The content on this page has been converted from PDF to HTML format using an artificial intelligence (AI) tool as part of our ongoing efforts to improve accessibility and usability of our publications. Note:

- No human verification has been conducted of the converted content.

- While we strive for accuracy errors or omissions may exist.

- This content is provided for informational purposes only and should not be relied upon as a definitive or authoritative source.

- For the official and verified version of the publication, refer to the original PDF document.

If you identify any inaccuracies or have concerns about the content, please contact us at [email protected].

FRC response to EC consultation on non-binding guidelines on methodology for reporting non-financial

Financial Reporting Council

Nicolas Bernier-Abad Accounting and Financial Reporting Unit DG FISMA European Commission SPA2 00/089 1000 Brussels Belgium

4 April 2016

Dear Nicolas,

Non-Binding Guidelines for Reporting Non-Financial Information by Companies

Thank you for the opportunity to comment on the European Commission Consultation. We believe that non-mandatory guidance can be helpful to companies when implementing legal requirements and based on our experience in the UK with the FRC's Guidance on the Strategic Report1 can lead to improvements in the quality of corporate reporting. The FRC attaches great importance to Clear & Concise reporting and ensuring that the annual report includes information that is relevant to investors.

We have some concerns about the direction of travel of the Commission's proposals, in particular that some of the questions may be re-opening positions that were agreed at the time of negotiating the EU Directive on disclosure of non-financial and diversity information (the 'non-financial reporting Directive'). We have completed the questionnaire but our overarching comments are highlighted below.

(a) Audience of the non-financial statement (Q2) – we believe that asking the question about the audience of the non-financial statement in the context of guidelines that support the non-financial reporting Directive is inappropriate. The EU legal framework sets out that the primary audience for information contained in an annual report is the company's shareholders and materiality is determined in that context.

We acknowledge that other stakeholders will have an interest in a company's activities and reporting can improve transparency. However, where information is of interest to a broader group of stakeholders, we encourage the disclosure of information outside the annual report. In our view, considering the placement of information depending on the audience will result in more relevant information for all users.

(b) Principles-based guidelines (Q4) – we commend the Commission for developing a Directive that is proportionate, principles-based and takes into account materiality. In developing the guidelines, we believe that the Commission should ensure that it does not go beyond the principles in the Directive and inadvertently introduce new disclosures.

In our view, any guidelines should be concise, principles-based and allow companies flexibility to tell their story. We do not support prescriptive guidelines as these can lead to boiler plate reporting as well as resulting in excessive detail that can obscure relevant information.

(c) Key performance indicators (KPIs) (Q6) – when reporting KPIs, we believe that it is critical that companies report KPIs that are material to their business rather than including a long list of indicators. It is for the directors' to apply judgement in determining which indicators are key to their business. We are concerned that including a comprehensive list of KPIs in the guidelines will result in companies including immaterial KPIs in their annual report. In addition, we consider that it is important that, where relevant, KPIs are linked to the business model and strategy.

(d) National frameworks (Q8) – we believe that any European Commission guidelines should complement national frameworks and be flexible to enable member states to use national guidance where it exists. The UK legislation for narrative reporting is broader than non-financial reporting and it is vital that UK companies are not precluded from using local guidance as a result of the European guidelines.

(e) Reference to other frameworks (Q8) - we do not support the guidelines containing an exhaustive list of all frameworks for non-financial reporting. We believe that this would be confusing for companies given that there are a number of frameworks in existence that address similar issues, many of which do not have authoritative status. The Directive deliberately contains a broad principle that companies may rely on “national, Union-based or international frameworks”. We believe that the guidelines should not include a greater degree of prescription of the framework than is set out in the Directive.

We would be pleased to share our experiences of developing guidance as the Commission considers its guidelines.

If you would like to discuss these comments, please contact Deepa Raval on 020 7492 2424.

Yours sincerely

Melanie Mclaren Executive Director DDI: 020 7492 2406 Email: [email protected]

Case Id: 78216664-6a56-4ce3-ad43-d0fdd90dd388 Date: 05/04/2016 16:02:05

Public consultation on non-binding guidelines on methodology for reporting non-financial information

Fields marked with * are mandatory.

Introduction

The Directive 2014/95/EU on disclosure of non-financial and diversity information by certain large undertakings and groups entered into force on 6 December 2014, after having been published in the EU Official Journal on 15 November 2014. The Directive 2014/95/EU amends Directive 2013/34/EU on the annual financial statements, consolidated statements and related reports of certain types of undertakings.

The Directive 2014/95/EU aims at improving the transparency of certain large EU companies as regards non-financial information, and focuses on relevant, useful information.

Following Article 1 of the Directive, the new disclosure requirements apply to large public-interest entities with more than 500 employees. The concept of public-interest entities is defined in Article 2 of Directive 2013/34/EU, and includes companies listed in EU markets, as well as some unlisted companies, such as credit institutions, insurance companies, and other companies that are so designated by Member States because of their activities, size or number of employees.

Article 1 of the Directive establishes that companies concerned shall include in the management report a non-financial statement containing information relating to, as a minimum:

- Environmental matters

- Social and employee matters

- Respect for human rights

- Anti-corruption and bribery matters.

Article 1 of the Directive also establishes that the non-financial statement shall include:

- 1a brief description of the undertaking's business model;

- 2a description of the policies pursued by the undertaking in relation to those matters, including due diligence processes implemented;

- 3the outcome of those policies;

- 4the principal risks related to those matters linked to the undertaking's operations including, where relevant and proportionate, its business relationships, products or services which are likely to cause adverse impacts in those areas, and how the undertaking manages those risks;

- 5non-financial key performance indicators relevant to the particular business.

Companies, investors and society at large will benefit from increased transparency as it leads to stronger long-term performance. This is important for Europe's long-term competitiveness and the creation of jobs. Investors are more and more interested in non-financial information in order to have a comprehensive understanding of a company's position and performance, and to analyse and factor this information in their investment-decision process. The Directive 2014/95/EU aims at enhancing the consistency and comparability of non-financial information disclosed throughout the Union (recital 6).

The Directive has been designed in a non-prescriptive manner, and leaves significant flexibility for companies to disclose relevant information in the way that they consider most useful. Companies may rely on national frameworks, Union-based frameworks such as the Eco-Management and Audit Scheme (EMAS), or international frameworks such as the United Nations (UN) Global Compact, the Guiding Principles on Business and Human Rights implementing the UN 'Protect, Respect and Remedy' Framework, the Organisation for Economic Co-operation and Development (OECD) Guidelines for Multinational Enterprises, the International Organisation for Standardisation's ISO 26000, the International Labour Organisation's Tripartite Declaration of principles concerning multinational enterprises and social policy, the Global Reporting Initiative, or other recognised international frameworks (recital 9). Companies may also consider the sectorial OECD Due Diligence Guidance for Responsible Supply Chains of Minerals from Conflict-Affected and High-Risk Areas, as appropriate.

In order to provide further guidance and help companies implement these provisions the co-legislators have tasked the Commission with the preparation of non-binding guidelines on methodology for reporting non-financial information. Article 2 of the Directive refers to "guidance on reporting", and sets out that "the Commission shall prepare non-binding guidelines on methodology for reporting non-financial information, including non-financial key performance indicators, general and sectoral, with a view to facilitating relevant, useful and comparable disclosure of non-financial information by undertakings. [...]" The objective of the non-binding guidelines is to facilitate the disclosure of non-financial information by undertakings (recital 17).

The purpose of this public consultation is to collect information and views from stakeholders on guidance on reporting of non-financial information by companies across all sectors.

At this time, it is premature to prejudge what form the guidelines should take. This will depend on the outcome of this consultation. The guidelines should be relevant and useful across all economic sectors, and cover appropriately general principles, methodology, and non-financial key performance indicators.

In providing their input to this consultation, stakeholders are invited to consider the companies and groups concerned under Article 1 of the Directive. The new disclosure requirements relating to non-financial information apply to large public-interest entities with more than 500 employees. The concept of public-interest entities is defined in Article 2 of Directive 2013/34/EU, and includes companies listed in EU markets as well as some unlisted companies, such as credit institutions, insurance companies, and other companies that are so designated by Member States because of their activities, size or number of employees.

Please note: In order to ensure a fair and transparent consultation process only responses received through our online questionnaire will be taken into account and included in the report summarising the responses. Should you have a problem completing this questionnaire or if you require particular assistance, please contact [email protected].

More information:

- on this consultation

- on the protection of personal data regime for this consultation

1. Information about you

- Are you replying as:

- a private individual

- an organisation or a company

-

a public authority or an international organisation

-

First name and last name:

-

Name of your organisation: Financial Reporting Council

-

Name of the public authority:

Contact email address: The information you provide here is for administrative purposes only and will not be published [email protected]

- Is your organisation included in the Transparency Register? (If your organisation is not registered, we invite you to register here, although it is not compulsory to be registered to reply to this consultation. Why a transparency register?)

- Yes

-

No

-

If so, please indicate your Register ID number: 891654116196-35

-

Type of organisation:

- Academic institution

- Consultancy, law firm

- Industry association

- Non-governmental organisation

- Trade union

- Company, SME, micro-enterprise, sole trader

- Consumer organisation

- Media

- Think tank

-

Other

-

Please specify the type of organisation: Regulator

-

Type of public authority

- International or European organisation

- Regional or local authority

- Government or Ministry

- Regulatory authority, Supervisory authority or Central bank

-

Other public authority

-

Please specify the type of public authority:

-

Where are you based and/or where do you carry out your activity?

- Austria

- Belgium

- Bulgaria

- Croatia

- Cyprus

- Czech Republic

- Denmark

- Estonia

- Finland

- France

- Germany

- Greece

- Hungary

- Iceland

- Ireland

- Italy

- Latvia

- Liechtenstein

- Lithuania

- Luxembourg

- Malta

- Norway

- Poland

- Portugal

- Romania

- Slovakia

- Slovenia

- Spain

- Sweden

- Switzerland

- The Netherlands

- United Kingdom

- Other country

-

Please specify your country:

-

Field of activity or sector (if applicable): at least 1 choice(s)

- Accounting

- Auditing

- Rating agencies

- Banking

- Insurance

- Reporting/Communication

- Corporate Social Responsibility/ Sustainability

- Investment management (e.g. hedge funds, private equity funds, venture capital funds, money market funds, securities)

- Other

-

Not applicable

-

Please specify your activity field(s) or sector(s):

A Important notice on the publication of responses

- Contributions received are intended for publication on the Commission's website. Do you agree to your contribution being published? (see specific privacy statement)

- Yes, I agree to my response being published under the name I indicate (name of your organisation/company/public authority or your name if your reply as an individual)

- No, I do not want my response to be published

2. Your opinion

For the purposes of this public consultation:

"The GUIDELINES": The non-binding guidelines on methodology for reporting non-financial information that the Commission will prepare in accordance with Article 2 of Directive 2014/95/EU on disclosure of non-financial and diversity information by certain large undertakings and groups ("the DIRECTIVE").

"KPIs": Key performance indicators.

I. General principles and key attributes of the non-financial information

Q1. What aspects of disclosure of non-financial information do you think that should be addressed by the GUIDELINES?

Please, order in terms of importance (1 least important, 9 most important)

- Materiality/Relevance

- Usefulness

- Comparability

- Avoiding undue administrative burden

- Comprehensiveness

- Fairness and balance

- Understandability

- Reliability

-

Other

-

Please specify what other aspect of disclosure of non-financial information should be addressed by the GUIDELINES:

Clear & Concise communication

Q2. Who should be considered in your opinion the main audience of the non-financial statement?

Please, check the box of the alternative that you consider most appropriate.

- The shareholders

- The investment community in a broad sense

- Users of information with an economic interest, such as suppliers, customers, employees, etc.

- All users of information (including consumers, local communities, NGOs, etc.)

-

Other

-

Please specify who else should be considered in your opinion the main audience of the non-financial statement:

-

Q2.1 Could you please provide a brief explanation on your answer regarding who should be considered the main audience of the non-financial statement? 400 character(s) maximum

In our view, the primary audience for the annual report is shareholders as set out in the EU legal framework.

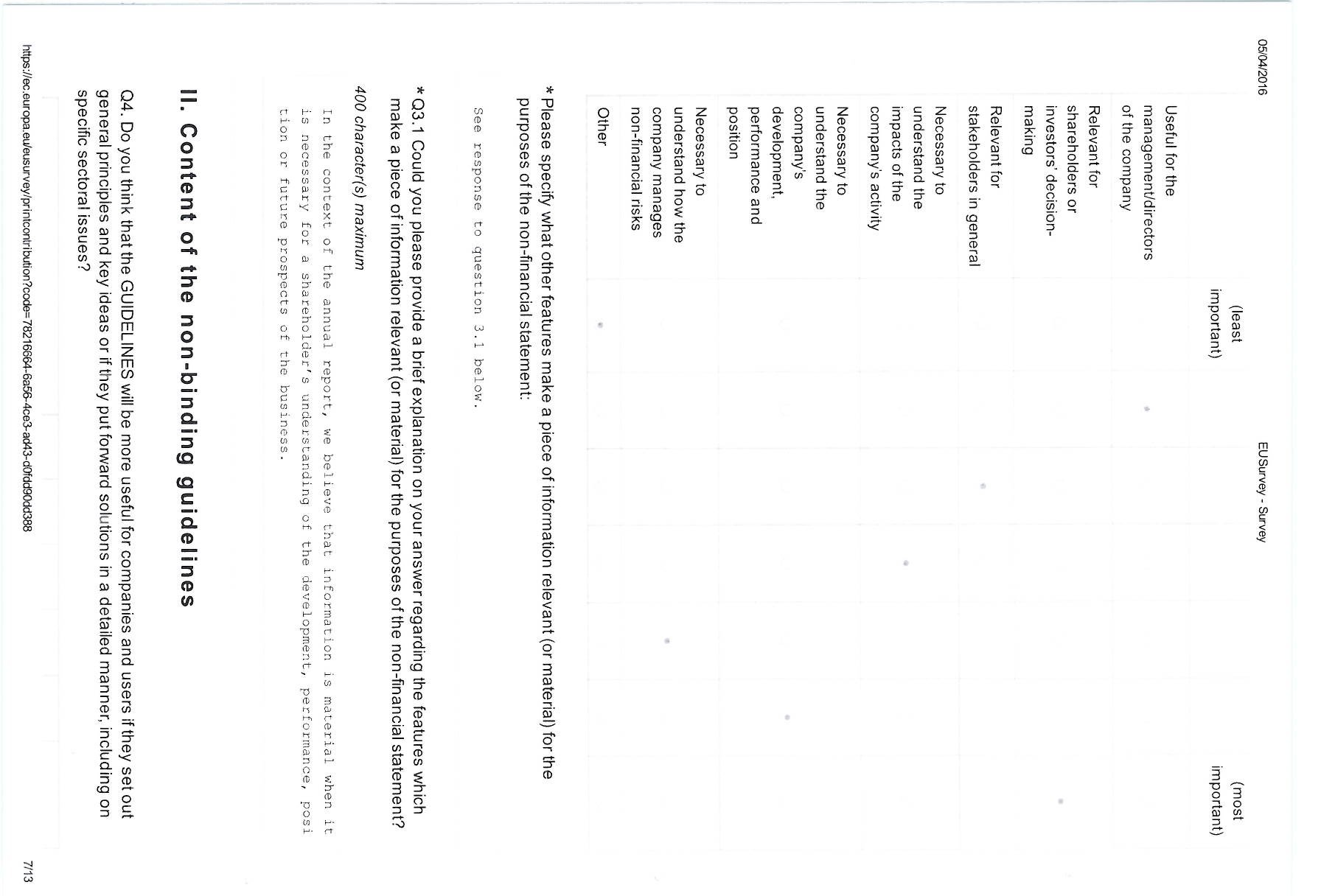

Q3. In your opinion, what features make a piece of information relevant (or material) for the purposes of the non-financial statement?

Please order in terms of importance (1 least important, 7 most important)

- Useful for the management/directors of the company

- Relevant for shareholders or investors' decision-making

- Relevant for stakeholders in general

- Necessary to understand the impacts of the company's activity

- Necessary to understand the company's development, performance and position

- Necessary to understand how the company manages non-financial risks

-

Other

-

Please specify what other features make a piece of information relevant (or material) for the purposes of the non-financial statement:

See response to question 3.1 below.

- Q3.1 Could you please provide a brief explanation on your answer regarding the features which make a piece of information relevant (or material) for the purposes of the non-financial statement? 400 character(s) maximum

In the context of the annual report, we believe that information is material when it is necessary for a shareholder's understanding of the development, performance, position or future prospects of the business.

II. Content of the non-binding guidelines

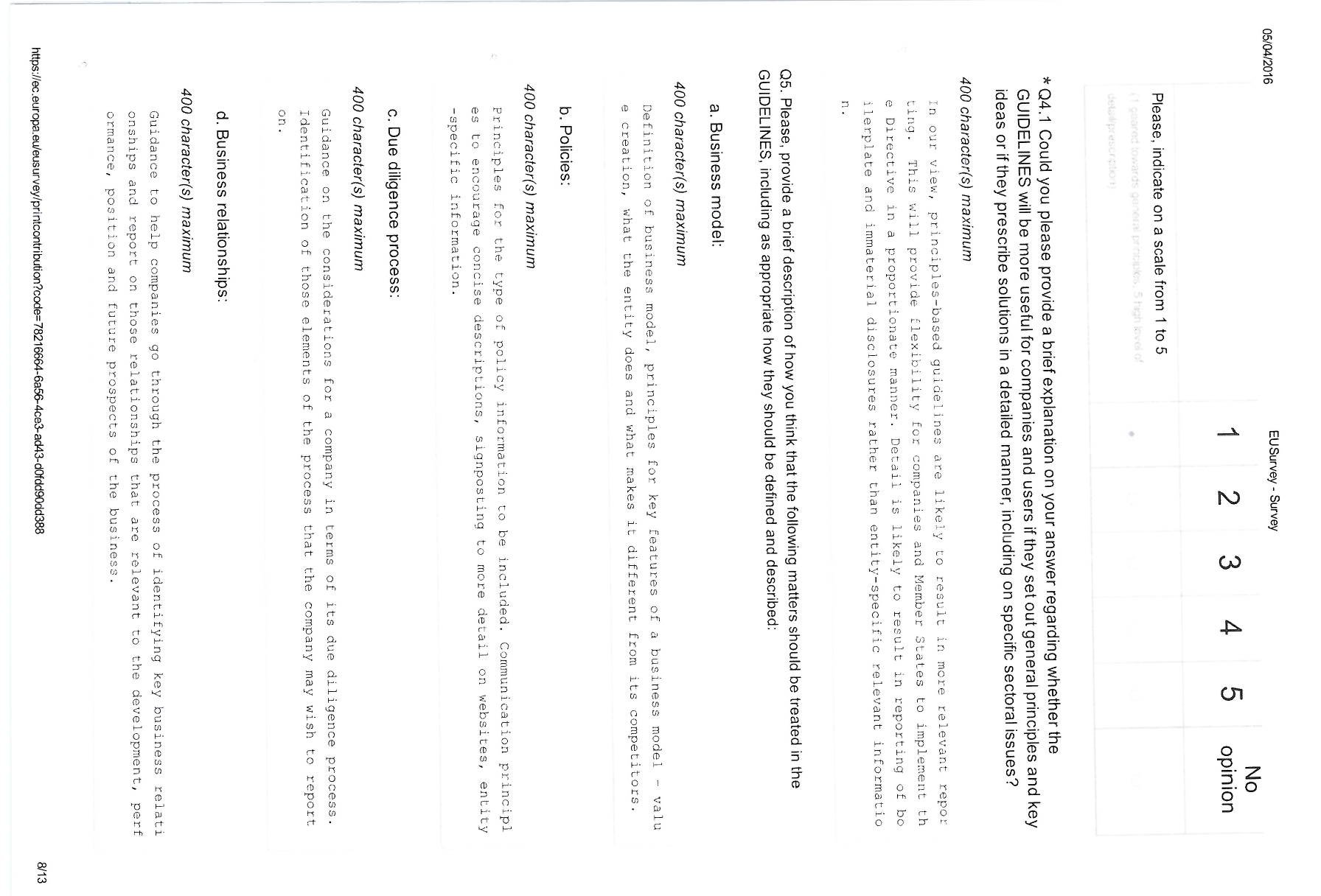

Q4. Do you think that the GUIDELINES will be more useful for companies and users if they set out general principles and key ideas or if they put forward solutions in a detailed manner, including on specific sectoral issues?

Please, indicate on a scale from 1 to 5 (1 geared towards general principles, 5 high level of detail/prescription)

- Q4.1 Could you please provide a brief explanation on your answer regarding whether the GUIDELINES will be more useful for companies and users if they set out general principles and key ideas or if they prescribe solutions in a detailed manner, including on specific sectoral issues? 400 character(s) maximum

In our view, principles-based guidelines are likely to result in more relevant reporting. This will provide flexibility for companies and Member States to implement the Directive in a proportionate manner. Detail is likely to result in reporting of boilerplate and immaterial disclosures rather than entity-specific relevant information.

Q5. Please, provide a brief description of how you think that the following matters should be treated in the GUIDELINES, including as appropriate how they should be defined and described:

- Business model: 400 character(s) maximum Definition of business model, principles for key features of a business model – value creation, what the entity does and what makes it different from its competitors.

- Policies: 400 character(s) maximum Principles for the type of policy information to be included. Communication principles to encourage concise descriptions, signposting to more detail on websites, entity-specific information.

- Due diligence process: 400 character(s) maximum Guidance on the considerations for a company in terms of its due diligence process. Identification of those elements of the process that the company may wish to report on.

- Business relationships: 400 character(s) maximum Guidance to help companies go through the process of identifying key business relationships and report on those relationships that are relevant to the development, performance, position and future prospects of the business.

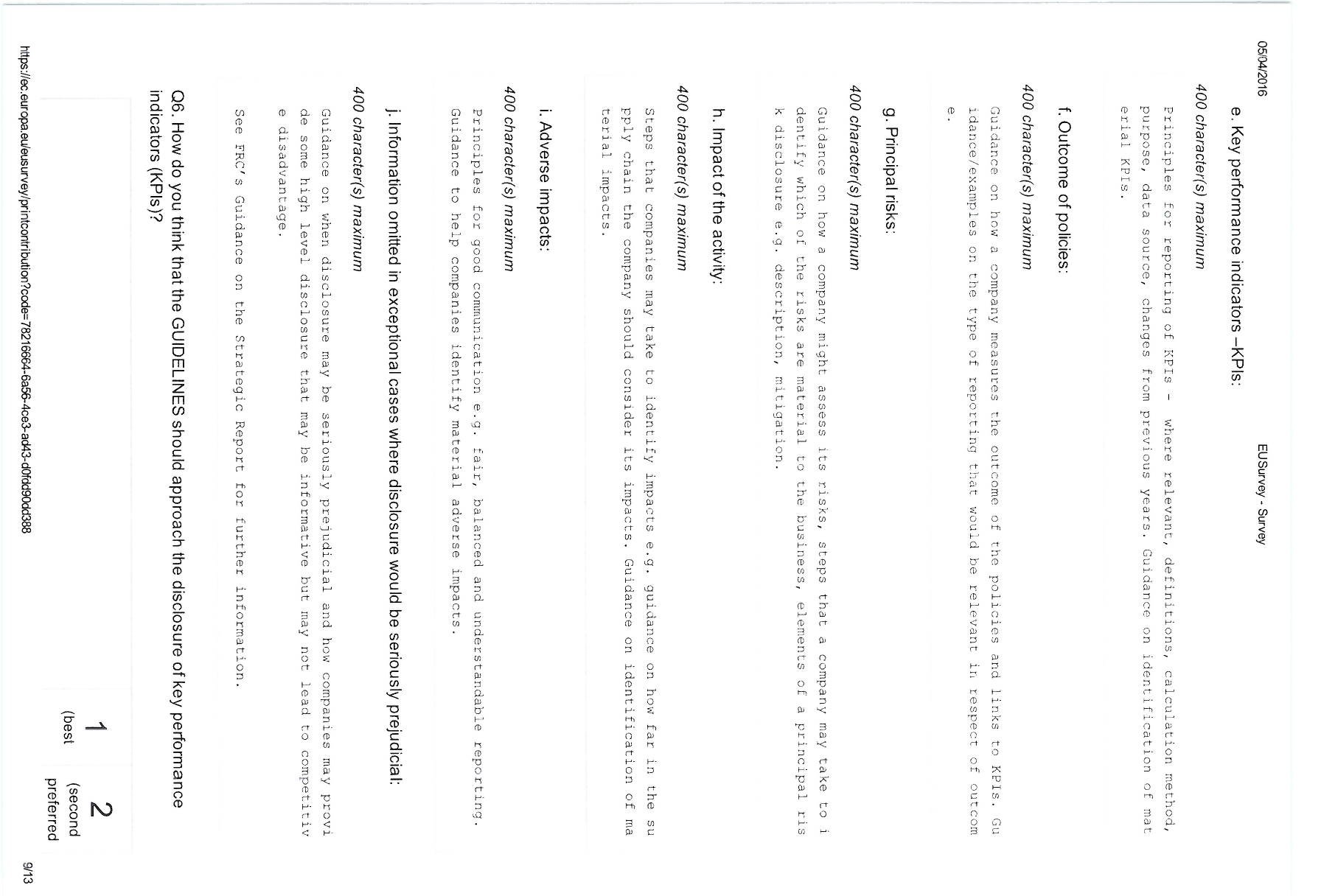

- Key performance indicators -KPIs: 400 character(s) maximum Principles for reporting of KPIs – where relevant, definitions, calculation method, purpose, data source, changes from previous years. Guidance on identification of material KPIs.

- Outcome of policies: 400 character(s) maximum Guidance on how a company measures the outcome of the policies and links to KPIs. Guidance/examples on the type of reporting that would be relevant in respect of outcome.

- Principal risks: 400 character(s) maximum Guidance on how a company might assess its risks, steps that a company may take to identify which of the risks are material to the business, elements of a principal risk disclosure e.g. description, mitigation.

- Impact of the activity: 400 character(s) maximum Steps that companies may take to identify impacts e.g. guidance on how far in the supply chain the company should consider its impacts. Guidance on identification of material impacts.

- Adverse impacts: 400 character(s) maximum Principles for good communication e.g. fair, balanced and understandable reporting. Guidance to help companies identify material adverse impacts.

- Information omitted in exceptional cases where disclosure would be seriously prejudicial: 400 character(s) maximum Guidance on when disclosure may be seriously prejudicial and how companies may provide some high level disclosure that may be informative but may not lead to competitive disadvantage.

See FRC's Guidance on the Strategic Report for further information.

Q6. How do you think that the GUIDELINES should approach the disclosure of key performance indicators (KPIs)?

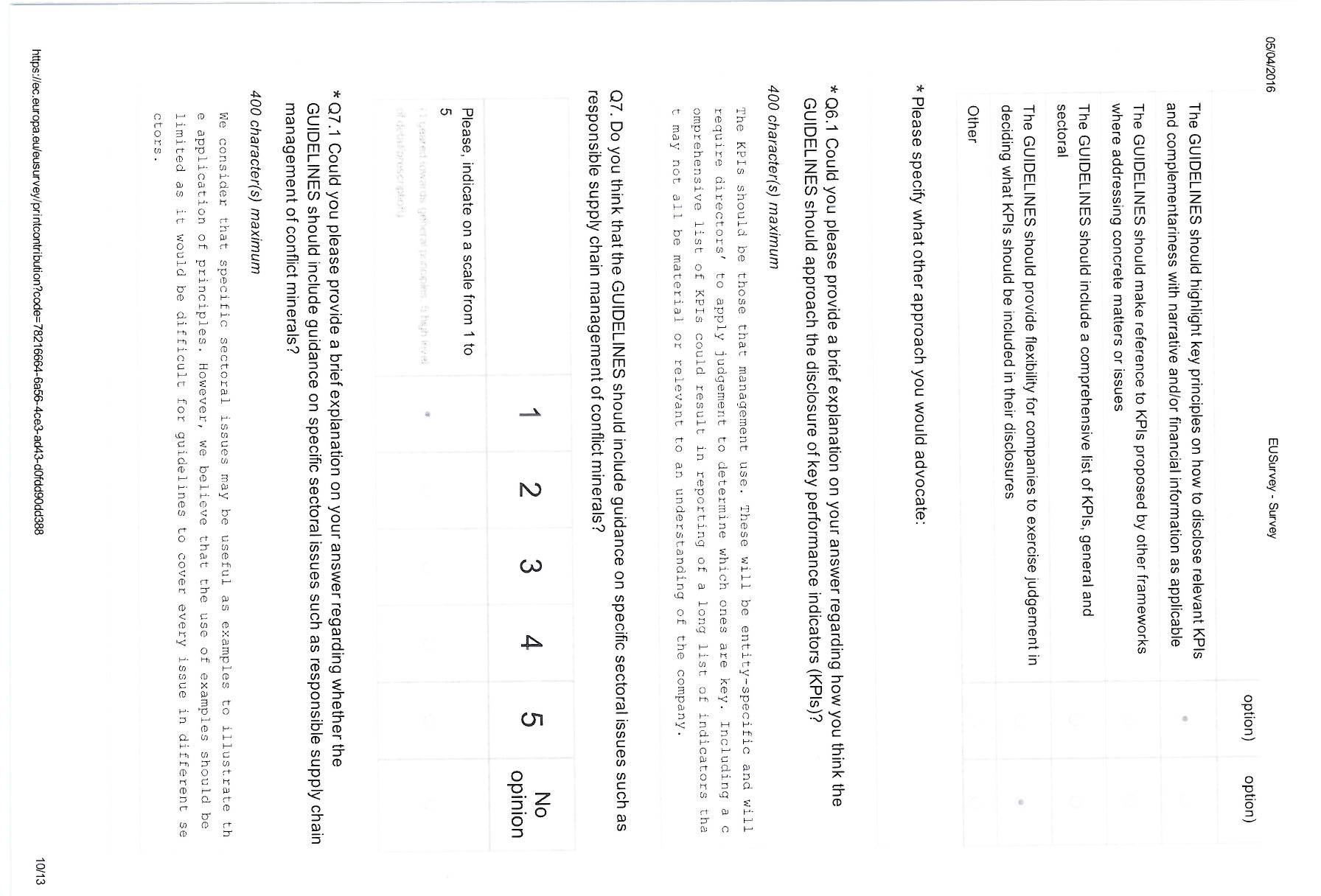

- The GUIDELINES should highlight key principles on how to disclose relevant KPIs and complementariness with narrative and/or financial information as applicable

- The GUIDELINES should make reference to KPIs proposed by other frameworks where addressing concrete matters or issues

- The GUIDELINES should include a comprehensive list of KPIs, general and sectoral

- The GUIDELINES should provide flexibility for companies to exercise judgement in deciding what KPIs should be included in their disclosures

-

Other

-

Please specify what other approach you would advocate:

-

Q6.1 Could you please provide a brief explanation on your answer regarding how you think the GUIDELINES should approach the disclosure of key performance indicators (KPIs)? 400 character(s) maximum

The KPIs should be those that management use. These will be entity-specific and will require directors' to apply judgement to determine which ones are key. Including a comprehensive list of KPIs could result in reporting of a long list of indicators that may not all be material or relevant to an understanding of the company.

Q7. Do you think that the GUIDELINES should include guidance on specific sectoral issues such as responsible supply chain management of conflict minerals?

Please, indicate on a scale from 1 to 5 (1 geared towards general principles, 5 high level of detail/prescription)

- Q7.1 Could you please provide a brief explanation on your answer regarding whether the GUIDELINES should include guidance on specific sectoral issues such as responsible supply chain management of conflict minerals? 400 character(s) maximum

We consider that specific sectoral issues may be useful as examples to illustrate the application of principles. However, we believe that the use of examples should be limited as it would be difficult for guidelines to cover every issue in different sectors.

III. Interaction with other frameworks and other aspects

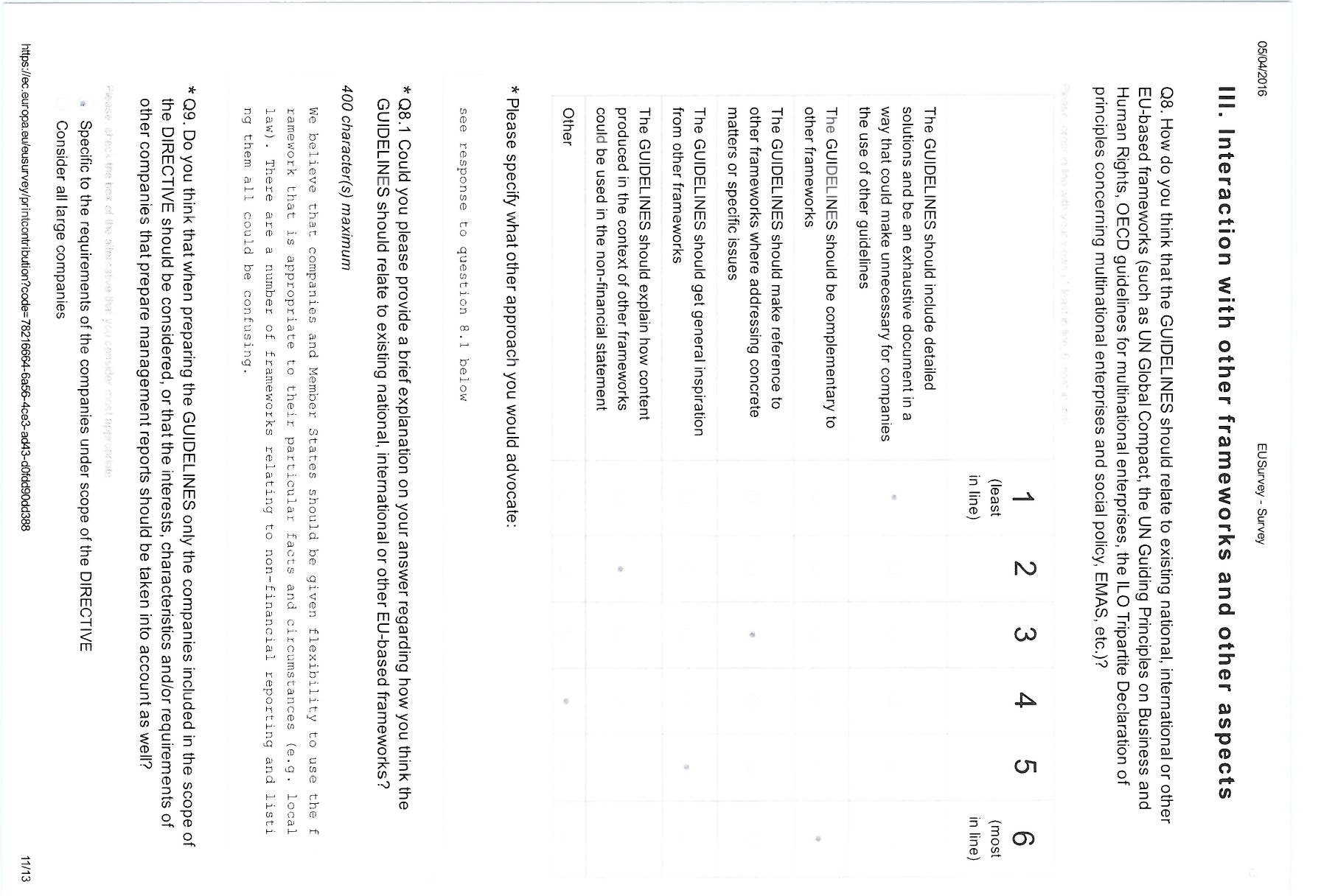

Q8. How do you think that the GUIDELINES should relate to existing national, international or other EU-based frameworks (such as UN Global Compact, the UN Guiding Principles on Business and Human Rights, OECD guidelines for multinational enterprises, the ILO Tripartite Declaration of principles concerning multinational enterprises and social policy, EMAS, etc.)?

Please compare in line with your views (1 least in line, 6 most in line)

- The GUIDELINES should include detailed solutions and be an exhaustive document in a way that could make unnecessary for companies the use of other guidelines

- The GUIDELINES should be complementary to other frameworks

- The GUIDELINES should make reference to other frameworks where addressing concrete matters or specific issues

- The GUIDELINES should get general inspiration from other frameworks

- The GUIDELINES should explain how content produced in the context of other frameworks could be used in the non-financial statement

-

Other

-

Please specify what other approach you would advocate:

see response to question 8.1 below

- Q8.1 Could you please provide a brief explanation on your answer regarding how you think the GUIDELINES should relate to existing national, international or other EU-based frameworks? 400 character(s) maximum

We believe that companies and Member States should be given flexibility to use the framework that is appropriate to their particular facts and circumstances (e.g. local law). There are a number of frameworks relating to non-financial reporting and listing them all could be confusing.

- Q9. Do you think that when preparing the GUIDELINES only the companies included in the scope of the DIRECTIVE should be considered, or that the interests, characteristics and/or requirements of other companies that prepare management reports should be taken into account as well?

Please, check the box of the alternative that you consider most appropriate

- Specific to the requirements of the companies under scope of the DIRECTIVE

- Consider all large companies

- Consider all companies

-

Focus on the requirements of the companies under the scope of the DIRECTIVE, but also propose best practice for other companies that prepare management reports

-

Q9.1 Accordingly, do you think that the content of the guidelines should be different according to the targeted companies? Could you please provide a brief explanation? 400 character(s) maximum

In our view the content of the guidelines should be similar for all companies but the guidance should be clearly differentiate between mandatory requirements in the Directive and non-mandatory guidance.

Q10. Does your company disclose annually relevant non-financial information?

Please, check the box of the alternative that you consider most appropriate

- Yes

- No

- Don't know / no opinion / not relevant

If your company does disclose annually relevant non-financial information, does it use any existing reporting framework(s)?

Please check the box of the alternative that you consider most appropriate.

- Yes

- No

- Don't know / no opinion / not relevant

If your company does use any existing reporting framework(s), could you please indicate which one(s)? 100 character(s) maximum

IV. Disclosures related to board diversity policy

- Q11. Should the GUIDELINES provide more clarity on what companies should disclose as regards their board diversity?

Please check the box of the alternative that you consider most appropriate

- Yes

- No

- Don't know / no opinion / not relevant

- Q11.1 Could you please provide a brief explanation on your answer regarding whether the GUIDELINES should provide more clarity on what companies should disclose as regards their board diversity policy? 400 character(s) maximum

We consider that the guidelines should cover the full content of the Directive and encourage companies to include a brief description of the boards policy on diversity. See UK Corporate Governance Code for further information.

3. Additional information

Please, upload, as needed, any relevant document or information that you consider useful for the purposes of this consultation.

In doing so, you are invited to take into account the content of recital 7 of the DIRECTIVE:

"Where undertakings are required to prepare a non-financial statement, that statement should contain, as regards environmental matters, details of the current and foreseeable impacts of the undertaking's operations on the environment, and, as appropriate, on health and safety, the use of renewable and/or non-renewable energy, greenhouse gas emissions, water use and air pollution. As regards social and employee-related matters, the information provided in the statement may concern the actions taken to ensure gender equality, implementation of fundamental conventions of the International Labour Organisation, working conditions, social dialogue, respect for the right of workers to be informed and consulted, respect for trade union rights, health and safety at work and the dialogue with local communities, and/or the actions taken to ensure the protection and the development of those communities. With regard to human rights, anti-corruption and bribery, the non-financial statement could include information on the prevention of human rights abuses and/or on instruments in place to fight corruption and bribery".

20160404_-_Response_to_EC_consultation_Final.pdf Guidance-on-the-Strategic-Report.pdf

Useful links

- Consultation details (http://ec.europa.eu/finance/consultations/2016/non-financial-reporting-guidelines/index_en.htm)

- Consultation document (http://ec.europa.eu/finance/consultations/2016/non-financial-reporting-guidelines/docs/consultation-document_en.pdf)

- Specific privacy statement (http://ec.europa.eu/finance/consultations/2016/non-financial-reporting-guidelines/docs/privacy-statement_en.pdf)

- More on the Transparency register (http://ec.europa.eu/transparencyregister/public/homePage.do?locale=en)

Contact

-

A copy of the FRC's Guidance is available at https://www.frc.org.uk/Our-Work/Codes-Standards/Accounting-and-Reporting-Policy/Clear-and-Concise-Reporting/Narrative-Reporting/Guidance-on-the-Strategic-Report.aspx ↩