The content on this page has been converted from PDF to HTML format using an artificial intelligence (AI) tool as part of our ongoing efforts to improve accessibility and usability of our publications. Note:

- No human verification has been conducted of the converted content.

- While we strive for accuracy errors or omissions may exist.

- This content is provided for informational purposes only and should not be relied upon as a definitive or authoritative source.

- For the official and verified version of the publication, refer to the original PDF document.

If you identify any inaccuracies or have concerns about the content, please contact us at [email protected].

Cash flow statements and liquidity (IAS 7, IFRS 7)

Key to symbols

- ✅ Represents good practice

- ⚠️ Represents an omission of required disclosure or other issue

- 💡 Represents an opportunity for enhancing disclosures

Examples of better disclosure...

Including some identified from our routine monitoring of corporate reports (marked *).

1. Executive summary

Introduction

Recent Annual Reviews1 have identified cash flow statements as an area requiring significant improvement in view of the frequency of errors identified in our corporate reporting reviews. The objective of this thematic review is to explore in more detail issues identified in our routine work as well as to consider some of the themes from the FRC Lab's project: Disclosures on the sources and uses of cash2. This includes providing further guidance to avoid some of the more common errors that have been identified from routine reviews.

Our review of liquidity risk disclosures included consideration of companies' assessments of going concern and longer-term viability because the management of cash flows and liquidity risk is an integral feature of these assessments, both of which contain disclosures relevant to liquidity risk.

When this thematic review was announced in December 2019, we explained that we would also consider companies' disclosure of liquidity risk. Since then, a number of topics that this thematic was designed to cover were included in the Covid-19 thematic review. However, we believe there is value in exploring some of the liquidity risk points in more detail and provide further examples of better disclosure. Our sample included companies reporting both before and after the UK lockdown from March.

We selected companies from a range of sectors and industries, including several which are perceived to face greater risks concerning cash flow, liquidity and viability. This included general retailers, retail property, and tourism and leisure. We initially selected a sample of 20 annual reports and accounts; however, the sample was extended to 30 companies as we saw the value of considering a greater number of accounts published since April.

Key findings

Cash flow statement

The majority of companies complied with the requirements of IAS 7 in the presentation of the cash flow statement. However, in line with our findings from routine reviews, we challenged companies where requirements did not appear to be met, due to:

- Material inconsistencies between items in the cash flow statement and the notes

- Missing or incorrectly classified cash flows

- Inconsistencies between financing cash flows and the reconciliation of changes in liabilities arising from financing activities in the notes

We also identified several areas for improvement in the disclosure of accounting policies for the treatment of significant and large one-off transactions in the cash flow statement. Consistent with our findings from routine reviews, we note most companies could improve their disclosures of accounting policies and judgements in relation to the cash flow statement.

Liquidity

Several companies published their accounts before the UK lockdown in March and many of these accounts contained only boiler plate disclosures in respect of liquidity risk and related issues. There was, however, a marked improvement in going concern, viability and liquidity disclosures following the initial economic impact of Covid-19, most notably in smaller listed companies. The findings on liquidity risk disclosures in this thematic are consistent with the findings of our thematic review on the financial reporting effects of Covid-19 published in July 2020.

The majority of companies in our sample that published their accounts from April onwards disclosed key liquidity information such as availability of cash, undrawn borrowing facilities and compliance with covenants. We did, however, identify that some companies could improve their disclosures of covenant testing, and assumptions and judgements around going concern and viability.

2. Scope and sample

Background and scope of our review

Our review consisted of a limited scope desktop review of the annual reports and accounts of 30 entities.

As part of our routine monitoring activity, we often ask companies for additional information regarding the nature or classification of transactions presented in the cash flow statement.

In the light of the downturn in the worsening economic outlook, particularly as a result of the impact of Covid-19, liquidity disclosures are under increasing scrutiny from investors.

Therefore, we considered the comprehensiveness and quality of cash flow and liquidity disclosures throughout the annual report and accounts, including compliance with the requirements of IAS 7 'Statement of Cash Flows' and IFRS 7 'Financial Instruments: Disclosures'.

We also considered the following areas that are linked to cash and liquidity:

- Strategic report, including the use of cash and liquidity based alternative performance measures ('APMs')

- Viability statement

- Going concern assessment.

In line with our philosophy of promoting continuous improvement in reporting, we have identified both examples of better practice and areas for improvement. The examples are taken from reviews performed for the purpose of this thematic, as well as our routine reviews.

Our sample

We initially planned to review the full-year accounts of a sample of 20 entities, including 12 companies with December year ends, most of which reported before the UK lockdown in March. As a result of the impact of Covid-19, we extended the sample to 30 to allow the inclusion of more companies reporting from April onwards.

Our sample covers a cross section of industries, with a focus on industries which are potentially facing particular liquidity stress such as travel and leisure, and high street retailers.

Our sample did not include financial services companies such as banks and insurers, which are subject to regulatory capital, liquidity and solvency regimes.

INDUSTRIES SAMPLED

Pie chart showing the distribution of sampled industries: - Travel & Leisure: 20% - Industrial Goods & Services: 13% - Retail: 13% - Personal & Household Goods: 10% - Food & Beverage: 7% - Construction & Materials: 6% - Media: 7% - Real Estate: 7% - Technology: 7% - Other: 10%

3. Key findings

Cash flow statement

Findings of previous routine reviews

The cash flow statement has featured in the top ten most frequently raised topics in our corporate reporting reviews in recent years, as highlighted in successive editions of our Annual Reviews of Corporate Reporting. It ranked as the seventh area of challenge in our reviews last year1.

Our reviews continue to highlight significant concerns regarding the preparation of some companies' cash flow statements. In 2019/20, five companies (2018/19: 4, 2017/18: 7) restated their cash flow statements as a result of our enquiries. We are concerned that most of these errors were basic in nature and were evident from our desktop review of the accounts. We believe that the errors could have been avoided by robust pre-issuance review by companies, built into their financial statement close process. We have, therefore, provided further information about the nature of the questions we have raised on the cash flow statement in the last three years to help companies avoid regulatory challenge.

The most frequent questions related to investing activities, the definition of cash and cash equivalents, the reconciliation of profit to net cash flows from operating activities, the acquisition or disposal of subsidiaries, and incorrect classification of cash flows.

We also wrote to companies on a number of areas where we considered disclosures had been omitted or could be improved. The most common areas related to the disclosures of changes in liabilities arising from financing activities (IAS 7.44A). Other common issues related to the acquisition and disposal of subsidiaries, and cash flows from investing activities.

IAS 7 DETAILED QUESTIONS BY TOPIC

Pie chart showing the distribution of detailed questions by topic: - Investing activities - Other - Bank borrowings included in cash and cash equivalents - Direct / indirect method - IAS 7.44A disclosures - Non-cash transactions - Reconciliation to operating profit - Definition of cash & cash equivalents - Acquisition / disposal of subsidiaries

IAS 7 DISCLOSURE IMPROVEMENTS BY TOPIC

Pie chart showing the distribution of disclosure improvements by topic: - Disclosure of changes in liabilities arising from financing activities - Acquisition / disposal of subsidiaries - Investing activities - Additional liquidity disclosures - Definition of cash & cash equivalents - Interest presentation - Other

Summary of historical cash flow statement errors where corrective action was required

A list of cash flow statement errors requiring restatement following a corporate reporting review is included in the appendix at the end of this report. We encourage companies to consider these matters as they provide an indication of the types of issues companies should look for, and correct, when performing their pre-issuance reviews.

A summary of the impact of these cash flow statement errors requiring restatement is presented in the graphs showing, as a percentage of the number of cases, whether the impact of the correction led to an increase, decrease or no change for each cash flow statement category.

This analysis shows that there is not necessarily a clear trend to the cash flow statement errors, with errors leading to increases and decreases in cash flows included in all three categories. We found examples of restatements distorting each possible pairing of categories (for example reclassifications between operating and investing, operating and financing, and investing and financing), and several which were included in all three categories. Some restatements resulted in no net change in cash flows, while others impacted the net cash flows for the period.

Our analysis does, however, show that errors to operating and investing cash flows (75% of cases requiring restatement) appear to be more frequent than errors in financing cash flows (44% of cases requiring restatement). Further information on the nature of these errors is provided in the appendix.

Impact on operating cash flows (% of cases)

Pie chart showing 31% Increase, 44% Decrease, 25% None.

Impact on investing cash flows (% of cases)

Pie chart showing 31% Increase, 44% Decrease, 25% None.

Impact on financing cash flows (% of cases)

Pie chart showing 25% Increase, 19% Decrease, 56% None.

Findings from this thematic

Our findings for this thematic were generally consistent with our annual routine reviews. Most companies presented a cash flow statement that complied with the requirements of IAS 7. However, we found some cases of potential non-compliance and have written to three companies, out of our sample of 30, with substantive questions relating to their cash flow statement.

Many of our questions result from straightforward consistency checks between amounts presented in the cash flow statement and other primary statements and notes.

Definition of cash3 and cash equivalents

Paragraph 6 of IAS 7 states that “cash comprises cash on hand and demand deposits". It also describes cash equivalents as short-term, highly liquid investments that are readily convertible to known amounts of cash and which are subject to an insignificant risk of changes in value.

Paragraph 45 of IAS 7 requires a reconciliation of the amounts shown as cash and cash equivalents in the statement of cash flows with the equivalent items reported in the statement of financial position.

Judgement may have to be exercised in determining what comprises cash and cash equivalents. While IAS 7 provides only limited guidance on the meaning of 'cash', it is generally well understood. Judgement may exist as to what comprises cash equivalents based on the terms of particular instruments and the company's practices. The standard states that investments will normally qualify as cash equivalents only if the maturity, at acquisition, is less than three months.

Bank overdrafts, in certain circumstances, may be included as part of cash equivalents in the cash flow statement (see section below on the Composition of cash and cash equivalents). Where this is the case, we expect disclosure of the basis for including overdrafts within cash equivalents and a reconciliation between cash and cash equivalents as presented in the cash flow statement and the corresponding items in the statement of financial position.

We expect companies to provide a sufficiently detailed accounting policy to explain what is included within cash and cash equivalents.

Composition of cash and cash equivalents

IAS 7 requires cash equivalents to be held for the purpose of meeting short-term cash commitments and be subject to an insignificant risk of changes in value, with a short maturity of three months or less from the date of acquisition. Bank overdrafts which are repayable on demand may be included as a component of cash and cash equivalents.

IAS 7 also requires disclosures of any restrictions on the use of cash and cash equivalents by the group.

The types of borrowings which can be included as a component of cash and cash equivalents, for the purpose of the cash flow statement, were considered by the IFRS Interpretations Committee ("the Committee”) in March 20184. The fact pattern considered short-term loans and credit facilities that have a short contractual notice period (for example, 14 days). The agenda decision includes the observation that 'if the balance of a banking arrangement does not often fluctuate from being negative to positive, then this indicates that the arrangement does not form an integral part of the entity's cash management and, instead, represents a form of financing.'

Examples of better disclosure included:

- An accounting policy detailing what constitutes cash and cash equivalents;

- Analysis of the components of cash and cash equivalents, for example, cash at bank, short term deposits, money market funds;

- Description of the terms of deposits, such as maturity, break clauses and interest rates;

- Whether overdrafts are included within cash and cash equivalents and, if so, the terms of such arrangements; and

- Disclosure of the amount of restricted cash and the nature of the restrictions.

Composition of cash and cash equivalents (cont.)

⚠️ We identified one company where an invoice discounting facility was treated as part of cash and cash equivalents in the cash flow statement, despite appearing not to fluctuate between an asset and liability position.

Examples of better disclosure...

"Cash and cash equivalents Included within cash and cash equivalents are amounts held by the Group's travel and insurance businesses which are subject to contractual or regulatory restrictions. These amounts held are not readily available to be used for other purposes within the Group and total £98.2m (2019: £108.6m).

Cash at bank earns interest at floating rates based on daily bank deposit rates. Short term deposits are made for varying periods of between one day and three months, depending on the immediate cash requirements of the Group, and earn interest at the respective short term deposit rates.

The bank overdraft is subject to a guarantee in favour of the Group's bankers and is limited to the amount drawn. The bank overdraft is repayable on demand."

Saga plc, Annual Report and Accounts 2020, p174

Treatment of interest and dividends

IAS 7 allows an accounting policy choice for the presentation of interest and dividends. Interest paid and interest and dividends received may be classified as operating cash flows because they enter into the determination of profit or loss. Alternatively, interest paid and interest and dividends received may be classified as financing cash flows and investing cash flows respectively, because they are costs of obtaining financial resources or represent returns on investments.

We expect companies to select an appropriate accounting policy for the presentation of interest, including interest relating to leases, and dividends and to apply this consistently.

⚠️ We identified several companies through our routine reviews which did not apply a consistent, IAS 7 compliant, accounting policy for the presentation of interest and dividends.

Cash flows from operating activities

All companies in our sample used the indirect method, where profit and loss is adjusted for the effects of non-cash items, showing a reconciliation from profit before tax to net cash from operating activities, either on the face of the cash flow statement or in the notes, as required by paragraph 20 of IAS 7.

Our previous thematic, “Reporting by Smaller Listed and AIM Quoted Companies" contained an example reconciliation between the cash flows from movements in working capital and amounts presented in the statement of financial position. We believe disclosures of this nature are helpful where the cash flow impact of working capital movements is not apparent from the changes in the statement of financial position, for example, due to business combinations in the year.

Examples of better disclosures included:

- A reconciliation to explain the cash flow impact of working capital movements, where this was not apparent from the statement of financial position;

- A logical ordering of the items presented, for example, grouping similar items together such as working capital movements and non-cash items; and

- References to relevant notes.

The issues we identified in respect of operating cash flows included:

- ⚠️ Changes in cash flows from working capital which were inconsistent with movements in the statement of financial position; and

- ⚠️ Material unexplained variances in impairment and depreciation charges between the cash flow statement reconciliation and the notes to the accounts.

Cash flows from investing activities

Paragraph 16 of IAS 7 requires that only expenditure that results in a recognised asset in the statement of financial position is eligible for classification as investing activities.

We expect companies to exclude cash flows that do not result in a recognised asset within investing activities, such as acquisition expenses in a business combination or settlement of provisions.

For many companies in our sample, the cash flows from investing activities agreed to the amounts presented in the notes. Where there are material differences, we believe it would be helpful to provide an explanation.

Examples of better disclosures included:

- References to notes which agreed to the amounts presented in the cash flow statement; and

- A reconciliation between the cash flows in the cash flow statement and notes where the reason for the difference was not apparent.

The issues identified included:

- ⚠️ Material unexplained differences in additions to property, plant and equipment between the cash flow statement and the property, plant and equipment notes; and

- ⚠️ Settlements of provisions and other liabilities being presented as investing cash flows.

Examples of better disclosure...

Cash flows from investing activities

NEXT PLC, Annual Report and Accounts 2019*, p136

Acquisition and disposal of subsidiaries

Paragraph 39 of IAS 7 states that the aggregate cash flows arising from obtaining or losing control of subsidiaries or other businesses should be presented separately and classified as investing activities.

Where the impact of acquiring or disposing of a subsidiary or business is material, we expect the notes to provide a breakdown of the impact on the cash flow statement.

We expect companies to carefully consider the nature of cash flows occurring at the point of acquisition, such as settlement of the acquiree's debt and working capital movements. In addition, key accounting judgements should be disclosed; for example, determining if amounts paid relate to consideration or are a separate transaction.

Examples of better disclosures included:

- References to notes which agreed to the amounts presented in the cash flow statement; and

- A breakdown of the cash flows resulting from the acquisition or disposal of subsidiaries and other businesses.

Examples of better disclosure...

Disposals and closures

G4S PLC, Annual Report and Accounts 2019, p194

Deferred or contingent consideration

IAS 7 does not contain detailed guidance on the classification of deferred and contingent consideration and cash flows may be presented under different activities in the cash flow statement. For example:

- movements in contingent consideration may be presented as operating cash flows, with the initial estimate being shown as investing;

- both deferred and contingent consideration could have an implicit financing element, depending on the nature of the transaction; or

- contingent consideration that was deemed to be post-acquisition remuneration, should be presented as an operating cash flow.

As such, where amounts are material, we expect companies to disclose the accounting policy they have applied.

Examples of better disclosures included:

- An explanation of the accounting policy applied for the cash flow statement presentation of deferred or contingent consideration; and

- A breakdown of the amounts shown within each section of the cash flow statement.

Examples of better disclosure...

"Acquisition-related arrangements

The cash payments are reflected in the cash flow statement partly in operating cash flows and partly within investing activities. The tax relief on these payments is reflected in the Group's Adjusting items as part of the tax charge. The part of each payment relating to the original estimate of the fair value of the contingent consideration on the acquisition of the Shionogi-ViiV Healthcare joint venture in 2012 of £659 million is reported within investing activities in the cash flow statement and the part of each payment relating to the increase in the liability since the acquisition is reported within operating cash flows."

GSK PLC, Annual Report 2019, p52

Cash flows from financing activities

Paragraph 17 of IAS 7 provides examples of cash flows from financing activities including: proceeds from issuing shares; cash payments to owners to redeem shares; and proceeds and repayment of loans and cash payments in relation to the outstanding liability relating to a lease.

Paragraph 44A of IAS 7 requires disclosures that enable users to evaluate changes in liabilities arising from financing activities, including both changes arising from cash flows and non-cash changes.

While the standard is not prescriptive, the most common way of meeting the requirements of paragraph 44A is to present a reconciliation.

The area where we identified most potential issues was in the disclosure of changes in liabilities arising from financing activities; for example, some incorrectly included derivative assets which were not hedging risks relating to borrowings, and so should not have been presented as part of liabilities from financing activities. In addition, while companies can include cash and cash equivalents to present a 'net debt' reconciliation, care should be taken to ensure the requirements of IAS 7 are met, for example, by providing a subtotal of liabilities arising from financing activities.

In several cases, we found inconsistencies between amounts presented in the cash flow statement and the disclosure of changes in liabilities arising from financing activities.

The topics on which we wrote to companies in our sample included:

- ⚠️ Settlement of liabilities shown as a cash flow in the disclosure of changes in liabilities arising from financing activities, but which was not included in the cash flow statement;

- ⚠️ Settlement of financing liabilities in the cash flow statement appeared inconsistent with movements in the statement of financial position and notes; and

- ⚠️ Non-cash amounts, such as assets purchased under finance leases and non-cash finance charges, incorrectly presented as cash flows.

Disclosure of accounting policies and significant judgements

Paragraph 117 of IAS 1 requires disclosure of significant accounting policies.

Paragraph 122 of IAS 1 requires disclosure of judgements, apart from those involving estimations that management has made in the process of applying the entity's accounting policies and that have the most significant effect on the amounts recognised in the financial statements.

We have recently reported evidence of some improvement in the reporting of significant judgements5. However, we continue to be surprised by the lack of disclosure of cash flow related judgements, even where it is clear that such judgements have been made.

💡 Given IAS 7 does not contain detailed guidance on many types of transactions, we believe judgement will often be required, given the range, complexity and size of transactions companies undertake.

Most companies in our sample did not provide accounting policies for the cash flow statement.

However, we were pleased to find some better examples of accounting policies in relation to the cash flow statement. Examples of better disclosures of accounting policies in relation to the cash flow statement and which include:

- a description of where contingent consideration is presented within the cash flow statement;

- an explanation of where cash flows from supplier financing arrangements are presented within the cash flow statement; and

- an explanation of where cash flows from leases are presented.

Examples of better disclosure...

"Cash and cash equivalents Lease payments are presented as follows in the Group statement of cash flows:

- short-term lease payments, payments for leases of low-value assets and variable lease payments that are not included in the measurement of the lease liabilities are presented within cash flows from operating activities;

- payments for the interest element of recognised lease liabilities are included in 'interest paid' within cash flows from operating activities; and

- payments for the principal element of recognised lease liabilities are presented within cash flows from financing activities.”

Intercontinental Hotels Group plc, Annual Report and Form 20-F 2019, p141

We will continue to challenge companies where we believe significant judgements have been made in the presentation of the cash flow statement but are not disclosed. In some cases, the treatment in the cash flow statement may be the result of another accounting judgement, for example, whether a sale and leaseback transaction contains a financing element, or the application of hedge accounting. In these cases, we expect companies to explain the impact on the cash flow statement and link the cash flow presentation to the underlying accounting judgement.

Other selected topics

Our routine reviews have highlighted additional areas of cashflow reporting to which companies should pay close attention.

Foreign currency cash flows

IAS 7 requires that cash flows denominated in a foreign currency are reported in a manner consistent with IAS 21. The effect of exchange rate changes on cash and cash equivalents is presented in order to reconcile the movements in cash and cash equivalents during the year.

We know from routine revies that the treatment of foreign currency cash flows can be complex and prone to errors, although we did not find any such errors in our sample.

We expect companies to consider the presentation of foreign currency cash flows in their pre-issuance review of the financial statements. Where our enquiries have led to errors being identified elsewhere in their cash flow statement, corresponding errors, or balancing figures, have often also been identified within foreign currency.

Hedge accounting

The guidance in IAS 7 and IFRS 9 states that cash flows arising from a hedging instrument are classified as operating, investing or financing activities, on the basis of the classification of the cash flows arising from the hedged item.

The disclosures in paragraph 44A of IAS 7 on changes in liabilities arising from financing activities, also apply to financial assets which hedge liabilities arising from financing activities.

Discontinued operations

Paragraph 33(c) of IFRS 5 requires disclosure of the net cash flows attributable to the operating, investing and financing activities of discontinued operations. These disclosures may be presented either in the notes or in the financial statements.

Companies have flexibility in how cash flows from discontinued operations are presented and we see a range of acceptable approaches from our routine reviews, including:

- presenting cash flows from discontinued operations by category in the notes to the financial statements;

- presenting cash flows from discontinued operations by category on the face of the cash flow statement; and

- presenting cash flows from discontinued operations as a separate column within the cash flow statement.

Disclosure of material non-cash transactions

Paragraph 43 of IAS 7 requires that investing and financing transactions that do not require the use of cash or cash equivalents shall be excluded from a statement of cash flows. The standard also requires that such transactions shall be disclosed elsewhere in the financial statements in a way that provides all the relevant information about these investing and financing activities

The standard gives examples of non-cash transactions which include acquiring assets through leases, acquisitions of an entity by an equity issuance and conversion of debt to equity.

Examples of better disclosure...

Non-cash investing and financing transactions

| 2020 £'000 | 2019 £'000 | |

|---|---|---|

| Acquisition of property, plant and equipment by means of a lease | 3,500 | 4,000 |

| Acquisition of subsidiary by issue of ordinary shares | 26,000 | - |

| Settlement of borrowings by issue of ordinary shares | 18,000 | - |

Illustrative example created for the purpose of this thematic

Strategic report

Operating and financial review

The Companies Act 2006, s414C6 and s414CB6 require the strategic report to explain the company's business model (which means how the company generates and preserves value), the company's year end position, and how it has developed and performed during the year. The business review should, therefore, include both information on historical performance and forward looking information explaining the company's strategy and business model.

All companies in our sample provided a summary of IFRS cash flows, adjusted cash flows and liquidity in the strategic report. However, the quality of disclosures varied. Better examples presented concise information in clearly labelled sections. Most companies presented an analysis of both IFRS cash flows and alternative performance measures (APMs).

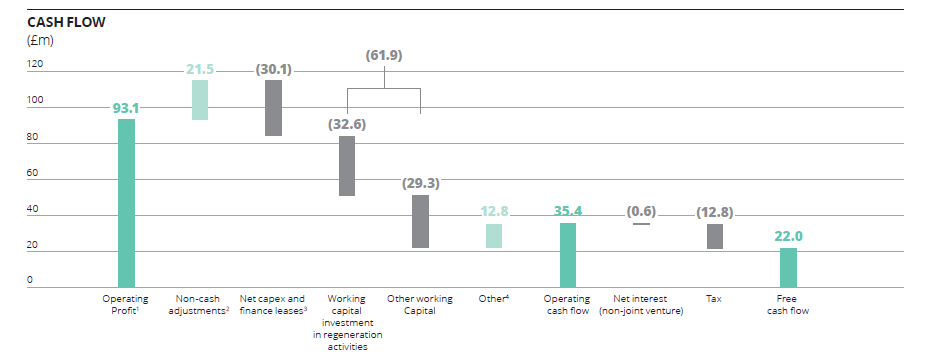

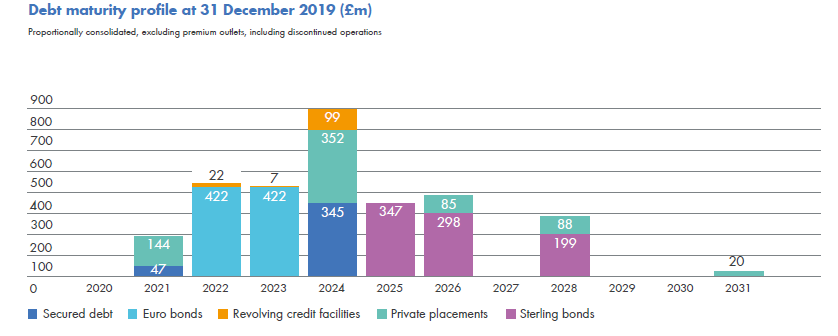

Most companies made good use of tables to present summaries of key information and reconciliations in a clear and easy to read manner. In addition, several companies used graphs to visually explain movements in net debt or debt maturity profiles.

As a result of the impact of Covid-19, many of the companies in our sample provided additional information about their liquidity position, including available liquidity, and provided an update at the time the report was published. We also noticed an increase in disclosures about events which happened after the balance sheet date, such as subsequent funding or financing transactions.

💡 Terms such as 'available liquidity' should be explained to allow users to understand how it relates to amounts presented in the financial statements, even if the meaning is readily apparent.

💡 Disclosures should clearly distinguish between discussions of the company's liquidity position at the balance sheet date and the date the financial statements were signed.

Examples of better disclosures included:

- Summary cash flow statement information, including year end cash and net debt positions, supported by explanation of the cash flows by operating, investing and financing activities;

- Explanation of movements in cash, net debt or debt maturity profiles;

- Description of available liquidity resources, including composition of cash and cash equivalents and undrawn borrowing facilities;

- Details of debt and borrowing facilities including financial covenants;

- Disclosure of other relevant obligations such as off balance sheet arrangements, supply chain financing, pension commitments and contingent liabilities; and

- Narrative explanation of cash and liquidity based APMs such as free cash flow, cash conversion, net debt and leverage.

Operating and financial review

Examples of better disclosure...

Debt maturity profile at 31 December 2019 (£m)

Proportionally consolidated, excluding premium outlets, including discontinued operations

Hammerson plc, Annual Report and Accounts 2020, p57

Use of APMs and KPIs

Alternative performance measures (APMs) have been a focus of our work in recent years and were the subject of a previous thematic review published in 2017. While the principles around reporting APMs set out in that review remain relevant, we issued additional guidance in May 20207 in response to the challenges of the pandemic.

Alternative performance measures

As part of our review, we considered compliance with the ESMA guidelines8 with particular emphasis on the clarity of labels and definitions and clear reconciliations to measures presented in the financial statements. We considered what constituted a cash flow or liquidity based APM, and compared APMs with similar titles and definitions.

APMs were used throughout strategic reports and we observed different approaches to locating information required to comply with the ESMA guidelines such as definitions and reconciliations. The majority of companies provided an appendix with the definitions of all APMs.

All companies in our sample provided between two and eight cash flow or liquidity based APMs. While all companies presented some measure of net debt or net cash, some companies used it predominantly as an input into another APM such as 'net debt to EBITDA9' ratio.

After net debt, the most common APMs were 'net debt to EBITDA' (leverage) ratio, 'free cash flow' and 'cash conversion ratio'. Other APMs used included measures of adjusted operating cash flow and measures relating to capital expenditure and working capital.

Key performance indicators ('KPIs')

By comparison, most companies had only one or two cash flow or liquidity KPIs, although 23% of the sample had no such KPIs. We found this surprising given the importance of cash and liquidity to companies' performance. The most common KPIs were net debt and free cash flow followed by cash conversion ratio and net debt to EBITDA ratio.

No. of APMs / KPIs per company

Bar chart showing number of companies against number of measures (0 to 8) for APMs and KPIs.

Most common APMs & KPIs

Stacked bar chart showing number of companies against various APMs/KPIs (Net debt, Net debt/EBITDA, Free cash flow, Cash conversion ratio, Adjusted operating cash flow, Net capex, Gross capex).

Use of APMs and KPIs

We expect companies to present APM disclosures that:

- have clear and accurate labelling;

- have an explanation of their relevance and use;

- are reconciled to the closest IFRS measure; and

- are not given more prominence than the equivalent IFRS measures.

In line with the findings of our routine reviews, we found that most companies complied with the ESMA guidelines and met the expectations set out in our previous thematic.

Examples of better disclosures included:

- explanation of why variants of certain measures were used, for example, where one measure of leverage is used by management and another measure is used for covenant testing;

- providing a comprehensive section on APM disclosures detailing definitions, explanations and reconciliations where multiple APMs are used; and

- disclosure of the closest equivalent statutory measure for each APM presented.

We did, however, identify a few instances where there was room for improvement:

- ⚠️ In two cases, companies presented multiple versions of net debt (for example, 'net debt' and 'adjusted net debt') without explaining why multiple measures were necessary. In addition, the definitions and labels did not clearly distinguish between the separate measures of net debt, with the consequence that it was not clear as to which measure the commentary was referring; and

- ⚠️ One company presented an APM (comprising adjusted operating cash flows) with a label that could be confused with an IFRS measure.

Examples of better disclosure...

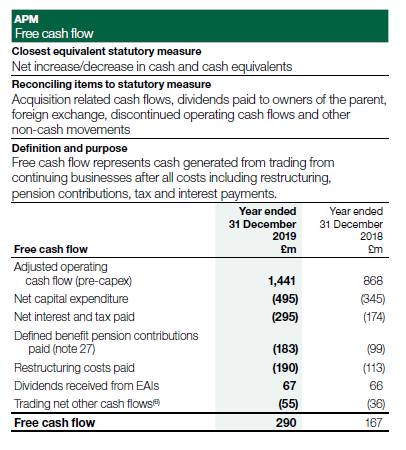

APM Free cash flow

Closest equivalent statutory measure Net increase/decrease in cash and cash equivalents

Reconciling items to statutory measure Acquisition related cash flows, dividends paid to owners of the parent, foreign exchange, discontinued operating cash flows and other non-cash movements

Definition and purpose Free cash flow represents cash generated from trading from continuing businesses after all costs including restructuring, pension contributions, tax and interest payments.

Melrose Industries PLC, Annual Report 2019, p194

Principal risks and uncertainties (PRUs)

Liquidity or funding risk was identified as a principal risk and uncertainty for 23% of the companies in our sample. These risks included management of working capital and the availability of cash or borrowing facilities. A further 13% of companies disclosed other treasury risks indirectly related to liquidity and cash flow, such as potential cash requirements from pension commitments or exposure to currency or other financial risks.

Unsurprisingly, many companies that published their annual report and accounts from April onwards, identified Covid-19 as either a principal risk or as a significant emerging risk which developed after the balance sheet date. Where Covid-19 was identified as a principal risk, the impact on cash flows and liquidity was included as part of this risk.

The remaining 34% of companies did not identify any risks relating to cash flows or liquidity. However, this does include companies which published their annual reports and accounts before March, when the impact of Covid-19 was not generally considered to be a major risk.

💡 We expect all companies to reassess their disclosure of principal risks and uncertainties in future reporting periods to ensure that liquidity risks are appropriately considered.

Examples of better disclosures included:

- Entity-specific risks and changes to those risks both during the year and anticipated to arise in the future;

- A description of mitigating factors and actions taken; and

- Links to strategy, business model and KPIs.

Going concern

Paragraphs 25 and 26 of IAS 1 require the directors to make an assessment of the company's ability to continue to operate as a going concern for at least 12 months from the balance sheet date. As part of this assessment, the directors must consider whether there are any material uncertainties that may cast significant doubt on the ability of the company to continue to operate as a going concern. Where these uncertainties exist, they must be disclosed.

Determining whether or not a material uncertainty exists is considerably more difficult given the uncertain economic climate as a result of Covid-19. Management may have exercised significant judgement in reaching the conclusion that no material uncertainties exist, in which case, disclosure of that significant judgement is required in accordance with paragraph 122 of IAS 1.

The Financial Reporting Lab report: 'Covid-19 - Going concern, risk and viability[^10]' provides useful guidance on the information that could be included within going concern disclosures, and the factors that boards may need to consider in making their going concern assessment. The Covid-19 Thematic Review[^10] also provides further guidance and examples of better disclosures.

Most of the companies in our sample that published accounts before March provided boiler plate going concern disclosures. There was, however, a marked improvement in disclosure made by those companies that published accounts later in the year. Of these companies, most included helpful, company-specific going concern disclosures within their financial statements. However, the level of detail presented varied with some companies providing high level going concern disclosures, which would have been improved by further detail of the underlying assumptions supporting the assessment.

Our findings were consistent with the findings of the Covid-19 Thematic which observed that the most helpful going concern disclosures had the following characteristics:

- Clear explanation of any material uncertainties that may cast doubt on the company's going concern status;

- Explanation of the different going concern scenarios that had been considered, such as the impact of Covid-19;

- Indication of which inputs were subjected to stress tests and explanation of how these stress tests affected the going concern conclusions; and

- Explanation of whether the company would need to make structural changes in order to continue to operate as a going concern.

In addition, we also found helpful examples which:

- Explained the company's exposure to vulnerable sectors, countries and key suppliers;

- Described the assumptions which were considered before the impact of Covid-19 were known;

- Provided outputs of reverse stress tests and commented on the likelihood of such scenarios; and

- Described the governance process taken by the board to challenge the assessment made.

Viability statements

Unlike going concern, the viability statement is designed to provide information to stakeholders about the longer term economic and financial viability of the company. Consequently, the viability statement requires a longer term assessment of a company's ability to meet its liabilities as they fall due, although there is an element of overlap.

The Financial Reporting Lab report: 'Covid-19 - Going concern, risk and viability' provides useful guidance on the information that could be included within the viability statement and the factors that boards may need to consider in determining whether the group is viable over the longer term. The Covid-19 Thematic Review also provides further guidance and examples of better disclosures.

As a result of the economic uncertainty caused by Covid-19, high quality viability disclosures are critical to enable users of accounts to understand how a company intends to deal with the challenges posed by the pandemic.

💡 Given the current uncertain environment, it is even more important that the viability statement sets out clearly the company's specific circumstances, and the degree of uncertainty about the future. In particular, the board should draw attention to any qualifications or assumptions made in determining the company's viability.

We continue to observe that the better viability disclosures included:

- Identification of areas which were particularly subject to uncertainty and how that uncertainty may be mitigated;

- Explanation of the viability scenarios that had been prepared, including a description of key assumptions within each scenario and how they impacted the viability conclusion;

- Indication of which inputs had been subject to stress testing and reverse stress testing and explanation of how this impacted the viability assessment;

- Explanation of the impact of post balance sheet events such as the arrangement of new lending facilities, extension of existing facilities and renegotiation or waiver of bank covenants; and

- Linkage to relevant information included in other areas of the annual report.

Many of the companies in our sample failed to present clear details of the assumptions that underpinned their viability assessment. In addition, while some companies referred to the use of stress testing in assessing viability, very few companies provided details of stress testing or reverse stress testing performed.

In particular we identified that:

- ⚠️ One company in our sample planned to raise further funds after the reporting date, but it was not clear how this had been treated for the purpose of the scenarios considered.

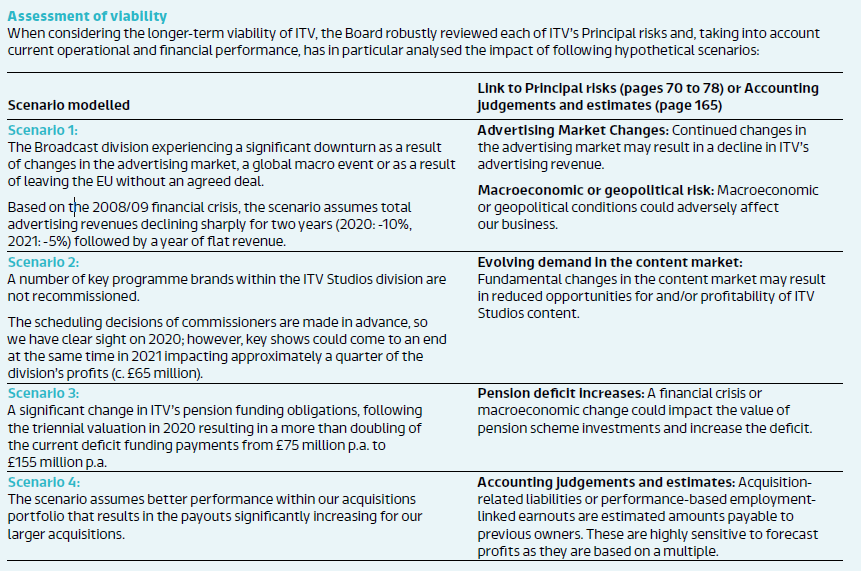

Clear linkage provided to other areas of the annual report including accounting judgement and estimates.

Examples of better disclosure...

Assessment of viability When considering the longer-term viability of ITV, the Board robustly reviewed each of ITV's Principal risks and, taking into account current operational and financial performance, has in particular analysed the impact of following hypothetical scenarios:

ITV Plc, Annual Report 2019, p79

IFRS 7 liquidity risk disclosures

Qualitative disclosures

IFRS 7 requires quantitative and qualitative disclosures of the exposure to liquidity risk and how it arises, as well as disclosure of the company's objectives, policies and processes for managing the risk, and the methods used to measure it. IFRS 7 permits these disclosures to be incorporated by reference from the financial statements and presented elsewhere in the report and accounts.

Many companies in our sample provided relatively brief qualitative disclosures of liquidity risk in the financial risk management notes, with more detailed information provided elsewhere (such as details of liquidity risk presented in the going concern disclosures, viability statement and governance and liquidity policies included in the strategic report).

💡 The Group needs to ensure that it has sufficient liquid funds available to support its working capital and capital expenditure requirements. All subsidiaries submit weekly and bi-monthly cash forecasts to the treasury function to enable them to monitor the Group's requirements.

Better disclosures contained:

- entity-specific policies on managing liquidity risk;

- details of liquid resources and uncommitted facilities;

- references to liquidity information contained in other notes; and

- information about any changes to liquidity risk management.

Maturity analysis

IFRS 7 requires a maturity analysis of all financial liabilities to be provided (including leases and issued financial guarantees). The maturity analysis should include undiscounted, contractual cash flows, including principal and interest payments. The time bands disclosed need to be consistent with the information provided internally to key management personnel.

Liquidity risk disclosures will continue to be a key area of interest for investors given the uncertainty in the current economic environment. While all companies in our sample provided a maturity analysis, the quality varied.

💡 While the appropriate level of disaggregation of time bands may differ between companies, we expect companies to consider whether a greater degree of disaggregation than reported previously is required in the current circumstances.

💡 Companies should consider if it is clearer to present liquidity information together in one location rather than in separate maturity tables.

Examples of better disclosures in our sample included:

- clear explanation of what the maturity analysis represented;

- information presented in a way which could be easily compared to items in the statement of financial position (for example, showing the carrying value next to the total of undiscounted contractual cash flows);

- all relevant liabilities, including lease liabilities, presented together for easy analysis; and

- sufficient granularity in the time bands chosen.

Areas identified as warranting improvement included:

- ⚠️ some companies in our sample failed to clearly distinguish the maturity analysis presented on an undiscounted basis from that presented on a discounted basis, for example, by having the same titles for both;

- ⚠️ several companies excluded contractual interest cash flows from the contractual undiscounted cash flows; and

- ⚠️ several companies presented the maturity disclosures in separate notes, which made it hard to understand the aggregate position.

Maturity analysis

Examples of better disclosure...

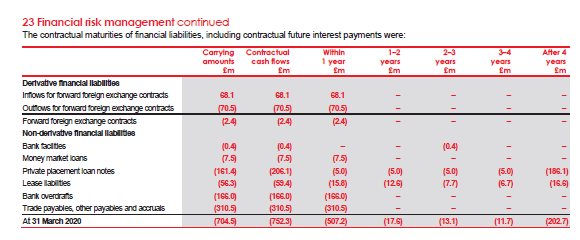

23 Financial risk management continued

The contractual maturities of financial liabilities, including contractual future interest payments were:

Electrocomponents plc, Annual Report and Accounts 2020, p143

Compliance with banking covenants

In our Covid-19 Thematic Review we stated that, in the current environment, we expect companies to disclose details of their banking covenants, even when they have complied with the terms of the arrangements and there is significant headroom. Any judgements made in assessing compliance with covenants should also be explained.

We were pleased to see that the majority of companies that published the annual report and accounts after March provided information regarding their compliance with the terms of covenants and waivers agreed with their debt providers.

Where a company had multiple covenants, or covenant levels changing over time we found tabular disclosures to be helpful.

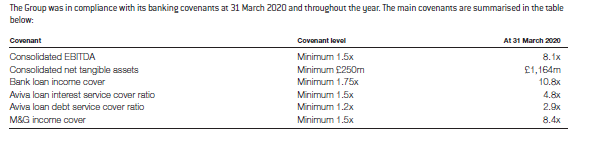

Examples of better disclosure...

The Group was in compliance with its banking covenants at 31 March 2020 and throughout the year. The main covenants are summarised in the table below:

Big Yellow Plc, Annual report 2019/20, p143

Compliance with banking covenants

In our Covid-19 Thematic Review we identified that better disclosures explained:

- how calculated covenant ratios compare with the requirements of lending arrangements;

- the available headroom;

- whether the adoption of IFRS 16 had any impact on covenants;

- any waivers agreed with debt providers; and

- any changes post year-end as a result of further measures taken (for example, equity raise).

This review also identified that the better disclosures explained:

- the impact on covenants of new borrowing facilities and government support;

- how often covenants are tested;

- how covenant levels will change over time; and

- any restrictions on the company such as over shareholder distributions or acquisitions.

Examples of better disclosure...

"Mitie's two key covenant ratios are calculated on a pre-IFRS 16 basis. These are the leverage (ratio of consolidated total net borrowings to consolidated EBITDA to be no more than three times) and interest cover covenant (ratio of consolidated EBITDA to net finance costs to be no less than four times).”

MITIE Plc, Annual report and accounts 2020*, p43

Seasonality

Paragraph 35 of IFRS 7 states that if the quantitative data disclosed as at the end of the reporting period are unrepresentative of an entity's exposure to risk during the period, an entity shall provide further information that is representative.

In addition to disclosure of the exposure to liquidity risk at the reporting date, several companies in our sample provided additional disclosures of the exposure during the year. Examples of better disclosures included:

- disclosure of the maximum drawdown of revolving credit facilities during the year;

- explanation of the impact of seasonality on liquidity and working capital in comparison to seasonality in the business operations; and

- use of metrics which considered average exposures in the report period (such as average daily net cash) in addition to the position at the reporting date.

Working capital and supplier financing arrangements

Companies are reminded that supply chain financing arrangements, including reverse factoring transactions, are currently an area of focus for the FRC.

We note that the IASB's Interpretations Committee recently considered the principles and requirements in IFRS Standards relating to reverse factoring. While a final decision has yet to be reached, the Committee noted that companies should not gross up the cash flow statement, unless the arrangement involves cash inflow and outflow for the entity when an invoice is settled by the financing transaction.

Companies also need to determine whether to derecognise the supplier payable and recognise a liability to the finance provider, and what additional disclosures about exposures to risk from financial instruments, significant judgements and material effects are required.

Where companies are using material supplier financing arrangements, we expect disclosure of:

- the amount of the facility and usage;

- the accounting policy applied, including the basis on which the company recognised the liability to suppliers;

- whether the liability is included within the determination of key performance indicators such as net debt;

- the cash flows generated by such arrangements; and

- the impact on liquidity risk which could arise from losing access to the facility, for example, acceleration of payments to suppliers leading to demands on cash and working capital.

Findings from our thematic

Three companies in our sample disclosed material supplier financing arrangements. In addition, a further four companies disclosed immaterial arrangements, or stated explicitly that no supplier financing arrangements were used.

Examples of better disclosures included:

- a description of the supplier financing arrangements used including the purpose of the arrangement;

- how amounts relating to the arrangement are presented in the balance sheet and cash flow statement;

- details of interest or fees payable;

- the impact on the timing of the company's cash flows; and

- how liquidity risk is managed in relation to the risk of losing access to the facility.

* Morrisons was not part of the sample for this thematic review but was identified as an example of better disclosure by Moody's in their letter to the IFRS Interpretations Committee on supply chain financing: https://cdn.ifrs.org/-/media/feature/meetings/2020/april/ifric/ap03-supply-chain-financing.pdf

4. Next steps

Engagement with companies

We are writing letters to three companies included in our sample where there is a substantive question relating to the cash flow statement, and to a further five companies drawing their attention to aspects of their disclosures which could be improved.

Impact on our future reviews

We will continue to challenge companies during our routine reviews when we do not see:

- Clear explanation of going concern, viability and liquidity information, such as availability of cash, undrawn borrowing facilities and compliance with covenants

- Disclosure of assumptions and judgements made in assessing going concern and viability

- Disclosure of supplier financing arrangements, including the impact on liquidity risk management

- Evidence of robust pre-issuance reviews to ensure cash flow statements and related notes are compliant with the requirements of IAS 7 and free from basic errors

- Consistency between the amounts and descriptions of items in the cash flow statement, and other areas of the annual report including: the strategic report, other primary statements, disclosures of changes in financing liabilities and other notes

- Disclosure of any judgements in relation to the cash flow statement, particularly for large, one-off transactions, and disclosure of related accounting policies, such as for the composition of cash and cash equivalents, the presentation of interest and contingent consideration

Appendix

Summary of historical cash flow statement errors where corrective action was required

We summarise below the matters where companies were required to take corrective action by restating the cash flow statement as a result of CRR enquiries. We encourage companies to consider these matters as they provide an indication of the types of issues companies should look for, and correct, when performing their pre-issuance reviews.

Cash flow statement errors requiring restatement following CRR review, relating to reclassifications, included:

| Error | Impact of correction on... | ||

|---|---|---|---|

| Operating | Investing | Financing | |

| :---------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------- | :-----------: | :----------: | :----------: |

| Payments of purchase consideration for subsidiary undertakings conditional on the continuing employment of the vendors in the business incorrectly classified as investing cash flows rather than operating cash flows | ↓ | ↓ | |

| Payments for the purchase of businesses incorrectly classified as operating activities rather than investing activities | ↓ | ||

| Company presented cash outflows on its investment in legal cases and the purchase of property for resale, relating to a case settlement, within investing activities. However, the cash inflow upon settlement of cases was presented within operating activities. Both types of cash outflow should have been presented within operating activities because they arose in respect of the company's principal revenue-producing activities | ↓ | ↑ | |

| Post-acquisition and restructuring cost cash flows included within investing activities rather than operating activities | ↓ | ↑ | |

| Cash flows relating to joint venture funding incorrectly classified as financing rather than investing activities | ↓ | ↑ | ↑ |

| Advances to joint ventures were presented as operating cash flows rather than investing activities | ↑ | ↓ | |

| Acquisition-related expenses recognised in the income statement incorrectly classified as investing activities rather than operating activities | ↓ | ↑ | |

| Company classified promissory notes as debt, but movements in the balance classified as operating, rather than financing, cash flows | ↑ | ↓ | |

| Restructuring cash outflow incorrectly classified as investing activities rather than operating activities | ↓ | ↑ | |

| Incorrect classification of movements in certain restricted cash balances, which were included in financing activities rather than in investing activities | ↓ | ↑ |

Appendix (2)

Summary of historical cash flow statement errors where corrective action was required (cont.)

Cash flow statement errors requiring restatement following CRR review, which did not relate to reclassifications, included:

- Non-cash movement relating to the unwind of a discount incorrectly included in the cash flow statement

- Company had presented assets purchased under finance leases as a cash flow

- Cash flow statement was restated due to a number of errors: an unpaid liability was treated as a cash outflow, acquisition-related expenses were classified as investing cash flows rather than as operating cashflows and amounts on the settlement of a derivative was omitted from the cash flow statement.

- Cash flows on loans payable had been incorrectly netted and classified as operating activities rather than financing activities.

Appendix (3)

Consistency checks

The consistency checks performed by our reviewers compare:

- Items in the reconciliation to net cash from operating activities to profit and loss and the notes, for example: depreciation, amortisation, impairments and disposal gains;

- Cash flows from working capital movements to changes in the balance sheet and notes;

- Purchases and proceeds of property, plant and equipment and intangibles to the related notes;

- Cash flows from acquisition and disposal of businesses to the notes;

- Cash flows from transactions with shareholders to movements in the statement of changes in equity; and

- Proceeds and repayment of borrowings to the disclosures of changes in liabilities from financing activities.

While not all figures in the cash flow statement can be agreed to another primary statement or the notes to the accounts, and there may be valid reasons for differences, we still find such consistency checks useful in identifying potential errors.

Financial Reporting Council

Information about the Financial Reporting Council can be found at: https://www.frc.org.uk

Follow us on Twitter @FRCnews or Linked in

Our purpose

The FRC's purpose is to serve the public interest by setting high standards of corporate governance, reporting and audit, and by holding to account those responsible for delivering them.

The FRC does not accept any liability to any party for loss, damage or costs however arising, whether directly or indirectly, whether in contract, tort or otherwise from any action or decision taken (or not taken) as a result of any person relying on or otherwise using this document or arising from any omission from it.

© The Financial Reporting Council Limited 2020 The Financial Reporting Council Limited is a company limited by guarantee. Registered in England number 2486368.

FINANCIAL REPORTING COUNCIL 8TH FLOOR 125 LONDON WALL LONDON EC2Y 5AS

+44 (0)20 7492 2300

www.frc.org.uk

-

https://www.frc.org.uk/accountants/corporate-reporting-review/annual-activity-reports ↩↩

-

https://www.frc.org.uk/investors/financial-reporting-lab ↩

-

Paragraph AG3 of IAS 32 sates that 'Currency (cash) is a financial asset because it represents the medium of exchange and is therefore the basis on which all transactions are measured and recognised in financial statements'. ↩

-

https://www.ifrs.org/news-and-events/updates/ifric-updates/march-2018/ ↩

-

Whether either of these sections applies will depend on whether company meets the qualifying conditions as set out in the Companies Act. A helpful summary of these qualifying conditions is set out in the FRC's Guidance on the Strategic Report, p 7. ↩

-

https://www.frc.org.uk/about-the-frc/covid-19/company-guidance-updated-20may-2020-(covid-19)?viewmode=0 ↩↩

-

https://www.esma.europa.eu/press-news/esma-news/esma-publishes-final-guidelines-alternative-performance-measures ↩

-

EBITDA - earnings before interest depreciation and amortisation ↩

-

https://www.frc.org.uk/covid-19-guidance-and-advice ↩