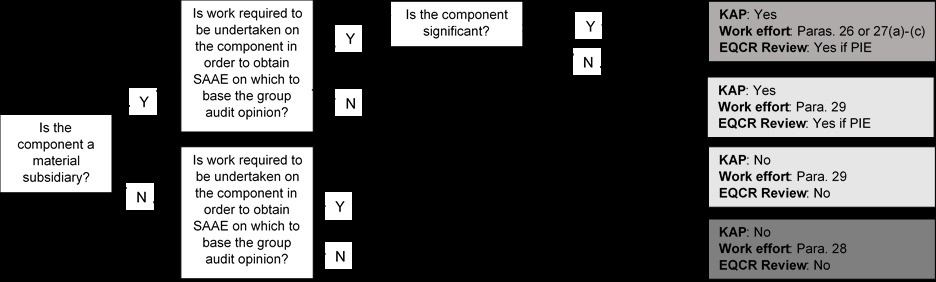

Summary

This guidance can be summarised in a flowchart and table as follows:

This table summarises the interrelationship between the new requirements and the assessment of component auditors.

| Category | Is Component: Significant? Material? | Work Required to Obtain SAAE? | Action Required Designate KAP | GET Review | EQCR Review | GAP13 only |

|---|---|---|---|---|---|---|

| 1 | Significant-Material | Yes | ✓ | ✓ | ✓ | ✓ |

| 2 | Not Significant-Material | Yes | ✓ | ✓ | ✓ | ✓ |

| 2 | Not Significant-Material | No | X | X | X | ✓ |

| 3 | Not Significant-Not Material | Yes | X | ✓ | X | |

| 3 | Not Significant-Not Material | No | X | X | X |

Colour coding denotes work effort: Most Effort Moderate Effort Least Effort

8th Floor, 125 London Wall, London EC2Y 5AS Tel: +44 (0)20 7492 2300 Fax: +44 (0)20 7492 2301 www.frc.org.uk The Financial Reporting Council Limited is a company limited by guarantee. Registered in England number 2486368. Registered office: as above.

-

ISA (UK) 600 (Revised June 2016) Special Considerations—Audits Of Group Financial Statements (Including The Work Of Component Auditors). ↩

-

ISA (UK) 600, paragraph 9(m). ↩

-

ISA (UK) 600 does not define what constitutes a significant component. This is a matter of auditor judgment. However, paragraphs A5-A6 provide some guidance. ↩

-

See FRC Technical Advisory Group – Rolling Record Of Actions Arising, pages 45–46. ↩

-

See ISA (UK) 200 (Revised June 2016) Overall Objectives of the Independent Auditor and the Conduct of an Audit in Accordance with International Standards on Auditing (UK), paragraph 6. ↩

-

See ISQC (UK) 1 (Revised June 2016) Quality Control For Firms That Perform Audits and Reviews Of Financial Statements, And Other Assurance And Related Services Engagements, paragraph 12(h)-1 for the definition of KAP and paragraph 30D-1 for the appointment of KAP(s). ↩

-

Paragraph 29 of ISA (UK) 600 sets out the requirement to perform work on non-significant components where SAAE would not otherwise be obtained. Paragraphs A51 provides guidance on the factors to consider when selecting these non-significant components and the type of work to be performed. ↩

-

See paragraph 26 of ISA (UK) 600. ↩

-

See paragraph 27(b) of ISA (UK) 600. ↩

-

See paragraph 36R-1 of ISQC (UK) 1. ↩

-

See paragraph 21R-1 of ISA (UK) 220 (Revised June 2016) Quality Control For An Audit Of Financial Statements. ↩

-

See paragraph 21R-2 of ISA (UK) 220. ↩

-

Analytical procedures performed at the group level in accordance with paragraph 28 of ISA (UK) 600. ↩