The content on this page has been converted from PDF to HTML format using an artificial intelligence (AI) tool as part of our ongoing efforts to improve accessibility and usability of our publications. Note:

- No human verification has been conducted of the converted content.

- While we strive for accuracy errors or omissions may exist.

- This content is provided for informational purposes only and should not be relied upon as a definitive or authoritative source.

- For the official and verified version of the publication, refer to the original PDF document.

If you identify any inaccuracies or have concerns about the content, please contact us at [email protected].

FRC Key Facts and Trends in the Accountancy Profession (August 2022)

The Financial Reporting Council (FRC) serves the public interest by setting high standards of corporate governance, reporting and audit, and by holding to account those responsible for delivering them.

The FRC sets the UK Corporate Governance and Stewardship Codes and UK standards for accounting and actuarial work; monitors and acts to promote the quality of corporate reporting; and operates independent enforcement arrangements for accountants and actuaries. As the Competent Authority for audit in the UK, the FRC sets auditing and ethical standards and monitors and enforces audit quality. Our work is aimed at investors and others who rely on company reports, audit and high-quality risk management. The FRC is a transparent organisation that consults openly and reports to Parliament.

The content in this publication is provided for general information purposes only. Although the FRC endeavours to ensure the accuracy of the information provided by the accountancy firms and bodies in preparing this publication, the FRC has not performed a detailed review of information supplied. Accordingly, the FRC accepts no responsibility for any reliance others may place upon the information herein and it shall not be liable for any loss or damage arising from the use of the information contained within this publication nor from any action or decision taken as a result of using such information.

The FRC does not accept any liability to any party for any loss, damage or costs howsoever arising, whether directly or indirectly, whether in contract, tort or otherwise from any action or decision taken (or not taken) as a result of any person relying on or otherwise using this document or arising from any omission from it.

The Financial Reporting Council Limited 2022

The Financial Reporting Council Limited is a company limited by guarantee. Registered in England number

- Registered Office: 8th Floor, 125 London Wall, London, EC2Y 5AS

- Foreword

- Section One – Main Highlights

- Section Two – Members and students of the Accountancy Bodies

- Registered members and students in the UK and ROI

- Registered members and students worldwide

- Analysis of members and students of the seven Accountancy Bodies

- Students who became members

- Sectoral employment of members and students worldwide

- Female members and students worldwide

- Age of members and students worldwide

- Footnotes

- Figure 7: Age of members worldwide, 2017 and 2021

- Figure 8: Age of Students Worldwide, 2017 and 2021

- Diversity information on members and students

- Location of students

- Profile of students of the Accountancy Bodies worldwide

- Graduate entrants to training

- The Association of Accounting Technicians (AAT)

- Section Three – Resource Information on the Accountancy Bodies

- Resource income of the seven accountancy bodies

- Figure 16: Total income worldwide, 2017 to 2021

- Average income per body from members and students

- Figure 17: Average income per members and students worldwide, 2017 to 2021

- Breakdown of income

- Figure 18: Breakdown of income, 2021

- Staffing of the Accountancy Bodies

- Figure 19: Staffing, 2017 to 2021, FTEs

- Diversity information on the workforce under the Equality Act 2010

- Figure 20: Diversity information on the workforce, 2021

- Section Four – Oversight of audit regulation

- Recognised Supervisory Bodies (RSBs)

- Number of firms registered with the RSBs

- Figure 21: Total registered firms by number of principals, 2019 to 2021

- Statutory audit firms

- Figure 22: Firm registrations, 2019 to 2021

- Monitoring of registered audit firms by the FRC's Audit Quality Review team

- Monitoring of registered audit firms by the RSBs

- Complaints about auditors

- Recognised Qualifying Bodies (RQBs)

- Approved training offices

- 5. Audit firms

- Growth of fee income

- Audit fee income per Responsible Individual (RI)

- Concentration of listed company audits

- Diversity of senior management at PIE audit firms

- Age of the workforce at PIE audit firms

- Diversity information collected by the PIE audit firms (workforce)

- Section Six – Data tables of the charts

- Section Seven – Glossary

Foreword

This is the twentieth edition of Key Facts and Trends in the Accountancy Profession.

This publication provides statistical information and trends on the members and students in the accountancy profession. Information is obtained from the following accountancy bodies: the six UK Chartered Accountancy bodies, 1 the Association of International Accountants (AIA) ('the accountancy bodies') and the Association of Accounting Technicians (AAT) ('all bodies'). In the sections below, the tables on members show data for the UK and the Republic of Ireland (ROI) combined and worldwide data. We include the UK and ROI figures together, partly because members and firms are entitled to practise in both jurisdictions and partly because in some cases it is difficult for all bodies to separate the data. However, it should be noted that in the case of audit, practising rights in Ireland are subject to discreet obligations which mean only a limited number of firms and members are able to practise in both jurisdictions. The Irish Auditing and Accounting Supervisory Authority (IAASA) publishes information relating specifically to the ROI accountancy bodies, which can be found at http://www.iaasa.ie.

Where appropriate we highlight significant trends and explain possible limitations of the data; however, it is important to note that we do not check the accuracy of the information provided. Where there are notable trends in the data, we follow this up with all bodies and firms to verify that they are content with the information they provided, but we do not include commentary on the possible reasons for any particular trends. We stress that it is often difficult to make comparisons between the different accountancy bodies, or between the audit firms that audit public interest entities (PIEs), 2 given the differences in the way data is classified by those bodies and firms and because of different regulatory arrangements in the UK, ROI and rest of the world.

In this edition, 25 firms with PIE clients (out of 43) participated compared with 26 firms in last year's publication. Competition between the Big Four audit firms and the Challenger firms remains a major focus. This year, the five largest firms 3 outside the Big Four audited 23 FTSE 350 companies; this compares with 19 last year and 10 the year before.

As well as the competitiveness and resilience of the UK audit market, diversity at all bodies and audit firms continues to be high on the FRC's agenda. Consistent with the Public Sector Equality Duty (PSED), the FRC must consider the following objectives in its oversight of all bodies:

- Eliminate unlawful discrimination, harassment, victimisation and any other conduct prohibited by the Act;

- Advance equality of opportunity between people who share a protected characteristic 4 and people who do not share it; and

- Foster good relations between people who share protected characteristics and people who do not share it.

In relation to diversity, we asked the PIE audit firms to provide information on the following nine diversity indicators: ethnicity, disability, religion/belief, sexual orientation, marital status, school type attended, first generation to attend university, being from a lower socioeconomic-background, and having caring responsibilities. We also requested data on gender, ethnicity, disability and sexual orientation in respect of senior management at the PIE audit firms.

Further details can be found in the Diversity section of this publication.

As always, we are grateful to those who took the time to complete our questionnaire on how we can continue to improve this publication, viewable here.

Section One – Main Highlights

The Accountancy Bodies 2017 to 2021

Membership of the accountancy bodies continues to grow. The seven bodies in this report have nearly 390,000 members in the UK and ROI, and over 590,000 members worldwide. The growth in membership between 2020 and 2021 was 2.1% in the UK and ROI, and 2.8% worldwide. This is in line with compound annual growth rates from 2017 to 2021 is 2.0% in the UK and ROI, and 2.7% worldwide. (Figures 1 and 2)

There are nearly 162,000 students in the UK and ROI, and over 597,000 worldwide. Between 2020 and 2021, student numbers increased by 0.3% in the UK and ROI, and by 1.6% worldwide. (Figures 1 and 2) This compares with compound annual growth rates from 2017 to 2021 of –0.4% for the UK and ROI and 0.3% worldwide. UK and ROI student numbers fell slightly for ACCA (−1.3%) and CIMA in 2021 (-1.7%) and worldwide student numbers also fell for CIMA (–5.2%). The number of audit firms registered with the Recognised Supervisory Bodies (RSBs) 5 continues to decline. The total number of registered audit firms was 4,745 as at 31 December 2021, falling from 5,007 and 5,127 registered firms as at 31 December 2020 and

-

(Figure 21) Since 2017, there has been a consistent annual increase in the income generated from all members and students worldwide for ICAEW. ACCA continues to generate the highest income of all the bodies at nearly £223m in

-

CAI earns the highest average income from members and students at £682 per individual for 2021. (Figures 16 and 17)

Overall, the accountancy bodies collect data on their members and students concerning six of the nine protected characteristics under the Equality Act 2010; seven bodies collect data on age and sex, six on race, and five on disability, for example. Three of the bodies also collect data on socio-economic background (Figure 9). Figure 20 shows the number of bodies that collect diversity data on their own workforce in respect of the protected characteristics; all nine of the protected characteristics were used by at least one of the bodies to record diversity information on their workforce. All the bodies have diversity policies/statements in place.

The audit firms 2019 to 2021

Figure 33 shows the total fee income, split by audit and non-audit services, for the 25 audit firms with Public Interest Entity (PIE) clients for 2021 year ends, that replied to our survey. Firms are listed in order of fee income from audit, rather than total fee income. All data is provided on a voluntary basis to the FRC. The Big Four firms continued to see an increase in their total fee income of 4.6% in 2021 compared to an increase of 2.7% in the previous year. Firms outside the Big Four have also seen an increase in their total fee income in 2021 of 5.9% compared to an increase of 13.1% in

-

(Figure 36) Audit fee income for the Big Four firms increased by 6.5% in 2021 compared with a 7.9% increase in the previous year. Audit fee income for audit firms outside the Big Four increased by 12.5% in 2021 compared with a 20.9% increase in

-

(Figure 36) Fees for non-audit work to audit clients increased by 10.3% for the Big Four compared to a reduction of 2.2% in

-

In contrast, non-Big Four firms saw a decrease in these fees of 6.8% in 2021 compared to an increase of 6.1% the year before. (Figure 36) The average audit fee income per Statutory Auditor / Responsible Individual (RI) for Big Four firms in 2021 was £2.30m compared to £1.08m for non-Big Four firms. The average for all firms with PIE clients was £1.83m, an increase of £0.15m compared to

-

(Figure 37) In 2020, the five largest firms outside the Big Four audited 7.6% (19) of the FTSE 250 companies; in 2021 they audited 10% (23). Two firms outside these five (and the Big Four), also audited 1.6% (4) of the FTSE 250 companies in 2021 compared with 0.8% (2) in

-

(Figure 39)

With regards to diversity at audit firms, we have focused on senior management at each of the 25 PIE audit firms responding to our survey, highlighting those managers, directors and partners who are female, from black, Asian, and minority ethnic backgrounds, have a disability, or are LGBTQ+. 6 (Figures 40 to 44) We asked the PIE audit firms whether they collect information on a range of diversity indicators for their workforce: age, race, disability, religion/belief, sexual orientation, marital status, school type attended, first generation to attend university, and caring responsibilities. The data and the staff completion rates on each indicator are set out in Figure

- The firms were also asked whether they have a diversity policy in place (Figure 47). This year we also asked whether PIE audit firms collect information on socio-economic background.

Section Two – Members and students of the Accountancy Bodies

Registered members and students in the UK and ROI

Figure 1 shows growth rates for the five years to 31 December 2021, and the number of members and students in the UK and ROI as at 31 December 2021.

Figure 1: Members and students in the UK and ROI Bar chart showing the number of members and students for ACCA, CIMA, CIPFA, ICAEW, CAI, ICAS, and AIA for years 2017 to

- Each body has two bars for each year (Members and Students) showing values between 0 and 140,000.

| Members in the UK & ROI | ACCA | CIMA | CIPFA | ICAEW | CAI | ICAS | AIA | TOTAL |

|---|---|---|---|---|---|---|---|---|

| Total numbers for 2021 | 106,561 | 85,517 | 12,451 | 135,681 | 27,530 | 20,211 | 1,379 | 389,330 |

| % growth (20-21) | 3.2 | 1.2 | 1.3 | 1.8 | 4.1 | -0.1 | 6.0 | 2.1 |

| % growth (17-21) | 12.6 | 3.5 | -1.4 | 7.2 | 15.2 | 9.1 | 6.7 | 8.1 |

| % compound annual growth (17-21) | 3.0 | 0.9 | -0.4 | 1.8 | 3.6 | 2.2 | 1.6 | 2.0 |

| Students in the UK & ROI | ACCA | CIMA | CIPFA | ICAEW | CAI | ICAS | AIA | TOTAL |

|---|---|---|---|---|---|---|---|---|

| Total numbers for 2021 | 75,188 | 47,101 | 2,116 | 25,014 | 7,662 | 4,112 | 144 | 161,337 |

| % growth (20-21) | -1.3 | -1.7 | 0.1 | 7.3 | 4.2 | 7.1 | 3.6 | 0.3 |

| % growth (17-21) | -8.4 | -2.4 | 13.9 | 19.4 | 15.1 | 7.2 | 13.4 | -1.5 |

| % compound annual growth (17-21) | -2.2 | -0.6 | 3.3 | 4.5 | 3.6 | 1.7 | 3.2 | -0.4 |

Registered members and students worldwide

Figure 2 shows growth rates for the five years to 31 December 2021 and the number of worldwide 7 members and students as at 31 December 2021.

Figure 2: Members and students worldwide Bar chart showing the number of members and students worldwide for ACCA, CIMA, CIPFA, ICAEW, CAI, ICAS, and AIA for years 2017 to

- Each body has two bars for each year (Members and Students) showing values between 0 and 450,000.

| Members worldwide | ACCA | CIMA | CIPFA | ICAEW | CAI | ICAS | AIA | TOTAL |

|---|---|---|---|---|---|---|---|---|

| Total numbers for 2021 | 236,827 | 116,302 | 13,991 | 161,411 | 30,622 | 23,252 | 10,061 | 592,466 |

| % growth (20-21) | 3.5 | 1.6 | 5.9 | 2.3 | 3.5 | 0.8 | 5.5 | 2.8 |

| % growth (17-21) | 15.9 | 6.3 | 1.9 | 8.1 | 15.3 | 8.1 | 40.4 | 11.4 |

| % compound annual growth (17-21) | 3.8 | 1.5 | 0.5 | 2.0 | 3.6 | 2.0 | 8.9 | 2.7 |

| Students worldwide | ACCA | CIMA | CIPFA | ICAEW | CAI | ICAS | AIA | TOTAL |

|---|---|---|---|---|---|---|---|---|

| Total numbers for 2021 | 446,232 | 93,696 | 5,842 | 33,958 | 7,668 | 4,154 | 5,556 | 597,106 |

| % growth (20-21) | 2.6 | -5.2 | 10.6 | 7.3 | 4.3 | 7.9 | 3.3 | 1.6 |

| % growth (17-21) | 7.6 | -26.4 | 32.7 | 21.9 | 15.1 | 7.9 | 3.6 | 1.2 |

| % compound annual growth (17-21) | 1.9 | -7.4 | 7.3 | 5.1 | 3.6 | 1.9 | 0.9 | 0.3 |

Analysis of members and students of the seven 8 Accountancy Bodies

The total membership of the seven accountancy bodies in the UK and ROI rose by 2.1% in 2021 compared to 1.9% in

- Total membership has continued to grow steadily at a compound annual growth rate of 2.0% for the period 2017 to 2021. (Figure 1)

Growth rates of membership vary considerably at each of the individual accountancy bodies in the UK and ROI. Whilst ICAEW continues to have the largest number of members in this jurisdiction, AIA, CAI and ACCA showed the strongest rates of growth in 2021 at 6.0%, 4.1% and 3.2% respectively. Only ICAS saw a fall in 2021 of 0.1%. (Figure 1) The total number of students in the UK and ROI has increased by 0.3% from 2020 to 2021 compared with a decrease of 2.1% between 2019 and

-

ACCA has the largest number of students but saw a decrease in numbers between 2020 and 2021 of 1.3%, whilst ICAS and ICAEW saw the largest % increases in 2021. (Figure 1) The worldwide membership of the accountancy bodies has grown by 2.8% from 2020 to 2021 and at a compound annual growth rate of 2.7% for the period 2017 to

-

(Figure 2) Overall, worldwide student numbers increased by 1.6% from 2020 to 2021; this compares to a decrease of 2.7% between 2019 and 2020, with a compound annual growth rate of 0.3% between 2017 and

-

(Figure 2)

Qualifications differ across the Recognised Qualifying Bodies (Figure 31). Just over 74% of the total worldwide student membership are training with ACCA for their qualifications. (Figure 2)

Students who became members

Figure 3 shows the number of students worldwide who became members as at 31 December for each of the years 2017 to 2021.

Figure 3: Students to members worldwide, 2017 to 2021 Bar chart showing the number of students who became members worldwide for ACCA, CIMA, CIPFA, ICAEW, CAI, ICAS, and AIA for years 2017 to

- Bars for each body show values between 0 and 16,000 across the years.

| ACCA | CIMA | CIPFA | ICAEW | CAI | ICAS | AIA | TOTAL | |

|---|---|---|---|---|---|---|---|---|

| 2017 | 15,533 | 5,147 | 112 | 3,403 | 1,153 | 585 | 12 | 25,945 |

| 2018 | 14,756 | 3,598 | 133 | 4,525 | 996 | 801 | 5 | 24,814 |

| 2019 | 14,683 | 3,798 | 199 | 4,359 | 1,243 | 657 | 3 | 24,942 |

| 2020 | 12,450 | 3,933 | 183 | 4,444 | 1,189 | 794 | 6 | 22,999 |

| 2021 | 13,423 | 4,156 | 223 | 4,244 | 1,224 | 755 | 2 | 24,027 |

| % growth (20-21) | 7.8 | 5.7 | 21.9 | -4.5 | 2.9 | -4.9 | -66.7 | 4.5 |

ICAEW, ICAS and AlA have all seen a decline in the number of students becoming members in 2021 compared with

- Overall, the total number of students who became members worldwide has risen from 2020 to 2021 by 4.5%. This compares with a decrease of 7.8% from 2019 to 2020.

Sectoral employment of members and students worldwide

Figure 4 shows the percentage of members and students worldwide for each of the seven accountancy bodies, according to their sectoral employment 9 as at 31 December 2021.

Figure 4: Sectoral employment worldwide, 2021

Stacked bar chart showing the percentage of members and students in different employment sectors (Other, Retired, Public Sector, Industry & Commerce, Working in Practice) for ACCA, CIMA, CIPFA, ICAEW, CAI, ICAS, and AIA. Each body has two bars representing Members and Students.

The Industry and Commerce sector employs the highest percentage of members (54%) and students (41%) across the accountancy bodies. CIMA and AlA members in this sector make up 73% and 87% of their respective total memberships.

Over three-quarters of students at ICAEW, CAI and ICAS are in practice (i.e. working at an accountancy firm). In contrast, 2% or less of CIMA, CIPFA and AlA students are employed in practice.

Female members and students worldwide

Figures 5 and 6 show the percentage of female members and students worldwide, respectively, as at 31 December for each of the years 2017 to 2021.

Figure 5: Female members worldwide, 2017 to 2021

Line graph showing the percentage of female members worldwide for ACCA, CIMA, CIPFA, ICAEW, CAI, ICAS, and AIA from 2017 to 2021, with percentages ranging from 25% to 50%.

Since 2017, all the accountancy bodies have increased their percentage of female members worldwide. AlA experienced the largest increase of 3 percentage points, in this period. ACCA continues to have the highest percentage of female members of all the accountancy bodies.

The overall percentage of female members worldwide has increased from 36% in 2017 to 37% in 2021.

Figure 6: Female students worldwide, 2017 to 2021

Line graph showing the percentage of female students worldwide for ACCA, CIMA, CIPFA, ICAEW, CAI, ICAS, and AIA from 2017 to 2021, with percentages ranging from 35% to 65%.

The overall percentage of female students (50%) is greater than the overall percentage of female members (37%).

ACCA had the largest percentage of female students in 2021 at 60%.

For 2017 to 2020, CAI and ICAS figures refer only to the proportion of female students in the student intake, not of the total student population.

Age of members and students worldwide

Figures 7 and 8 compare the age distribution of members and students as at 31 December 2017 and 2021.

Figure 7: Age of members worldwide, 2017 and 2021

Stacked bar chart showing the age distribution of members worldwide (Under 25, 25-34, 35-44, 45-54, 55-64, 65 and over, Not Stated) for ACCA, CIMA, CIPFA, ICAEW, CAI, ICAS, and AIA for years 2017 and 2021.

There were significant differences in the age profiles of the worldwide members of the seven accountancy bodies in

- ACCA, CAI and ICAS had relatively high proportions of members aged under 35 at 26%, 27% and 24% respectively, while CIPFA had the largest percentage of members aged 45 and over at 74%.

The largest proportion of worldwide members were aged between 35 to 44 in 2021, accounting for 29% of the total population.

Footnotes

Figure 7: Age of members worldwide, 2017 and 2021

A stacked bar chart showing the age distribution of members worldwide for ACCA, CIMA, CIPFA, ICAEW, CAI, ICAS, and AIA in 2017 and

- Age categories include Under 25, 25-34, 35-44, 45-54, 55-64, 65 and over, and Not Stated. Most bodies show a significant proportion of members in the 35-44 and 45-54 age ranges.

There were significant differences in the age profiles of the worldwide members of the seven accountancy bodies in

- ACCA, CAI and ICAS had relatively high proportions of members aged under 35 at 26%, 27% and 24% respectively, while CIPFA had the largest percentage of members aged 45 and over at 74%.

The largest proportion of worldwide members were aged between 35 to 44 in 2021, accounting for 29% of the total population.

Figure 8: Age of Students Worldwide, 2017 and 202110

A stacked bar chart illustrating the age distribution of students worldwide for ACCA, CIMA, CIPFA, ICAEW, CAI, ICAS, and AIA in 2017 and

- Age categories are Under 25, 25-34, 35-44, 45 and over, and Not Stated. Many bodies, particularly ICAEW and ICAS, show a very high percentage of students under 34.

In 2021, 39% of all students from the seven accountancy bodies were under the age of 25 compared with 38% in 2017. ICAEW, ICAS and CAI had the highest percentage of students aged 34 or under at 97%, 96%, and 88% respectively in

- In comparison, CIPFA had the largest proportion of students aged 35 and over at 49%.

Diversity information on members and students

We asked all bodies whether they collect data on the protected characteristics recognised under the Equality Act 2010, and this year also asked whether any of the bodies collected data on the socio-economic background of their members and students. Figure 9 shows the number of professional bodies that collect data on the protected characteristics and socio-economic background with respect to their members and students.

Figure 9: Diversity information collected on members and students, 2021

A bar chart showing the number of accountancy bodies that collect diversity information on members and students across various protected characteristics and socio-economic background in

- Categories include Age, Disability, Race, Religion or belief, Sex, Sexual orientation, and Socio-economic background. For most categories, around 6-7 bodies collect data on members, and 4-5 bodies collect data on students.

In 2021, six of the nine protected characteristics under the Equality Act 2010, were used by at least one of the bodies to record data on members and students. The other three Equality Act indicators (marriage and civil partnerships, pregnancy and maternity, and gender reassignment) were not recorded. In addition, three of the bodies recorded data on socio-economic background.

Location of students

Figure 10 shows the location11 (UK and ROI, and the rest of the world) of students of the accountancy bodies as at 31 December 2021.

Figure 10: Location of students, 2021

A stacked bar chart showing the percentage distribution of students by location (UK & ROI vs. Rest of the World) for ACCA, CIMA, CIPFA, ICAEW, CAI, ICAS, and AIA in

- ACCA and AIA have a majority of students outside the UK & ROI, while ICAEW, CAI, and ICAS primarily have students within the UK & ROI.

97% of AIA and 83% of ACCA students were based outside the UK and ROI. In contrast, ICAS and CAI had 1% or less of students based outside the UK and ROI.

27% of all students from the accountancy bodies were studying in the UK and ROI.

Profile of students of the Accountancy Bodies worldwide

Figure 11 sets out on a worldwide basis the length of time12 that individuals have been registered as students with these accountancy bodies.

Figure 11: Profile of students worldwide, 2021

A stacked bar chart showing the percentage of students worldwide by length of registration time (≤ 1 Year, > 1 - 2 Years, > 2 - 3 Years, > 3 - 4 Years, > 4 - 5 Years, ≥ 5 Years) for ACCA, CIMA, CIPFA, ICAEW, CAI, ICAS, and AIA in

- The chart illustrates varying durations of student registration across the different bodies.

A high percentage of CAI, ICAEW and ICAS students complete their training in four years or less, with only 14%, 13% and 10% of their students, respectively, being registered for more than four years, as at 31 December 2021.

Graduate entrants to training

Figure 12 shows the percentages of students worldwide of each accountancy body who, at the time of registering as students, were (i) graduates of any discipline and, of those, (ii) graduates who held a 'relevant degree'.13

Figure 12: Graduate entrants worldwide, 2021

A bar chart showing the percentage of students holding a degree and a relevant degree for ACCA, CIMA, CIPFA, ICAEW, CAI, ICAS, and AIA in

- The chart indicates that a higher percentage of students hold a general degree compared to a relevant degree across most bodies.

Comparisons of the percentage of students holding 'relevant degrees' are difficult to assess because the accountancy bodies use different definitions of a 'relevant degree'.

The accountancy bodies do not require entrants to hold a university degree and offer a range of entry routes.

ACCA, ICAEW, CAI, ICAS and CIMA also have apprenticeship schemes intended for non-graduates/school leavers as an entry route into the accountancy profession.

The Association of Accounting Technicians (AAT)

Members and students in the UK and ROI and worldwide

AAT is used as an entry-level qualification by some of the chartered accountancy bodies included in this publication. Figure 13 shows the number of AAT members and students, and the overall percentage growth from 2017 to 2021.

Figure 13: AAT members and students, 2017 to 2021

| Members | UK & ROI | Worldwide | Students | UK & ROI | Worldwide |

|---|---|---|---|---|---|

| 2017 | 45,537 | 48,580 | 64,777 | 77,649 | |

| 2018 | 50,745 | 52,584 | 93,068 | 98,897 | |

| 2019 | 50,619 | 52,346 | 87,482 | 92,094 | |

| 2020 | 48,362 | 50,028 | 80,138 | 83,997 | |

| 2021 | 48,860 | 50,452 | 79,611 | 83,245 | |

| % growth (20–21) | 1.0 | 0.8 | -0.7 | -0.9 | |

| % growth (17–21) | 7.3 | 3.9 | 22.9 | 7.2 |

A bar chart showing the number of AAT members and students in the UK & ROI and worldwide from 2017 to

- The chart displays four series: Members UK & ROI, Members Worldwide, Students UK & ROI, and Students Worldwide. Student numbers peaked in 2018 and declined, while member numbers increased and then stabilized.

The number of members in the UK and ROI, and worldwide increased by 1% and 0.8% respectively between 2020 and

- This is in contrast to a decrease in the number of students by 0.7% in the UK and ROI, and 0.9% worldwide.

Age distribution of members and students

Figure 14 indicates the age distribution of AAT members and students for 2021.

Figure 14: AAT Age of members and students worldwide 2021

A bar chart showing the age distribution of AAT members and students worldwide in 2021 across four age groups: Under 25, 25-34, 35-44, and 45 and over. Members are primarily in the 45 and over age group, while students are concentrated in the Under 25 and 25-34 age groups.

The highest percentage of members (52%) are aged 45 and over, while the highest percentage of students (62%) are under the age of 35.

Resource Information

Figure 15: AAT Resource information, 2017 to 2021

| £m | 2017 | 2018 | 2019 | 2020 | 2021 |

|---|---|---|---|---|---|

| Fees & subscriptions | 16.10 | 15.97 | 17.23 | 17.69 | 17.63 |

| Education & exam fees | 12.26 | 12.25 | 12.68 | 10.39 | 12.60 |

| Regulation & discipline | 0.03 | 0.05 | 0.07 | 0.05 | 0.06 |

| Commercial activities | 0.44 | 0.56 | 0.56 | 0.45 | 0.51 |

| Other (including investment income) | 1.13 | 1.30 | 1.09 | 0.91 | 0.41 |

| Total income | 29.96 | 30.13 | 31.63 | 29.49 | 31.21 |

| Number of staff | 256 | 261 | 264 | 225 | 217 |

Section Three – Resource Information on the Accountancy Bodies

Resource income of the seven accountancy bodies

We collected resource information on the seven Accountancy Bodies for year ends in

- Figures 16 and 17 show the total and average income respectively from worldwide members and students of the accountancy bodies between 2017 and 2021,^14 respectively.

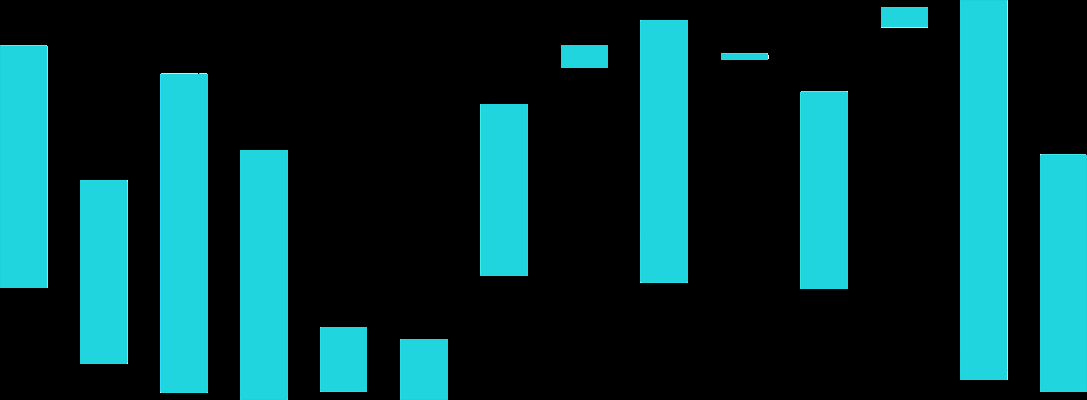

Figure 16: Total income worldwide, 2017 to 2021

A line chart showing the total income worldwide (£m) for ACCA, CIMA, CIPFA, ICAEW, CAI, ICAS, and AIA from 2017 to

- ACCA consistently has the highest income, while other bodies show varying trends over the period.

Since 2017, ICAEW has experienced a continuous increase in their income. ACCA has the highest income of the seven accountancy bodies, £223m in 2021.

CIMA and AIA have seen an overall decrease in their income between 2017 and 2021, down 0.9% and 1.1%, respectively.

ICAEW figures have been updated for 2019, 2020 and 2021 to show post audit information.

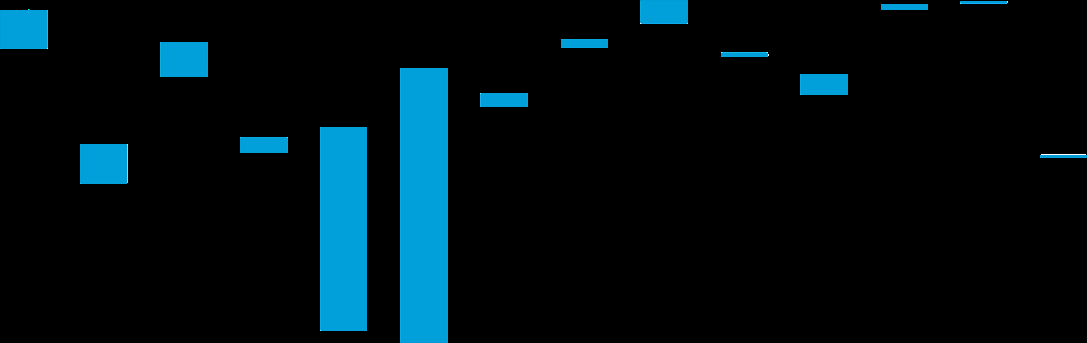

Average income per body from members and students

The average income per member and student is calculated by dividing the income of each accountancy body, excluding 'Commercial activities' and 'Other' (Figure 18), by its total worldwide population of members and students.

Figure 17: Average income per members and students worldwide, 2017 to 2021

A line chart showing the average income per member and student worldwide (£) for ACCA, CIMA, CIPFA, ICAEW, CAI, ICAS, and AIA from 2017 to

- CAI and ICAS show the highest average income, while ACCA and CIMA are lower.

CAI and ICAS had the highest average income per member and student in 2021 with £682 and £671 respectively.

The fluctuation in CAI's average income per member and student since 2017 is partly a result of the exchange rates applied (€1.127 in 2017, €1.115 in 2018, €1.171 in 2019, €1.1250 in 2020 and €1.1633 in 2021).

Breakdown of income

Figure 18 provides an analysis of the streams of income for the accountancy bodies for 2021.

Figure 18: Breakdown of income, 2021

A stacked bar chart showing the breakdown of income by source for ACCA, CIMA, CIPFA, ICAEW, CAI, ICAS, and AIA in

- Income streams include Fees & Subscriptions, Education & Exam Fees, Regulation & Discipline, Commercial Activities, and Other (Including Investment Income). Fees & Subscriptions and Education & Exam Fees are major components for most bodies, while CIPFA relies heavily on Commercial Activities.

Fees and subscriptions, taken together with education and exam fees from members and students, are the main sources of income for each of the bodies with the exception of CIPFA. CIPFA's main source of income is from commercial activities (68%).15

Fees and subscriptions and education and exam fees make up 94% of income for AIA.

Staffing of the Accountancy Bodies

Figure 19 shows the number of staff (full-time equivalent) employed worldwide by the seven accountancy bodies from 2017 to 2021.

Figure 19: Staffing, 2017 to 2021, FTEs

| Staffing | ACCA | CIMA | CIPFA | ICAEW | CAI | ICAS | AIA | TOTAL |

|---|---|---|---|---|---|---|---|---|

| 2017 | 1,358 | 198 | 259 | 706 | 149 | 154 | 25 | 2,849 |

| 2018 | 1,362 | 190 | 216 | 741 | 150 | 161 | 23 | 2,843 |

| 2019 | 1,383 | 487 | 211 | 692 | 156 | 146 | 21 | 3,096 |

| 2020 | 1,404 | 383 | 196 | 707 | 161 | 151 | 19 | 3,021 |

| 2021 | 1,362 | 405 | 207 | 707 | 166 | 173 | 19 | 3,039 |

| % growth (20–21) | -3.0 | 5.7 | 5.6 | 0.0 | 3.1 | 14.6 | 0.0 | 0.6 |

| % growth (17–21) | 0.3 | 104.5 | -20.1 | 0.1 | 11.4 | 12.3 | -24.0 | 6.7 |

| % compound annual growth (17–21) | 0.1 | 19.6 | -5.4 | 0.0 | 2.7 | 3.0 | -6.6 | 1.6 |

In 2017, CIMA amalgamated with the American Institute of Certified Public Accountants (AICPA). Post-merger, in 2017 and 2018, CIMA was able to supply staff numbers for the UK only, rather than for the whole of the new Association; the 2019, 2020 and 2021 figures once again include CIMA staff worldwide.

Diversity information on the workforce under the Equality Act 2010

We asked the bodies whether they collect information in relation to all the protected characteristics under the Equality Act

- Figure 20 shows the number of bodies that collect this diversity information on their workforce.

Figure 20: Diversity information on the workforce, 2021

A bar chart showing the number of accountancy bodies that collect diversity information on their workforce in 2021, categorised by Age, Disability, Gender reassignment and civil partnership, Pregnancy and maternity, Race, Religion or Belief, Sex, and Sexual orientation. Most characteristics are recorded by 5-7 bodies, with fewer for Gender reassignment and civil partnership (1 body).

All the bodies confirmed that they have a diversity policy and/or statement in place. The policies cover a range of issues such as equality, inclusion and social mobility for both their workforces and external stakeholders. The policies also extend to dealing with bullying and harassment in the workplace.

In 2021, all nine of the protected characteristics were used by at least one of the bodies to record this diversity information on their workforce.

All the diversity policies are aimed at improving awareness of diversity and ensuring that no employee or applicant for employment is treated less favourably than another because of their protected characteristic.

There is no requirement for employees to disclose their diversity status to their employer.

Section Four – Oversight of audit regulation

Recognised Supervisory Bodies (RSBs)16

Under the Statutory Audit and Third Country Auditors Regulations (SATCAR) 201617 the FRC is the designated Competent Authority for statutory audit in the UK. SATCAR 2016 sets out the responsibilities of the Competent Authority and permits the FRC to delegate some of the tasks required to fulfil its responsibilities.

The FRC delegates statutory tasks for the regulation of auditors of non-PIEs to the RSBs through delegation agreements. The FRC oversees the fulfilment of the 'Delegated Tasks', which include provisions for:

- The application of technical standards and of other standards on professional ethics and internal quality control of statutory audits and statutory audit work (including provision for security compliance with those standards).

- Registration: The application of the FRC's criteria for determining whether persons are eligible for appointment as statutory auditors, the registration of such persons, keeping the register18 and making it available for inspection;

- Continuing professional development: Procedures for maintaining the competence of statutory auditors;

- Audit monitoring: Monitoring of statutory auditors and the quality of audit work; and

- Enforcement: Except for categories retained by the FRC, investigations and imposing and enforcing sanctions in relation to breaches of relevant requirements by statutory auditors.

The FRC also exercises delegated statutory functions under Part 42 of the Companies Act 2006 for the recognition, supervision and de-recognition of RSBs. The FRC reports annually to the Secretary of State (SoS) on the discharge of these functions.19

Number of firms registered with the RSBs

Figure 21 shows the number of registered audit firms for each RSB split by the number of principals20 at each firm, for each of the three years to 31 December 2021.

Figure 21: Total registered firms by number of principals, 2019 to 2021

| Number of principals per firm | ACCA | ICAEW | CAI | ICAS | TOTAL |

|---|---|---|---|---|---|

| 1 | 904 | 871 | 290 | 36 | 2,101 |

| 2-3 | 476 | 971 | 238 | 66 | 1,751 |

| 4-6 | 80 | 397 | 49 | 30 | 556 |

| 7-10 | 59 | 123 | 15 | 6 | 203 |

| 11-50 | 22 | 83 | 9 | 3 | 117 |

| 50+ | 0 | 12 | 3 | 2 | 17 |

| Total as at 31.12.21 | 1,541 | 2,457 | 604 | 143 | 4,745 |

| Total as at 31.12.20 | 1,565 | 2,561 | 723 | 158 | 5,007 |

| Total as at 31.12.19 | 1,577 | 2,636 | 750 | 164 | 5,127 |

The number of audit firms registered to carry out statutory audit work in the UK and ROI continues to fall. The number of registered audit firms fell by 2.3% in 2020 (to 5,007) and 5.2% in 2021 (to 4,745). The number of RSBs with registered audit firms with two to three principals fell from 1,808 in 2020 to 1,751 in

- None of the RSBs saw an increase in the number of registered audit firms that are sole practitioners.

Statutory audit firms

Figure 22 details the number of registrations by firms split by:

- New applications: applications submitted to become a registered statutory audit firm;

- Referred to a committee: applications referred by case managers to a committee to make a decision;

- Approved by committee: committees can approve applications with conditions and restrictions if deemed necessary;

- Voluntarily surrendered: where a registered statutory audit firm no longer wants to carry out statutory audit work; and

- Withdrawn by the RSB: where an RSB's committee deems a firm unable to carry out statutory audits to the standard required.

Figure 22: Firm registrations, 2019 to 2021

| New applications | Referred to committee | Approved by committee | Voluntarily surrendered | Withdrawn by the RSB | |

|---|---|---|---|---|---|

| ACCA | 87 | 2 | 2 | 131 | 6 |

| ICAEW | 116 | 4 | 2 | 261 | 6 |

| 2019 | |||||

| CAI | 37 | 4 | 2 | 69 | 1 |

| ICAS | 5 | 1 | 1 | 12 | 1 |

| TOTAL | 245 | 11 | 7 | 473 | 14 |

| ACCA | 39 | 2 | 2 | 44 | 7 |

| ICAEW | 80 | 5 | 4 | 177 | 4 |

| 2020 | |||||

| CAI | 27 | 6 | 4 | 52 | 2 |

| ICAS | 4 | 0 | 0 | 10 | 0 |

| TOTAL | 150 | 13 | 10 | 283 | 13 |

| ACCA | 76 | 0 | 0 | 93 | 7 |

| ICAEW | 84 | 6 | 5 | 179 | 8 |

| 2021 | |||||

| CAI | 18 | 1 | 1 | 56 | 1 |

| ICAS | 1 | 0 | 0 | 15 | 1 |

| TOTAL | 179 | 7 | 6 | 343 | 17 |

The RSBs saw a 38.8% decrease in new applicants from 2019 to 2020, there was a 19.3% increase from 2020 to 2021.

- New applications: applications submitted to become a registered statutory audit firm;

- Referred to a committee: applications referred by case managers to a committee to make a decision;

- Approved by committee: committees can approve applications with conditions and restrictions if deemed necessary;

- Voluntarily surrendered: where a registered statutory audit firm no longer wants to carry out statutory audit work; and

- Withdrawn by the RSB: where an RSB's committee deems a firm unable to carry out statutory audits to the standard required.

Figure 22: Firm registrations, 2019 to 2021

| New applications | Referred to committee | Approved by committee | Voluntarily surrendered | Withdrawn by the RSB | |

|---|---|---|---|---|---|

| ACCA | 87 | 2 | 2 | 131 | 6 |

| ICAEW | 116 | 4 | 2 | 261 | 6 |

| 2019 | CAI | 37 | 4 | 2 | 69 |

| ICAS | 5 | 1 | 1 | 12 | |

| TOTAL | 245 | 11 | 7 | 473 | 14 |

| ACCA | 39 | 2 | 2 | 44 | 7 |

| ICAEW | 80 | 5 | 4 | 177 | 4 |

| 2020 | CAI | 27 | 6 | 4 | 52 |

| ICAS | 4 | 0 | 0 | 10 | |

| TOTAL | 150 | 13 | 10 | 283 | 13 |

| ACCA | 76 | 0 | 0 | 93 | 7 |

| ICAEW | 84 | 6 | 5 | 179 | 8 |

| 2021 | CAI | 18 | 1 | 1 | 56 |

| ICAS | 1 | 0 | 0 | 15 | |

| TOTAL | 179 | 7 | 6 | 343 | 17 |

The RSBs saw a 38.8% decrease in new applicants from 2019 to 2020, there was a 19.3% increase from 2020 to 2021.

Monitoring of registered audit firms by the FRC's Audit Quality Review team

The FRC's Audit Quality Review team (AQR) monitors the quality of the audit work of statutory auditors and audit firms in the UK that audit Public Interest Entities (PIEs) and certain other entities within the scope retained by the FRC (these are currently large AIM/ Lloyd's Syndicates/Listed Non-UK).

Figure 23 below details the number of reviews of audits conducted by the AQR team during the years ended 31 March 2019 to 31 March 2021.21, 22 & 23

Figure 23: AQR monitoring, 2019/20 to 2021/22

| Inspection category | Audit reviews 2019/20 | Audit reviews 2020/21 | Audit reviews 2021/22 |

|---|---|---|---|

| Deloitte LLP | 17 | 20 | 17 |

| EY LLP | 14 | 19 | 17 |

| KPMG LLP/KPMG Audit Plc | 18 | 22 | 19 |

| PricewaterhouseCoopers LLP | 17 | 21 | 18 |

| Big Four firms | 66 | 82 | 71 |

| BDO LLP | 8 | 9 | 12 |

| Grant Thornton UK LLP | 9 | 7 | 5 |

| Mazars LLP | 5 | 7 | 8 |

| PKF Littlejohn | 0 | 4 | 0 |

| MHA MacIntyre Hudson | 0 | 3 | 0 |

| Haysmacintyre | 0 | 2 | 0 |

| Crowe UK LLP | 0 | 1 | 2 |

| Gerald Edelman | – | 1 | 0 |

| RSM UK Audit LLP | 4 | 1 | 1 |

| Jeffreys Henry | – | 1 | 0 |

| Johnston Carmichael | – | 1 | 0 |

| UHY Hacker Young | 1 | 1 | 0 |

| Beever and Struthers | 0 | 0 | 2 |

| Begbies Chartered Accountants | 0 | 0 | 1 |

| Bennett Brooks & Co | 0 | 0 | 0 |

| Blick Rothenberg | – | – | – |

| BSG Valentine | 1 | 0 | 0 |

| Carter Backer Winter | 0 | 0 | 1 |

| Edwards Accountants | 0 | 0 | 1 |

| Edwards Veeder | 0 | 0 | 0 |

| Hazlewoods | 0 | 0 | 1 |

| HW Fisher | – | – | 1 |

| King & King | – | – | 3 |

| KPMG Audit LLC | 0 | 0 | 2 |

| Price Bailey | 0 | 0 | 0 |

| Shipleys | 0 | 0 | 0 |

| 94 | 120 | 111 | |

| Crown Dependency (CD) audit firms | 5 | 1 | 4 |

| 98 | 120 | 115 | |

| Third Country Auditors | 5 | 1 | 4 |

| Private sector audits | 104 | 121 | 119 |

| National Audit Office (NAO) | 7 | 7 | 9 |

| Local Audit | 15 | 20 | 20 |

| Foundation Trusts | – | 2 | 4 |

| Public sector audits | 22 | 29 | 33 |

| Total audits inspected | 125 | 150 | 152 |

Monitoring of registered audit firms by the RSBs

Figure 24 shows the number of monitoring visits conducted by the RSBs during the years ending 31 December 2019 to 31 December 202124 and the number of monitoring visits conducted as a percentage of the total number of registered audit firms at each RSB. There is a statutory requirement that the RSBs should monitor the activities undertaken by each registered audit firm at least once every six years.25

Figure 24: RSB monitoring and percentage of total registered Audit Firms, 2019 to 202126 & 27

| ACCA | ICAEW | CAI | ICAS | TOTAL | ||

|---|---|---|---|---|---|---|

| Number | 348 | 533 | 107 | 31 | 1,019 | |

| 2019 | % | 22.1 | 20.2 | 14.3 | 18.9 | 19.9 |

| Number | 186 | 410 | 107 | 29 | 732 | |

| 2020 | % | 11.9 | 16.0 | 14.8 | 18.4 | 14.6 |

| Number | 338 | 553 | 145 | 36 | 1,072 | |

| 2021 | % | 21.9 | 22.5 | 24.0 | 25.2 | 22.6 |

Bar chart showing RSB monitoring statistics by year: The chart visualizes the percentage of total registered audit firms monitored by each RSB (ACCA, ICAEW, CAI, ICAS) over the years 2019, 2020, and 2021, mirroring the data presented in Figure

- The Y-axis ranges from 0 to 30, representing percentages. Each bar group represents a year, and within each group, bars are colored blue for ACCA, purple for ICAEW, green for CAI, and pink for ICAS.

Reasons for monitoring visits to registered audit firms by RSBs

Figure 25 shows the reasons for the monitoring visits to registered audit firms by the RSBs during the years ended 31 December 2019 to 31 December 2021.28 & 29

Figure 25: Monitoring visit reason, 2019 to 2021

| ACCA | ICAEW | CAI | ICAS | TOTAL | ||

|---|---|---|---|---|---|---|

| 2019 | 4 | 9 | 35 | 2 | 50 | |

| Requested by the registration/ | 2020 | 6 | 3 | 14 | 0 | 23 |

| licensing committee | 2021 | 6 | 1 | 17 | 2 | 26 |

| 2019 | 113 | 136 | 12 | 8 | 269 | |

| Specifically selected due to | 2020 | 33 | 80 | 33 | 14 | 160 |

| heightened risk | 2021 | 77 | 112 | 36 | 11 | 236 |

| 2019 | 231 | 388 | 60 | 18 | 697 | |

| Cyclical visits | 2020 | 147 | 327 | 60 | 15 | 549 |

| 2021 | 255 | 440 | 92 | 21 | 808 | |

| 2019 | 0 | 0 | 0 | 3 | 3 | |

| Firms with PIEs visited with AQR | 2020 | 0 | 0 | 0 | 0 | 0 |

| involvement | 2021 | 0 | 0 | 3 | 2 | 5 |

Since 17 June 2016, audit firms that audit PIEs are subject to review by the FRC's AQR team. Prior to this date, different arrangements applied where the RSBs were responsible for the monitoring of some of these firms. The RSBs have no involvement in the monitoring of PIE audits, although they may rely on the AQR team's whole firm procedures when monitoring non-PIE audits at those audit firms.

Gradings of monitoring visits to registered Audit Firms by RSBs

Figures 26 to 29 show the grades for the audit monitoring visits to the firms and full audit file reviews conducted by the Association of Chartered Certified Accountants (ACCA), Institute of Chartered Accountants in England and Wales (ICAEW), Chartered Accountants Ireland (CAI) and Institute of Chartered Accountants of Scotland (ICAS) during the years ended 31 December 2019 to 2021.

The RSBs continue to have different systems for grading the quality of firms and full audit files reviewed.

- File grading: ICAEW, CAI and ICAS use the same definitions for grading full audit files. ACCA's definitions are set out below. The percentage of audit files provided in the tables for each of the RSBs is calculated on the basis of the number of files actually graded.

- Firm grading: This grade is given following a review by an RSB's inspection unit. The grades and definitions used are set out below.

- Other types of file review: Ungraded, limited and/or restricted are classifications for reviews conducted but not graded. An ungraded review is when a firm has no audit clients in a particular year. A limited and/or restricted review is a brief review of a specific risk or aspects noted from a previous visit.

File grading

ICAEW, 30 CAI and ICAS:

| 1 | No concerns regarding the sufficiency and quality of audit evidence or the appropriateness of significant audit judgements in the areas reviewed; only limited weakness in documentation of audit work; and any concerns in other areas are limited in nature (both individually and collectively). |

| (Satisfactory) | |

| 2A | Only limited concerns regarding the sufficiency or quality of audit evidence or the appropriateness of significant audit judgements in the areas reviewed; and/or weaknesses in documentation of audit work are restricted to a small number of areas; and/or some concerns, assessed as less than significant (individually and collectively), in other areas. |

| (Generally | |

| acceptable) | |

| 2B | Some concerns, assessed as less than significant, regarding the sufficiency or quality of audit evidence or the appropriateness of significant audit judgements in the areas reviewed; and/or more widespread weaknesses in documentation of audit work; and significant concerns in other areas (individually or collectively). |

| (Improvement | |

| required) | |

| 3 | Significant concerns regarding the sufficiency or quality of audit evidence or the appropriateness of significant audit judgements in the areas reviewed (not limited to the documentation of the underlying thought processes); and/or very significant concerns in other areas (individually or collectively). |

| (Significant | |

| improvements | |

| required) |

Association of Chartered Certified Accountants (ACCA):

ACCA uses the following initial grade assessment in determining the overall outcome on audit work.

| A Outcomes | The audit work appears appropriate in scope and extent with no significant deficiencies, forming a reasonable basis for the audit opinion. |

| B Outcomes | Minor deficiencies were noted in the audit work, but these do not result in a significant risk of any material misstatements remaining undetected and the audit opinion is adequately supported by the work recorded. |

| C Outcomes | There is serious non-compliance with applicable standards and/or deficiencies in the audit evidence recorded such that there is a significant risk that any material misstatements would remain undetected. |

Summary of monitoring results by body

Each year a mixture of firms are selected for review; however, as firm selection changes annually, monitoring results are not directly comparable year on year.

Furthermore, the sample of firms monitored each year will often include a disproportionate number of weaker firms, selected due to the targeted selection of firms deemed to be high risk. This needs to be taken into account when interpreting the percentage of D outcomes at each body (D outcomes are defined below).

Outcomes reported in the below tables include a number of visits to audit registered firms that have no audit clients. These reviews are done on a desktop basis.

Figure 26: ACCA gradings, 2019 to 2021

| Firm gradings | 2019 | 2020 | 2021 | File gradings | 2019 | 2020 | 2021 |

|---|---|---|---|---|---|---|---|

| A & B | No. | 264 | 142 | 184 | A Outcomes | No. | 34 |

| Outcomes | % | 76 | 76 | 54 | % | 6 | |

| No. | 43 | 15 | 41 | B Outcomes | No. | 471 | |

| C Outcomes | % | 12 | 8 | 12 | % | 74 | |

| No. | 41 | 30 | 34 | C Outcomes | No. | 128 | |

| D Outcomes | % | 12 | 16 | 10 | % | 20 | |

| No. | 0 | 0 | 79 | Ungraded/Limited | No. | 0 | |

| P Outcomes | % | 0 | 0 | 24 | /Restricted review |

Firm grading (ACCA) 31

| A Outcomes | The firm complies with auditing standards, ACCA's Global Practising Regulations (GPRs), and the Code of Ethics and Conduct (CEC) and the Ethical Standards for Auditors (ESA) issued by the FRC. |

| (Good) | |

| B Outcomes | The firm is eligible for audit registration; it complies with the GPRs, CEC and the ESA and 50% or more of its audit files inspected, including all significant audits, comply substantially with relevant auditing standards. |

| (Satisfactory) | |

| C Outcomes | The firm is eligible for audit registration and it complies with the GPRs, CEC and ESA but its quality controls over audit work are not effective and either the majority of the firm's audit files, or the significant audit files, inspected do not comply with relevant auditing standards. |

| (Unsatisfactory and | When a firm's work is considered very poor or if a firm has a second or subsequent unsatisfactory visit and there are no mitigating factors the visit is graded D, which indicates that regulatory action is required and will usually result in a referral to a Regulatory Assessor or the Admissions and Licensing Committee (ALC). Regulatory action in this context includes ACCA referring the findings of a monitoring visit to the Assessment Department to consider whether disciplinary action is appropriate. D outcomes do not always result from an inadequate standard of audit work, but could be for failure to meet the eligibility requirements for holding a firm's auditing certificate; they may also indicate a referral to the Assessment Department for other regulation breaches such as non-compliance with client money rules or with the terms of a regulatory order. |

| improvements required) | |

| D Outcomes | |

| (Regulatory action | |

| required) | |

| P Outcomes | These are visits where the final outcome has not been determined at 31 December. This is a consequence of a process change associated with the introduction of the Audit Monitoring Committee, whereby the outcome is only determined once the firm has submitted its action plan and it has been assessed by ACCA and/or the Committee. |

Institute of Chartered Accountants in England and Wales (ICAEW)

Figure 27: ICAEW gradings, 2019 to 2021

| Firm gradings | 2019 | 2020 | 2021 | File gradings | 2019 | 2020 | 2021 |

|---|---|---|---|---|---|---|---|

| A & B | No. | 269 | 249 | 340 | 1 Outcomes | No. | 199 |

| Outcomes | % | 54 | 58 | 63 | % | 25 | |

| No. | 88 | 73 | 83 | 2A Outcomes | No. | 395 | |

| C Outcomes | % | 18 | 17 | 15 | % | 49 | |

| No. | 43 | 33 | 24 | 2B Outcomes | No. | 151 | |

| D Outcomes | % | 9 | 8 | 4 | % | 19 | |

| No. | 96 | 78 | 91 | 3 Outcomes | No. | 62 | |

| N Outcomes | % | 19 | 18 | 17 | % | 8 | |

| Ungraded/Limited | No. | 154 | |||||

| /Restricted review |

Firm grading (ICAEW)

| A Outcomes | Where there are no instances of non-compliance with the Audit Regulations and no matters requiring follow-up action. |

| B Outcomes | Where there are some instances of non-compliance with the Audit Regulations. ICAEW's Quality Assurance Department (QAD) are confident that the firm has the commitment and ability to correct the issue(s) and the firm's responses address the matters raised without the need for follow-up action. |

| C Outcomes | Where there are instances of non-compliance and follow-up action is required: |

| * Submit information – additional details or evidence of the firm's actions previously agreed is required to demonstrate its commitment and ability to correct the issue. | |

| * Accept withdrawal – non-compliance that would require a follow-up action if the firm had not proposed to withdraw from the audit registration (no need for a report to Audit Registration Committee (ARC)). | |

| * Release from conditions and/or restrictions – some or no instances of non-compliance and confidence that previous conditions and restrictions can be lifted. | |

| D Outcomes | Where instances of non-compliance are likely to be serious or extensive and require a detailed report to ARC that can include three potential outcomes: |

| * Impose conditions and/or restrictions – non-compliance is likely to be serious or extensive and/or the firm's responses may be inadequate and/or raise doubts about the firm's ability/willingness to make the improvements. | |

| * Withdrawal - reserved for the most serious situations when the firm's audit registration should be withdrawn. | |

| * Committee consideration – to provide information to the committee when no conditions or restrictions have been proposed but the committee is required to consider the results of the visit. | |

| N Outcomes | Used for visits where no statutory audit work has been reviewed. For example, a firm continues with audit registration, but has no audit clients and no audit work has been reviewed; or a firm's withdrawal application is under consideration by QAD. This rating is also applied to Year 2 visits to large firms where no audit files are reviewed. |

Chartered Accountants Ireland (CAI)

Figure 28: CAI gradings 2019 to 2021

| Firm gradings | 2019 | 2020 | 2021 | File gradings | 2019 | 2020 | 2021 |

|---|---|---|---|---|---|---|---|

| A & B | No. | 70 | 69 | 120 | 1 Outcomes | No. | 56 |

| Outcomes | % | 62 | 79 | 81 | % | 31 | |

| No. | 10 | 3 | 14 | 2A Outcomes | No. | 74 | |

| C Outcomes | % | 9 | 3 | 9 | % | 41 | |

| No. | 33 | 15 | 14 | 2B Outcomes | No. | 28 | |

| D Outcomes | % | 29 | 18 | 9 | % | 16 | |

| 3 Outcomes | No. | 21 | |||||

| % | 12 | ||||||

| Ungraded/Limited | No. | 45 | |||||

| /Restricted review |

Firm grading (CAI)

| A Outcomes | Where no instances of breaches have been recorded. |

| B Outcomes | Where breaches were noted, and the firm is deemed to have the ability (competence and resources) to address the issue(s) within the stated timescales. |

| C Outcomes | There will generally be no matters to follow up on firms graded A and/or B. |

| Where breaches have been noted and the firm has undertaken actions to address the issues raised. In such instances, the firm is required to provide a written undertaking to cover the volunteered actions. The Quality Assurance Committee (QAC) will not impose conditions or restrictions; however, there is a need for further confirmation/follow-up. | |

| D Outcomes | Where breaches or issues have been identified which require consideration by the Head of Quality Assurance and by the QAC. There are four classes of D reports: D1, D2 and D3 reports are determined by the seriousness of the regulatory action, while D4 reports provide information to the QAC. |

Institute of Chartered Accountants of Scotland (ICAS)

Figure 29: ICAS gradings 2019 to 2021

| Firm gradings | 2019 | 2020 | 2021 | File gradings | 2019 | 2020 | 2021 |

|---|---|---|---|---|---|---|---|

| A & B | No. | 10 | 8 | 14 | 1 Outcomes | No. | 1 |

| Outcomes | % | 32 | 28 | 39 | % | 1 | |

| No. | 18 | 20 | 22 | 2A Outcomes | No. | 65 | |

| C Outcomes | % | 58 | 69 | 61 | % | 73 | |

| No. | 3 | 1 | 0 | 2B Outcomes | No. | 17 | |

| D Outcomes | % | 10 | 3 | 0 | % | 19 | |

| No. | 0 | 0 | 0 | 3 Outcomes | No. | 6 | |

| N Outcomes | % | 0 | 0 | 0 | % | 7 | |

| Ungraded/Limited | No. | 43 | |||||

| /Restricted review |

Firm grading (ICAS)

| A Outcomes | Where no issues have been identified and no follow-up action is needed. |

| B Outcomes | Where some regulatory issues were identified; however, these issues have been addressed adequately by the firm's closing meeting responses and no further action is required. |

| C Outcomes | Where there are regulatory issues and there is a need for the firm to submit evidence of action taken in a restricted area. The 'C' grading is split into a 'C–' or 'C+' grading with 'C–' being more serious, where one or more of the issues identified are considered to be pervasive; whereas C+ is where findings are specific to particular individuals or files and do not indicate systemic problems. |

| D Outcomes | Where the standard of compliance is such that the Authorisation Committee (AC) needs to consider appropriate follow-up action, such as imposition of conditions and restrictions or withdrawal of registration. |

Complaints about auditors

Figure 30 shows the number of audit-related complaints received by the RSBs from 2019 to 2021 split by (i) number of new complaints, (ii) number of cases passed to the FRC (iii) number of cases referred to the Committee,32 (iv) number of cases closed in the year and (v) average time taken to close a case.33

Figure 30: Complaints, 2019 to 2021

| ACCA | ICAEW | CAI | ICAS | TOTAL | ||

|---|---|---|---|---|---|---|

| 2019 | 10 | 156 | 8 | 7 | 181 | |

| Number of new | 2020 | 1 | 117 | 11 | 4 | 133 |

| complaints | 2021 | 15 | 145 | 3 | 2 | 165 |

| 2019 | 0 | 0 | 0 | 0 | 0 | |

| Number of cases referred | 2020 | 0 | 0 | 0 | 0 | 0 |

| to the FRC | 2021 | 0 | 0 | 0 | 0 | 0 |

| 2019 | 8 | 40 | 9 | 4 | 61 | |

| Number of cases passed | 2020 | 3 | 35 | 6 | 4 | 48 |

| to the Committee | 2021 | 0 | 28 | 10 | 1 | 39 |

| 2019 | 8 | 123 | 12 | 7 | 150 | |

| Number of cases closed | 2020 | 7 | 139 | 10 | 5 | 161 |

| in the year | 2021 | 4 | 152 | 13 | 1 | 170 |

| 2019 | 3.9 | 14 | 6.6 | 4.0 | ||

| Average time taken to | 2020 | 4.5 | 17 | 4.0 | 7.8 | |

| close a case (in months) | 2021 | 5.6 | 14 | 0.0 | 1.0 |

The definition of the average time taken to close a case differs across the accountancy bodies. Some record their data having regard to cases that are opened and closed within a particular year, while other bodies take the total length for a case to be concluded.

Bar chart showing New Complaints (2019-2021):

This blue bar chart represents the number of new complaints received by ACCA, ICAEW, CAI, and ICAS for the years 2019, 2020, and 2021, mirroring the 'New applications' data from Figure 30.

Bar chart showing Cases Referred to Committee (2019-2021):

This cyan bar chart represents the number of cases referred to committee by ACCA, ICAEW, CAI, and ICAS for the years 2019, 2020, and 2021, mirroring the 'Referred to committee' data from Figure 30.

Bar chart showing Cases Closed in the Year (2019-2021):

This blue bar chart represents the number of cases closed in the year by ACCA, ICAEW, CAI, and ICAS for the years 2019, 2020, and 2021, mirroring the 'Number of cases closed in the year' data from Figure 30.

Bar chart showing Average Time Taken to Close (2019-2021 - ACCA, ICAEW, CAI): This yellow bar chart represents the average time taken to close a case (in months) by ACCA, ICAEW, and CAI for the years 2019, 2020, and 2021, mirroring the 'Average time taken to close a case (in months)' data from Figure

- ICAS data is not shown on this chart as it uses a different basis.

Bar chart showing Average Time Taken to Close (2019-2021 - ICAS): This pink bar chart specifically represents the average time taken to close a case (in months) by ICAS for the years 2019, 2020, and 2021, mirroring the 'Average time taken to close a case (in months)' data from Figure

- This chart isolates ICAS data due to its different calculation method.

Recognised Qualifying Bodies (RQBs)

The FRC also exercises delegated statutory functions under Part 42 of the Companies Act 2006 for the recognition, supervision and decognition of those accountancy bodies responsible for offering the audit qualification (RQBs) in line with the requirements of Schedule 11 of the Act. There are five bodies34 in the UK recognised to offer the audit qualification. RQBs must have rules and arrangements in place to register students and track their progress, administer examinations and ensure that appropriate training is given to students in an approved environment. The FRC reports annually to the SoS on the discharge of these functions. Figure 31 shows the number of students registered with each RQB as at 31 December 2019 to

- It also shows the number of members who were awarded the audit qualification and the number of students following the audit route or eligible for the audit qualification.35

Figure 31: RQB students and members, 2019 to 2021

| ACCA | ICAEW | CAI | ICAS | AIA | ||

|---|---|---|---|---|---|---|

| 2019 | 79,937 | 22,842 | 7,009 | 3,862 | 135 | |

| Number of students in the UK | 2020 | 76,208 | 23,309 | 7,351 | 3,839 | 139 |

| and ROI | 2021 | 75,188 | 25,014 | 7,662 | 4,112 | 144 |

| 2019 | N/A | 18,657 | 3,640 | N/A | 3 | |

| Number of students following the | 2020 | N/A | 18,705 | 3,862 | N/A | 3 |

| audit route or eligible for the audit | 2021 | N/A | 19,345 | 4,538 | N/A | 3 |

| qualification | ||||||

| 2019 | 58 | 1,219 | 266 | 170 | 0 | |

| The number of members who were | 2020 | 100 | 1,082 | 572 | 1,148 | 0 |

| awarded the audit qualification | 2021 | 82 | 1,222 | 8036 | 288 | 0 |

| 2019 | 2,954 | 105,306 | 8,874 | 11,496 | 9 | |

| The number of members who hold | 2020 | 2,941 | 104,654 | 9,446 | 12,409 | 9 |

| the audit qualification | 2021 | 2,824 | 103,893 | 9,329 | 12,242 | 9 |

The audit qualification of some members may be counted twice – firstly by the body awarding the qualification, and then again if they become a member of another body while retaining their initial qualification.

Approved training offices

Figure 32 shows the total number of approved training offices37 in the UK and ROI over the period 2019 to

- The pie chart represents the 2021 data in percentages by each body.

Figure 32: UK and ROI training offices, 2019 to 2021, and proportion of total training offices per body in 2021

| ACCA | ICAEW | CAI | ICAS | AIA | ||

|---|---|---|---|---|---|---|

| Number of approved | 2019 | 3,415 | 4,552 | 697 | 405 | 10 |

| training offices in the | 2020 | 3,383 | 4,694 | 594 | 413 | 10 |

| UK & ROI | 2021 | 3,250 | 4,949 | 581 | 402 | 10 |

Pie chart showing the proportion of total training offices per body in 2021:

This pie chart visualizes the distribution of approved training offices in the UK & ROI among different accountancy bodies for the year 2021. * ICAEW accounts for 53.8%. * ACCA accounts for 35.4%. * CAI accounts for 6.3%. * ICAS accounts for 4.4%. * AIA accounts for 0.1%.

5. Audit firms

This section covers audit firms with PIE38 clients who responded to our survey. The FRC as Competent Authority has ultimate responsibility for the performance and oversight of the audit regulation tasks, as mandated originally by EU Regulation 537/2014 and EU Directive 2006/43/EC (as amended), and applied in the UK.39 The FRC cannot by law delegate the Regulatory Tasks of audit monitoring and enforcement pertaining to PIEs.

The information in this section has been provided on a voluntary basis and we would like to thank all the firms that responded to our requests. Some of this information is publicly available (for example firms that are Limited Liability Partnerships (LLPs) must file accounts at Companies House if they meet the statutory requirements). Figure 33 shows the fee income for audit and non-audit services for the 25 audit firms with PIE audit clients that responded to our request for the year ended

- This year we also include the fee incomes from PIE clients and non-PIE clients, and the breakdown of audit staff and non-audit staff at the firms in Figure 33. Firms are listed in order of their audit fee income, rather than by total fee income. This is not a league table. Not all accountancy firms have PIE audit clients, therefore firms without PIE audit clients are not approached to provide information for this publication. It is possible that there are firms not included in this publication that have a higher audit fee income than those that are listed in the tables below.

Care is needed if making detailed comparisons between firms using the information in Figure 33, as some firms do not analyse their fee income this way and have made an informed estimate of the figures. In addition, firms may classify their audit and non-audit income in slightly different ways. Figures 34 and 35 analyse the detailed fee income from Figure 33 for the Big Four firms and for many of the audit firms outside of the Big Four respectively.40

Figure 36 shows the percentage growth of fee income for firms with PIE clients for 2019/20 and 2020/21, while Figure 37 focuses on the audit fee income per responsible individual. Figure 38 shows those audit firms that audit companies listed on the FTSE 100, FTSE 250, other regulated markets and the Alternative Investment Market (AIM) as at each firm's financial year end for

- Figure 39 looks at the concentration of listed companies, split between the Big Four, the next five firms41 and a select number of audit firms that carry out statutory audits as at 31 December for the past five years.

In relation to diversity, we asked the firms to provide information on the following nine diversity indicators: race, disability, religion/belief, sexual orientation, marital status, school type attended, first generation to attend university, socio-economic background and caring responsibilities (Figure 46). This is the first year we have asked the firms whether they provide information on socio-economic background. We also requested data on gender, race, disability, and sexual orientation in respect of senior management at the PIE audit firms (Figures 40 to 44). A separate analysis of age can be found in Figure 45, which aggregates all the firms' workforces. Of the firms asked, approximately three-quarters have diversity policies in place, with some firms having set diversity targets for their staff, boards and committees (Figure 47).

Figure 33: UK fee income of audit firms with PIE audit clients, 2021 (by fee income from audit)

| UK firm name | UK structure | No. of principals42 | No. of audit principals | No. of RIs43 | Audit staff | Non-audit staff | No. of PIE audit clients | Fee income: audit (£m)44 | Fee income: non-audit work to audit clients (£m)45 | Fee income: non-PIE audit clients (£m) | Fee income: PIE clients (£m) | Fee income: non-PIE clients (£m) | Total fee income (£m) |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| PricewaterhouseCoopers46 | LLP | 914 | 169 | 327 | 968 | 5,577 | 409 | 790 | 201 | 2,566 | 303 | 487 | 3,557 |

| KPMG | LLP | 533 | 133 | 311 | 886 | 3,391 | 293 | 646 | 150 | 1,637 | 225 | 421 | 2,433 |

| EY UK | LLP | 717 | 122 | 234 | 678 | 4,876 | 266 | 595 | 156 | 2,003 | 177 | 418 | 2,754 |

| Deloitte | LLP | 674 | 106 | 262 | 1,047 | 6,526 | 321 | 573 | 288 | 3,002 | 249 | 324 | 3,863 |

| BDO | LLP | 370 | 131 | 151 | 466 | 985 | 212 | 276 | 91 | 363 | 36 | 240 | 730 |

| Grant Thornton UK | LLP | 201 | 52 | 96 | 320 | 1,085 | 27 | 146 | 49 | 376 | 4 | 141 | 570 |

| RSM | LLP | 357 | 104 | 127 | 183 | 743 | 25 | 99 | 53 | 223 | 9 | 90 | 375 |

| Mazars | LLP | 141 | 49 | 62 | 154 | 390 | 57 | 83 | 21 | 130 | 24 | 59 | 234 |

| Crowe UK | LLP | 83 | 40 | 43 | 92 | 148 | 18 | 41 | 12 | 49 | 1 | 40 | 102 |

| MHA MacIntyre Hudson | LLP | 84 | 53 | 44 | 85 | 86 | 21 | 28 | 19 | 28 | 4 | 24 | 75 |

| Haysmacintyre | LLP | 38 | 27 | 34 | 55 | 38 | 5 | 21 | 6 | 11 | 0 | 21 | 38 |

| PKF Littlejohn | LLP | 35 | 21 | 21 | 37 | 48 | 50 | 19 | 4 | 18 | 2 | 17 | 41 |

| Johnston Carmichael | LLP | 60 | 13 | 23 | 35 | 153 | 18 | 11 | 6 | 38 | 0 | 10 | 55 |

| UHY Hacker Young | LLP | 30 | 14 | 17 | 25 | 36 | 9 | 8 | 4 | 7 | 0 | 8 | 19 |

| Price Bailey | LLP | 26 | 10 | 13 | 18 | 40 | 1 | 7 | 2 | 19 | 0 | 7 | 28 |

| Gerald Edelman | LLP | 16 | 7 | 7 | - | - | 1 | 6 | 2 | 7 | 0 | 6 | 14 |

| Beever and Struthers | Partnership | 17 | 10 | 13 | 22 | 14 | 12 | 5 | 1 | 6 | 1 | 4 | 13 |

| Shipleys | LLP | 14 | 10 | 13 | 26 | 17 | 2 | 4 | 1 | 10 | 0 | 4 | 15 |

| Hazlewoods | LLP | 27 | 10 | 13 | 16 | 56 | 5 | 4 | 3 | 24 | 0 | 4 | 31 |

| Carter Backer Winter | LLP | 17 | 6 | 9 | 10 | 15 | 1 | 2 | 1 | 12 | 0 | 2 | 15 |

| Bennett Brooks & Co | Limited company | - | - | 3 | 4 | 27 | 2 | 1 | 0 | 7 | 0 | 1 | 8 |

| BSG Valentine | LLP | 8 | 2 | 4 | 3 | 7 | 1 | 1 | 0 | 5 | 0 | 1 | 7 |

| Begbies Chartered Accountants | Limited company and Partnership | 10 | 9 | 9 | - | - | 1 | 1 | 0 | 3 | 0 | 1 | 4 |

| Edwards Accountants (Midlands) | Limited company | 3 | 3 | 3 | 8 | 4 | 1 | 1 | 0 | 2 | 0 | 1 | 3 |

| Edwards Veeder | Limited company | 4 | 4 | 4 | 6 | 0 | 1 | 0 | 0 | 1 | 0 | 0 | 1 |

Figure 34: Proportion of total fee income for the Big Four firms, 2019 to 2021

A bar chart showing the proportion of total fee income for the Big Four firms from 2019 to 2021, broken down into Audit Fee Income, Fee Income from Non-Audit work to Audit Clients, and Fee Income from Non-Audit Clients. - In 2019: Audit Fee Income (74.4%), Non-Audit work to Audit Clients (19.3%), Non-Audit Clients (6.3%). - In 2020: Audit Fee Income (73.7%), Non-Audit work to Audit Clients (20.3%), Non-Audit Clients (6.0%). - In 2021: Audit Fee Income (73.0%), Non-Audit work to Audit Clients (20.7%), Non-Audit Clients (6.3%).

Figure 35: Proportion of total fee income for audit firms with PIE audit clients outside the Big Four firms, 2019 to 2021

A bar chart showing the proportion of total fee income for audit firms with PIE audit clients outside the Big Four firms from 2019 to 2021, broken down into Audit Fee Income, Fee Income from Non-Audit work to Audit Clients, and Fee Income from Non-Audit Clients. - In 2019: Audit Fee Income (57.7%), Non-Audit work to Audit Clients (28.3%), Non-Audit Clients (14.1%). - In 2020: Audit Fee Income (56.6%), Non-Audit work to Audit Clients (30.2%), Non-Audit Clients (13.2%). - In 2021: Audit Fee Income (56.2%), Non-Audit work to Audit Clients (32.1%), Non-Audit Clients (11.6%).

Growth of fee income

Figure 3647 shows the percentage growth rate of fee income for each of the years 2019/20 and 2020/21 for audit firms with PIE clients, split between (i) the Big Four audit firms and audit firms outside the Big Four and (ii) between audit and non-audit income.

Audit firm population changes year-on-year based on those firms with PIE clients that choose to respond to this survey.

Figure 36: Growth of fee income, 2020 and 2021

A bar chart illustrating the percentage growth of fee income for Big Four and Non-Big Four firms in 2020 and 2021 across different categories: Total Fee Income, Audit Fee Income, Non-Audit Work to Audit Clients Fee Income, and Non-Audit Work to Non-Audit Clients Fee Income. - For Total Fee Income (2020, 2021): Big Four firms (4.6%, 5.9%), Non-Big Four firms (5.9%, 12.5%). - For Audit Fee Income (2020, 2021): Big Four firms (6.5%, 10.3%), Non-Big Four firms (12.5%, -6.8%). - For Non-Audit Work to Audit Clients Fee Income (2020, 2021): Big Four firms (-2.0%, 3.7%), Non-Big Four firms (-5.9%, 5.3%). - For Non-Audit Work to Non-Audit Clients Fee Income (2020, 2021): Big Four firms (3.7%, 5.3%), Non-Big Four firms (5.3%, 0%).

Total fee income grew by 4.6% for Big Four firms and 5.9% for non-Big Four firms. Audit fee income growth was stronger at 6.5% for Big Four firms and 12.5% for non-Big Four but lower than last year's growth rates in both cases.

Fee income from non-audit work for audit clients increased by 10.3% for Big Four firms (after a fall last year) but declined by 6.8% for non-Big Four firms. For non-audit work for non-audit clients, fee income increased by 3.7% for Big Four firms and 5.3% for non-Big Four firms.

Audit fee income per Responsible Individual (RI)

Figure 37 illustrates audit fee generated per Responsible Individual (RI) for 2019 to

- This information is split between the Big Four firms and the audit firms outside the Big Four.

Figure 37: Average audit fee income per RI, 2019 to 2021

| Audit Fee Income Per RI (£m) | 2019 | 2020 | 2021 |

|---|---|---|---|

| Big Four firms | 2.07 | 2.23 | 2.30 |

| Average of all firms with PIE clients | 1.61 | 1.68 | 1.83 |

| Non-Big Four firms | 0.85 | 0.89 | 1.08 |

A line chart showing the average audit fee income per Responsible Individual (RI) from 2019 to 2021 for Big Four firms, average of all firms with PIE clients, and Non-Big Four firms. - Big Four firms: 2.07 in 2019, 2.23 in 2020, 2.30 in 2021. - Average of all firms with PIE clients: 1.61 in 2019, 1.68 in 2020, 1.83 in 2021. - Non-Big Four firms: 0.85 in 2019, 0.89 in 2020, 1.08 in 2021.

There has been a continual increase in the average income per RI for all firms since 2004, when we began our data collection for this publication.

Figure 38: Concentration of listed company audits, 2021 (by number of listed clients48 – FTSE 100, FTSE 250, UK equity listed on regulated markets and the Alternative Investment Market (AIM))

| UK firm name | UK structure | Year end | No. of FTSE 100 audit clients48 | No. of FTSE 250 audit clients48 | Total no. of other clients listed on regulated markets48 | No of AIM audit clients48 |

|---|---|---|---|---|---|---|

| PricewaterhouseCoopers | LLP | 30 June | 26 | 74 | 73 | 80 |

| EY UK | LLP | 02 July | 23 | 42 | 66 | 16 |

| KPMG49 | LLP | 30 September | 23 | 39 | 45 | 23 |

| Deloitte | LLP | 31 May | 21 | 47 | 119 | 24 |

| BDO | LLP | 02 July | 1 | 17 | 131 | 166 |

| Grant Thornton UK | LLP | 31 December | 0 | 4 | 9 | 62 |

| MHA MacIntyre Hudson | LLP | 31 March | 0 | 2 | 1 | 9 |

| RSM | LLP | 31 March | 0 | 1 | 13 | 56 |

| Crowe UK | LLP | 31 March | 0 | 0 | 19 | 44 |

| Mazars | LLP | 31 August | 0 | 0 | 16 | 16 |

| PKF Littlejohn | LLP | 31 May | 0 | 0 | 7 | 70 |

| Hazlewoods | LLP | 30 April | 0 | 0 | 5 | 4 |

| Price Bailey | LLP | 31 March | 0 | 0 | 1 | 3 |

| BSG Valentine | LLP | 30 September | 0 | 0 | 1 | 1 |

| Edwards Veeder | Limited Company | 31 March | 0 | 0 | 1 | 1 |

| Begbies | Limited company and Partnership | 31 March | 0 | 0 | 1 | 0 |

| Carter Backer Winter | LLP | 31 March | 0 | 0 | 1 | 0 |