The content on this page has been converted from PDF to HTML format using an artificial intelligence (AI) tool as part of our ongoing efforts to improve accessibility and usability of our publications. Note:

- No human verification has been conducted of the converted content.

- While we strive for accuracy errors or omissions may exist.

- This content is provided for informational purposes only and should not be relied upon as a definitive or authoritative source.

- For the official and verified version of the publication, refer to the original PDF document.

If you identify any inaccuracies or have concerns about the content, please contact us at [email protected].

Audit Quality Inspection Report May 2016: BDO LLP

The FRC is responsible for promoting high quality corporate governance and reporting to foster investment. We set the UK Corporate Governance and Stewardship Codes as well as UK standards for accounting, auditing and actuarial work. We represent UK interests in international standard-setting. We also monitor and take action to promote the quality of corporate reporting and auditing. We operate independent disciplinary arrangements for accountants and actuaries, and oversee the regulatory activities of the accountancy and actuarial professional bodies.

The FRC does not accept any liability to any party for any loss, damage or costs howsoever arising, whether directly or indirectly, whether in contract, tort or otherwise from any action or decision taken (or not taken) as a result of any person relying on or otherwise using this document or arising from any omission from it.

The Financial Reporting Council Limited 2016 The Financial Reporting Council Limited is a company limited by guarantee. Registered in England number 2486368. Registered Office: 8th Floor, 125 London Wall, London EC2Y 5AS

About the FRC's Audit Quality Review team

Our objective

The FRC's mission is to promote high quality corporate governance and reporting to foster investment. The Audit Quality Review team (AQR) contributes to this objective by monitoring and promoting improvements in the quality of auditing.

What we do

AQR assesses the quality of the audits of listed and other major public interest UK entities and the policies and procedures supporting audit quality at the major audit firms in the UK. We also review audits of entities incorporated in Jersey, Guernsey or the Isle of Man whose securities are traded on a regulated market in the European Economic Area. We adopt a risk-based approach to our work and focus our reviews of individual audits on key areas specific to each review.

Our team

AQR consists of approximately 35 professional and support staff. Our inspection teams have extensive expertise with an average of 19 years post-qualification experience. Our audit quality review work is subject to rigorous internal quality control reviews. Independent non-executives oversee our work.

Working with Audit Committees (or equivalent bodies)

Audit Committees play an essential role in reviewing and monitoring the effectiveness of the audit process. We are committed to engaging with Audit Committees to improve the overall effectiveness of our reviews and to support our common objective of promoting audit quality. We speak with Audit Committee Chairs during the year as part of our work. We also send our reports on each individual audit reviewed to the Chair of the relevant Audit Committee (or equivalent body).

Priority sectors and areas of focus

Our priority sectors for inspection in 2015/16 were insurance; food, drink and consumer goods manufacturers and retailers; companies servicing the extractive industries; and business services. We reviewed a number of audits from these sectors at the firms, together with a number of first year audits which were identified as an area of focus given the extent of changes in auditors following increased audit tendering. We also paid particular attention to the audit of revenue recognition and complex supplier arrangements.

Thematic reviews

In addition to our annual programme of audit reviews, we undertake one or more thematic reviews each year. We review firms' policies and procedures in respect of a specific aspect of auditing, and their application in practice, enabling us to make comparisons between firms with a view to identifying both good practice and areas for improvement.

This year we have published reports on “Firms' audit quality monitoring” (January 2016) and "Engagement Quality Control Reviews” (February 2016). We expect all firms to take appropriate action to address the findings from our thematic reviews which apply to them.

Developments in Audit Quality 2015/16

In addition to reports on each of the major firms we have reviewed, the FRC intends to issue later in 2016 (and annually thereafter) a report on the quality of audit in the UK. This will include a report on the overall findings of our AQR activity.

- About the FRC's Audit Quality Review team

- 1. Overview

- 2. Key findings requiring action and the firm's response

- Ensure more effective audit procedures are performed for the audit of revenue

- Improve the testing of controls and ensure any change in the planned approach to rely on controls is compensated by enhanced substantive testing

- Ensure effective communication with Audit Committees

- Improve the response to the risk of fraud through more targeted testing of journals

- Embed the changes to the firm's procedures to identify independence breaches

- Strengthen the firm's monitoring procedures over its quality control systems

- 3. Assessment of the quality of audits reviewed

- Appendix A – Objectives, scope and basis of reporting

- Appendix B – How we assess audit quality

1. Overview

This report sets out the principal findings arising from the 2015/16 inspection of BDO LLP (“BDO” or "the firm") carried out by the Audit Quality Review team of the Financial Reporting Council ("the FRC"). We conducted this inspection in the period from March 2015 to January 2016 ("the time of our inspection"). We inspect BDO, and report publicly on our findings, annually.

Our report focuses on the key areas requiring action by the firm to safeguard and enhance audit quality. It does not seek to provide a balanced scorecard of the quality of the firm's audit work. Our findings cover matters arising from our reviews of both individual audits and the firm's policies and procedures which support and promote audit quality.

Section 2 sets out the principal findings arising from our reviews and the actions taken or to be taken by the firm.

Section 3 sets out our overall assessment of the quality of the audits we reviewed in our 2015/16 inspection and how it compares with our assessments for the previous four years.

Appendix A sets out our objectives, scope and basis of reporting.

Appendix B explains how we assess audit quality and explains the basis of our categories of audit quality.

We acknowledge the co-operation and assistance received from the partners and staff of the firm in the conduct of our 2015/16 inspection.

Scope of our 2015/16 inspection

Our inspection comprised a review of the firm's policies and procedures supporting audit quality and reviews of selected aspects of individual audits.

The areas covered by our review of the firm's policies and procedures included:

- Tone at the top;

- Independence and ethics;

- Audit methodology, training and guidance; and

- The firm's own audit quality monitoring.

We reviewed selected aspects of eight individual audits in 2015/16. In selecting which aspects of an audit to inspect, we took account of those areas identified to be of higher risk by the auditors and Audit Committees, our knowledge and experience of audits of similar entities and the significance of an area in the context of the audited financial statements.

Key findings

In response to the findings from our last inspection, the firm has implemented the agreed actions and has continued to enhance its procedures, including:

- Training and enhanced guidance have been provided to cover AQR findings, other regulatory and internal reviews and other audit matters.

- The resources of the firm's Ethics function have increased.

- New processes for monitoring and resolving independence queries have been introduced.

Our key findings in the current year requiring action by the firm which are elaborated further in section 2 together with the firm's actions to address them, are that the firm should:

- Ensure more effective audit procedures are performed for the audit of revenue.

- Improve the testing of controls and ensure any changes in the planned approach to rely on controls is compensated by enhanced substantive testing.

- Ensure effective communication with Audit Committees.

- Improve the response to the risk of fraud through more targeted testing of journals.

- Embed the changes to the firm's procedures to identify independence breaches.

- Strengthen the firm's monitoring procedures over its quality control systems.

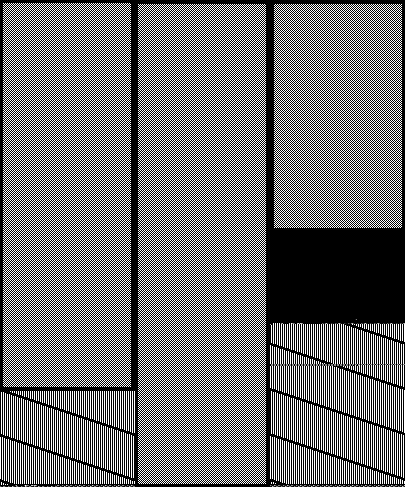

The following chart shows our assessment of the quality of the firm's audits which we reviewed in 2015/16 with comparative information for 2013/15. Further details are provided in section 3.

Assessment of Quality of Audits Reviewed

Bar chart showing the quality of audits reviewed for 2015/16 compared to 2013/15. Categories are 'Good with limited improvements required', 'Improvements required', and 'Significant improvements required'. For 'Good with limited improvements required': 2015/16 shows 4 audits, 2013/15 shows 5 audits. For 'Improvements required': 2015/16 shows 4 audits, 2013/15 shows 2 audits. For 'Significant improvements required': 2015/16 shows 0 audits, 2013/15 shows 1 audit.

None of the audits inspected in 2015/16 were assessed as requiring significant improvement.

Section 3 sets out examples of good practice which contributed to audits being assessed as requiring no more than limited improvements. It also sets out the principal issues resulting in audits being assessed as requiring more than limited improvements.

We expect all the firms we inspect to make continuous improvements such that, by 2019, at least 90% of FTSE 350 audits reviewed will be assessed as requiring no more than limited improvements1.

Root cause analysis

Thorough and robust root cause analysis is necessary to enable firms to develop effective action plans which are likely to result in improvements in audit quality being achieved. At our request, the firm has performed root cause analysis in respect of our key findings in this report.

Firm's overall response and actions: We continue to place quality at the top of our agenda and we welcome the acknowledgement that we have implemented actions and enhanced our procedures in response to the findings from the last inspection. We appreciate the feedback provided to us by the review team which is a valuable contribution to enable us to fulfil our commitment to improving audit quality.

We would like to thank the review team for the professional way in which they conducted our review.

We have considered the root causes of the issues identified during the review. In doing so we have identified two contributory factors in relation to the findings regarding the audit of revenue and the testing of controls. These were that our detailed understanding of certain aspects of the audited entities' revenue systems could have been improved and that the audit team's should have been more closely involved with work that was undertaken by the firm's IT specialists in order to ensure that it focused appropriately on key controls. The firm will shortly be implementing an amendment to its methodology which relates to the way in which controls relevant to the audit are assessed. This will require us to re-emphasise the importance of analysing the audited entities' systems in order to identify key controls to design an effective audit strategy.

The fact that the above issues arose also led us to conclude that the review processes performed by more senior members of the team could be improved, in particular ensuring that there is sufficient documentation on file in support of the work that has been done. We consider that proper project management of the audit process by a member of the audit team to ensure that the appropriate work is completed and reviewed by the right person at the right time is an important factor in ensuring that the above issues are addressed. We are currently undertaking a project to investigate how project management can be strengthened during the audit process.

We have implemented a number of changes as a result of a full scale review of partners' financial interests and continue to monitor the adequacy of our policies and procedures in this area. The firm introduced new client take on systems during the year which includes robust measures to prevent the provision of non audit services to audit clients without the prior approval of the audit partner.

2. Key findings requiring action and the firm's response

We set out below the key areas where we believe improvements are required to safeguard and enhance audit quality and safeguard auditor independence. The firm was asked to provide a response setting out the actions it has taken or will be taking in each of these areas.

Ensure more effective audit procedures are performed for the audit of revenue

Revenue is an important driver of an entity's operating results and auditors need to evaluate and address fraud and other risks in relation to revenue recognition. A failure to perform sufficient audit work in this area increases the risk that a material misstatement of revenue in the financial statements will not be identified.

The audit of revenue was the area where we raised the most findings. These primarily related to the following areas:

- Adequacy of substantive analytical procedures: expectations should be developed from independent sources, with explanations obtained and corroborated. In one audit the source of the information was not sufficient to develop the expectations adequately and in another audit there was insufficient corroboration of management's explanations regarding variations from expectations.

- Sufficiency of the substantive evidence to address the cut off assertion: on three audits insufficient evidence was obtained to confirm that revenue was recorded in the correct period.

- Testing of revenue through data analytics (“CAATs”): data analytics can be an effective way of obtaining audit evidence when appropriately performed. In one audit there were insufficient audit procedures for testing the completeness and accuracy of the source data used in the CAATS.

Firm's actions: In carrying out our root cause analysis in this area we have identified a contributory factor to the issues identified above which is that our detailed understanding of certain aspects of the audited entities' revenue systems could have been improved. This resulted in certain aspects of the test design not being focussed appropriately.

Considering the specific points raised we would note the following:

- Substantive Analytical Procedures (SAPs) guidance, which will focus on the decision as to whether SAPs are a suitable response to the level of risk identified and will re-emphasise key aspects such as how expectations should be developed and the need to corroborate management's explanations, will be released by the end of June 2016.

- A number of communications to date have emphasised the importance of the team documenting a thorough understanding of the system (both manual and IT aspects) during the planning stages of the audit. We have created a network of local IT champions who will support the firms IT specialists.

- The Firm will also be implementing changes to the methodology and the way in which controls are assessed as relevant to the audit and this will be used as an opportunity to re-emphasise the importance of a good understanding of an entity's systems including the interaction with our IT specialists. This will commence in June 2016.

- Information produced by the entity (IPE) has been covered a number of times in the last quarter of 2015. IPE guidance has been released and IT champions briefed on the importance of testing the completeness and accuracy of source data.

Improve the testing of controls and ensure any change in the planned approach to rely on controls is compensated by enhanced substantive testing

Testing the operational effectiveness of controls is necessary to provide the auditor with a proper basis on which to place reliance on them. This includes testing controls over the access and operation of an entity's IT systems, as well as any relevant manual controls. The firm's audit methodology requires that, when a controls approach is taken, the majority of the audit evidence for the relevant area of the financial statements should be obtained from controls testing.

Our findings related to the audit procedures to ensure that controls operated effectively and could be relied upon, and included the adequacy of testing over manual controls and IT general controls, including logical access and program change controls:

- On one audit insufficient evidence was obtained to confirm that the cash reconciliation controls were operating effectively.

- On one audit, where there had been a change in systems during the year, there was insufficient testing of changes to the old system and over the effectiveness of controls in the new system, including weaknesses identified in the operations of controls. On another audit, there was no testing of certain IT general controls to support reliance on automated reports.

We identified situations where the substantive procedures had not been enhanced to compensate for the weaknesses in controls testing. In view of the weighting given to the audit evidence obtained from controls testing in the firm's methodology, it is important for audit teams to increase the level of substantive testing where the planned level of evidence is not obtained from controls testing.

Firm's actions: In considering the issues that arose in this area we identified that whilst teams were using the firm's IT specialists where appropriate, the audit teams were not always sufficiently involved in the work that was undertaken by the specialist team.

The specific issues noted were a consequence of the above. In addition, the teams did not fully appreciate the level of detailed testing required.

As noted above the firm is implementing a number of changes to its audit methodology which will result in retraining in this area, in particular a focus on controls relevant to the audit. This will also entail a fresh approach to the consideration of complexity in IT systems. IT champions have been created for each office to assist audit teams in the mapping of IT systems and IT general and application controls.

Ensure effective communication with Audit Committees

Effective communication with Audit Committees is important to assist both the auditors and the Audit Committees in discharging their responsibilities.

We reviewed the communications with Audit Committees on all audits. We found examples of good communications between audit teams and the Audit Committees. However, on a number of audits we identified areas where the communications could have been improved, for example:

- Changes in the planned audit approach not being communicated to the Audit Committee.

- Insufficient reporting on IT control weaknesses.

- Insufficient reporting on certain areas of judgment.

- A failure to report audit findings sufficiently in advance of the Audit Committee meeting.

Firm's actions: We acknowledge the importance of accurate and timely communications with the audit committee. We have recently undertaken a project to update our audit committee reporting guidance and we communicated to the audit stream in October 2015 the importance of timely communications that are consistent with the work performed and the audit findings. The issues identified above were used as examples to remind audit teams about proper practise in this area.

Improve the response to the risk of fraud through more targeted testing of journals

Auditors need to evaluate and address fraud risks in relation to the financial statements. The testing of journals is one of the procedures required by auditing standards to respond to the risk of fraud. A failure to perform sufficient audit work in this area increases the risk that a material misstatement in the financial statements relating to fraud would not be identified.

On several audits there was insufficient focus on the fraud risk characteristics when determining which journals should be tested. Further, on one audit there was no evidence of journals testing for the largest component within the group.

Firm's actions: The systems of audited entities are becoming increasingly complex and we are therefore investing in developing tools to address audit risk in these complex areas with a significant volume of transactions. IT specialists will be involved where necessary but new audit tools such as BDO Advantage (our data analytics tool) will allow audit teams to perform similar audit tests themselves. BDO Advantage was introduced to the audit stream towards the end of 2015 and is currently being rolled out to all audit teams. At the same time we are taking the opportunity to remind audit teams of the importance of understanding the specific risk characteristics of each audited entity to ensure that testing performed on journals is focused and effective.

We issued a reminder to audit teams in January 2016 about the importance of timely filing of all audit evidence and documentation on to the audit file.

Embed the changes to the firm's procedures to identify independence breaches

A lack of appropriate procedures to ensure that independence breaches are identified or prevented could compromise the independence and objectivity of the firm's audit work.

Following our prior year findings on independence matters, the firm introduced a system to test partners' financial interests on a rolling basis over an average three year cycle. Given the timing of implementation, the results were not available at the time of our review.

The firm should embed the changes to its procedures to enable it to identify ethical and independence breaches on a timely basis.

Firm's actions: Following a review of our procedures, policies and systems regarding partner's financial interests, which included inter-alia, consideration of the root cause of a small number of self-identified, and self-reported breaches, we implemented a number of changes.

As noted, one significant enhancement was the introduction in the autumn of 2015 of a rolling programme of auditing of partners' financial interests. We will continue to monitor the adequacy of our policies and procedures in this important area.

With regard to non-audit services, a new automated Client Take on (CTO) system directly refers potential non-audit engagements with audit clients to the RI for approval.

Strengthen the firm's monitoring procedures over its quality control systems

A robust audit quality monitoring process is important in identifying areas where improvements can be made and also enables high quality audit work to be recognised. As part of this process, the firm evaluates the effectiveness of its quality control systems and reviews the quality of completed audits.

We reviewed the firm's Audit Quality Assurance Review (AQAR) process as part of the AQR thematic review, the results of which were published in January 2016. Our findings mainly related to the firm's procedures to monitor the effectiveness of the firm's quality control systems, in particular:

- The scope of testing: the AQAR process did not cover some of the areas of quality control which we selected for review.

- The approach to office visits, including sample sizes: the AQAR includes a review of procedures at specific offices. We found that the approach to the office inspections, including the sample sizes used for testing, was inconsistent.

Firm's actions: Given the importance of a robust quality monitoring process we have recently reviewed our policies and procedures in this area. Our previous approach was deliberately designed to allow flexibility in dealing with the variety of our offices and was appropriate in the circumstances, however the firm has changed over recent years and a new approach is needed. From 2016 onwards Firmwide monitoring will be managed centrally to improve consistency and ensure all areas are reviewed annually.

3. Assessment of the quality of audits reviewed

We reviewed selected aspects of eight individual audits in 2015/16, none of which were first year engagements.

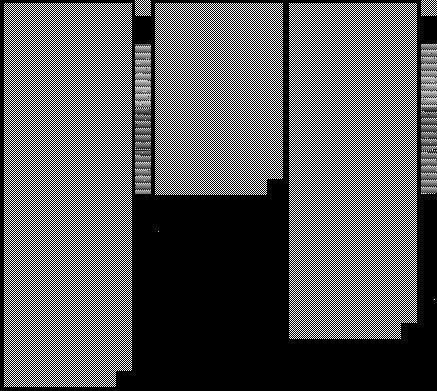

The bar chart below shows the results of our assessment of the quality of the audits we reviewed in 2015/16, with comparatives for the previous four years2. The number of audits within each category in each year is shown at the top of each bar.

Assessment of Quality of Audits Reviewed - 2011-2016

Bar chart showing the quality of audits reviewed from 2011-2016. Categories are 'Good with limited improvements required', 'Improvements required', and 'Significant improvements required'. For 'Good with limited improvements required': 2015/16 shows 4 audits, 2013/15 shows 5 audits, 2011/13 shows 2 audits. For 'Improvements required': 2015/16 shows 4 audits, 2013/15 shows 2 audits, 2011/13 shows 3 audits. For 'Significant improvements required': 2015/16 shows 0 audits, 2013/15 shows 1 audit, 2011/13 shows 2 audits.

We identified the following example of good practice in 2015/16 which contributed to audits being assessed as requiring no more than limited improvements:

- The evidence of involvement of senior team members in key aspects of the audit.

- The level of involvement of group audit teams in the audit of overseas components.

The principal issues resulting in four audits being assessed as requiring more than limited improvements in 2015/16 included the following (further details of which are set out in section 2):

- A lack of sufficient substantive audit evidence in relation to revenue.

- Deficiencies in the testing of controls on which reliance was placed.

Audits inspected in 2015/16

We estimate that the firm audited 87 UK entities within the scope of independent inspection as at 31 December 2014. Of these entities, our records show that 54 had securities listed on the main market of the London Stock Exchange, including three FTSE 250 companies. In addition there were five audits within our scope, including one FTSE 100 company, relating to entities incorporated in Jersey, Guernsey or the Isle of Man whose securities are traded on a regulated market in the European Economic Area.

The following chart provides a breakdown of the audits inspected in 2015/16 by type of entity3:

Audits reviewed by type of entity

Bar chart showing the number of audits reviewed by type of entity: * FTSE 100: 1 review * FTSE 250: 0 reviews * Other Listed: 1 review * AIM: 3 reviews * Other: 0 reviews

Audit Quality Indicators

The firm's transparency report for the year ended 30 June 2015 includes certain Audit Quality Indicators (AQIs) which the six largest audit firms are using. We believe that such AQIs provide useful additional information to those wishing to understand firms' approaches to monitoring and improving audit quality.

We are pleased that firms have made a good start in identifying and monitoring AQIs. We would, however, encourage them to gather the relevant data on a more consistent basis and follow-up the results more effectively.

Audit Quality Review FRC Audit Division May 2016

Appendix A – Objectives, scope and basis of reporting

| Matter | Explanation |

|---|---|

| Objectives of our inspection | The overall objective of our work is to monitor and promote improvements in the quality of auditing. As part of our work, we monitor compliance with the regulatory framework for auditing, including the Auditing Standards, Ethical Standards and Quality Control Standards for auditors issued by the FRC and other requirements under the Audit Regulations issued by the relevant professional bodies. The standards referred to in this report are those effective at the time of our inspection, or, in relation to our reviews of individual audits, those effective at the time the relevant audit was undertaken. |

| Audits in the scope of our inspection | In addition to the UK audits in scope, as stated in section 3 of our report, the UK firm audits a number of entities incorporated in Jersey, Guernsey or the Isle of Man whose securities are traded on a regulated market in the European Economic Area. These audits are inspected by us under separate arrangements agreed with the relevant regulatory bodies in those jurisdictions. The results of these reviews are included in this report. Our records show that, at the time of our inspection, the firm had five such audits, including one FTSE 100 company. BDO also supplies audit services to local authorities and the NHS (Local Public Audits - LPAs). Whilst we review LPAS undertaken by firms, this is done under separate arrangements agreed with the Public Sector Audit Appointments Limited (PSAA), previously the Audit Commission. The results of these reviews are not included in this report because the LPA inspections fulfil a different purpose to those considered in this report. These reviews of LPAs form part of the PSAA's assessment of the quality of contracted-out audits. The PSAA publishes its assessment both in overall terms and individually by firm. The most recent reports can be found on its website. |

| Impact of our risk-based inspection approach | Our inspection was not designed to identify all weaknesses which may exist in the design and/or implementation of the firm's policies and procedures supporting audit quality or in relation to the performance of the individual audit engagements selected for review and cannot be relied upon for this purpose. |

| Key audit areas inspected | In selecting which aspects of an audit to inspect, we take account of those areas considered to be higher risk by the auditors and Audit Committees, our knowledge and experience of audits of similar entities and the significance of an area in the context of the audited financial statements. The rationale for including each area of audit work (or excluding any area of focus listed in the auditors' report) is documented as part of the planning process for each audit inspected. |

| Our reports on individual audits | We issue a report on each individual audit reviewed during an inspection to the relevant audit engagement partner or director and the chair of the relevant entity's Audit Committee (or equivalent body). |

| Our emphasis on improvements to audit quality | We seek to identify areas where improvements are, in our view, needed in order to safeguard audit quality and/or comply with regulatory requirements and to agree an action plan with the firm designed to achieve these improvements. Accordingly, our reports place greater emphasis on weaknesses identified which require action by the firm than areas of strength and are not intended to be a balanced scorecard or rating tool. |

| Basis of our public reporting | While our public reports seek to provide useful information for interested parties, they do not provide a comprehensive basis for assessing the comparative merits of individual firms. The findings reported for each firm in any one year reflect a wide range of factors, including the number, size and complexity of the individual audits selected for review which, in turn, reflects the firm's client base. An issue reported in relation to a particular firm may therefore apply equally to other firms without having arisen in the course of our inspection fieldwork at those other firms in the relevant year. Also, only a small sample of audits is selected for review at each firm and the findings may therefore not be representative of the overall quality of each firm's audit work. |

| Purpose of this report | This report has been prepared for general information only. The information in this report does not constitute professional advice and should not be acted upon without obtaining specific professional advice. To the full extent permitted by law, the FRC and its employees and agents accept no liability and disclaim all responsibility for the consequences of anyone acting or refraining from acting in reliance on the information contained in this report or for any decision based on it. |

| Inspection findings included in our public report | We exercise judgment in determining those findings to include in our public report on each inspection, taking into account their relative significance in relation to audit quality, in the context of both the individual inspection and any areas of particular focus in our overall inspection programme for the year. Where appropriate, we have commented on themes arising or issues of a similar nature identified across more than one audit. |

| Inspection of audits outside our scope | The professional accountancy bodies in the UK register firms to conduct audit work. Their monitoring units are responsible for monitoring the quality of audit engagements falling outside the scope of our work but within the scope of audit regulation in the UK. Their work, which is overseen by the FRC, covers audits of UK incorporated companies and certain other entities which do not have any securities listed on the main market of the London Stock Exchange and are not otherwise defined as being within the scope of our work. All matters raised in this report are based solely on the work which we carried out for the purposes of our inspection. |

Appendix B – How we assess audit quality

We assess the quality of the audit work we inspect using the following four categories:

- Good (category 1);

- Limited improvements required (category 2A);

- Improvements required (category 2B); and

- Significant improvements required (category 3).

The assessments of the quality of the audits we reviewed in our public reports on individual firms combine audits assessed as falling within categories 1 and 2A.

These four categories have been used consistently since 2008, although there have been some minor refinements to the category descriptions over the years. They reflect our assessment of the overall significance of the areas requiring improvement that we have reported to the Audit Committee and the auditor. We expect the auditor to make appropriate changes to its audit approach for subsequent years to address all issues raised.

An audit is assessed as good where we identified no areas for improvement of sufficient significance to include in our formal report. Category 2A indicates that we had only limited concerns to report. Category 2B indicates that more substantive improvements were needed in relation to one or more issues reported.

An audit is assessed as requiring significant improvements (category 3) if we have significant concerns in relation to the sufficiency or quality of audit evidence, the appropriateness of key audit judgments or other matters identified. In such circumstances we may request some remedial action by the firm to address our concerns and to confirm that the audit opinion remains appropriate. We will generally review a subsequent year's audit to confirm that appropriate action has been taken.

We exercise judgment in assessing the significance of issues identified and reported. Relevant factors in assessing significance include the materiality of the area or matter concerned, the extent of concerns regarding the sufficiency or quality of audit evidence, whether appropriate professional scepticism appears to have been exercised, and the extent of non-compliance with Standards or a firm's methodology.

Our inspections focus on how selected aspects of a particular audit were performed. They are not designed to assess whether the information being audited was correctly reported. An assessment that an audit required significant improvements, therefore, does not necessarily mean that an inappropriate audit opinion was issued, the financial statements failed to show a true and fair view or that any elements of the financial statements were not properly prepared.

Equally, where we have assessed an audit as requiring significant improvements, this does not necessarily imply potential misconduct on the part of an individual or audit firm which may warrant investigation and/or enforcement action by the FRC.

Financial Reporting Council 8th Floor 125 London Wall London EC2Y 5AS +44 (0)20 7492 2300 www.frc.org.uk

-

FRC Plan and Budget 2016/17 ↩

-

Changes to the proportion of audits falling within each category from year to year reflect a wide range of factors, which may include the size, complexity and risk of the individual audits selected for review and the scope of the individual reviews. For this reason, and given the sample sizes involved, changes from one year to the next are not necessarily indicative of any overall change in audit quality at the firm. ↩

-

The listed entities whose audits we reviewed include two investment trusts or similar entities. ↩